Green Packaging Market Size, Share & Industry Analysis, By Material (Paper & Paperboard, Plastic, Metal, and Others), By Packaging Type (Recycled Content Packaging, Reusable Packaging, and Degradable Packaging), By End-use Industry (Food & Beverages, Healthcare, Personal Care & Cosmetics, Consumer Goods, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

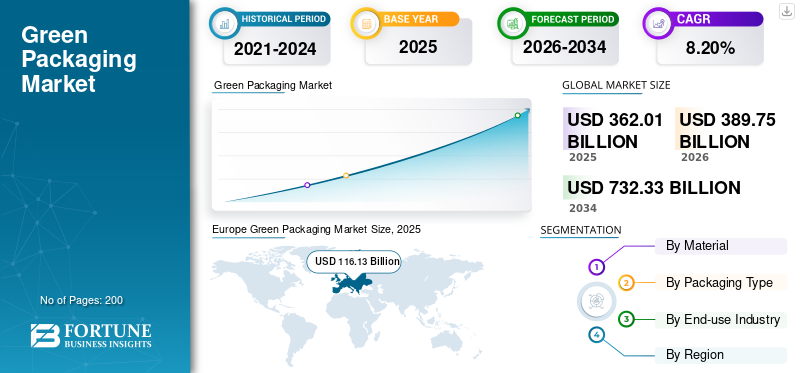

Green Packaging Market Size and Future Outlook

The global green packaging market size was valued at USD 362.01 billion in 2025. The market is projected to grow from USD 389.75 billion in 2026 to USD 732.33 billion by 2034, exhibiting a CAGR of 8.20% during the forecast period. Europe dominated the global green packaging market with a market share of 32.08% in 2025.

Green packaging refers to the use of sustainable materials and design methodologies that aim to minimize environmental impacts throughout the entire product life cycle. It emphasizes the importance of reducing resource use, minimizing carbon emissions, and curtailing waste. This process is implemented by using recyclable, biodegradable, compostable, reusable, or renewable materials. The primary driver of the market’s growth is the combined impact of stringent environmental regulations and rising consumer and business sustainability awareness.

Many key industry players, such as Amcor plc, Sonoco Products Company, and Tetra Pak, are focusing on developing innovative products, aimed at reducing plastic waste, and conducting R&D.

Download Free sample to learn more about this report.

Green Packaging Market Key Takeaways

- 2025 Market Size: USD 362.01 billion

- 2026 Market Size: USD 389.75 billion

- 2034 Forecast Market Size: USD 732.33 billion

- CAGR: 8.20% from 2026–2034

- Europe dominated the green packaging market with a 32.08% share in 2025.

- The plastic segment is projected to grow at a 7.84% CAGR during the forecast period.

- The reusable packaging segment is projected to register a 8.03% CAGR over the forecast period.

Europe

Europe reached USD 116.13 billion in 2025 and is projected to record the highest regional CAGR of 7.83%.

North America

North America generated USD 90.14 billion in 2025, supported by strong regional demand.

Asia Pacific

Asia Pacific reached USD 76.71 billion in 2025, ranking as the third-largest regional market.

U.S.

The market reached USD 73.37 billion in 2025, driven by strong regional demand.

Japan

The market generated USD 13.65 billion in 2025, accounting for 3.77% of global sales.

Read More

GREEN PACKAGING MARKET TRENDS

Circular Economy, Material Innovation, and Minimalism Emerges as a Key Trend

Several significant trends are shaping the global green packaging industry. One prominent trend is the transition toward circular economy practices, where packaging is designed for reuse, facilitates easy recycling, and aims to minimize environmental impact throughout its lifecycle. Companies are increasingly incorporating eco-design principles, such as light weight and recycled materials into their packaging strategies to minimize material consumption and waste.

Additionally, there is a swift adoption of advanced eco-materials, including plant-based polymers, bagasse, and innovative composites, which help reduce carbon footprints. In conjunction with advancements in material science, minimalist, innovative packaging designs that reduce resource use while enhancing functionality are becoming increasingly popular among both consumers and manufacturers. These trends signify a market moving away from conventional linear models toward more sustainable, efficiency-focused systems.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Environmental Regulations and Consumer Sustainability Demand Drive Market Growth

A significant force driving the green packaging market growth is the increasing regulatory pressure from governments worldwide to minimize plastic waste and promote the use of sustainable materials. Stringent regulations such as bans on single-use plastics mandates for recycling, and frameworks for extended producer responsibility, are urging manufacturers to transition to recyclable, biodegradable, or compostable packaging options to comply with these laws and avoid fines.

Concurrently, heightened awareness of environmental issues among consumers has led to a greater demand for eco-friendly products. Research shows that a considerable percentage of consumers favor brands that provide sustainable packaging, which in turn encourages companies to embrace greener packaging alternatives, maintain market presence, enhance brand reputation companies, and align with their sustainability objectives.

MARKET RESTRAINTS

Budget Constraints and Infrastructure Limitations to Restrict Market Growth

Despite robust growth momentum, the adoption of green packaging solutions faces significant obstacles, mainly due to higher production and supply chain costs. Sustainable materials, such as bioplastics, compostable films, and recycled polymers, often incur costs that are considerably higher than those of traditional petroleum-based plastics. This is primarily due to their limited manufacturing scale and specialized processing requirements. The cost differential limits adoption among price-sensitive sectors and small to medium-sized enterprises, especially in emerging markets. In addition to cost challenges, the lack of sufficient recycling infrastructure in numerous regions undermines the effectiveness of sustainable packaging systems, diminishing their environmental benefits and reducing economic incentives for widespread implementation.

MARKET OPPORTUNITIES

Expansion in Key End-Use Industries and Innovation Provides Lucrative Opportunities

There are significant opportunities for expansion across various high-impact sectors, particularly in food & beverage, personal care, and electronic commerce packaging, which collectively account for a substantial share of global packaging demand. The rise in online shopping and the growing consumption of ready-to-eat products drives high demand for sustainable packaging solutions, such as biodegradable packaging trays, paper bottles, and plant-based films.

Moreover, advancements in materials science, including next-generation bioplastics, smart packaging technologies, and minimalist designs, are enabling companies to offer more functional and cost-effective green packaging options. These innovations, bolstered by incentives such as tax benefits and sustainability certifications, create a promising environment for investment and product differentiation in the global market.

MARKET CHALLENGES

Supply Chain and Material Performance Issues Emerge as a Major Challenge to Market Growth

Although there are numerous opportunities, the green packaging sector encounters significant operational and technical obstacles. Inefficiencies within the supply chain, such as limited availability of sustainable raw materials and reliance on agricultural feedstocks that are vulnerable to price fluctuations, complicate sourcing and production planning. Additionally, some eco-friendly materials may not yet offer the same barrier properties or durability as traditional packaging, raising concerns about product protection and shelf life and potentially hindering their use in sensitive sectors such as food and pharmaceuticals. These performance deficiencies, coupled with the worldwide variability in recycling practices and infrastructure, continue to hinder adoption rates amid growing environmental demands.

Segmentation Analysis

By Material

Paper & Paperboard is the Preferred Material Owing to its Affordability and Environmental Benefits

Based on material, the market is divided into paper & paperboard, plastic, metal, and others.

The paper & paperboard segment is expected to account for the largest green packaging market share due to its robust environmental benefits, cost efficiency, and extensive recyclability. Materials composed of paper originate from renewable resources and possess established recycling processes in both developed and developing nations, rendering them among the most accessible and scalable sustainable packaging options. In contrast to numerous bio-based plastics, paper & paperboard can be conveniently collected, recycled repeatedly, and reintegrated into the packaging value chain, thereby promoting the goals of a circular economy.

The plastic segment is expected to grow at a CAGR of 7.84% over the forecast period.

By Packaging Type

Consumer Awareness and Preference for Eco-friendly Products Fuels Recycled Content Packaging

Based on packaging type, the market is segmented into recycled content packaging, reusable packaging, and degradable packaging.

In 2025, the recycled content packaging segment dominated the global market. Consumer awareness and preference for eco-friendly products are driving the use of recycled packaging, particularly in regions with robust recycling systems, such as North America, Europe, and certain areas of Asia Pacific. Technological innovations have further improved the quality and functionality of recycled materials, enabling them to compete with traditional packaging in terms of strength, barrier properties, and visual appeal. This synergy of environmental benefits, regulatory compliance, cost efficiency, and enhanced material performance ensures that recycled-content packaging retains a leading role in the green packaging sector.

The reusable packaging segment is projected to grow at a CAGR of 8.03% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Food & Beverages is the Leading End-Use Industry Due to Strict Regulatory Oversight

Based on end-use industry, the market is segmented into food & beverages, healthcare, personal care & cosmetics, consumer goods, and others.

The food and beverages segment is expected to hold a dominant market share over the forecast period driven by its substantial packaging requirements, stringent regulatory scrutiny, and growing consumer preference for sustainable food packaging options. Furthermore, food and beverage companies face significant regulatory requirements to minimize plastic waste and achieve recycling or composting goals, especially in advanced markets. Concurrently, environmentally aware consumers are shaping buying choices, prompting brands to adopt eco-friendly packaging as a crucial element of differentiation and a factor in building brand trust.

The healthcare segment is projected to grow at a CAGR of 7.74% over the forecast period.

Green Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

Europe Green Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the second-largest share in 2024, at USD 83.16 billion, and achieved USD 90.14 billion in 2025. In North America, the market is primarily driven by increasingly stringent environmental regulations and robust corporate sustainability commitments. Both federal and state governments are implementing restrictions on single-use plastics, mandates for recycled content, and Extended Producer Responsibility (EPR) programs, particularly in the U.S. and Canada.

U.S. Green Packaging Market

Owing to North America’s strong contribution and the U.S dominance in the region, the market reached USD 73.37 billion in 2025, accounting for roughly 20.27% of global sales. In the U.S., the market is significantly influenced by corporate commitments to Environmental, Social, and Governance (ESG) standards, sustainability mandates from retailers, and state-level environmental regulations. Prominent retailers and food chains are exerting pressure on suppliers to transition to packaging that is recyclable, reusable, or compostable, to fulfill their internal sustainability goals.

Europe

Europe is projected to grow at a CAGR of 7.83% over the coming years, the highest among all regions, and reached a valuation of USD 116.13 billion in 2025. Europe is primarily driven by sustainability initiatives guided by policy and a well-established circular economy framework. The area benefits from robust regulatory coherence with EU directives, including targets to reduce packaging waste, recycling quotas, and prohibitions on non-recyclable materials.

U.K. Green Packaging Market

The U.K. market captured USD 20.56 billion in 2025, representing approximately 5.68% of global revenues.

Germany Green Packaging Market

Germany hit USD 29.16 billion in 2025, equivalent to around 8.06% of global sales.

Asia Pacific

Asia Pacific reached USD 76.71 billion in 2025 and secured third position in the market. In the region, India and China reached USD 19.78 billion and USD 23.76 billion, respectively in 2025. The region’s market expansion is driven by rapid urbanization, rising disposable incomes, and the growth of the packaged food and e-commerce sectors. China, India, and those in Southeast Asia are experiencing a rise in packaged goods consumption, leading to increased packaging volumes and greater environmental strain.

Japan Green Packaging Market

In 2025, Japan generated 3.77% of global sales with a valuation of USD 13.65 billion. A significant cultural emphasis on resource efficiency, waste minimization, and rigorous recycling practices drives Japan's market. Government initiatives that promote a circular economy, combined with consumer demands for eco-friendly packaging, continue to foster consistent adoption across the food, electronics, and consumer goods industries.

China Green Packaging Market

The Chinese market is projected to be among the largest worldwide, with 2025 revenues at USD 23.76 billion, representing roughly 6.56% of global sales.

India Green Packaging Market

India’s market registered USD 19.78 billion in 2025, accounting for roughly 5.46% of global revenues.

Latin America and the Middle East & Africa

Latin America reached a valuation of USD 49.85 billion in 2025 and is expected to witness moderate growth during the forecast period. The market in Latin America is driven by rising concerns about waste management and growing acceptance among Fast-Moving Consumer Goods (FMCG) companies. The growth of urban populations, consumer demands for eco-friendly packages, and the constraints on landfill capacity are prompting governments to implement regulations to reduce plastic waste and enhance recycling.

In the Middle East & Africa, South Africa achieved USD 8.61 billion in 2025.

Saudi Arabia Green Packaging Market

Saudi Arabia reached approximately USD 10.08 billion in 2025, accounting for roughly 2.78% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Expanding Product Launch and Acquisitions Propelling Market Progress

The global green packaging market has a semi-consolidated structure, with prominent players including Amcor plc, Sonoco Products Company, and Tetra Pak. The significant market share of these companies is due to numerous strategic initiatives, including collaborations among operating entities to advance research.

For instance, in July 2025, Kotányi incorporated Sonoco’s 94% paper-based GreenCan into its latest spice collection, aiming to promote greater recyclability and align with the EU Green Deal’s life-cycle strategy for circularity. It has been reported that the body and lid of Sonoco’s GreenCan are made of 94% paper, of which 69% is recycled. The remaining 6% consists of barrier protection, a design feature that safeguards the product from moisture, oxygen, and other external elements while maintaining the pack’s recyclability.

Other notable players in the global market include Sealed Air, DS Smith, and Mondi. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY GREEN PACKAGING COMPANIES PROFILED

- Amcor plc (Switzerland)

- Sonoco Products Company (U.S.)

- Tetra Pak (Norway)

- Sealed Air (U.S.)

- DS Smith (U.K.)

- Mondi (U.K.)

- Tipa Ltd. (Israel)

- DuPont (U.S.)

- Greenpackaging Kft (India)

- Econovus (India)

- Pont Green (Netherlands)

- Greedot Biopack Pvt. Ltd. (India)

- Ball Corporation (U.S.)

- Nampak Ltd (South Africa)

- Pactiv Evergreen (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Sabert Corporation Europe introduced its PULPUltra food packaging solution across Europe and the U.K. & Ireland, specifically designed for fresh ready-to-eat meals and hot foods, and composed of over 95% bagasse fibers. Having already been launched in Ireland with customized children’s meal packaging and in France with the Gastronorme range, this solution - which is treated with a barrier spray coating of less than 5% - is reported to provide ‘exceptional’ oil and grease resistance (OGR) permeation in direct contact with hot food applications.

- December 2025: Tetra Pak, in partnership with García Carrión, introduced the inaugural application of its paper-based barrier technology for juice packaging. This advancement in sustainable food packaging solutions represents a crucial move toward diminishing dependence on fossil-based materials, as the new packaging material is now being launched in various markets.

- November 2025: Mondi, a worldwide leader in sustainable packaging and paper, is reinforcing its status as a reliable partner for the food sector with the introduction of an expanded food packaging portfolio. This portfolio now features solid board solutions and digital printing capabilities, a result of the acquisition of Schumacher Packaging, which enhances Mondi's capacity to serve clients throughout Europe. With this advancement, Mondi offers one of the most extensive selections of food packaging on the market, encompassing corrugated and solid board solutions, as well as a complete array of flexible packaging.

- April 2023: Antalis Packaging introduced two new initiatives designed to provide customers with information regarding environmentally friendly products, thereby encouraging them to choose the most suitable eco-friendly solutions. The Green Star System is a classification rating system that Antalis claims is ‘based on a rigorous set of criteria’. Examples of these criteria include recycled materials, sourced materials, and technical recyclability.

- December 2020: Global supplier of flexible packaging and lidding films, KM Packaging, introduced a new line of compostable products. The C-Range of bio-plastic packaging materials encompasses shrink wrap, stretch wrap, adhesive tape, nets, and bags. This addition strengthens KM's collection of sustainable flexible packaging solutions and provides customers with an expanded selection.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.20% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Packaging Type, End-use Industry, and Region |

|

By Material |

· Paper & Paperboard · Plastic · Metal · Others |

|

By Packaging Type |

· Recycled Content Packaging · Reusable Packaging · Degradable Packaging |

|

By End-use Industry |

· Food & Beverages · Healthcare · Personal Care & Cosmetics · Consumer Goods · Others |

|

By Region |

· North America (By Material, