Dietary Supplement Testing Services Market Size, Share & Industry Analysis, By Service Provider (In-house Testing Labs, Contract Research Organizations (CROs), & Independent Third-Party Testing Laboratories), By Test Type (Microbiological Testing, Chemical Analysis, Heavy Metals Testing, Pesticide Residue Analysis, Stability Testing, & Others), By Technology (Traditional Testing and Rapid Testing), By Ingredient Type (Ingredient-Level Testing and Finished Product Testing), By End-User (Manufacturers, Regulatory Bodies, Research Laboratories, and Others), and Regional Forecast, 2026-2034

DIETARY SUPPLEMENT TESTING SERVICES MARKET SIZE AND FUTURE OUTLOOK

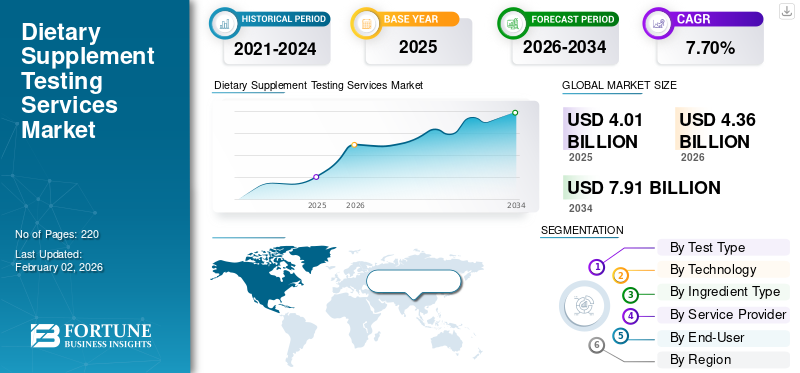

The global dietary supplement testing services market size was valued at USD 4.01 billion in 2025 and is projected to grow from USD 4.36 billion in 2026 to USD 7.91 billion by 2034, exhibiting a CAGR of 7.70% during the forecast period. North America dominated the dietary supplement testing services market with a market share of 35.00% in 2025.

Dietary supplement testing services are specific analytical processes provided by labs to assess the quality, safety, composition, and regulatory ingredient compliance of dietary supplements, such as labeling accuracy verification, contaminant detection, and confirmation of ingredient quality.

The market is quickly expanding as a result of increasing consumer interest in health, demand for preventative healthcare, increasing regulations, advancements in testing technology, and increased online sales avenues for supplements. Collectively, these factors drive the need for new and trustworthy testing services and thus the market.

The main participants within the market include Eurofins Scientific, SGS SA, Intertek Group plc, Bureau Veritas, ALS Limited, and TÜV SÜD.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Growing Need for Safe, Pure, and Effective Supplements Drives Market Expansion

The rising global focus on personal health and wellness has significantly fueled the demand for dietary supplement testing services. Consumers today are more informed and discerning, seeking supplements that are not only effective but also safe, pure, and compliant with health regulations. This shift in consumer expectations compels manufacturers to invest in advanced testing processes to detect contaminants, verify ingredient authenticity, and meet both national and international quality standards. As transparency and trust become vital to brand reputation, thorough testing plays an increasingly central role in ensuring product reliability and driving market growth.

Market Restraints

High Testing Costs Impede the Growth of the Market

High operating costs continue to be a barrier to the dietary supplement industry's adoption of thorough testing procedures, despite their significance. Advanced analytical techniques such as mass spectrometry and chromatography raise testing costs dramatically because they call for specialized equipment and knowledgeable personnel. These expenses may be unaffordable for startups and smaller manufacturers, which would restrict their capacity to conduct numerous testing cycles or satisfy changing regulatory standards. As a result of cost barriers that slow market adoption generally and impede the dietary supplement testing services market growth in cost-sensitive regions, the gap between large corporations and small businesses grows.

