Drone Payload Market Size, Share, Russia-Ukraine War Impact & Industry Analysis, By Class (Micro UAVs (Below 2 Kg), Mini UAVs (2-20 Kg), Small UAVs (20-50 Kg), and Tactical UAVs (MALE & HALE)), By Platform (Fixed-Wing, and Rotary-Wing), By Payload Type (EO/IR, Cameras, Search and Rescue, Signal Intelligence, Electronics Intelligence, Laser Sensors, CBRN Sensors, and Others), By Application, and Regional Forecast, 2026-2034

DRONE PAYLOAD MARKET SIZE AND FUTURE OUTLOOK

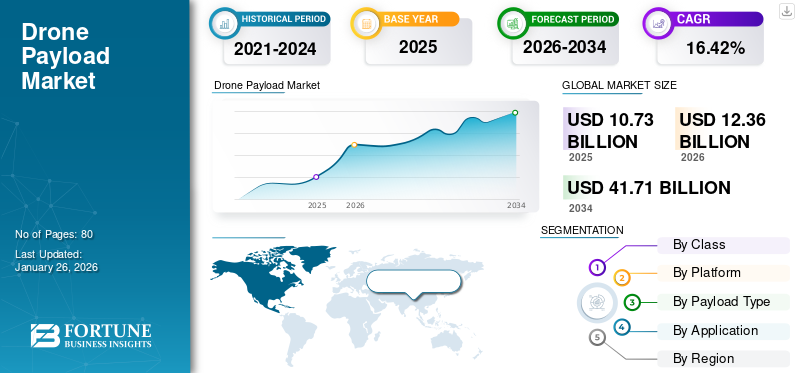

The global drone payload market size was valued at USD 10.72 billion in 2025. The market is projected to grow from USD 12.36 billion in 2026 to USD 41.71 billion by 2034, exhibiting a CAGR of 16.42% during the forecast period. North America dominated the drone payload market with a market share of 34.12% in 2025.

Payloads transform drones from simple flying platforms into versatile tools capable of executing precision tasks across industries such as agriculture, energy, logistics, construction, and public safety. In defense, the integration of electro-optical, infrared, and electronic warfare systems has become indispensable for intelligence, surveillance, reconnaissance, and tactical missions.

The market is evolving into a critical enabler of both commercial and defense operations, driven by rising demand for advanced sensors, imaging systems, communication modules, and cargo delivery solutions. The market benefits from advancements in miniaturization, edge computing, and modular designs, which allow drones of varying sizes to carry increasingly sophisticated payloads. At the same time, regulatory frameworks, privacy concerns, and payload weight constraints continue to shape the adoption patterns. With rapid growth in AI-powered analytics, multispectral sensors, and delivery payload systems, the market is poised for sustained expansion as industries seek higher efficiency, automation, and real-time decision-making capabilities.

The market features a mix of established defense contractors, specialized sensor developers, and commercial drone innovators. Companies such as Lockheed Martin, Northrop Grumman, and Thales dominate the defense-focused payload segment with advanced surveillance and communication systems. On the commercial side, DJI, Parrot SA, and Skydio lead with modular payloads and AI-enabled imaging solutions. Specialized firms such as Teledyne FLIR, AeroVironment, and Quantum Systems are strong in thermal imaging, LiDAR, and tactical payloads. Additionally, technology suppliers including Velodyne LiDAR and Trimble provide precision mapping sensors, while Israel Aerospace Industries (IAI) and Elbit Systems strengthen the market through military-grade payloads and electronic warfare solutions.

Download Free sample to learn more about this report.

Drone Payload Market Takeaways

- 2025 Market Size: USD 10.72 billion

- 2026 Market Size: USD 12.36 billion

- 2034 Forecast Market Size: USD 41.71 billion

- CAGR: 16.42% from 2026-2034

- North America dominated the drone payload market with a 34.12% share in 2025.

- The tactical UAVs (MALE and HALE) segment held the leading market share of 43.51% in 2026.

- The rotary-wing segment captured the largest share of 73.26% in 2026.

North America

North America accounted for USD 3.66 billion in 2025 and is projected to reach USD 4.19 billion in 2026, driven by strong defense investments and UAV modernization programs.

