Digital Publishing Market Size, Share & Industry Analysis, By Publishing Type (eBooks & Digital Books, Digital Journals, Digital Magazines, Digital News Publishing, Learning & Courseware Publishing, and Others), By Format (eBooks, PDF, and Audio Publishing), By Enterprise Type (Large Enterprises and Small & Medium-sized Enterprises), By End-user (Individual Consumers, Students, Educators and Trainers, and Academic and Research Users), and Regional Forecast, 2026-2034

DIGITAL PUBLISHING MARKET SIZE AND FUTURE OUTLOOK

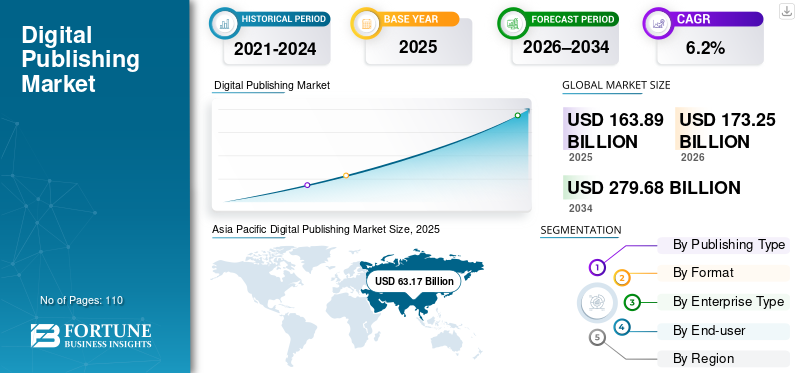

The global digital publishing market size was valued at USD 163.89 billion in 2025. The market is projected to grow from USD 173.25 billion in 2026 to USD 279.68 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the digital publishing market with a market share of 38.54% in 2025.

Digital publishing platforms are content delivery and management systems designed to handle large-scale digital content, making them essential for modern media, education, and corporate knowledge applications. They are widely used for eBooks, digital magazines, news platforms, educational materials, and interactive content, where fast content delivery, personalization, and cross-device compatibility are critical. As organizations and individual users increasingly adopt e-learning, subscription services, and multimedia content, demand for advanced digital publishing platforms continues to rise as they enable seamless access, real-time updates, and scalable content distribution.

Key companies such as Amazon, Inc., Apple. Inc., Alphabet, Inc., and RELX Group are strengthening their positions through platform innovation, partnerships, and strategic investments to expand functionality, efficiency, and user accessibility. These players are focusing on improving cross-device compatibility, cloud-based integration, content personalization, and analytics capabilities to support larger audiences and broaden adoption across individual consumers, educational institutions, and enterprises.

Download Free sample to learn more about this report.

DIGITAL PUBLISHING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 163.89 billion

- 2026 Market Size: USD 173.25 billion

- 2034 Forecast Market Size: USD 279.68 billion

- CAGR: 6.2% (2026–2034)

- Asia Pacific dominated the market with a 38.54% share in 2025.

- Consumer segment is expected to lead with a 37.6% share in 2026.

- eBooks segment is projected to dominate with a 24.5% share in 2026.

Asia Pacific

Asia Pacific valued at USD 63.17 billion in 2025, driven by high smartphone-based digital reading.

North America

North America reached USD 45.85 billion in 2025, supported by strong subscription-based content adoption.

Europe

Europe valued at USD 39.61 billion in 2025, fueled by digital literacy and premium content demand.

U.S.

Market stood at USD 39.65 billion in 2025.

Japan

Market reached USD 9.90 billion in 2025.

Read More

IMPACT OF GENERATIVE AI

Rising Content Demand and Personalization Driving Adoption of Generative AI in Digital Publishing

Generative AI is transforming the digital publishing industry by enabling faster, cheaper, and more scalable content creation. It can automatically produce articles, summaries, e-books, and even multimedia content, helping publishers meet the growing demand for fresh, engaging material. For instance,

- In January 2025, Arc XP, in collaboration with AWS, is using generative AI to streamline journalism for publishers such as “Le Parisien”. The AI automates tasks such as summarization, tagging, translation, and social media posting, letting journalists focus on high-quality reporting.

