Disinfectants Market Size, Share & Industry Analysis, By Type (Chlorine-based, Quaternary Ammonium Compounds, Alcohol-based, and Others), By End-use (Healthcare, Institutional & Commercial, Industrial, Residential, and Others), and Regional Forecast, 2026-2034

Disinfectants Market Size and Future Outlook

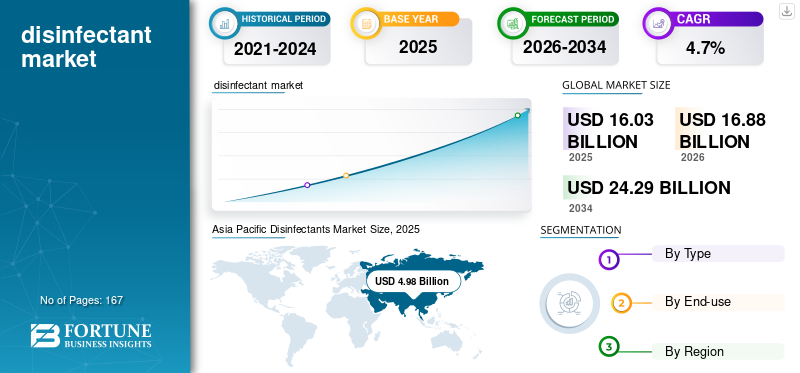

The global disinfectants market size was valued at USD 16.03 billion in 2025. The market is projected to grow from USD 16.88 billion in 2026 to USD 24.29 billion by 2034, growing at a CAGR of 4.7% during the forecast period. Asia Pacific dominated the disinfectants market with a market share of 31.06% in 2025.

Disinfectants are antimicrobial formulations applied to inanimate surfaces, instruments, equipment, and environmental contact points to inactivate or eliminate bacteria, fungi, and viruses. The efficacy of products increasingly relies on the antimicrobial active system, pathogen claims, contact duration, material compatibility, and regulatory approval. The Environmental Protection Agency (EPA) characterizes disinfectants as products that destroy or irreversibly inactivate microorganisms on hard surfaces, whereas the World Health Organization (WHO) continues to emphasize the importance of infection prevention across various care environments.

A primary driver of product demand is the persistent requirement for infection prevention across hospitals, clinics, laboratories, public facilities, institutional & commercial-service environments, and households. The World Health Organization (WHO) reports that healthcare-associated infections are among the most common adverse events in healthcare delivery, with approximately 7 per 100 patients in high-income countries and 15 per 100 in low- and middle-income countries acquiring at least one healthcare-associated infection (HAI) during acute-care stays. WHO also emphasizes that many of these infections are preventable through enhanced infection prevention and control measures. The Centers for Disease Control and Prevention (CDC)’s latest report on HAI progress further demonstrates that healthcare systems continue to monitor and invest in infection control initiatives across both acute and long-term care environments. These circumstances underpin the sustained long-term demand for disinfectants in the healthcare sector, particularly in healthcare facilities such as hospitals and clinics, and in settings with high patient turnover or frequent surgical procedures.

The market is predominantly led by major corporations such as Reckitt, The Clorox Company, Ecolab Inc., STERIS plc, and Solenis. These companies are supported by extensive product portfolios, regulatory approvals, robust distribution networks, and well-established positions within consumer, professional, and healthcare channels. Ecolab positions itself as a provider of water, hygiene, and infection-prevention solutions, with approximately USD 16 billion in annual revenue. Meanwhile, STERIS emphasizes infection prevention as the core of its healthcare and life sciences offerings. Reckitt continues to expand the Dettol brand through innovation and Clorox maintains a significant presence in both consumer and professional cleaning and disinfecting markets.

Download Free sample to learn more about this report.

DISINFECTANTS MARKET TRENDS

Shift toward Faster, Safer, and Sustainability-Led Formulations is a Significant Market Trend

A significant trend in the market is the move from conventional broad-use chemistries toward faster-contact, lower-residue, and more material-compatible solutions. Buyers increasingly prefer hydrogen peroxide, accelerated peroxide, citric acid, and other eco-friendly, non-toxic disinfectant platforms that deliver strong efficacy without the odor, residue, or handling burden often associated with older formulations. This is especially visible in healthcare and institutional settings, where staff safety, turnaround time, and compatibility with high-touch equipment matter alongside pathogen-kill claims. Company launches from Ecolab, Diversey, CloroxPro, and LANXESS all reflect this transition toward performance plus sustainability.

