Dry Bulk Shipping Market Size, Share & Industry Analysis, By Commodity (Iron Ore, Coal, Grains, Bauxite, and Others), By Vessel (Capesize, Panamax, Supramax, and Others), By Design (Gearless Bulk Carriers, Conventional Bulkers, Combined Bulk Carriers, and Others), By Operation (Owned Fleet and Chartered Fleet), By Trade Route (Long-Haul Trade and Short-Sea Trade), and Regional Forecast, 2026-2034

Dry Bulk Shipping Market Size and Future Outlook

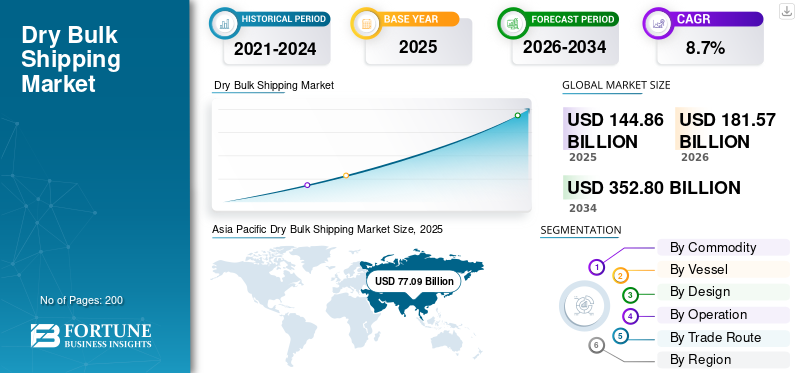

The global dry bulk shipping market size was valued at USD 144.86 billion in 2025. The market is projected to grow from USD 181.57 billion in 2026 to USD 352.80 billion by 2034, exhibiting a CAGR of 8.7% during the forecast period. Asia Pacific dominated the dry bulk shipping market with a market share of 53.22% in 2025.

Dry bulk shipping covers the transportation of unpackaged, bulk commodities such as coal, iron ore, grain, bauxite, cement, and fertilizers via specialized vessels including Capesize, Panamax, Supramax, and Handysize ships. It facilitates the international trade of raw materials essential for energy production, steel manufacturing, agriculture, and construction, operating through charter agreements and spot contracts across major global maritime trade routes.

Key drivers of the market include the rising global demand for raw materials such as iron ore, coal, and grains, growth in steel production and infrastructure development, and expanding energy consumption. The increasing agricultural trade, industrialization in emerging economies, favorable trade policies, and fleet capacity utilization influenced by freight rates and vessel supply-demand dynamics are additional factors supporting industry expansion.

Major players in the market include Oldendorff Carriers, Star Bulk Carriers, Golden Ocean Group, Pacific Basin Shipping, Cargill Ocean Transportation, and Bunge. These players compete through fleet expansion, fuel-efficient vessels, long-term charter agreements, digital voyage optimization, and strategic global trade route positioning.

Download Free sample to learn more about this report.

DRY BULK SHIPPING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 144.86 Billion

- 2026 Market Size: USD 181.57 Billion

- 2034 Forecast Market Size: USD 352.80 Billion

- CAGR: 8.7% from 2026–2034

- Asia Pacific dominated the dry bulk shipping market with a 53.22% share in 2025.

- The grains segment led the market due to strong global demand for staple agricultural commodities.

- Capesize vessels dominated the market owing to their large cargo capacity for iron ore and coal transportation.

Asia Pacific

Asia Pacific led the global market, supported by strong steel production, rising coal imports, expanding grain consumption, and rapid industrialization across China and India.

Europe

Europe is the second-largest market and is projected to grow at a CAGR of 8.6%, driven by grain imports, short-sea trade, and industrial commodity shipments.

North America

North America maintains a significant market position due to robust grain, coal, and mineral exports supported by well-established export terminals.

U.S.

The dry bulk shipping market is projected to reach USD 18.30 billion in 2026.