Asia Pacific

Asia Pacific reached USD 3.26 billion in 2025 and is expected to grow to USD 3.80 billion in 2026 due to rising drone adoption across defense, agriculture, and logistics sectors.

Europe

Europe recorded USD 2.53 billion in 2025 and is projected to reach USD 2.92 billion in 2026, supported by increasing surveillance and border security applications.

U.S.

The market reached USD 3.51 billion in 2025, supported by rising military drone procurement and advanced ISR payload integration initiatives.

Japan

Growing investments in industrial drones, disaster management systems, and autonomous aerial technologies are supporting market expansion across commercial and defense applications.

Read More

RUSSIA-UKRAINE WAR IMPACT

Russia–Ukraine War Accelerated Military Demand, Shifted Supply Chains, and Rapid Field-Driven Innovation

The Russia-Ukraine conflict has had a pronounced and multifaceted impact on the drone payload market growth, particularly in accelerating military demand and prompting rapid, practical innovation. The conflict showcased operational value of small, low-cost UAVs equipped with effective payloads from improvised munitions and target designation to reconnaissance using off-the-shelf EO/IR, thermal cameras, and signal-intelligence kits. This battlefield validation increased defense procurement interest in quickly fieldable payloads, modular payload bays, and hardened sensor suites, shortening procurement cycles for certain classes of equipment. At the same time, the war exposed vulnerabilities in supply chains for high-end components (specialized optics, inertial measurement units, RF components), leading some manufacturers to seek alternative suppliers, onshore critical production, or redesign products around readily available parts.

Data from the theater also fueled innovation in counter-UAV payloads jamming, spoofing, and net-capture systems and in software for swarm coordination and autonomous target detection, accelerating capabilities that were previously experimental. On the commercial side, heightened geopolitical risk and export controls tightened the movement of dual-use sensors and electronics, complicating international sales and collaboration. Humanitarian and reconstruction needs in and near conflict zones creates niche demand for payloads specialized in damage assessment, mine detection, and communications-relay roles. Public perception shifted with the visibility of armed drones triggered renewed debate over ethics and regulations, which could influence long-term commercial acceptance of certain payload types. Overall, the conflict acted as both a crucible for rapid capability demonstration and a forcing function for supply-chain resilience and operational reinforcement across the drone payload industry.

DRONE PAYLOAD MARKET TRENDS

Rapid Miniaturization and Sensor Fusion are Reshaping Payload Design to Emphasize Market Growth

The market is moving decisively toward lighter, more integrated systems that combine multiple sensing, communication, and effect capabilities into single modular units. Advances in semiconductor manufacturing, battery energy density, and MEMS sensors allow payloads that once required large platforms to be fitted on small, agile UAVs. This shift expands use-cases from industrial inspection and precision agriculture to last-mile delivery and tactical reconnaissance. At the same time, software-driven capabilities such as on-board AI, edge computing, and real-time data compression reduce the reliance on high-bandwidth links. This enable meaningful autonomy drones that can preprocess imagery, detect anomalies, and make navigation decisions without constant human oversight.

Interoperability is also rising in importance, payloads are increasingly built to standard physical and electrical mounts and to open data formats so operators can swap sensors across platforms quickly. Commercialization pressures push manufacturers to offer ‘payload-as-a-service’ or subscription models where customers pay for analytics and outcomes rather than raw hardware, accelerating adoption among enterprises that lack in-house drone expertise. Regulatory evolution is uneven in some regions, clearer rules for beyond-visual-line-of-sight (BVLOS) and airspace integration are unlocking larger-scale operations, which favors scalable and networked payload systems. Environmental concerns are nudging designs toward recyclable materials and lower power consumption. In short, the market trend favors compact, multi-function, smart payloads that are platform-agnostic and backed by software analytics transforming drones from single-purpose tools into adaptable data-collection nodes within larger digital workflows.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET OPPORTUNITIES

Industry-specific Verticalization and Service-oriented Payload Offerings to Accentuate Market Growth

