Eco-friendly Food Packaging Market Size, Share & Industry Analysis, By Material (Biodegradable, Recyclable, and Compostable), By Product Type (Trays & Containers, Bags & Pouches, Boxes & Cartons, Bottles & Jars, and Others), By End Users (Food Service, Retail, and Food Processing), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

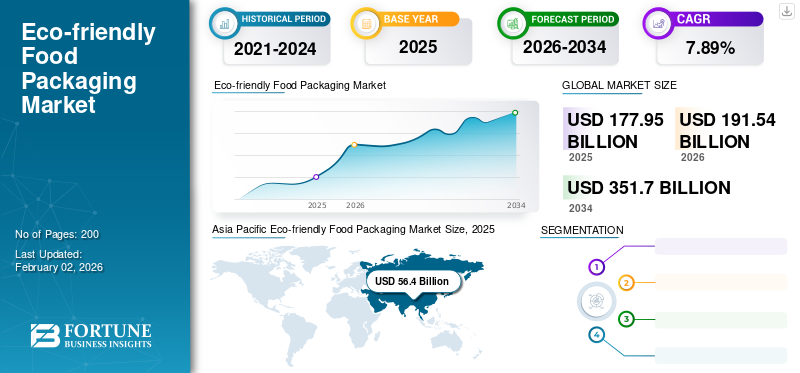

The global eco-friendly food packaging market size was valued at USD 177.95 billion in 2025 and is projected to grow from USD 191.54 billion in 2026 to USD 351.70 billion by 2034, exhibiting a CAGR of 7.89% during the forecast period. Asia Pacific dominated the eco-friendly food packaging market with a market share of 31.69% in 2025.

Eco-friendly food packaging consists of sustainable materials designed to reduce environmental impact through aspects such as sourcing, design, and management after use, particularly emphasizing recyclability, compostability, or reuse. The need for these solutions is swiftly rising, fueled by increasing consumer awareness regarding plastic waste and a demand for more sustainable alternatives.

Furthermore, the market encompasses several major players, Huhtamaki Oyj, Genpak LLC, and Stora Enso, at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

ECO-FRIENDLY FOOD PACKAGING MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 177.95 Billion

- 2026 Market Size: USD 191.54 Billion

- 2034 Forecast Market Size: USD 351.70 Billion

- CAGR: 7.89% from 2026–2034

- Asia Pacific dominated the eco-friendly food packaging market with a 31.69% share in 2025.

- Biodegradable materials are projected to account for 46.86% of the market in 2026.

- Food service is expected to hold a 43.71% market share in 2026.

Asia Pacific

Asia Pacific generated USD 56.40 billion in 2025 and is projected to reach USD 61.23 billion in 2026.

North America

North America accounted for USD 44.08 billion in 2025 and is expected to grow to USD 47.53 billion in 2026.

Europe

Europe recorded USD 35.74 billion in 2025 and is projected to reach USD 38.38 billion in 2026.

U.S.

eco-friendly food packaging market is estimated to reach USD 38.28 billion by 2026.

China

China markets are projected to reach USD 20.22 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growing Environmental Concerns and Stricter Regulations Against Single-Use Plastics Are Driving Market Growth

The market is mainly influenced by heightened environmental awareness and more stringent regulations aimed at ban on single use plastics. Growing consumer consciousness surrounding sustainability goals, waste reduction, and health has led to increased demand for biodegradable, compostable, and recyclable packing materials. Various governments and regulatory agencies around the world are implementing bans on plastic and offering incentives for sustainable packaging, which is motivating food companies to switch to eco-friendly options.

Additionally, the food sector's move toward decreasing its carbon footprint, along with rising demands from health-focused and environmentally-conscious consumers, is encouraging companies to innovate with packaging materials such as paper, plant based packaging, and edible films. Moreover, the increasing demand for sustainable packaging solutions also boosts the market expansion. Furthermore, the growth of e-commerce and food delivery services has heightened the rising demand for sustainable packaging solutions that maintain food quality while reducing environmental harm. It thus drives the global eco-friendly food packaging market growth.