Market Opportunities

Expansion Opportunity in Emerging Economies Creates New Market Opportunities

Increasing urbanization, rising disposable incomes, and increasing health literacy are changing the dietary supplement sector in developing markets in Asia, Latin America, and Africa. Consumers in these markets are adopting preventive healthcare practices and consuming nutritional supplements for improved health. The growing consumer demand for dietary supplements has created an urgent need for effective testing and quality assurance programs in order to validate products entering into the online and offline marketplace. Testing service providers can leverage opportunities by working with regional manufacturers, establishing testing facilities in-country, and offering low-cost testing solutions in these quickly emerging economies.

DIETARY SUPPLEMENT TESTING SERVICES MARKET TRENDS

Rising Adoption of Rapid Testing Technologies Boosts the Market Growth

The dietary supplement testing market is being transformed by technological advancements, with a significant shift toward rapid and automated testing methods. Recent technologies, including real-time polymerase chain reaction (PCR), biosensor technologies, and portable analyzers, are making it possible to test for contaminants and authenticity at an accelerated and more accurate pace. Rapid methods aid manufacturers in shortening turnaround times, expediting quality control, and bringing products to market faster, without compromising on accuracy. Rising demand for efficiency has resulted in advanced rapid testing solutions becoming one of main trends across the industry, giving companies that implement rapid, accurate testing solutions a competitive advantage, while increasing consumer trust.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Test Type

Critical Need to Detect Harmful Pathogens Boosts Microbiological Testing Segment Growth

Based on the test type, the market is segmented into microbiological testing, chemical analysis, heavy metals testing, pesticide residue analysis, stability testing, and others (adulteration, etc.).

In 2026, the microbiological testing segment is anticipated to hold the largest revenue share, amounting to USD 1.12 billion in the global market with a share of 6.88% in 2026. The increase in revenue is attributed to the importance of identifying adverse pathogens such as bacteria, yeast, and mold that can impact both product safety and consumer health. Furthermore, the segment’s growth is also owing to various regulatory requirements in the U.S. and the EU that require microbiological testing and compliance with Good Manufacturing Practices (GMP) to ensure the absence of contamination risks in dietary supplements.

Of all the segments, chemical analysis has the highest CAGR of 8.8% in the global market. The growth of the segment is attributable to the increasing complexity of dietary supplement formulations requiring exact identification of active ingredients, contaminants and possible adulterants. Additionally, the increased regulatory emphasis on label accuracy and authenticity testing and the growing demand for more advanced methods of chemical analysis (such as chromatography and spectroscopy) to establish the quality and safety of dietary supplements are also attributed to the growth of the segment.

By Ingredient Type

Ingredient-Level Testing Segment Dominates Market Owing to Established Reliability and Widespread Adoption

Based on ingredient type, the market is divided into ingredient-level testing and finished product testing.

In 2024, the ingredient-level testing segment is accounted for the largest revenue share of USD 1.88 billion in the overall global market. This revenue growth is a result of established dependability and widespread use across the industry in the routine quality control samples for both the raw ingredients and finished supplements. The growth is also supported by regulatory authorities’ favor for validated, conventional testing protocols that ensure compliance with safety and purity standards.

Of all the segments, finished product testing is projected to riched the highest CAGR at 9.4% in the global market with a share of 12.84% in 2026, driven by the increased need for faster turnaround times on product release cycles and efficiency in the supply chain. The growth is also supported by the advancement in portable and high-throughput workgroup technologies which allow manufacturers to test for contaminants and establish ingredient integrity quicker while meeting evolving regulatory changes.

By Service Provider

Strong Demand from Supplement Manufacturers Augments the Independent Third-Party Testing Laboratories Segment Growth

Based on the service provider, the market is divided into in-house testing labs, Contract Research Organizations (CROs), independent third-party testing laboratories, and others.

