Driver Monitoring System Market Size, Share & Industry Analysis, By System Integration (Eye Tracking System, Driver Identification, Steering Behavior Monitoring System, and Heart Rate Monitoring System), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Heavy Commercial Vehicles), By Sensor Suite (Camera-based NIR/IR (monocular), Stereo/Depth (dual cam / ToF-assisted), RGB + NIR Hybrid, and Camera + Sensor-fusion add-ons), By ADAS Level (Level L2/L2+ and Level L3), and Regional Forecast, 2026-2034

Driver Monitoring System Market Size and Future Outlook

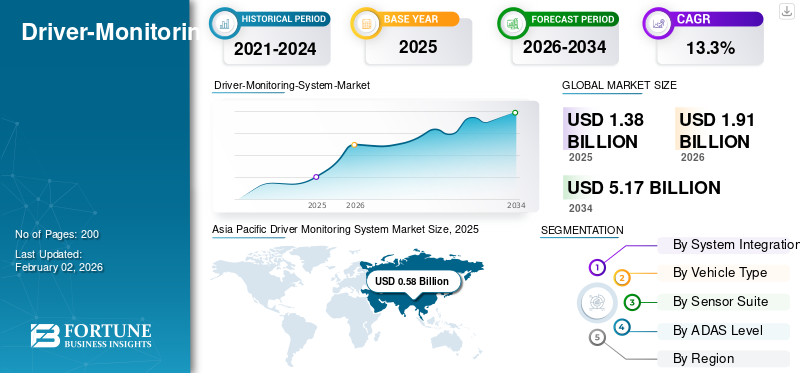

The driver monitoring system market size was valued at USD 1.38 billion in 2025. The market is projected to grow from USD 1.91 billion in 2026 to USD 5.17 billion by 2034, exhibiting a CAGR of 13.3% during the forecast period. Asia Pacific dominated the global driver monitoring system market with a market share of 42.03% in 2025.

A Driver Monitoring System (DMS) is an in-cabin safety technology that utilizes infrared/near-infrared cameras, along with computer vision, to track a driver’s eyes, gaze, head pose, eyelid closure, and yawning, thereby detecting distraction and drowsiness. Some implementations include steering torque, lane-keeping data, seat/PPG sensors, or tracking heart rate signals. When attention lowers, the DMS issues escalating alerts, limiting the hands-free features, and may trigger safe-stop maneuvers in higher-automation modes. Integrated with ADAS and HMI, DMS helps meet regulatory and rating requirements while improving real-world crash avoidance.

The market is expanding rapidly as regulations and safety ratings elevate DMS from a premium option to a core requirement. The EU General Safety Regulation and Euro NCAP protocols, along with IIHS safeguards in North America, are driving the standard fitment of vehicle safety features across new platforms. Most near-term volume applications utilize monocular IR cameras; however, stereo/depth and sensor fusion with occupant monitoring technology is growing for robust hands-free supervision and early Level 3 (L3) capabilities. Adoption leads in passenger cars, with rising fitment in LCV fleets and selective HCV programs. Key players include Valeo, Bosch, Continental, Magna, Denso, Panasonic Automotive, Hyundai Mobis, Aptiv, ZF, Forvia, Gentex, Visteon, Marelli, Seeing Machines, Smart Eye, Cipia, Jungo, Eyeris, emotion3D, Tobii, and Xperi.

U.S. tariffs on Chinese autos and components impact DMS cost structures by increasing prices for components such as cameras, IR emitters, optics, and semiconductors sourced from China. To manage bill-of-materials risk, Tier-1s and OEMs accelerate local supply chains in Mexico, Canada, and associated Asian suppliers, while dually sourcing the key modules. In the short term, tariffs can slow the adoption in the new entry segments or compress margins and in the longer term, they will catalyze the North American supply chains that will reduce the exposure and lead times. Despite headwinds, safety-rating pressure keeps DMS on roadmaps, with sourcing shifts rather than feature removals.

Download Free sample to learn more about this report.