Opportunities in the market are abundant for companies that combine hardware excellence with domain-specific software and services. Verticalization designing payloads and analytics tuned to the needs of a particular industry (e.g., pipelines, precision viticulture, roof inspections, coastal erosion monitoring) unlocks higher willingness to pay as customers receive turnkey solutions that map directly to operational KPIs. There is sizable room for growth in payloads that enable routine, repeatable missions; modular LiDAR and photogrammetry packages tailored for construction and surveying workflows; thermal and acoustic sensors for energy-asset preventive maintenance; multispectral payloads bundled with agronomy dashboards for crop advisors. Another major opportunity is payload-as-a-service and managed operations, as many enterprises prefer outsourcing flight planning, data collection, and analytics rather than buying equipment and hiring pilots. Thus, providers who can deliver validated outcomes on subscription terms will capture steady revenue.

Innovations in hybrid power systems, higher energy-density batteries, and hydrogen fuel cells for larger drones can extend endurance and unlock long-duration maritime or pipeline-monitoring missions. Urban logistics and air-taxi ecosystems where regulatory frameworks present demand for standardized cargo pods and safe-release mechanisms. Finally, secondary markets such as retrofit kits to modernize legacy platforms, spare-part ecosystems, and secure communication modules for sensitive operations offer recurring revenue streams. Companies that highlight interoperability, rigorous data pipelines, and clear ROI metrics for customers will be best positioned to convert these opportunities into scale.

MARKET DRIVERS

Demand for High-value Data and Automation from Commercial and Defense Users to Boost Market Growth

The principal driver of the market is an expanding appetite for actionable, high-resolution data across many industries paired with a push to automate repetitive or hazardous tasks. Sectors such as agriculture want precise multispectral and hyperspectral imaging to optimize inputs and monitor crop health; utilities and energy companies require thermal and LiDAR sensors to inspect assets rapidly and safely; construction and mining adopt photogrammetry and LiDAR for volumetric and progress tracking; and logistics players experiment with specialized cargo pods and release mechanisms for point deliveries. Public safety and defense continue to drive demand for electro-optical/infrared (EO/IR), signal intelligence, and electronic warfare payloads. Improvements in data processing on-board AI, photogrammetric software, and cloud analytics increase the value of each sortie by turning raw sensor outputs into decisions and KPIs, which validates investment in better payloads.

Labor shortages and cost pressures encourage automation where inspecting a transmission line manually is expensive and slow. Meanwhile, a drone with a thermal camera and automated defect detection can perform the same work faster and with less risk. Falling costs of sensors, rising competition among component suppliers, and modular payload bays that support rapid integration reduce entry barriers for new payload types. Finally, business model innovation leasing, managed services, and outcome-based contracts makes advanced payloads economically accessible to mid-market firms, further fueling demand and ongoing product development.

MARKET RESTRAINTS

Regulatory Uncertainty and Airspace Integration Issues Hampers Market Growth

Despite strong demand, several restraints slower the growth and complicates commercialization. Regulatory fragmentation across countries and regions with limitations on where and how payload-equipped drones can operate; inconsistent rules for BVLOS flights, night operations, and urban air mobility restrict many high-value applications that require wide-area or routine flights. Certification and airworthiness processes for payloads intended for manned-aircraft-integrated operations or for transporting goods are often lengthy and costly, disadvantaging smaller innovators and raising barriers to market entry. Privacy and data-protection concerns impose operational constraints where certain sensors (e.g., persistent high-resolution imaging or signal interception) face legal and public acceptance limits that reduce potential use cases.

Technical constraints such as limited flight endurance (battery life), payload weight vs. lift trade-offs, and electromagnetic interference in crowded RF environments restrict the scale and duration of missions. Supply-chain fragility for high-end components (specialized optics, chips) can delay production and raise costs; geopolitical tensions and export controls add uncertainty for manufacturers reliant on cross-border sourcing. Additionally, integration complexity making sensors, processors, and communications work seamlessly together and with enterprise IT systems requires skilled engineering and bespoke software, which increases time-to-deployment and cost. Collectively these restraints keep some sectors away from fully realizing drone payload potential until regulatory harmonization, certification pathways, and technical limitations are eased.

