Design-To-Source Intelligence Market Size, Share & Industry Analysis, By Deployment (Cloud-based and On-premises), By Enterprise Type (Large Enterprises and Small and Medium Sized Enterprises (SMEs)), By Application (Product Data Intelligence (PDI), Design Optimization, Sourcing & Procurement Intelligence, Supply Chain Risk Management, and Cost & Compliance Management), By Industry Vertical (Electronics & Semiconductors, Automotive & Mobility, Aerospace & Defence, Industrial Equipment, Medical Devices & IoT, and Others (Telecommunication, etc.)), and Regional Forecast, 2026-2034

DESIGN-TO-SOURCE INTELLIGENCE MARKET SIZE AND FUTURE OUTLOOK

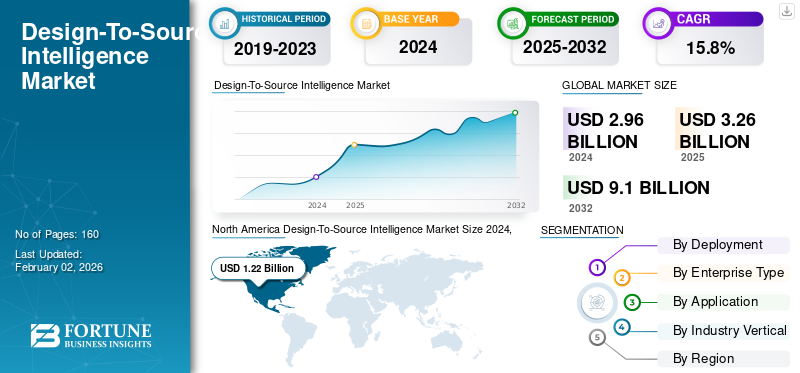

The global design-to-source intelligence market size was valued at USD 3.26 billion in 2025. The market is projected to grow from USD 3.64 billion in 2026 to USD 11.71 billion by 2034, exhibiting a CAGR of 15.74% during the forecast period. North America dominated the design-to-source intelligence market with a market share of 40.99% in 2025.

Design-to-Source Intelligence (DSI) refers to an integrated approach of embedding sourcing and supply chain insights into product design at an early stage to allow manufacturers to optimize decisions from the start. Using data analytics and data-driven processes, DSI provides cost efficiency, quicker innovation cycles, as well as stronger design robustness while addressing obsolescence and component shortages, and more lifecycles.

The growth of the market is driven by a massive increase in online data, a focus on real-time cybersecurity and threat detection, and adoption of AI and automation to facilitate better decision making at scale. Another driver of demand in the market is the growing incidence of software that works on subscription-based models. Digitalization in government and corporate spaces and demand for risk assessment and regulatory compliance, will also drive the market demand.

The leading firms are Supplyframe, Luminovo Gmbh, JAGGAER, Ivalua, Source Intelligence, and HCL Technologies Limited.

Download Free sample to learn more about this report.

Global Design-To-Source Intelligence Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.26 billion

- 2026 Market Size: USD 3.64 billion

- 2034 Forecast Market Size: USD 11.71 billion

- CAGR: 15.74% from 2026–2034

- North America dominated the design-to-source intelligence market with a 40.99% share in 2025.

- The cloud-based segment is projected to dominate the market with a 62.61% share in 2026.

- The large enterprises segment is projected to dominate the market with a 62.23% share in 2026.

North America

The market was valued at USD 1.34 billion in 2025 and is projected to reach USD 1.49 billion in 2026.

Europe

The market was valued at USD 0.91 billion in 2025 and is projected to reach USD 1.01 billion in 2026.

Asia Pacific

The market was valued at USD 0.82 billion in 2025 and is expected to reach USD 0.93 billion in 2026.

U.S.

The market is expected to reach USD 1.11 billion in 2026.

Japan

The market is valued at USD 0.12 billion in 2026.

Read More

Impact of AI

AI-driven Intelligence Accelerates Product Development and Strengthens Supply Chain Resilience

The global design-to-source intelligence market is evolving at a rapid pace, with AI making it possible to make decisions throughout the lifecycle of product development. AI minimizes uncertainties in the supply chain by predicting with high accuracy the availability of components, lead times, as well as possible supplier risks, thus speeding up the design cycles. The technology also enables proactive sourcing options by identifying cost-effective and credible components at an early stage of the design. This reduces the development cycle and also improves the general quality and reliability of the product. As a result, the manufacturers have the opportunity to react more quickly to the changes in the market and remain more resilient and competitive in the global supply chains.

MARKET DYNAMICS

Market Drivers

Growing Complexity of Product Designs and Component Ecosystems Drives Market Growth

The increasing complexity of contemporary product design and the broadening scope of electronic parts are key stimuli of the design-to-source intelligence market growth. Modern, sophisticated products are based on thousands of components supplied by various suppliers worldwide, and procurement strategies have become more complex and prone to interference. Problems such as component shortage, obsolescence, and single-source risks increase risks and operation expenses. Therefore, the companies are resorting to AI-driven intelligent sourcing to handle part lifecycle, supplier reliability, and forecast bottlenecks. These features make complex design ecosystems easy to use and enhance the quality of decisions, and shorten the product development cycle.