This trend is also reinforced by regulatory transparency and evidence-based product selection. EPA continues to maintain searchable lists of disinfectants for pathogens such as SARS-CoV-2 and provides updated guidance on the use of EPA-registered antimicrobial products. The increase in the U.S. Environmental Protection Agency (EPA) focus on searchable registration tools, emerging viral pathogen claims, and safe-use guidance is making end users more cautious of label-backed efficacy, active chemistry, and use-case fit. As a result, selection is shifting away from purely price-led purchasing toward claim-backed, application-specific products, particularly in advance healthcare environments, institutional & commercial contact-adjacent spaces, and premium institutional cleaning programs.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Infection-Control Standards across Healthcare and Public Environments to Accelerate Product Adoption

The most important growth driver is the continued need to reduce pathogen transmission in care, public, and shared environments. The incidence of healthcare-associated infections (HAIs) remains a powerful driver for disinfectants market growth. The WHO reports that HAIs affect patients and health systems every day and are a major driver of antimicrobial resistance, while CDC continues to track infection outcomes across hospitals and long-term care settings. This keeps disinfection spending embedded in operating protocols rather than purely discretionary maintenance budgets.

The strongest effect is visible in hospitals and clinics, ambulatory centers, diagnostic labs, and other healthcare facilities where environmental hygiene directly influences patient safety, accreditation, and workflow. Growth in hospital admissions, aging populations, rising procedure volumes, and the increasing complexity of reusable devices all support higher usage intensity. In practice, the demand expands with the number of beds or facilities, more frequent room turnover, stricter protocols for high-touch surfaces, and rising disinfection loads around surgical procedures, endoscopy, and critical care. STERIS, Ecolab, and Diversey all position their offerings around these exact infection-prevention needs.

A second growth layer stems from commercial and residential hygiene habits that remain stronger than before the pandemic. This supports the ongoing demand for antiseptics and disinfectants in workplaces, schools, hospitality, transit, and homes. Reckitt’s Dettol and Clorox’s cleaning and disinfecting portfolios continue to reflect this combination of institutional and growing consumer demand, particularly where convenience, trusted brands, and visible germ-protection claims matter.

MARKET RESTRAINTS

Regulatory Compliance, Surface Compatibility, and Chemistry Restrictions to Limit Industry Expansion

Although the product demand is robust, the market faces significant constraints due to regulatory and application-specific compliance requirements. Disinfectants must meet local registration rules, label language requirements, efficacy testing expectations, and safety requirements before they can be marketed for specific pathogens or settings. EPA’s disinfectant framework emphasizes proper registration, pathogen-specific lists, and use instructions, which raises the documentation burden for suppliers and can slow entry for smaller manufacturers or new chemistries. In healthcare and institutional & commercial settings, the tolerance for compliance gaps is especially low.

The product substitution is also challenging. Surface type, material sensitivity, soil load, contact time, residue, ventilation needs, and worker handling all influence what can realistically be used. For example, strong oxidizers or chlorine-based disinfectants may offer broad-spectrum efficacy but can cause compatibility issues with certain metals, electronics, or coated surfaces. Meanwhile, some high-level disinfection applications require validated processes and dedicated test methods, which reduces flexibility in procurement. STERIS and Ecolab product materials show how healthcare users increasingly select among peroxide, peracetic acid, quaternary ammonium, or other systems based on use case rather than price alone.

These factors can slow market growth in cost-sensitive environments, especially where distributors or facility operators want to rationalize SKUs quickly. Even when a novel product offers greener positioning, a switch may be delayed until the buyer confirms efficacy claims, user training, dispenser compatibility, and local regulatory acceptance. Driven by this aspect, the market still has room for both legacy and newer chemistries to coexist.