AI also enables personalization, delivering content tailored to individual reader preferences, which increases engagement, loyalty, and subscription conversions. In addition, AI can generate visuals, infographics, and interactive elements, enhancing the appeal and interactivity of digital publications. It also supports data-driven content strategies by analyzing trends and audience behavior to optimize what is published.

DIGITAL PUBLISHING MARKET TRENDS

Integration of Multimedia and Interactive Features Shaping Market Growth

Digital publishing is moving far beyond just text, with publishers increasingly incorporating multimedia and interactive elements to engage readers more effectively. Videos, podcasts, infographics, animations, and interactive quizzes are now commonly integrated into articles, eBooks, and online magazines. This approach not only makes content more visually appealing but also helps convey complex information in an easy-to-understand way.

Interactive features encourage readers to spend more time on the platform, participate actively, and even share content with others, increasing reach and engagement. Younger audiences, in particular, prefer dynamic, engaging content over plain text, making multimedia integration a key trend for attracting and retaining readers. Publishers who successfully leverage these tools can differentiate themselves from competitors, enhance user experience, and open new revenue streams through premium interactive content or sponsored media.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Internet and Smartphone Penetration Drives Market Growth

The rapid growth of internet access and smartphone adoption is a major driver of the digital publishing market growth. As more people across the globe gain reliable internet connections and own smartphones, tablets, and other smart devices, digital content becomes more accessible to a wider audience. For instance,

- According to DemandSage, globally, around 5.78 billion people use smartphones, accounting for approximately 70% of the world’s 8.25 billion population.

- The ITU estimates that by 2025, around 6 billion people (74% of the global population) will be using the Internet, up from 60% in 2020, meaning 1.3 billion new users came online during this period.

This allows publishers to reach readers anytime and anywhere, eliminating the limitations of traditional print media. Mobile devices, in particular, enable on-the-go reading, instant downloads, and interactive experiences, which greatly enhance user engagement. Additionally, increased connectivity opens opportunities for publishers to expand into emerging markets, where digital media can be more cost-effective and convenient than physical copies. As a result, growing internet and smartphone penetration are accelerating the adoption of digital publications and expanding the market’s overall reach and potential.

MARKET RESTRAINTS

Changing Consumer Preferences Restrain Market Growth

One significant restraint for the market is changing consumer preferences. Modern readers often have shorter attention spans and prefer content that is quick, engaging, and easy to consume. Traditional digital publications, such as long-form articles or eBooks, can struggle to hold readers' attention when free alternatives such as blogs, news snippets, and online articles are widely available. This shift makes it challenging for publishers to retain paying audiences, and those who cannot adapt to new consumption habits risk losing readers and revenue.

Social media platforms such as Instagram Reels, TikTok, and YouTube Shorts have further changed the landscape by offering information and entertainment in very short, visually appealing formats. These platforms make it easier for users to access content instantly, often in just a few seconds, which competes directly with traditional digital publishing. For instance,

- According to DemandSage, around 2 billion people interact with Instagram Reels daily, which receive 200 billion+ views and 22% more engagement than regular videos.

Publishers now face the pressure to create content that is not only informative but also concise, interactive, and shareable to capture attention in this fast-paced environment.

MARKET OPPORTUNITIES

Rising Demand for E-Learning and Educational Content to Boost Market Growth

The demand for e-learning and online educational content is growing rapidly, creating a significant opportunity for digital publishers. As more students, professionals, and lifelong learners turn to online resources, there is a strong need for eBooks, tutorials, interactive courses, and study materials that are accessible anytime, anywhere.

Digital platforms make it easy to deliver up-to-date content, personalized learning paths, and multimedia elements such as videos, quizzes, and infographics, thereby making learning more engaging and effective. For instance,

- A Brandon-Hall study found that e-learning can reduce the time employees spend learning by 40% to 60% compared to traditional classroom training for the same material.