MARKET CHALLENGES

Technical Integration, Interoperability, and Trust in Autonomous Analytics Are Major Challenges in Market

The drone payload market share faces several practical and systemic challenges that go beyond regulation and cost. Technical integration remains challenging as combining diverse sensors (LiDAR, SAR, multispectral, gas detectors), power systems, communication radios, and edge compute units into a compact, vibration-resistant package that performs reliably across temperatures is nontrivial. Each added capability complicates thermal management, electromagnetic compatibility, and weight distribution, often requiring custom engineering that raises price and time to market. Interoperability between payloads and heterogeneous drone platforms is an industry pain point; despite growing interest in standard mounts and APIs, many legacy platforms and bespoke payloads still require adapters and glue software, reducing operational flexibility.

Another key challenge is the reliability and explainability of on-board analytics customers to trust automated detections and classifications, particularly in safety or life-critical contexts. False positives or unexplainable AI decisions can erode confidence and create liability issues. Data management is complex as high-resolution sensors generate huge datasets that strain storage, transmission, and analytics pipelines, requiring robust edge filtering and secure cloud workflows. Operationally, scaling beyond pilot projects, demands mature maintenance, spare-part provisioning, and trained personnel; many organizations underestimate the people and process changes required. Finally, cybersecurity is also rising concern as payloads that transmit sensitive imagery, telemetry, or intercepted signals are attractive targets, and securing the full stack firmware, communications, cloud is complex and resource-intensive. Overcoming these challenges will require industry standards, stronger integrations, robust validation of analytics, and investment in operational maturity.

SEGMENTATION ANALYSIS

By Class

Increased Demand for Tactical UAVs (MALE & HALE) Driven by Need for Persistent Surveillance and Multi-Role Combat Capabilities

By class, the market is segmented into micro UAVs (below 2 Kg), mini UAVs (2-20 Kg), small UAVs (20-50 Kg), and tactical UAVs (MALE & HALE).

The tactical UAVs ((MALE) and (HALE)) segment will capture the largest market with a share of 43.51% in 2026, the segment is anticipated to dominate with 43.32% share. The Medium Altitude Long Endurance (MALE) and High Altitude Long Endurance (HALE) UAV segments are witnessing strong demand in the market due to their ability to carry heavier, more sophisticated payloads over extended durations. These UAVs are critical assets for militaries as they provide persistent surveillance, reconnaissance, and strike capabilities, often operating in contested or hard-to-reach environments.

The small UAVs (20-50 Kg) segment is expected to grow at a CAGR of 17.4% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Rotary-Wing Drone Payloads Dominates due to VTOL Capability and Operational Versatility

The platform segment is classified into fixed-wing and rotary-wing.

The rotary-wing segment will capture the largest market with a share of 73.26% in 2026. In 2025, the segment is anticipated to dominate with 73.21% share. The rotary-wing segment holds a strong and growing share in market due to its inherent ability to perform vertical take-off and landing (VTOL), hover in place, and operate effectively in confined or rugged environments. These capabilities make rotary drones highly valuable for missions requiring close-range observation, rapid deployment, and high maneuverability.

The fixed-wing segment is expected to grow at a CAGR of 17.1% over the forecast period.

By Payload Type

Rising Demand for EO/IR Drone Payloads Driven by Enhanced Surveillance and Targeting Capabilities

The Payload Type segment is classified into EO/IR, cameras, search and rescue, signal intelligence, electronics intelligence, laser sensors, CBRN sensors, and others.

The EO/IR segment will capture the largest market with a share of 23.34% in 2026. In 2025, the segment is anticipated to dominate with 23.29% share. The Electro-Optical/Infrared (EO/IR) payload segment is experiencing growth in the market due to its critical role in providing high-resolution imaging, day-night surveillance, and precision targeting across both military and commercial applications. EO/IR sensors enable drones to detect and track objects in diverse environmental conditions, including low light, fog, or smoke, making them indispensable for intelligence, surveillance, and reconnaissance (ISR) missions.

The cameras segment is expected to grow at a CAGR of 20.2% over the forecast period.

By Application

Combat and Combat Support Missions Segment Leads Market Owing to Modern Warfare Needs and Rising Demand for Advanced Combat Support Capabilities

By application, the market is classified into perimeter security & border management, combat and combat support missions, situational awareness, disaster management & first responders, surveying, mapping, & monitoring, precision agricultural management, power station management, asset & operations management, emergency medical logistics, and others.