MARKET OPPORTUNITIES

Premium Healthcare Hygiene and Peroxide and Plant-based Innovation to Drive White-Space Expansion

A major opportunity lies in faster-acting, safer, and premium-positioned products built around hydrogen peroxide, peracetic acid, citric acid, and other next-generation actives. These chemistries align well with the customer demand for shorter contact times, broad-spectrum efficacy, improved user experience, and better sustainability narratives. Ecolab’s plastic-free hospital wipe, Diversey’s Oxivir expansion, and CloroxPro’s EcoClean wipes all point toward the same market direction. Buyers increasingly reward products that combine disinfection efficacy with softer environmental and material-compatibility profiles.

Healthcare remains the most attractive premium opportunity. As providers seek to improve room turnover, infection scores, staff productivity, and patient confidence, there is a greater opportunity for differentiated disinfection systems rather than commodity-only purchasing. This includes wipes, RTU sprays, concentrated formats, high-level disinfectants, and integrated hygiene programs bundled with training and monitoring. In that context, the healthcare-facing segment is expected to grow faster than several mature institutional applications, driven by advanced healthcare standards, the need for device reprocessing, and increasing complexity in outpatient and procedural settings.

Another visible opportunity is plant-based or naturally derived innovation in consumer hygiene. Reckitt’s Dettol innovation in China shows that the market can create new pockets of demand when companies simplify ingredients without losing their trusted efficacy positioning. This matters as the next phase of premiumization is less about emergency buying and more about consumers paying for convenience, gentler profiles, and brand assurance.

MARKET CHALLENGES

Price Competition, Demand Normalization, and Balancing Efficacy with User Acceptance Continue to Pressure Suppliers

One of the biggest challenges is that the market is no longer supported by one-time pandemic buying patterns. Many categories now compete in a more normalized demand environment, putting pressure on pricing, promotion, and product differentiation. Suppliers have to prove not only germ-kill performance but also better usability, lower residue, faster turnaround, and sustainability advantages. This is especially hard in large-volume commercial channels where procurement teams compare many technically acceptable products.

There is also an ongoing challenge in balancing broad efficacy with practical everyday use. A disinfectant may perform extremely well under test conditions, but adoption can weaken if the odor is too strong, if contact times are too long, or if the chemistry damages surfaces and equipment. In professional environments, labor availability and compliance are equally important. A product that is theoretically strong but operationally inconvenient may lose share to a more user-friendly alternative. This is why suppliers continue to invest in one-step cleaners, wipes, RTU systems, and dispensing innovations rather than only stronger chemistry.

Finally, the market remains exposed to raw-material volatility and packaging costs. Chlorine derivatives, surfactants, solvents, wipes, substrates, and specialty packaging can all affect margins, particularly in markets with strong private-label competition. Larger branded and professional players are better positioned as they can spread regulatory, manufacturing, and sales costs across broader portfolios, but smaller firms may find it difficult to achieve economies of scale. This dynamic keeps the market moderately consolidated in premium segments while more fragmented in value tiers.

Segmentation Analysis

By Type

High Demand for Quaternary Ammonium Compounds to Bolster Segmental Growth

Based on type, the market is segmented into chlorine-based, quaternary ammonium compounds, alcohol-based, and others.

The quaternary ammonium compounds segment accounted for the largest disinfectants market share in 2025, owing to its extensive use in hospitals, commercial buildings, institutional & commercial-service back-of-house environments, and general institutional cleaning. Quat systems remain widely accepted due to their effectiveness on numerous hard surfaces, relative ease of formulation into wipes and concentrates, and familiarity among cleaning personnel. They continue to maintain a substantial installed base in routine environmental disinfection and are prominently featured on EPA-registered product lists. Furthermore, this segment is projected to exhibit a CAGR of 4.7% throughout the analysis period.

Chlorine-based disinfectants remain significant in high-risk sanitation, outbreak response, and cost-constrained applications owing to their cost-effectiveness and ability to eliminate pathogens. Nevertheless, expansion in this sector remains relatively modest due to issues such as odor emissions, corrosion potential, handling challenges, and the growing interest in cleaner-label and user-friendly formulations. Moreover, it is anticipated that this segment will experience a CAGR of 3.5% throughout the forecast period.

By End-use

To know how our report can help streamline your business, Speak to Analyst

Healthcare Segment to Depict the Fastest CAGR with Surging Hygiene Standards

In terms of end-use, the market is categorized into healthcare, institutional & commercial, industrial, residential, and others.