Japan

The market continues to benefit from substantial imports of iron ore, coal, and other raw materials required for steel production, manufacturing, and energy generation.

Read More

DRY BULK SHIPPING MARKET TRENDS

Long-Term Charter Agreements and Strategic Fleet Modernization Emerge as Key Market Trends

A notable trend in the market is the growing preference for long-term charter agreements combined with fleet modernization strategies. Cargo owners increasingly seek stable freight costs and reliable supply chains, prompting shipowners to secure time-charter contracts that ensure predictable revenue streams. At the same time, companies are phasing out older vessels and investing in modern, fuel-efficient ships equipped with advanced ballast water treatment systems and emission-reduction technologies. This approach improves operational reliability while aligning with evolving regulatory standards. Financial institutions are also favoring environmentally compliant vessels when extending credit, reinforcing modernization efforts. The shift toward long-term partnerships and technologically advanced fleets reflects a strategic move toward stability, efficiency, and sustainable growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Infrastructure and Steel Production to Accelerate Bulk Commodity Trade

The surging infrastructure development and urbanization across emerging and developed economies are significantly driving the dry bulk shipping market growth. The large-scale construction of roads, bridges, railways, ports, and residential complexes requires substantial volumes of steel and cement, increasing the seaborne trade of iron ore, coking coal, and limestone. Countries in Asia Pacific, the Middle East, and Africa are investing heavily in industrial corridors and energy projects, further stimulating raw material imports. Additionally, government-backed stimulus packages aimed at strengthening domestic manufacturing continue to boost steel output. As steel mills depend on consistent shipments of raw materials, the demand for Capesize and Panamax vessels remains strong. This sustained industrial activity directly supports higher fleet utilization and freight rate stability.

- In January 2026, World Steel Association reported India’s 2025 crude steel output rose 10.4% YoY to 164.9 Mt and projected 9% steel demand growth in 2026, supporting the continued seaborne flows of iron ore and coking coal.

MARKET RESTRAINTS

Freight Rate Volatility and Cyclical Trade Patterns to Restrain Market Stability

The market is highly cyclical and sensitive to fluctuations in freight rates, which can significantly restrain revenue predictability for shipowners and operators. Freight rates are influenced by the global commodity demand, vessel supply imbalances, geopolitical tensions, and macroeconomic slowdowns. Periods of oversupply in vessel capacity often lead to sharp declines in charter rates, pressuring profit margins and limiting new investments. Additionally, unexpected disruptions such as trade sanctions, port congestion, or global economic uncertainty can weaken cargo volumes. The industry’s reliance on a limited number of major commodities further amplifies vulnerability to demand swings. Such volatility creates financial risk, complicates long-term planning, and affects capital expenditure decisions across the dry bulk shipping ecosystem.

MARKET OPPORTUNITIES

Digital Fleet Optimization and Decarbonization Investments to Create Growth Opportunities

The increasing adoption of digital technologies and sustainability initiatives presents substantial market growth opportunities. Shipowners are investing in voyage optimization software, real-time performance monitoring systems, and predictive maintenance tools to enhance fuel efficiency and reduce operating costs. The integration of artificial intelligence and advanced analytics enables better route planning, minimizing idle time and bunker consumption. Simultaneously, tightening environmental regulations from the IMO are encouraging investments in energy-efficient vessel designs, scrubbers, and alternative fuels such as LNG and biofuels. Companies that modernize fleets and adopt green shipping practices can secure premium charter contracts and strengthen relationships with environmentally conscious cargo owners. These advancements improve compliance and also enhance long-term competitiveness.