Market Restraints

Fragmented Supplier Ecosystems and Inconsistent Data Quality Across Regions Hinder Growth

Although it is experiencing a significant development rate, the design-to-source intelligence market faces significant issues with disconnected supplier ecosystems and poor data quality. Supplier networks come in a myriad of different forms, and what is common in fact that they do not have a standardized way of sharing and updating information. Such a lack of consistency presents predictive sourcing models as inaccurate and decreases the level of trust in decisions made based on analytics. Furthermore, the sourcing strategies at scale are challenging to optimize in case of incomplete or old supplier and component data. To overcome such challenges, it is necessary to have increased transparency, data structures, and collaborative platforms where reliable and high-quality information is assured worldwide across supply chains.

Market Opportunities

Integration with Upstream Design Workflows Drive Growth, Creating Opportunities

There are considerable growth prospects in employing design-to-source intelligence solutions in direct upstream design and engineering processes. By integrating sourcing insights at an early design stage, the team will be able to make better decisions regarding the choice of components and suppliers, as well as risks in the product lifecycle. This integration enables the cross functional work, reduces expensive redesigns, and shortens time to market. Allowing design engineers and procurement teams to operate on the same platform of intelligence can help companies better control costs, enhance product performance and differentiate effectively. This harmonized design/sourcing is a major competitive edge as digital transformation nears completion.

DESIGN-TO-SOURCE INTELLIGENCE MARKET TRENDS

Increased Integration of AI/ML-Driven Analytics Emerges as a Major Market Trend

One of the biggest trends that has influenced the design-to-source intelligence market is the increased use of AI and machine learning-based analytics. Companies are also integrating these technologies in design and procurement processes, to create predictive information on component supply, pricing patterns and possible disruptions. These sophisticated systems constantly acquire experience throughout history and real time data, which enables automated suggestions during part selection and the sourcing strategies. With the maturity of AI algorithms, they are more precise in determining the lead time and risks, enabling more intelligent and agile product development. This direction is redesigning sourcing efficiency and resilience in industries.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Deployment

Lower Upfront Infrastructure Cost Boosts Cloud-Based Segment Growth

Based on the deployment, the market is segmented into cloud-based and on-premises.

The cloud-based segment is projecteed to dominate the market with a share of 62.61% in 2026. The segment dominates as it enables rapid scalability, lower upfront infrastructure cost, and support real‑time collaboration between design and sourcing teams.

Of all the segments, cloud-based hold the highest CAGR of 18.2% in the global market. The segment is growing fastest as firms shift away from on‑premises systems toward flexible, subscription‑based sourcing intelligence solutions

By Enterprise Type

Large Enterprises Segment Dominates Market Owing to Its Global Sourcing Operations

Based on enterprise type, the market is divided into large enterprises and Small and Medium Sized Enterprises (SMEs).

Large enterprises segment is projecteed to dominate the market with a share of 62.23% in 2026. The segment continues to generate the major revenue due to its strong budgets, global sourcing operations and need for advanced DSI platforms.

Small and medium sized enterprises hold the highest CAGR of 19.0% in the global market. The segment’s growth is driven by increased availability of affordable, cloud‑native intelligence tools that allow smaller firms to embed sourcing insights earlier in the design process.

By Application

Cost Visibility Augments the Sourcing and Procurement Intelligence Segment Growth

Based on the application, the market is divided into Product Data Intelligence (PDI), design optimization, sourcing & procurement intelligence, supply chain risk management, and cost & compliance management.

Sourcing and procurement intelligence segment is projecteed to dominate the market with a share of 43.65% in 2026. The growth is due to the immediate value derived from design‑to‑source capabilities such as cost visibility, supplier risk assessment and component availability within procurement workflows.

The segment also represents the largest CAGR at 17.2% in the global market. This application records the highest growth as organizations increasingly recognize the importance of embedding sourcing intelligence early in the design phase to minimize redesign, cost and lead‑time risks.

By Industry Vertical

Rapid Obsolescence and Global Supply‑Chain Risk Augments the Electronics & Semiconductors Segment Growth

Based on the industry vertical, the market is divided into electronics & semiconductors, automotive & mobility, aerospace & defence, industrial equipment, medical devices & IoT, and others (telecommunication, etc.).

The electronics & semiconductors segment is projecteed to dominate the market with a share of 30.42% in 2026. The growth is due to rising complexity of components, rapid obsolescence and global supply‑chain risk which intensify the need for design‑to‑source intelligence.

Of all the segments, medical devices hold the highest CAGR of 20.5% in the global market. The segment exhibits the highest growth rates as they demand embedded intelligence, regulatory compliance and flexible sourcing models, driving uptake of design‑to‑source tools.