The healthcare segment is the fastest-growing segment during the forecast period, supported by rising hygiene standards, more frequent environmental cleaning, increased procedural throughput, and the persistent burden of HAIs. This includes acute-care hospitals, ambulatory surgical centers, diagnostic labs, long-term care, and specialty clinics. WHO and CDC data continue to support sustained investment in infection control, while suppliers such as STERIS, Ecolab, and Diversey are positioning themselves directly around hospitals and clinics, device reprocessing, and environmental hygiene workflows. Moreover, this segment is projected to grow at a CAGR of 5.3% over the forecast period.

The industrial segment is likely to grow significantly during the forecast period. This growth is supported by the need to maintain hygienic operating conditions across manufacturing plants, warehouses, utilities, cleanrooms, laboratories, and equipment-intensive production environments. Industrial users rely on disinfectants to reduce microbial contamination on work surfaces, processing areas, tools, and shared-touch infrastructure, particularly in sectors where contamination control, worker safety, and process reliability are critical. The product demand is especially strong in facilities linked with electronics, pharmaceuticals, chemicals, packaging, and other controlled production settings where sanitation protocols are integrated into routine operations. Furthermore, this segment is projected to grow at a CAGR of 4.9% during the analysis period.

The residential segment remains a significant demand center as trusted disinfection brands maintain a strong shelf presence, and household hygiene awareness remains above pre-pandemic levels. The category benefits from convenient formats such as wipes, sprays, and small packs, as well as brand-led innovation. Reckitt’s Dettol developments and Clorox’s continued strength in consumer cleaning show how home disinfection remains structurally relevant even as buying becomes less emergency-driven and more usage-based.

Disinfectants Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Disinfectants Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the largest market share at a value of USD 4.71 billion and maintained its leadership in 2025, with a value of USD 4.98 billion. The regional market is projected to maintain its dominance throughout the forecast period. The substantial demand in the region originates from its extensive population, dense healthcare infrastructure, rapid urbanization, expanding institutional & commercial service and public infrastructure sectors, as well as high household hygiene consumption. Furthermore, increased expenditure on hospitals, elder care, and infection prevention across both public and private healthcare systems further bolsters disinfectant usage in the healthcare and residential sectors.

China Disinfectants Market

By 2026, the Chinese market is projected to attain a valuation of USD 2.38 billion. China is the largest market in the Asia Pacific, supported by its hospital scale, urban household consumption, institutional cleaning demand, and broad distribution of domestic and multinational hygiene brands. The product demand is also supported by a stronger interest in premium and plant-based hygiene solutions, as seen in Reckitt’s Dettol innovation in China. The regional market growth is increasingly linked to branded, convenience-led, and family-safe formats rather than only low-cost commodity products.

To know how our report can help streamline your business, Speak to Analyst

Japan Disinfectants Market

The Japan market is estimated to be around USD 0.75 billion in 2026, accounting for roughly 4.4% of the global revenues.

India Disinfectants Market

The India market is estimated to touch a value of around USD 0.64 billion in 2026, accounting for roughly 3.8% of the global revenues.

Europe

Europe is expected to experience substantial market growth and is projected to grow at a CAGR of 3.5% over the forecast period. This market is likely to reach a valuation of USD 4.04 billion by 2026. The market is supported by stringent hygiene practices, hospital protocols, institutional & commercial-processing sanitation requirements, and rising demand for safer and more sustainable chemical systems. Europe is also favorable for peroxide-led and specialty high-level disinfection solutions as buyers pay closer attention to safety, residue, and environmental impact.

U.K. Disinfectants Market

The U.K. market is estimated to reach a value of around USD 0.74 billion in 2026, accounting for roughly 4.4% of the global revenues.

Germany Disinfectants Market

The Germany market is estimated to touch a valuation of around USD 0.98 billion in 2026, accounting for roughly 5.8% of the global revenues.

North America

The region benefits from high usage intensity in hospitals, outpatient care, long-term care, schools, offices, and institutional & commercial service. It also has a mature regulatory environment, advanced professional hygiene channels, and strong branded consumer participation. EPA registration visibility, CDC infection surveillance, and sustained innovation from Clorox, Ecolab, GOJO, and STERIS all support premiumization in the region.