In 2026, the segment is projected for independent third-party testing laboratories accounted for the largest share with a 13.07% in 2026, of the overall global market revenue, standing at USD 1.91 billion. This revenue growth can be attributed to supplement manufacturers' need for independent, accredited testing to establish consumer trust and meet global regulatory demands. Additionally, there is a growing trend of independent laboratories moving to fill these gaps by providing expertise, advanced testing capabilities, and scalable services, establishing theirs services as the ideal option for compliance and growth in a faster time frame. Rapid testing demonstrates the largest CAGR of 8.7% in the global market.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Proven Accuracy and Long-Standing Regulatory Acceptance Augments the Traditional Testing Segment Growth

Based on the technology, the market is divided into traditional testing and rapid testing.

The traditional testing segment had the largest revenue share of USD 3.20 billion in the overall global market in 2024. The traditional testing segment is anticipated for the largest Share with a 21.10% in 2026. Revenue growth is driven by validated accuracy, long-standing regulatory acceptance, and ongoing use in verifying dietary supplements’ safety and quality. In addition, this segment is still underpinned by the continued reliance of manufacturers and regulators on tested laboratory methodologies that ensure consistency and compliance.

Rapid testing holds the highest CAGR of 10.4% in the global market. The segment’s growth is led by demands from the industry for faster quality assurance to support shorter product launch cycles, and just-in-time manufacturing. The segment is further supported by advancements in rapid microbiological and chemical testing tools that provide owners with faster detectability of contamination, while reducing prices and turnaround time.

By End-User

Investment in Routine Testing Augments the Manufacturers Segment Growth

Based on the end user, the market is divided into manufacturers, regulatory bodies, research laboratories, and others.

The manufacturers segment held the largest revenue share of USD 1.66 billion in the overall global market in the year 2024. The increase in revenue is driven by the regulatory requirement for supplement producers to conduct extensive quality and safety checks before products reach the market. It is also supported by manufacturers’ investment in routine testing to safeguard brand reputation and ensure compliance with GMP and international standards.

Research laboratories holds the highest CAGR of 8.4% in the global market. The segment’s growth is mainly due to the rising demand for advanced analytical studies on supplement efficacy, authenticity, and innovation in formulation. It is also supported by increasing collaborations between academia, private labs, and industry players, which are fueling higher testing volumes and adoption of sophisticated techniques.

DIETARY SUPPLEMENT TESTING SERVICES MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America Dietary Supplement Testing Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North American market is still a leading regional contributor at USD 1.4 billion in 2025 with a projection of USD 1.52 billion in 2026. The leadership is attributable to an expanding dietary supplement sector, strict legal regulations, and high consumer awareness regarding product safety and quality. The region’s growth is also owing to supported by advanced laboratory infrastructure and widespread adoption of testing services by both manufacturers and regulatory bodies. The U.S. leads the North American market leads with approximately USD 1.26 billion in revenue in 2026.

Europe

In 2025, Europe generated USD 1.16 billion, contributing 28.80% to global market revenue, and is projected to grow to USD 1.24 billion in 2026. The dietary supplement testing services market in Europe is expected to reach USD 1.24 billion in 2026, resulting from higher consumer awareness regarding dietary supplements and their health benefits, leading to an increase in demand for safe and effective products. The U.K. leads with USD 0.25 billion, followed by Germany at USD 0.19 billion and France at USD 0.15 billion.

Asia Pacific

At present, the Asia Pacific region dominates the global market. The Asia Pacific market accounted for USD 0.98 billion in 2025, representing 24.40% of the global industry, and is expected to reach USD 1.08 billion in 2026, driven by a flourishing dietary supplement market, elevating disposable incomes, and growing consumer focus on health and wellness. Several factors can be attributed to the government’s continued initiatives to bolster food and supplement safety standards and increased adoption of modern testing technologies across the region.

In addition, Asia Pacific is projected to have the highest CAGR (8.71%) and remain the fastest growing market. The main contributors to growth in the markets are India and China, which project to have revenues of USD 0.16 billion, The Japan market is projected to valued at USD 0.18 billion by 2026, and USD 0.55 billion respectively in 2026.