MARKET CHALLENGES

Stringent Environmental Regulations and Compliance Costs to Pose Operational Challenges

Stringent environmental regulations continue to pose significant operational challenges for dry bulk shipping companies. The International Maritime Organization’s emission control mandates, carbon intensity indicators, and sulfur cap requirements demand substantial investments in cleaner fuels, exhaust gas cleaning systems, and energy-efficient retrofits. Compliance often involves high capital expenditure and increased operational costs, particularly for operators with aging fleets. Smaller shipowners may face financial strain when upgrading vessels or meeting evolving reporting requirements. Furthermore, uncertainties surrounding future decarbonization pathways and fuel availability complicate long-term fleet planning decisions. Balancing regulatory compliance with profitability remains a complex task, requiring careful financial management, technological upgrades, and proactive sustainability strategies to remain competitive in the evolving maritime landscape.

Segmentation Analysis

By Commodity

Strong Agricultural Trade Volumes to Reinforce Grains Segment Dominance

Based on commodity, the market is divided into iron ore, coal, grains, bauxite, and others.

The grains segment dominates the market due to consistent global demand for wheat, corn, soybeans, and other staple crops. Major exporters such as the U.S., Brazil, Argentina, and Ukraine generate steady transoceanic shipments, ensuring continuous vessel utilization across Handysize and Supramax fleets. Seasonal harvest cycles and food security policies further stabilize trade flows. Additionally, rising population and livestock feed demand sustain long-term grain transportation volumes, reinforcing segmental leadership.

The coal segment is projected to expand at a CAGR of 8.1% over the forecast period. The growing energy demand in emerging Asian economies and sustained metallurgical coal requirements for steel production continue to support seaborne coal trade and Panamax vessel deployment.

By Vessel

Large-Volume Iron Ore and Coal Trade to Strengthen Capesize Segment Leadership

In terms of vessel, the market is categorized into Capesize, Panamax, Supramax, and others.

The Capesize segment dominates the market owing to its large cargo-carrying capacity, primarily serving long-haul iron ore and coal routes between major exporting countries such as Australia and Brazil and key importers including China and Japan. These vessels efficiently transport high-volume commodities essential for steel production and energy generation. Strong industrial demand, economies of scale in bulk transport, and stable iron ore trade flows support consistent utilization rates. Their deployment on high-capacity routes reinforces segmental dominance.

The Panamax segment holds a significant share and is projected to expand at a CAGR of 8.4% over the forecast period. Growing coal, grain, and minor bulk shipments through Panama Canal trade routes and diversified cargo flexibility are driving the steady demand for Panamax vessels globally.

By Design

High Cost Efficiency and Suitability for Key Trade Routes to Drive Gearless Bulk Carrier Dominance

Based on design, the market is segmented into gearless bulk carriers, conventional bulkers, combined bulk carriers, and others.

The gearless bulk carriers segment dominates the dry bulk shipping market share due to its cost efficiency and suitability for major port-to-port trade routes equipped with advanced loading and unloading infrastructure. These vessels primarily transport high-volume commodities such as iron ore and coal between developed export and import terminals with shore-based cranes. Lower equipment maintenance requirements, higher cargo capacity, and reduced operational complexity enhance fuel efficiency and turnaround time. Their deployment on long-haul, high-density trade lanes ensures strong utilization rates and stable charter demand, reinforcing their leadership position in the global dry bulk fleet structure.

The conventional bulkers segment represents the second-largest category and is projected to expand at a CAGR of 8.6% over the forecast period. Their onboard crane systems provide greater flexibility to access ports with limited infrastructure, supporting diversified trade routes and emerging market cargo flows.

To know how our report can help streamline your business, Speak to Analyst

By Operation

Operational Flexibility and Asset-Light Strategies to Accelerate Chartered Fleet Dominance

Based on operation, the market is segmented into owned fleet and chartered fleet.

The chartered fleet segment dominates the market as operators increasingly prefer asset-light models to manage capacity in a highly cyclical environment. Time charters and voyage charters provide flexibility to scale operations based on freight rate movements and commodity demand without heavy capital investment in vessel ownership. This approach reduces balance sheet risk while enabling participation across multiple trade routes and cargo types. Major commodity traders and shipping companies rely on chartered tonnage to optimize fleet deployment, enhance route adaptability, and maintain cost control. The ability to quickly adjust fleet size in response to market volatility strengthens the segment’s leading position.