Drive Monitoring System Market Key Takeaways

- 2025 Market Size: USD 1.38 billion

- 2026 Market Size: USD 1.91 billion

- 2034 Forecast Market Size: USD 5.17 billion

- CAGR: 13.3% from 2026–2034

- Asia Pacific dominated the driver monitoring system market with a 42.03% share in 2025.

- Eye tracking systems held the largest share due to regulatory compliance and advanced driver monitoring capabilities.

- Passenger cars dominated the market owing to high production volumes and increasing DMS integration mandates.

Asia Pacific

Asia Pacific generated USD 0.58 billion in revenue in 2025 and accounted for the largest regional market share.

Europe

Europe’s regulatory framework is accelerating DMS adoption, with compliance requirements extending to all vehicle registrations by 2026.

North America

North America is witnessing strong demand growth driven by safety ratings and the expansion of hands-free ADAS features.

U.S.

Growing NCAP requirements and hands-free driving evaluations are supporting wider deployment of DMS technologies.

Japan

Rising adoption of advanced driver assistance and in-cabin monitoring technologies is contributing to market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Regulatory & Safety-Rating Mandates for Distraction and Drowsiness Detection is Driving the Demand in the Market Growth

The single biggest factor in the driver monitoring system market growth is regulation and safety-rating pressure that now explicitly requires or rewards the detection of drowsiness or distraction. In Europe, implementing rules under the General Safety Regulation outline approval for Driver Drowsiness & Attention Warning, with enforcement transitioning from 2024 to all registrations by 2026, effectively making DMS a table-stakes requirement. In the U.S., the Insurance Institute for Highway Safety introduced partial-automation safeguard ratings that grade the rigor of a vehicle’s driver monitoring, pushing OEMs to tighten supervision of hands-free features. At the same time, Smart Eye disclosed that it has more than 2 million vehicles in service, alongside hundreds of awarded programs across dozens of OEMs, evidence that fitment is scaling, not just being piloted.

Suppliers are expanding their features to align with the regulatory scope. Hyundai Mobis has unveiled a cabin-monitoring suite that flags ten high-risk passenger and driver behaviors, and Gentex has previewed mirror-integrated DMS as part of its next-generation interior systems portfolio. Importantly, public-sector safety rationales underpin these rules and ratings. Consequently, compliant systems are being designed to warn, escalate, and, in higher-automation modes, help trigger safe-stop strategies. This combined mandate, rating, and supplier scale-up loop reduces uncertainty for automakers, hard-wires DMS into global platform roadmaps, and steadily shifts the market from monocular IR to higher-confidence stereo/depth and sensor-fusion configurations as hands-free L2/L2+ and early L3 programs proliferate.

MARKET RESTRAINTS

Increasing Risk of Privacy, Biometric Data, and Cybersecurity Compliance are Hindering the Market Growth

A major restraint on the market is the risk of privacy, biometric data, and cybersecurity compliance, which slows rollouts, adds redesign cycles, and can trigger litigation. In the EU, data-protection authorities have issued specific guidance for connected vehicles that requires strict purpose limitation, minimization, and edge processing for in-cabin images, which raises integration costs and time for installation of camera-based DMS and OMS. China’s automotive data security rules add another layer, mandating localization, security assessments, and special handling of sensitive in-vehicle image data, complicating global platforms and software analytics pipelines.

In the U.S., biometric privacy laws are creating tangible legal exposure. Recent class actions have targeted driver-facing cameras for allegedly collecting facial geometry without obtaining required consent or making necessary disclosures, and settlements are emerging, signaling that fleets and vendors face real liability if their compliance is imperfect. Parallel to privacy, cyber approval regimes (e.g., UN R155) require OEMs to prove the end-to-end protection of in-cabin sensors and data paths, and approval can be refused if threat analyses or mitigations are incomplete, incurring another schedule and cost risk for DMS launches.

Recent product updates highlight how privacy constraints can hinder releases across regions. For example, attention-monitoring features tied to vision systems that are rolling out in one market but not yet live in another complicate validation, support, and regulatory filings. OEMs and Tier-1s must build consent flows, on-device redaction, retention limit controls, and robust cybersecurity measures, then defend them against audits and lawsuits. Each privacy or cyber gap can delay SOP, leading to removal of features on lower trims, or prompt conservative sensor choices, collectively slowing uniform, high-confidence DMS penetration.