U.S. Disinfectants Market

Given the U.S. dominance in the region, the U.S. market is estimated to reach around USD 4.85 billion in 2026, accounting for roughly 28.7% of the global sales.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are comparatively smaller markets but continue to expand as healthcare access, institutional hygiene standards, tourism infrastructure, and institutional & commercial-service sanitation improve. The market growth is moderate but structurally positive, particularly in urban centers, private healthcare, and premium imported brands. The need for practical, cost-effective, and broad-spectrum products remains high in these regions. The Latin America market is projected to reach USD 1.18 billion by 2026.

GCC Disinfectants Market

The GCC market is estimated to reach a value of USD 0.39 billion in 2026, accounting for approximately 2.3% of the global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies to Emphasize Regulatory Registrations and Application Engineering to Secure a Competitive Edge

The competitive landscape is moderately consolidated at the premium end and more fragmented in lower-cost regional tiers. Competitive strength depends on regulatory registrations, claim-backed efficacy, application engineering, channel reach, and the ability to serve both professional and consumer demand pools. In premium healthcare and institutional settings, supplier credibility is often built on pathogen-specific claims, training support, dispenser or wipe systems, and consistency across global locations. EPA visibility and infection-prevention positioning, therefore, matter as much as chemistry.

The leading market players include Reckitt, The Clorox Company, Ecolab Inc., STERIS plc, and Solenis. Reckitt and Clorox are strong in household and professional branded disinfection. Ecolab and Diversey are deeply embedded in institutional and healthcare hygiene programs. STERIS is especially strong in infection prevention and high-level disinfection and LANXESS participates through its Rely+On disinfection portfolio and active-ingredient capabilities. Solenis’ acquisition of Diversey has also strengthened the competitive position of integrated hygiene platforms across healthcare and institutional markets.

LIST OF KEY DISINFECTANTS COMPANIES PROFILED

- Reckitt (U.K.)

- The Clorox Company (U.S.)

- Ecolab Inc. (U.S.)

- STERIS plc (Ireland)

- Solenis (U.S.)

- LANXESS AG (Germany)

- GOJO Industries (U.S.)

- Neogen Corporation (U.S.)

- Spartan Chemical Company, Inc. (U.S.)

- Metrex (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Clorox completed the acquisition of GOJO Industries, adding the Purell brand and expanding its position in health, hygiene, and institutional end markets.

- November 2025: GOJO launched PURELL Hand Sanitizer Spray, introducing a new spray format intended to extend hand-hygiene usage occasions and refresh the premium portable segment.

- November 2025: GOJO introduced the PURELL CX10 Countermount Dispensing System at the at the 2025 ISSA North America Trade Show, extending its legacy of dispensing innovation. The move supports the broader hygiene and surface-disinfection ecosystem in healthcare, workplace, and commercial settings.

- September 2025: GOJO launched PURELL Clean & Go Wipes, a compact hygiene format for hands, faces, and quick cleanups, reflecting category expansion into convenience-led everyday use.

- September 2024: Diversey, a Solenis company, entered a strategic partnership with Synexis to distribute dry hydrogen peroxide microbial-reduction technology to healthcare customers in the U.S. and Canada.

- August 2024: CloroxPro launched Clorox EcoClean Disinfecting Wipes, a ready-to-use disinfecting wipe made with a 100% plant-based substrate and a citric acid active ingredient. The launch signifies the company’s initiative to tap into the rising demand for eco-friendly and non-toxic disinfectant solutions in institutional and healthcare cleaning.

- May 2024: Diversey launched Oxivir Three 64 for healthcare, while Ecolab launched Disinfectant 1 Wipe, described as the first EPA-registered 100% plastic-free degradable 1-minute hospital disinfection wipe. These launches underscore the shift toward peroxide-led and sustainability-oriented disinfection.

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.7% from 2026-2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, End-use, and Region |

| By Type |

|

| By End-use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 16.03 billion in 2025 and is projected to reach USD 24.29 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 4.7% during the forecast period of 2026-2034.

The healthcare segment is anticipated to expand at the fastest rate over the forecast period.

Asia Pacific held the highest market share in 2025.

Rising infection-control standards across healthcare and public environments are key factors accelerating the market growth.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us