The owned fleet segment holds the considerable market share, supported by long-term asset value appreciation and greater control over vessel operations, maintenance standards, and strategic deployment across core trade routes. The segment is anticipated to expand at a CAGR of 8.4% over the forecast period.

By Trade Route

High-Volume Intercontinental Commodity Flows to Reinforce Long-Haul Trade Dominance

Based on trade route, the market is segmented into long-haul trade and short-sea trade.

The long-haul trade segment dominates the market due to substantial intercontinental transportation of iron ore, coal, and grains between major exporting nations such as Australia, Brazil, and the U.S., and key importing regions including China, Japan, and Europe. These routes typically require Capesize and Panamax vessels operating over extended distances, generating higher freight revenues per voyage. Strong steel production demand and large-scale energy imports further sustain long-haul cargo volumes. Economies of scale, stable trade corridors, and consistent commodity flows ensure high vessel utilization, reinforcing the segment’s leading market position.

The short-sea trade segment represents the considerable market share, supported by regional commodity distribution within Europe, Southeast Asia, and the Mediterranean, enabling flexible cargo movement and faster turnaround cycles for smaller bulk carriers. The segment is poised to expand at a CAGR of 8.1% over the analysis period.

Dry Bulk Shipping Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Dry Bulk Shipping Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to register the fastest growth over the forecast period. Strong steel production in China and India, rising coal imports for power generation, and expanding grain consumption sustain high seaborne commodity volumes. Rapid industrialization, infrastructure investments, and manufacturing expansion across Southeast Asia further boost bulk trade flows. Major import-dependent economies and established port infrastructure ensure consistent vessel deployment, reinforcing regional leadership and accelerated growth.

China Dry Bulk Shipping Market

The China market is estimated to touch around USD 52.86 billion in 2026, accounting for a significant share of the global market revenues. Strong iron ore imports, coal demand, and steel production sustain high Capesize and Panamax vessel deployment.

India Dry Bulk Shipping Market

The India market is estimated to touch around USD 18.35 billion in 2026, accounting for a rising share of global market revenues. Rapid infrastructure expansion, coal imports, and grain trade support the fastest-growing regional demand.

Europe

Europe represents the second-largest market and is projected to grow at a CAGR of 8.6% over the analysis period. The region’s demand is driven by grain imports, intra-regional short-sea trade, and coal and bauxite shipments supporting industrial and energy needs. Strong port connectivity, established maritime networks, and diversified trade partnerships sustain vessel activity. Additionally, increasing focus on energy security and strategic commodity sourcing contributes to stable dry bulk cargo flows across European trade corridors.

Germany Dry Bulk Shipping Market

The Germany market is estimated to touch around USD 11.40 billion in 2026, accounting for a notable share of global market revenues. Industrial raw material imports and established port infrastructure drive steady bulk carrier activity.

U.K. Dry Bulk Shipping Market

The U.K. market is estimated to reach around USD 5.97 billion in 2026, accounting for a moderate share of global market revenues. Mediterranean short-sea trade and grain imports support consistent vessel operations and regional connectivity.

North America

North America holds the third-largest share in the market, supported by significant grain, coal, and mineral exports from the U.S. and Canada. The region plays a crucial role in supplying agricultural commodities to Asia and Europe. Established export terminals along the Gulf Coast and Pacific Northwest facilitate high-volume shipments. Stable mining activity and strong trade agreements further maintain steady demand for bulk carrier deployment across long-haul routes.