MARKET OPPORTUNITIES

Accelerating the Deployment of Advanced Thermal Management Systems for Electric and Hybrid Vehicles Generates Beneficial Growth Opportunities

A major opportunity for the global Driver Monitoring System (DMS) market is the rapid expansion from compliance DMS to full interior-sensing platforms that bundle driver attention, impairment checks, occupant monitoring, child-presence detection, and personalized HMI, unlocking broader safety credit, software features, and new revenue streams. Regulators and ratings bodies are already setting the floor. Hyundai Mobis recently unveiled an in-cabin suite that tracks posture, gaze, mobile phone use, seatbelt status, and even rear-seat child safety, signaling OEMs’ intent to move beyond single-purpose drowsiness alerts.

U.S. authorities recorded 3,308 deaths from distracted driving in 2022, sustaining pressure for robust, camera-based attention supervision. Looking ahead, the EU’s implementing rules for drowsiness and distraction standardize approval templates, while Euro NCAP’s roadmap ties driver monitoring performance to fostering a market where DMS is the doorway to better-off interior-sensing capabilities, for OEMs and Tier-1s, that means higher device per vehicle, software licensable across trims, and the ability to upsell features that address distraction, impairment, and passenger safety transforming DMS from a cost of compliance into a platform for safety leadership and recurring software value.

DRIVER MONITORING SYSTEM MARKET TRENDS

Hands-Free And Automated Features for Supervision and Monitoring

A major inclination reshaping the driver monitoring system market trends is the shift to supervisory gatekeeping for hands-free and automated features. Instead of just warning about drowsiness, DMS now determines if and how long features like lane-centering and highway assist can remain active, escalating from visual/haptic cues to slowdowns or safe stops when attention lapses.

GM Super Cruise uses a driver-attention camera to gate hands-free operation; Ford BlueCruise relies on a machine learning, driver-facing IR camera to verify eyes-on-road; and Mercedes-Benz DRIVE PILOT pairs conditional automation with driver-status checks and operational constraints. Looking ahead, announcements about next-gen systems, including plans for more capable hands-free experiences later this decade, suggest even tighter association of robustness of DMS and the availability of automated driving. This trend materially helps the market by moving DMS from a passive alert module to a core safety governor embedded in ADAS/HAD stacks, expanding standard fitment, raising technical requirements, and creating ongoing software value as algorithms evolve with ratings and regulatory test protocols.

Patent Analysis

- Patent number: US11685385B2

- Title: Driver-monitoring system

- Issue Year: June 2023

- Inventors: Yang Yang; Douglas L. Welk

- Current assignee: Aptiv Technologies AG

- Original assignee (at filing): Aptiv Technologies Ltd

The patent covers a controller that takes driver-monitor sensor data (e.g., camera). At the same time, the vehicle operates in autonomous mode, computes score for driver-supervisory metrics, and derives a supervision score to determine driver readiness and display an awareness status.

Download Free sample to learn more about this report.

Segmentation Analysis

By System Integration

Eye Tracking System Dominates Due to its Effective Functioning, Meeting the Requirements of Regulators and Safety Regulations

Based on the system integration, market is segmented into eye tracking system, driver identification, steering behavior monitoring system, and heart rate monitoring system.

The eye-tracking camera DMS is the backbone of modern attention supervision because it directly measures eyelid closure, gaze, and head pose signals that regulators and safety raters now require. In June 2024, Europe finalized the approval templates for Driver Drowsiness & Attention Warning and Advanced Driver Distraction Warning, moving from new types in 2024 to all registrations by 2026, which ensures the integration of camera DMS into platform designs. In November 2024, the U.S. NCAP roadmap explicitly listed distraction or drowsiness are among planned evaluation updates, ensuring OEMs will be scored on the quality of eye-tracking supervision. Together, rulemaking, ratings pressure, scale proof points, and improving packaging mean eye-tracking retains the largest share, while enabling to the upselling of the identification and impairment features that further expand the market growth.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Passenger Cars, Being the Highest in Volumes and Requiring DMS Leads to its Dominance in the Segment

Passenger cars, light commercial vehicles, and heavy commercial vehicles have been taken into consideration, as per vehicle type.