MARKET RESTRAINTS

High Production Cost of Sustainable Packaging Materials Hinders Market Growth

One of the major restraints for the eco-friendly food packaging sector is the elevated production costs associated with sustainable packaging materials in comparison to traditional plastics. Materials that are biodegradable and compostable, such as PLA (polylactic acid), films derived from seaweed, or molded fiber, frequently necessitate advanced processing technologies, specialized infrastructure, and higher raw material expenses, making them less economically viable for mass adoption. This cost inequality presents a considerable obstacle for small and medium-sized food producers, particularly in developing countries where price sensitivity is prominent.

MARKET OPPORTUNITIES

Growing Innovation and Expansion Create Lucrative Growth Opportunities

The market for eco-friendly food packaging offers considerable potential for innovation and growth. Biodegradable plastics and compostable films are creating new revenue opportunities for packaging producers, especially in rapidly expanding regions such as Asia Pacific, where the need for convenient yet sustainable options is increasing. Companies that focus on research and development for affordable and scalable substitutes to traditional plastics are probable to gain a competitive advantage. Collaborations between food brands, packaging manufacturers, and waste management companies to establish circular systems represent another possible area for growth. The rising popularity of plant-based diets and organic products enhances the demand for eco-friendly packaging that aligns with clean-label principles.

ECO-FRIENDLY FOOD PACKAGING MARKET TRENDS

Adoption of Circular Economy Models Emerges as a Key Market Trend

A significant trend in the market for eco-friendly food packaging is the adoption of circular economy principles, which prioritize reusability and closed-loop recycling systems. The incorporation of smart and sustainable packaging innovations, including water-based inks, compostable coatings, and minimalist designs, is also becoming more popular. Plant-based packaging materials sourced from sugarcane, corn starch, and seaweed are emerging as creative alternatives to traditional petroleum-based plastics. Furthermore, there is an increasing focus on lightweight packaging, which minimizes material use while decreasing transportation costs and emissions.

Brands are now more frequently utilizing packaging as a marketing strategy, highlighting eco-labels and "green" certifications to appeal to consumers who prioritize environmental considerations. The trend toward reusable packaging options, such as refillable containers and returnable glass bottles, is being driven by zero-waste retail initiatives and sustainability-focused startups.

MARKET CHALLENGES

Limited Infrastructure for Waste Management and Recycling Challenges Market Growth

A significant challenge is the insufficient infrastructure for waste management and recycling. Even when environmentally friendly packaging is made available, insufficient composting options, outdated recycling systems, and a lack of consumer knowledge regarding appropriate disposal frequently lead to these materials being discarded in landfills. This negates the intended ecological advantages and hampers the pace of adoption. Varying global recycling standards and ineffective collection networks make the situation even more difficult, particularly in developing markets.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Astonishing Benefits Offered by the Biodegradable Material Propel Segment Growth

In terms of material, the market is categorized into biodegradable, recyclable, and compostable.

The biodegradable segment captured the largest share of the market in 2025. In 2026, the segment is anticipating to dominate with a 46.86% share. Biodegradable materials provide considerable advantages for the environment by cutting down on landfill waste, minimizing plastic pollution, and reducing carbon footprints through materials that break down naturally. It also benefits businesses by attracting environmentally-minded consumers and providing flexible, occasionally nutrient-rich, packaging alternatives that aid in fostering a sustainable circular economy. Biodegradable options remove the need for harmful chemicals that may pollute soil and water, safeguarding ecosystems and aquatic life.

The recyclable material segment is expected to grow at a CAGR of 7.72% over the forecast period.

By Product Type

Remarkable Benefits Offered by Trays and Containers Contribute to the Segment Growth

In terms of product type, the market is categorized into trays & containers, bags & pouches, boxes & cartons, bottles & jars, and others.

The trays and containers segment captured the largest Eco-friendly food packaging market share in 2025. In 2026, the segment is anticipating to dominate with a 41.69% share. Eco-friendly food packaging trays and containers provide advantages, including decreasing waste, promoting sustainability, and lowering carbon emissions through the use of renewable, biodegradable, or recycled materials such as sugarcane, bamboo, and paper. These trays are frequently non-toxic, adaptable, budget-friendly, and can improve brand image by attracting environmentally aware customers. The remarkable benefits offered by these trays and containers thus drive the segmental growth.