U.S. Dry Bulk Shipping Market

The U.S. market is estimated to reach around USD 18.30 billion in 2026, accounting for a significant share of global market revenues. Strong grain and coal exports from Gulf Coast terminals sustain long-haul bulk trade volumes.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, demonstrates steady growth driven by mineral exports, iron ore shipments, and rising infrastructure investments. Brazil remains a major iron ore exporter, while Middle Eastern countries import grains and export industrial minerals. Expanding port development projects and resource-based economies contribute to increasing dry bulk trade volumes, supporting gradual market expansion across emerging maritime corridors.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players’ Emphasis on Fleet Expansion, Charter Strategy, and Operational Efficiency to Strengthen their Edge

The dry bulk shipping market is highly fragmented and competitive, characterized by the presence of global fleet operators, regional shipping companies, and commodity trading firms. Leading players such as Oldendorff Carriers, Star Bulk Carriers, Golden Ocean Group, Pacific Basin Shipping, and Cargill Ocean Transportation compete primarily on fleet size, vessel efficiency, charter coverage, and geographic reach. Companies focus on optimizing time charter equivalents (TCE), improving fuel efficiency, and strengthening relationships with major commodity exporters and importers to secure long-term contracts and stabilize revenue streams.

Strategic initiatives such as fleet modernization, mergers, and acquisitions, and long-term charter agreements are central to competitive positioning. Market participants are increasingly investing in fuel-efficient vessels and digital voyage optimization tools to reduce operating costs and comply with environmental regulations. Financial discipline, balance sheet strength, and access to capital markets also play a critical role in sustaining competitiveness during freight rate volatility. Additionally, diversified cargo portfolios and global trade route presence enable companies to mitigate regional demand fluctuations and maintain operational resilience.

LIST OF KEY DRY BULK SHIPPING COMPANIES PROFILED

- Bahri (Saudi Arabia)

- COSCO Shipping Bulk (China)

- Diana Shipping (Greece)

- Eastern Bulk (Norway)

- Genco Shipping & Trading (U.S.)

- Golden Ocean (Bermuda)

- Oldendorff Carriers (Germany)

- Pacific Basin (Hong Kong)

- Polsteam (Poland)

- Star Bulk (Greece)

- Cargill Ocean Transportation (Singapore)

- Bunge (U.S.)

KEY INDUSTRY DEVELOPMENTS

- February 2026: Diana Shipping Inc. entered a time charter contract with Tokyo-based Nippon Yusen Kabushiki Kaisha, through a separate fully-owned subsidiary, for one of its Post-Panamax dry bulk vessels, the m/v Phaidra.

- January 2026: Star Bulk Carriers announced the delivery of two fuel-efficient Newcastlemax bulkers equipped with scrubber systems, strengthening its Capesize fleet capacity and enhancing compliance with IMO emission regulations across long-haul iron ore trade routes.

- December 2025: Golden Ocean Group secured a series of time charter agreements for Capesize vessels with major commodity traders, improving revenue visibility and increasing fleet utilization amid strengthening iron ore shipments to Asia.

- November 2025: Oldendorff Carriers expanded its transatlantic grain logistics program, enhancing vessel deployment between South America and Europe to support rising agricultural export volumes during the peak harvest season.

- October 2025: Navios Maritime Partners L.P. announced its sale of two dry bulk vessels and agreed to sell one tanker vessel, took delivery of one tanker vessel, and chartered out three containerships and two tanker vessels.

- October 2025: Pacific Basin Shipping reported the acquisition of four modern Supramax vessels, reinforcing its minor bulk trade presence and improving operational efficiency through fleet renewal initiatives.

- September 2025: Cargill Ocean Transportation implemented advanced voyage optimization software across its chartered fleet, aiming to reduce fuel consumption and carbon emissions while improving time charter equivalent earnings.

REPORT COVERAGE

The global dry bulk shipping market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.7% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Commodity, By Vessel, By Design, By Operation, By Trade Route, and By Region |

| By Commodity |

|

| By Vessel |

|

| By Design |

|

| By Operation |

|

| By Trade Route |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 144.86 billion in 2025 and is projected to reach USD 352.80 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 77.09 billion.

The market is expected to exhibit a CAGR of 8.7% during the forecast period of 2026-2034.

The gearless bulk carriers segment leads the market by design.

Rising infrastructure and steel production is a key factor driving the market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us