Additionally, the shift toward remote education and professional upskilling has increased individuals' and institutions' willingness to pay for high-quality digital learning resources. Publishers who invest in creating high-quality educational content, offer flexible subscription models or pay-per-course models, and cater to diverse subjects and skill levels can capture a large, growing audience while generating steady and scalable revenue.

Segmentation Analysis

By End-user

Widespread Digital Content Consumption Boosted Market Dominance of Individual Consumers

Based on the end-user, the market is classified into individual consumers, students, educators and trainers, and academic and research users.

The individual consumers segment held the majority market share in 2025. In 2026, the segment is anticipated to dominate with a 37.6% as they represent the largest and most diverse audience for digital publishing content. With widespread smartphone and internet use, individuals regularly consume digital books, news articles, blogs, entertainment content, and self-learning materials for personal interest, convenience, and on-the-go access. Institutional users, such as academic or research organizations, and individual consumers engage with digital content daily, often through subscriptions, mobile apps, and social media platforms.

The individual consumers segment is expected to witness the highest CAGR of 7.8% during the forecast period. It is driven by increasing reliance on digital platforms for daily information, entertainment, and self-improvement. The rising use of smartphones, affordable internet access, and personalized content offerings is encouraging more individuals to adopt digital publishing services.

To know how our report can help streamline your business, Speak to Analyst

By Publishing Type

Rising Demand for Portable and On-Demand Reading Driving Dominance of eBooks and Digital Books

Based on the publishing type, the market is divided into eBooks & digital books, digital journals, digital magazines, digital news publishing, learning & courseware publishing, and others.

eBooks and digital books held the majority share in 2025. In 2026, the segment is anticipated to dominate with a 24.5% as they offer convenience, portability, and instant access to a wide range of content across devices. Readers can easily store, purchase, and access multiple books on smartphones, tablets, and e-readers, making them a preferred choice over physical books. Their widespread use in education, professional learning, and leisure reading further strengthens their dominant market position.

eBooks and digital books are expected to witness the highest CAGR of 8.6% during the forecast period due to increasing adoption of mobile reading, e-learning platforms, and subscription-based digital libraries. Continuous improvements in reading apps, interactive features, and personalized content recommendations are attracting new users.

By Format

Universal Compatibility and Ease of Access Fueled Majority Adoption of PDF Format

Based on format, the market is categorized into eBooks, PDF, and audio publishing.

PDF held the majority share in 2024. In 2025, the segment dominated with a 42.8% as it is widely accepted, easy to use, and compatible with almost all devices and operating systems. It preserves the original layout and formatting of content, making it ideal for eBooks, reports, academic papers, and official documents. Additionally, PDFs are easy to share, download, and store, making them a preferred format for publishers and readers across education, business, and personal use.

The audio publishing segment is expected to witness the highest CAGR of 9.2% during the forecast period.

By Enterprise Type

Strong Financial Capability and Scaled Operations Boosted Market Leadership of Large Enterprises

Based on the enterprise type, the market is segmented into large enterprises and small & medium-sized enterprises.

Large enterprises held the majority share in 2024. In 2025, the segment dominated with a 68.6% as they have greater financial resources, advanced digital infrastructure, and established content distribution networks. These organizations can invest heavily in digital publishing platforms, advanced technologies such as AI and analytics, and large-scale content production. Additionally, large enterprises serve a broad global audience and manage extensive content libraries, enabling them to generate higher revenue and maintain a stronger market presence than small and medium-sized enterprises.

Small & medium-sized enterprises are expected to witness the highest CAGR of 7.9% during the forecast period.

Digital Publishing Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

Asia Pacific

Asia Pacific Digital Publishing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held a majority of the digital publishing market share and reached a valuation of USD 63.17 billion in 2025, as digital reading is structurally embedded in everyday consumer behavior rather than functioning as an alternative to print. Large population in countries such as China, India, Japan, and South Korea primarily access content on smartphones, resulting in extremely high daily engagement with digital books, web novels, comics, and educational materials. Regional platforms have optimized monetization through episodic content, microtransactions, and integrated payment systems, enabling publishers to generate consistent revenue at scale.