Middle East & Africa

In 2025, Middle East & Africa represented USD 0.21 billion, accounting for 5.20% of the worldwide market, and is projected to grow to USD 0.22 billion in 2026. The region’s growth is attributable to the higher consumer demand for quality supplements, regulatory compliance, and increased health awareness in the population. GCC countries are predicted to have a dietary supplement testing services market share of USD 0.12 billion by 2025.

South America

In 2025, South America held 6.60% of the global market, reaching a valuation of USD 0.27 billion, and is projected to grow to USD 0.29 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Top Players Adopt Innovative Digital Technologies to Lead the Market

The global market is led by important players such as Eurofins Scientific, SGS SA, Intertek Group plc, Bureau Veritas, ALS Limited, TÜV SÜD and other significant companies. The majority of these companies operate via a widespread global network, use innovative digital technologies such as Building Information Modeling (BIM) and digital twins, regulatory compliance, and engage into strategic partnerships or acquisitions to compete in the marketplace. Other notable companies such as Merieux NutriSciences, NSF International, AsureQuality Limited, and EMSL Analytical, Inc., also emphasize innovation via the cloud-based solutions, acquisitions, and partnerships.

LIST OF KEY DIETARY SUPPLEMENT TESTING SERVICES COMPANIES PROFILED:

- Eurofins Scientific (France)

- SGS SA (Switzerland)

- Intertek Group plc (U.K.)

- Bureau Veritas (France)

- ALS Limited (Australia)

- TÜV SÜD (Germany)

- Covance Inc. (U.S.)

- Merieux NutriSciences (France)

- NSF International (U.S.)

- AsureQuality Limited (New Zealand)

- EMSL Analytical, Inc. (U.S.)

- QIMA (Hong Kong)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: NSF acquired Cambium Analytica, an analytical testing and development company that serves the natural food, beverage and dietary supplement industries. The move gives the global health and safety organization, known primarily for its third-party audits, additional capabilities in areas of the industry driving consumer trends.

- September 2025: Eurofins Food Chemistry Testing, Madison, Wis., and Eurofins Assurance announced the launch of product certification designed to safeguard the quality of dietary supplements, ingredients and food. To minimize risks from adulteration, contamination and other quality issues, product certification plays an important role for these highly regulated products.

- February 2025: Mérieux NutriSciences, a global leader in food safety, quality, and sustainability, announced the completion of its acquisition of Bureau Veritas' food testing activities in Japan, Morocco, Southeast Asia, and South Africa.

- June 2024: RSSL, a food and pharmaceutical contract research organisation, has launched a novel dietary supplement testing service to support clients in the industry to meet regulatory and quality requirements.

- April 2024: Sova Health, positioned as India’s first full-stack gut health company, launched two diagnostic tools—the Gut Microbiome Test (GMT) and the Food Intolerance Test (FIT)—as part of its move towards science-based digestive health management. The company, known for offering custom-based probiotics and personalised gut-balancing solutions, aims to deliver precision interventions through data-driven insights.

- May 2022: Bureau Veritas, a provider of laboratory testing, inspection, and certification services, announced the opening of its third U.S. microbiology laboratory, based in Reno, Nevada. The facility will conduct rapid pathogen testing and microbiology indicator analyses for the agrifood sector. The new laboratory is ISO 17025 accredited, which verifies the facility’s technical proficiency and the accuracy of the data it produces.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the dietary supplements testing services industry trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 7.70% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation |

By Test Type, Technology, Ingredient Type, Service Provider, End-User, and Region |

| By Test Type |

|

| By Technology |

|

| By Ingredient Type |

|

| By Service Provider |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 4.36 billion in 2026 and is projected to reach USD 7.91 billion by 2034.

The market is expected to exhibit steady growth at a CAGR of 7.70% during the forecast period.

The increasing consumer awareness regarding health and wellness is speeding up the market growth.

Eurofins Scientific, SGS SA, Intertek Group plc, Bureau Veritas, ALS Limited, and TÜV SÜD are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 1.4 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us