The bags and pouches product type segment is probable to grow at a CAGR of 7.90% over the forecast period.

By End Users

Growth of Online Food Delivery & Takeaway Boosting the Segmental Growth

Based on end users, the market is segmented into food service, retail, and food processing. In 2025, the global market was dominated by food service in terms of end-users. Furthermore, the segment is projected to hold a 43.71% share in 2026. Services such as Uber Eats, DoorDash, Deliveroo, Swiggy, and Zomato have changed the way people order food, turning takeaway and delivery into a common practice. This change has led to a significant increase in the use of single-use packaging, including plastic containers, utensils, straws, sachets, and bags. With billions of orders processed each year, the environmental impact is substantial. Packaging for food delivery must ensure that meals remain fresh, prevent spills, and provide insulation during transit. Innovative eco-friendly materials (such as bagasse containers, PLA-coated paper cups, and cellulose films) are designed to fulfill these needs while also being biodegradable or compostable. It thus drives the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

In addition, retail end users are projected to grow at a CAGR of 7.53% during the study period.

Eco-friendly Food Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Eco-friendly Food Packaging Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 56.4 billion in 2025, representing 31.69% of the global industry, and is expected to reach USD 61.23 billion in 2026. The adoption of eco-friendly packaging is rapidly expanding in the Asia Pacific region, fueled by its vast population, growing urbanization, and an increasing number of middle-class consumers.

Additionally, the product demand is being propelled by countries such as China, India, and Japan, where governmental initiatives and policies aimed at reducing plastic consumption promote sustainable options. Additionally, the flourishing food delivery and ready-to-eat meal industry, especially in markets such as India and Southeast Asia, serves as another significant catalyst, and is expected to drive the ecofriendly food packaging market during the forecast period. In the region, India and China are both estimated to reach USD 15.42 and USD 20.22 billion each in 2026. In 2026, the Japan market is estimated to reach USD 10.66 billion.

North America

North America maintained a strong presence in the global market, reaching USD 44.08 billion in 2025, accounting for 24.77% share, and is expected to reach USD 47.53 billion in 2026. Other regions, such as the North America and Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, the North America region is projected to record a growth rate of 7.98%, which is the second highest amongst all the regions, and touch the valuation of USD 44.08 billion in 2025. In North America, the market for eco-friendly food packaging is propelled by robust regulatory policies and an increasing consumer demand for sustainable options. The U.S. and Canada are experiencing tougher prohibitions and regulations on single use plastics, prompting food businesses to switch to recyclable and compostable alternatives. The swift growth of e-commerce and food delivery services further drives the necessity for sustainable but resilient packaging that resonates with consumer principles. In 2026, the U.S. market is estimated to reach USD 38.28 billion.

Europe

In 2025, Europe generated USD 35.74 billion, contributing 20.08% to global market revenue, and is projected to grow to USD 38.38 billion in 2026. The market for eco-friendly packaging in Europe is expanding as a result of strict environmental laws, including the EU Green Deal and the Single-Use Plastics Directive. Consumers in Europe are aware of environmental issues, which drives significant demand for packaging solutions that are recyclable, biodegradable, and reusable. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 6.98 billion, Germany to record USD 9.05 billion in 2026, and France to record USD 5.21 billion in 2025.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions would witness a moderate growth in this market. Latin America contributed 14.55% to the global market in 2025, with a valuation of USD 25.89 billion, and is projected to reach USD 27.62 billion in 2026. The food and beverage industry is experiencing rapid growth, and an increasing awareness among consumers regarding reducing environmental impacts, thus encouraging brands to stand out with sustainable packaging. The rising popularity of organic and natural food items is in line with the demand for eco-friendly packaging, consequently fueling market expansion. In 2025, Middle East & Africa represented USD 15.84 billion, accounting for 8.90% of the worldwide market, and is projected to grow to USD 16.78 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

A Wide Range of Product Offerings, coupled with a Strong Distribution Network of Key Companies, Supports their Leading Market Position

The global eco-friendly food packaging market shows a semi-concentrated structure with numerous small- to mid-size companies actively operating across the globe. These players are involved in product innovation, strategic partnerships, and geographic expansion.