Japan Digital Publishing Market

The Japan market in 2025 was valued at USD 9.90 billion, accounting for roughly 6.0% of global digital publishing revenues.

China Digital Publishing Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues valued at USD 24.24 billion, representing roughly 14.7% of global digital publishing sales.

India Digital Publishing Market

The India market in 2025 was valued at USD 8.27 billion, accounting for roughly 5.0% of the global market share.

North America

North America holds the second-highest share of the market largely due to its mature, highly monetized digital content ecosystem. Consumers in the region show a strong willingness to pay for premium content, including paid news platforms, academic databases, audiobooks, and subscription-based reading services. In addition, strict copyright enforcement and well-defined digital rights management systems help publishers protect revenue, encouraging sustained investment in digital publishing. The North America market was valued at USD 45.85 billion in 2025.

U.S. Digital Publishing Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at USD 39.65 billion in 2025, accounting for roughly 30.5% of Digital Publishing sales.

Europe

Europe is projected to record a growth rate of 5.5% in the coming years and reached a valuation of USD 39.61 billion in 2025. This is due to its mature publishing industry, high digital literacy, and strong adoption of e-learning and professional development platforms. Countries such as the U.K., Germany, and France have well-established digital infrastructure and a culture of paying for premium content, including eBooks, journals, and subscription-based publications. Additionally, stringent copyright laws and robust digital rights management encourage publishers to invest in digital platforms. At the same time, growing demand for multilingual content across the region supports the widespread use of digital publishing solutions.

U.K Digital Publishing Market

The U.K. market in 2025 was valued at USD 7.23 billion, representing roughly 4.4% of global Digital Publishing revenues.

Germany Digital Publishing Market

Germany’s market was valued at USD 9.79 billion in 2025, equivalent to around 5.9% of global Digital Publishing sales.

South America and Middle East & Africa

The Middle East & Africa is projected to record a growth rate of 8.7% in the coming years and is emerging as a significant player in the market, with the highest CAGR as younger populations in countries such as the UAE, Saudi Arabia, and Egypt prefer mobile-first reading. High smartphone penetration, combined with increased government support for digital education and smart learning platforms, is creating new opportunities for publishers. Furthermore, there is a growing demand for content in Arabic and localized languages, including eBooks, digital magazines, and professional training materials, which digital publishing platforms can deliver more efficiently than print.

South America is expected to grow at a significant CAGR, driven by a rapid shift toward mobile-first digital consumption, particularly among younger populations in Brazil and Argentina who rely heavily on smartphones for reading, learning, and news. There is a growing demand for localized eBooks, digital magazines, and professional training materials in Spanish and Portuguese that traditional print publishers cannot deliver as efficiently.

GCC Digital Publishing Market

The GCC market was valued at USD 0.99 billion in 2025, representing roughly 0.66% of global Digital Publishing revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Implement Strategic Initiatives to Adapt to Tech Changes

The market players are improving their product portfolios due to the increasing demand for more accurate health-tracking products. They are implementing various business strategies, such as partnerships, mergers, and acquisitions, to expand their businesses across the globe.

LIST OF KEY DIGITAL PUBLISHING COMPANIES PROFILED

- Amazon, Inc. (U.S.)

- Inc. (U.S.)

- Alphabet, Inc. (U.S.)

- RELX Group (U.K.)

- Thomas Reuters (Canada)

- News Corp (U.S.)

- Pearson PLC (U.K.)

- The New York Times Company (U.S.)

- Penguin Random House (U.S.)

- Adobe, Inc. (U.S.)

- Scribd (U.S.)

- Overdrive (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Amazon announced that readers could download EPUB and PDF files of DRM-free Kindle ebooks, marking a notable shift in digital publishing. DRM-protected ebooks remain unchanged, while newer DRM-free titles enable downloads by default. This gives readers more ownership and cross-platform access, but also raises concerns for authors about easier redistribution.