The combat and combat support missions segment will capture the largest market with a share of 28.66% in 2026. In 2025, the segment is anticipated to dominate with 28.56% share. The combat and combat support missions segment is one of the most significant demand generators in the market. Modern military operations increasingly depend on unmanned systems equipped with advanced payloads to enhance situational awareness, precision targeting, and survivability. For combat missions, drones carry electro-optical/infrared (EO/IR) cameras, synthetic aperture radar (SAR), laser designators, and weaponized payloads for strike roles, allowing forces to engage targets with precision while minimizing risks to personnel.

The emergency medical logistics segment is expected to grow at a CAGR of 21.8% over the forecast period.

DRONE PLAYLOAD MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, Middle East & Africa and Latin America.

North America

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 3.66 billion in 2025, representing 34.12% of the global industry, and is expected to reach USD 4.19 billion in 2026. North America leads the global market due to high defense spending, advanced UAV programs, and rapid adoption of commercial drones in agriculture, energy, and logistics. The U.S. and Canada focus on ISR, EO/IR, and precision payloads, supported by robust R&D and regulatory frameworks that enable large-scale deployment and innovation.

U.S. Drone Payload Market

In 2025, U.S. market is estimated to reach USD 3.51 billion. The U.S. leads the market due to substantial defense investments, advanced UAV programs, and growing commercial adoption in agriculture, energy, infrastructure inspection, and logistics. High demand for EO/IR, LiDAR, thermal, and multi-sensor payloads is driven by the need for precise intelligence, surveillance, and operational efficiency.

Europe

During the forecast period, Europe recorded a market size of USD 2.53 billion in 2025, capturing 23.57% of the global market share, and is projected to reach USD 2.92 billion in 2026. Europe exhibits steady demand driven by modernization of military forces, security surveillance, and industrial applications. Countries such as Germany, France, and the U.K. invest in rotary- and fixed-wing drones equipped with EO/IR, LiDAR, and thermal payloads, emphasizing interoperability, regulatory compliance, and integration with existing defense and industrial infrastructures.

Asia Pacific

In 2025, Asia Pacific represented USD 3.26 billion, accounting for 30.39% of the worldwide market, and is projected to grow to USD 3.8 billion in 2026. The Asia Pacific market is expanding rapidly, fueled by rising defense budgets, growing UAV manufacturing, and commercial adoption in agriculture, mining, and infrastructure monitoring. Nations such as China, India, and Japan prioritize MALE/HALE UAV payloads, advanced imaging systems, and multi-sensor packages to enhance security and operational efficiency.

Middle East & Africa

Middle East & Africa contributed 9.19% to the global market in 2025, with a valuation of USD 0.99 billion, and is projected to reach USD 1.13 billion in 2026. The Middle East shows increasing demand for drone payloads for border surveillance, defense modernization, and energy infrastructure monitoring. Countries such as UAE, Saudi Arabia, and Israel invest heavily in EO/IR, radar, and ISR payloads to strengthen strategic defense and support regional security operations.

Africa is set to attain the value of USD 555.80 million in 2025. Africa’s drone payload adoption is growing gradually, mainly for border monitoring, anti-poaching, agriculture, and disaster management. While limited by infrastructure and regulatory maturity, countries including South Africa and Kenya are exploring UAV payloads for surveillance and resource management applications.

Latin America

The Latin America market was valued at USD 0.29 billion in 2025, capturing 2.73% of global revenue, and is estimated to reach USD 0.33 billion in 2026. Latin America’s market is developing steadily, with applications in agriculture, mining, and environmental monitoring. Brazil, Mexico, and Chile are adopting EO/IR, LiDAR, and multispectral payloads to optimize resource management, enhance security operations, and improve commercial UAV efficiency.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Expanding Market Growth Through Advanced Payload Innovation and Defense Modernization

The market is shaped by a diverse set of key players ranging from global defense contractors to specialized sensor developers and commercial drone manufacturers. Defense giants such as Lockheed Martin, Northrop Grumman, Thales, Elbit Systems, and Israel Aerospace Industries (IAI) are driving growth by developing advanced ISR, electronic warfare, and combat payloads tailored for military UAVs. On the commercial front, companies such as DJI, Parrot, and Skydio dominate with modular payload systems and AI-enabled imaging for industries including agriculture, construction, and logistics.