Passenger cars lead DMS revenue as mandates and ratings target mass-market M1 vehicles first, creating the fastest compliance pull and widest unit base. OEM activity around supervised automation further concentrates DMS in cars. In January 2025, U.S. authorities escalated an investigation into hands-free systems, underscoring how camera-based driver attention serves as a gatekeeper for the availability of these features. In late 2025, GM announced a next-generation eyes-off highway system planned for 2028, implying even tighter association between DMS robustness and automated capabilities in passenger segments. With 92.5 million global vehicles produced in 2024, even a modest expansion in integration of DMS in passenger cars drives the largest absolute revenue increase. Packaged features like driver ID and child-presence detection, amplify value per car and reinforce PC leadership.

By Sensor Suite

Monocular NIR/IR Remain the Main Application it Maintains a Balance of Regulatory Compliance, Performance, Packaging, and Cost

Based on the sensor suite, the market is differentiated into camera-based NIR/IR (monocular), stereo/depth (dual cam / ToF-assisted), RGB+ NIR hybrid, and camera + sensor-fusion add-ons).

Monocular NIR/IR remains the dominant sensor suite because it strikes a balance between regulatory compliance, performance, packaging, and cost. In January 2025, a major Tier-1 showed mirror-integrated driver/in-cabin monitoring, compressing BOM and wiring; in March 2025, another Tier-1 unveiled an in-cabin monitoring system that analyzes posture and device use, both centered on IR-illuminated cameras. This preserves monocular’s share in the near term while creating a clean upgrade fordepth and fused configurations, where hands-free endurance, occlusion handling, or impairment checks demand more confidence, supporting market growth without stranding early investments.

By ADAS Level

L2/L2+ Retains Its Leadership Due to DMS-Governed Hands-Free Supervision

By ADAS level, the market is segmented into Level L2/L2+ and Level L3.

Level L2/L2+ dominates the driver monitoring system market share because it is already broadly deployed and now uses DMS as a supervisory for hands-free features. Europe’s June 2024 regulation related to drowsiness and distraction will be applied to all registrations in 2026, making attention supervision a standard even outside the realm of automation. Throughout 2025, news cycles reinforced DMS’s role in gating automation. U.S. authorities upgraded an investigation into a large hands-free fleet. At the same time, late-2025 announcements previewed next-generation hands-free/eyes-off capabilities that were impossible to scale without robust driver-status checks. Altogether, ratings scrutiny, regulatory timelines, and OEM product plans keep L2/L2+, the largest revenue pool for DMS.

At the same time, L3 grows from a smaller base and benefits from the same camera stack, ensuring the segment’s expansion feeds overall market growth.

DRIVER MONITORING SYSTEM MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

North America’s DMS demand is propelled by the pressure of ratings and the transition of DMS from warnings to gatekeeping for hands-free features. In 2024, the Insurance Institute for Highway Safety introduced partial-automation safeguard ratings that explicitly grade driver monitoring technologies, finding most systems inadequate, spurring OEM upgrades across 2025–2026 models. Together, ratings, safety data, and supplier scale accelerate fitment in passenger cars and high-content trims, with LCV fleets following as insurers and large operators specify attention-supervision features. In the U.S., ratings and policy serve as the propelling factor for the product demand. The NCAP Roadmap formalize DMS expectations, while distraction harm is also documented. These forces, combined with OTA-upgradable interiors, shift DMS from premium options to default supervision on hands-free advanced driver assistance systems (ADAS).

Asia Pacific

Asia Pacific Driver Monitoring System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates in sheer volume and is also the fastest-growing region as DMS becomes the supervisor for hands-free and L2/L2+ features in a region with rising automated capabilities. Hyundai Mobis has launched an In-Cabin Monitoring System that tracks gaze, posture, device use, and child presence, marking a shift from basic DMS to interior sensing. The global program scale also supports region’s rollouts, with Seeing Machines targeting 2.2 million vehicles by FY2024, and Smart Eye’s program awards providing capacity and algorithm maturity for Chinese, Japanese, and Korean platforms. As hands-free endurance and misuse-prevention thresholds rise, Asia Pacific shifts from monocular IR dominance toward stereo/ToF and sensor fusion on premium and export models, lifting-up the DMS revenue per vehicle and reinforcing the region’s lead in global growth.