- July 2025: Apple News+ Audio expanded beyond the U.S. to the U.K., Canada, and Australia, making professionally narrated news stories available in more regions. The service offers audio versions of top journalism from major global and local publications within the Apple News and Podcasts apps. This move reflects Apple’s growing focus on audio-first digital publishing and subscription-based news consumption.

- June 2025: Reuters expanded its digital news subscriptions to eight new countries, offering affordable, unlimited access to its website and app. Priced at about USD 1 per week, the move strengthens Reuters’ global direct-to-consumer strategy. It reflects a broader trend in digital publishing toward subscription-based, trusted journalism to sustain high-quality reporting worldwide.

- March 2025: OverDrive partnered with Podium Entertainment to distribute its audiobooks worldwide, serving as Podium’s exclusive partner outside the U.S. and Canada. This deal makes over 1,000 bestselling and genre-defining audiobooks available to libraries and schools globally, enhancing access to digital content and supporting the growth of digital publishing in the audiobook sector.

- October 2024: Adobe launched the Adobe Content Authenticity web app, a free tool that allows creators to attach Content Credentials to their digital work, ensuring proper attribution, protection, and transparency. The app also lets creators’ control whether their content can be used to train generative AI models, reinforcing trust and accountability in the digital publishing and creative ecosystem.

- August 2024: Scribd introduced Ask AI, a new AI-powered feature that helps users search, analyze, and discover content more easily across Scribd and Everand. The tool enables document summarization and question-based research on Scribd, while offering personalized ebook and audiobook recommendations on Everand.

- May 2024: News Corp and OpenAI signed a multi-year global partnership allowing OpenAI to use content from major News Corp publications, such as The Wall Street Journal and The Times. The deal gives OpenAI access to both current and archived journalism to improve AI responses with reliable, high-quality news sources. The partnership highlights a growing model in digital publishing in which AI platforms and traditional media collaborate to uphold journalistic standards and sustainability.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.2% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Publishing Type, Format, Enterprise Type, End-user, and Region |

|

By Publishing Type |

· eBooks and Digital Books · Digital Journals · Digital Magazines · Digital News Publishing · Learning and Courseware Publishing · Others (Reference and databases, Corporate and Technical Documentation Publishing, etc.) |

|

By Format |

· eBooks · Audio Publishing |

|

By Enterprise Type |

· Large Enterprises · Small & Medium-Sized Enterprises |

|

By End-user |

· Individual Consumers · Students · Educators and Trainers · Academic and Research Users |

|

By Region |

· North America (By Publishing Type, Format, Enterprise Type, End-user, and Country) o U.S. (By End-user) o Canada (By End-user) o Mexico (By End-user) · South America (By Publishing Type, Format, Enterprise Type, End-user, and Country) o Brazil (By End-user) o Argentina (By End-user) o Rest of South America · Europe (By Publishing Type, Format, Enterprise Type, End-user, and Country) o U.K. (By End-user) o Germany (By End-user) o France (By End-user) o Italy (By End-user) o Spain (By End-user) o Russia (By End-user) o Benelux (By End-user) o Nordics (By End-user) o Rest of Europe · Middle East & Africa (By Publishing Type, Format, Enterprise Type, End-user, and Country) o Turkey (By End-user) o Israel (By End-user) o GCC (By End-user) o North Africa (By End-user) o South Africa (By End-user) o Rest of Middle East & Africa · Asia Pacific (By Publishing Type, Format, Enterprise Type, End-user, and Country) o China (By End-user) o India (By End-user) o Japan (By End-user) o South Korea (By End-user) o ASEAN (By End-user) o Oceania (By End-user) o Rest of Asia Pacific |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 163.89 billion in 2025 and is projected to reach USD 279.68 billion by 2034.

In 2025, the market value stood at USD 45.85 billion.

The market is expected to exhibit a CAGR of 6.2% during the forecast period of 2026-2034.

By end-user, the individual consumers segment is expected to lead the market.

Increasing internet and smartphone penetration drives market growth.

Amazon, Inc., Apple. Inc., Alphabet, Inc., and RELX Group are the major players in the global market.

Asia Pacific dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 110

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us