Specialized firms including Teledyne FLIR, Velodyne LiDAR, Trimble, and Quantum Systems strengthen the market with thermal imaging, LiDAR, and precision mapping technologies. This growth is fueled by rising investments in defense modernization programs, increasing adoption of drones in industrial applications, and continuous technological innovation. By offering payloads that combine high performance with adaptability, these players are expanding the scope of drone operations across both military and commercial ecosystems.

LIST OF KEY DRONE PAYLOAD COMPANIES PROFILED:

- AeroVironment, Inc. (U.S.)

- Autel Robotics (U.S.)

- Parrot Drone S.A.S. (Switzerland)

- Yuneec (China)

- BAE Systems PLC (U.K.)

- Boeing (U.S.)

- Elbit Systems Ltd. (Israel)

- General Atomics Aeronautical Systems (U.S.)

- Hexagon AB (Sweden)

- Israel Aerospace Industries (Israel)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- SZ DJI Technology Co. Ltd. (China)

- Teledyne Technologies Inc. (U.S.)

- Textron Systems Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- August 2025 - Terra Drone Corporation, a prominent company specializing in drone technology and Urban Air Mobility (UAM), based in Japan, has entered into a sales partnership agreement (hereinafter referred to as "the agreement") with PT. Yanmar Diesel Indonesia (hereinafter referred to as "Yanmar Diesel Indonesia"), a subsidiary of Yanmar Holdings Co., Ltd., for the distribution of its internally developed agricultural drones.

- July 2025 - RRP Defence (RRP Group), via its subsidiary Vimananu, has formed a strategic alliance with the Franco-American company CYGR to create a state-of-the-art drone manufacturing facility in India. This initiative, located in Navi Mumbai, seeks to bolster India’s ‘Make in India’ campaign by producing unmanned aerial vehicles (UAVs) for defence, surveillance, and industrial uses.

- June 2025 - The International Rice Research Institute (IRRI) and Davao Unmanned Aerial Payload Type (DUAS) have reinforced their enduring collaboration by formalizing a Memorandum of Agreement (MOA) at the IRRI Headquarters located in Los Baños, Laguna.

- March 2025 - Leonardo and Baykar have entered into a partnership focused on unmanned technologies. This agreement leverages the industrial synergies and complementary strengths of both companies within the unmanned sector. The joint venture, which is headquartered in Italy, encompasses the design, development, production, and maintenance of unmanned aerial systems.

- July 2024 - Thales, a worldwide leader in the aerospace sector, along with Garuda Aerospace, has entered into a Memorandum of Understanding (MoU) to enhance the development of the drone ecosystem in India. This partnership is designed to encourage innovation and to propel the advancement of technological Payload Type that facilitate safe and secure drone operations, thereby supporting the expansion of drone-based applications in India.

REPORT COVERAGE

The research report on the growth of the Drone Payload market offers a comprehensive analysis by pinpointing the major companies, product categories, and primary applications within the market. Furthermore, the report outlines market trends and significant advancements in this sector. Alongside the previously mentioned elements, the report encompasses various factors that have played a role in the accelerated market growth observed in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTES | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.42% from 2026-2034 |

| Unit | Value (USD Billion) |

|

Segmentation By Region |

By Class

|

|

By Platform

|

|

|

By Payload Type

|

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says the market value stood at USD 10.72 billion in 2025 and is estimated to reach USD 41.71 billion by 2034.

The market is growing at a CAGR of 16.42% during the projection period (2026-2034).

The Tactical UAVs (MALE & HALE) segment is estimated to be the leading segment in this market during the forecast period.

The Rotary-Wing segment is estimated to be the leading segment in this market during the forecast period.

AeroVironment, Inc. (U.S.), Autel Robotics (U.S.), Parrot Drone S.A.S. (Switzerland), Yuneec (China), BAE Systems PLC (U.K.) are some of the leading OEMs in the market.

North America is projected to be the largest shareholder in the market.

- 2021-2034

- 2025

- 2021-2024

- 80

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us