Huhtamaki Oyj, Genpak LLC, and Stora Enso are some of the dominating players in the market. A comprehensive range of eco-friendly food packaging products, global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics of these players that support their dominance.

Additionally, other prominent players in the market are Mondi, Smurfit Kappa, Sonoco Products, and others. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with pharmaceutical companies to enhance their market presence.

LIST OF KEY ECO-FRIENDLY FOOD PACKAGING COMPANIES PROFILED

- Huhtamaki Oyj (Finland)

- Genpak LLC (U.S.)

- Stora Enso (Finland)

- Mondi (U.K.)

- Smurfit Kappa (Ireland)

- Sonoco Products (U.S.)

- Biomass Packaging (U.S.)

- Biopak (Australia)

- Amcor (Switzerland)

- Daio Paper Construction (Japan)

- Eco-Products (U.S.)

- Tetra Pak (Switzerland)

- TIPA (Israel)

- Vegware (Scotland)

- Alfipa (Germany)

KEY INDUSTRY DEVELOPMENTS

- July 2025: Mars, Incorporated, a worldwide leader in pet care products and services, advanced its efforts in recyclable pet food packaging by introducing a new mono-material pouch for its WHISKAS brand in Germany and the U.K. These newly designed WHISKAS pouches are intended to be recyclable and align with existing or future recycling systems. The transition to recyclable materials has decreased the packaging's carbon footprint by 46%.

- July 2025: INEOS Styrolution, a global frontrunner in styrenics, has successfully launched its 100% bio-based polystyrene, Styrolution PS 158K BC100. Starting in early 2025, food trays made from this bio-attributed material will be available in the Japanese market through a partnership with a prominent retail chain. It meets global food contact regulations, including the Japanese Food Sanitation Act, and has earned JCII's A certification, which guarantees strict food safety standards.

- June 2025: Mondi, a worldwide leader in sustainable packaging solutions, collaborated with Saga Nutrition, a French producer of pet food, to develop recyclable packaging for Saga’s line of dry pet food. As a component of Mondi's re/cycle portfolio, the re/cycle FlexiBag is intended to fulfill the firm's internal Path to Circularity Scorecard requirements in addition to the CEFLEX recycling guidelines.

- November 2024: Golden Paper, a prominent innovator in sustainable packaging solutions, announced the introduction of its latest line of eco-friendly kraft paper products. Created from entirely recycled materials and manufactured through environmentally conscious processes, this new range is aimed at satisfying the increasing need for sustainable options in packaging and various other sectors, providing companies with a high-performance solution that has a reduced environmental impact.

- November 2023: Rottneros Packaging, a leader in sustainable fiber-based solutions, is set to introduce a new collection of eco-friendly food trays intended to address the increasing need for sustainable packaging in the food sector. These cutting-edge trays are designed to substitute traditional plastic packaging, providing a renewable and biodegradable option that reflects current sustainability trends.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.89% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Product Type, End Users, and Region |

|

By Material |

· Biodegradable · Recyclable · Compostable

|

|

By Product Type |

· Trays & Containers · Bags & Pouches · Boxes & Cartons · Bottles & Jars · Others |

|

By End Users |

· Food Service · Retail · Food Processing |

|

By Geography |

· North America (By Material, Product Type, End Users, and Country) o U.S. o Canada · Europe (By Material, Product Type, End Users, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Product Type, End Users, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Product Type, End Users, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Product Type, End Users, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 191.54 billion in 2026 and is projected to reach USD 351.70 billion by 2034.

In 2025, the market value stood at USD 56.4 billion.

The market is expected to exhibit a CAGR of 7.89% during the forecast period of 2026-2034.

The trays and containers segment led the market by product type.

The key factors driving the market growth are the growing environmental concerns and stricter regulations against single-use plastics.

Huhtamaki Oyj, Genpak LLC, Stora Enso, Mondi, Smurfit Kappa, and Sonoco Products are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

An increase in demand from the food service sector is one of the factors that is expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us