To know how our report can help streamline your business, Speak to Analyst

DESIGN-TO-SOURCE INTELLIGENCE MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America recorded a market size of USD 1.34 Billion in 2025, capturing 40.99% of the global market share, and is projected to reach USD 1.49 Billion in 2026. This growth is due to high technology adoption, established supply‑chain intelligence ecosystems and strong investment in sourcing/design tools

The U.S. is at the forefront of the North American market, with expected revenue of USD 1.11 billion in 2026. Growth in the market is driven by increasing cybersecurity threats, strong government and military funding, and the proliferation of digital data from online sources.

North America Design-To-Source Intelligence Market Size 2025,(USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

In 2025, Europe represented USD 0.91 Billion, accounting for 28.02% of the worldwide market, and is projected to grow to USD 1.01 Billion in 2026. This growth is due to increased security and defense investments, EU regulatory frameworks that mandate better data handling, and the strong growth of social media intelligence (SOCMINT).

The U.K. market is valued at USD 0.13 billion by 2026, while the Germany market is valued at USD 0.19 billion by 2026.

Asia Pacific

The Asia Pacific market generated USD 0.82 Billion in 2025, representing 25.19% of the global market landscape, and is expected to reach USD 0.93 Billion in 2026. The growth is due to expansion of the manufacturing base, increasing supply‑chain complexity and adoption of advanced DSI solutions across firms.

The Japan market is valued at USD 0.12 billion by 2026, the China market is valued at USD 0.30 billion by 2026, and the India market is valued at USD 0.11 billion by 2026.

South America and Middle East & Africa

Middle East & Africa accounted for USD 0.15 Billion in 2025, representing 4.55% of the global market share, and is projected to reach USD 0.17 Billion in 2026. due to increased adoption of AI and IoT technologies, government initiatives to promote digital infrastructure and smart cities, and the need for advanced solutions in sectors like manufacturing, finance, and healthcare.

GCC countries are predicted to have a market share of USD 0.05 billion by 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players to Develop User-Friendly Intelligence Systems to Remain Competitive

The key players in the industry include Supplyframe, Luminovo Gmbh, JAGGAER, Ivalua, Source Intelligence, and HCL Technologies Limited. Key players leverage strategies such as building comprehensive platforms, fostering user-friendly intelligence systems, and employing a structured, multi-step OSINT framework for data collection, analysis, and reporting. These companies use a variety of methods such as public data aggregation, advanced analytics, and cross-functional teams to gather actionable insights and inform strategic decisions.

LIST OF KEY DESIGN-TO-SOURCE INTELLIGENCE COMPANIES PROFILED

- Supplyframe (U.S.)

- Luminovo Gmbh (Germany)

- JAGGAER (U.S.)

- Ivalua (France)

- Source Intelligence (U.S.)

- HCL Technologies Limited (India)

- Zensar Technologies (India)

- EDITED (U.K.)

- ITMAGINATION (Poland)

- Linagora (France)

- SPEC India (India)

- TradeGood (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025- Qualcomm Technologies, Inc. launched the Qualcomm Dragonwing™ IQ-X Series, offering next-generation industrial-grade processors engineered for PLCs, advanced HMIs, edge controllers, panel PCs and box PCs.

- February 2024- Supplyframe announced a major new release of its Design-to-Source Intelligence (DSI) Solutions. This release includes a number of first-of-its-kind capabilities to empower electronics design engineers, product leaders, and supply chain professionals with AI Insights, contextual market intelligence that identifies potential risk factors for commodities in their bill of materials (BOMs).

- June 2023- Siemens Digital Industries Software announced that it is integrating the Supplyframe™ Design-to-Source Intelligence platform with its Siemens Xcelerator portfolio of software and services to bring robust real-time supply chain intelligence to the world’s most comprehensive digital twin technology.

- November 2022- Supplyframe announced that Molex, a leading provider of electronic connectors and components, deployed Supplyframe’s innovative Design-to-Source Intelligence suite to enhance its existing business and new product development supplier interaction with a single digital platform. Through this partnership, Molex will use Supplyframe’s NPI and DirectSource solutions to bring both electronic and non-electronic commodities spend under management, increase operational efficiency, and accelerate quoting processes.

- January 2021- Digi-Key Electronics, which offers the world's largest selection of electronic components in stock for immediate shipment, launched a new video series focused on smart agriculture, sponsored by Supplyframe and Amphenol RF. The video series, titled "Farm Different" is a three-part series focused on the people, technology and challenges of modern agriculture.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the design-to-source intelligence market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attribute | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 15.74% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment, Enterprise Type, Application, Industry Vertical, and Region |

| By Deployment |

|

| By Enterprise Type |

|

| By Application |

|

| By Industry Vertical |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 3.64 billion in 2026 and is projected to reach USD 11.71 billion by 2034

The market is expected to exhibit steady growth at a CAGR of 15.74% during the forecast period.

Growing complexity of product designs and component ecosystems is speeding up the market growth

Supplyframe, Luminovo Gmbh, JAGGAER, Ivalua, Source Intelligence, and HCL Technologies Limited are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 1.34 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us