Europe

Europe leads the way in regulatory codification, making DMS a de facto standard. In June 2024, the EU issued Implementing Regulation 2024/1721, finalizing approval templates for Driver Drowsiness & Attention Warning and Advanced Driver Distraction Warning applicable to new types from 2024 and all registrations by 2026, which locks camera-based DMS into platform plans. The regulatory ensures rapid pull-through on passenger cars, followed by LCVs, as fleets and insurer-specific attention and distraction controls. This accelerates the installation of device per vehicle (camera, illuminator, compute, and software), supporting Europe’s role in global DMS growth through 2026 and beyond.

Rest of the World

Rest of World (RoW) market growth is steadily accelerating as regulatory ideas and rating practices diffuse, and as supplier’s package DMS with occupant monitoring for emerging markets. Many RoW programs begin with monocular IR, then they add sensor fusion where fleets or premium CKD programs require stronger misuse prevention. Although mandates are less uniform than in the EU, the NCAP-style focus on distraction and global publicity around weak driver-attention safeguards has raised expectations, prompting importers and assemblers to specify DMS in more trim levels. As parts localization grows, RoW markets benefit from falling module prices and OTA support, allowing faster refresh cycles and alignment with global ADAS roadmaps. The combination of supplier scale, diffusing standards, and cost-down trajectories keeps RoW on a consistent upward path, meaningfully contributing to the global DMS expansion after 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Inclination Toward Hands-Free, Internal Sensorized Systems With Connectivity, And Continuous Innovation By Companies Drives The Market Competition

Seeing Machines is widely regarded as the frontline specialist in automotive DMS, earning leadership through early research depth, robust OEM validations, and dual pathways embedded and aftermarket. Product lines include embedded DMS software/hardware IP for passenger vehicles, as well as the Guardian solution for commercial fleets, both designed to meet EU DDAW/ADDW templates and global rating protocols. Key specialties include low-latency attention estimation, misuse detection for hands-free features, and scalable integration that supports mirror-mounted, cluster-mounted, or roof console configurations, enabling rapid rollout across multiple OEM programs.

Tier-1 system integrators Bosch, Continental, Valeo, ZF, Forvia, Magna, Denso, Panasonic automotive market, Hyundai Mobis, Aptiv, Visteon, and Marelli compete to package DMS with interior electronics, displays, mirrors, and domain controllers. Differentiation centers on Euro NCAP performance, low-light robustness, occlusion handling, and integration form factors. Fleets accelerate adoption through aftermarket kits, while passenger cars drive scale via regulations and safety ratings that increasingly grade driver monitoring quality. Major players and vendors are converging on scalable IR camera modules, mirror-integrated packages, and OTA-upgradable software, with partnerships between Tier-1s and AI specialists accelerating global, regulation-aligned deployment.

LIST OF KEY DRIVER MONITORING SYSTEM COMPANIES PROFILED:

- Valeo (France)

- Bosch (Germany)

- Continental (Germany)

- Magna International (Canada)

- Denso Corporation (Japan)

- Panasonic Automotive Systems (Japan)

- Hyundai Mobis (South Korea)

- Aptiv (Ireland)

- ZF Group (Germany)

- Forvia (France)

- Gentex Corporation (U.S.)

- Visteon Corporation (U.S.)

- Marelli (Japan)

- Seeing Machines (Australia)

- Smart Eye (Sweden)

KEY INDUSTRY DEVELOPMENTS

- In October 2025, Magna emphasized that its mirror-integrated DMS, recognized with a 2024 Automotive News PACE Award, is scaling with a leading German OEM and expanding in China and Europe. Positioning the solution as first-to-market and regulation-ready, Magna underscored how interior integration reduces visual intrusion while meeting the requirements for distraction and drowsiness. The firm reiterated the importance of future-proofing via modularity for different vehicle lines. It linked the DMS to a wider interior sensing suite to help automakers improve safety features and user experience as global platforms standardize on in-cabin monitoring.

- In July 2025, Nota AI announced a collaboration with Renesas to deliver high-efficiency DMS on the RA8P1 MCU, demonstrating real-time attention analysis on a low-power, small-footprint controller. The partnership demonstrates how AI optimization and embedded NPUs can enable driver monitoring in cost-sensitive trims and compact ECUs, thereby expanding adoption beyond premium vehicles.

- In June 2025, Harman drew media attention for new tech aimed at monitoring and reducing driver distraction, showcasing elements from its portfolio. The approach combines AR display strategies with physiological and behavioral sensing to keep eyes on the road and modulate alerts. Reporting highlighted the rising need to curb smartphone-driven distraction and integrate driver-state insight with HMI and ADAS gating. Harman’s newsroom positioned these capabilities as part of a broader, safety-first in-cabin experience roadmap that can evolve via software and connected services.

- In February 2025, Hyundai Mobis unveiled an In-Cabin Monitoring System designed to track more than 10 risky behaviors, including phone use, unbelted occupants, hands off the wheel, and the presence of children in the rear seat. The system combines cameras with software logic to analyze posture, position, and biometric signals, issuing visual and audio warnings and targeting European OEMs for orders. Mobis noted ASPICE certification and performance exceeding NCAP thresholds, while signaling a roadmap to enhance healthcare features and a 2.0 version for fleets, as evidence of the rapid evolution from a basic DMS to a comprehensive interior sensing system.

- In January 2025, FEV introduced CogniSafe, an AI-supported DMS that applies deep learning and computer vision to monitor distraction, fatigue, and inattention in real time, even under challenging conditions. The company positioned CogniSafe as a holistic solution, combining multiple sensors and analytics to maintain driver readiness, particularly important as semi-automated features become more widespread and legal expectations become stricter. Messaging underscored safety outcomes, reducing human error crashes and aligning with growing regulatory scrutiny of driver supervision in partially automated driving. The launch shows engineering houses pushing beyond compliance to robust state estimation suitable for global platforms.

- In September 2021, Tesla expanded its camera-based DMS beyond vision-only cars, rolling it out to vehicles with radar via software update 2021.32.5. The cabin camera tracks driver attention and can reduce steering-wheel input with processing performed on-device to address privacy concerns. The rollout also widened geographic availability from the U.S. to Canada and Mexico, signaling Tesla’s shift from torque-sensing to direct, vision-based attention checks that better detect phone use and gaze direction. Owners reported fewer false prompts when DMS was active, foreshadowing tighter supervision of hands-free features across the fleet.

- In May 2021, Tesla enabled cabin camera-based DMS for Model 3 and Model Y, moving beyond steering-torque checks to gaze and eyelid assessment during Autopilot use. The feature was initially targeted at radar-less vehicles in the U.S., with the note that broader coverage would follow. The release documentation explained that camera data remains in the car unless a user opts into data sharing. At the same time, the system assigns probabilities to inattentive states and can escalate from alerts to disengaging assistance. The shift marked Tesla’s early pivot toward direct attention validation, a prerequisite for safer supervised automation.

REPORT COVERAGE

The Global Driver Monitoring System Market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The Driver Monitoring System Market forecast offers a comprehensive competitive landscape, encompassing market share, emerging opportunities, and profiles of key players in the automotive industry.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By System Integration, By Vehicle Type, By Sensor Suite, By ADAS Level, and By Region |

| By System Integration |

|

| By Vehicle Type |

|

| By Sensor Suite |

|

| By ADAS Level |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.38 billion in 2025 and is projected to reach USD 5.17 billion by 2032.

In 2024, the market value stood at USD 0.58 billion.

The market is expected to rise at a CAGR of 13.3% during the forecast period.

The Level L2/L2+ segment led the ADAS level segment.

Regulatory & safety-rating mandates for distraction and drowsiness detection are driving demand in the market, contributing to its growth.

Top players in the market include Seeing Machines, Smart Eye, Cipia, Tobii, Xperi, Eyeris, and Hyundai Mobis.

Asia Pacific dominated the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us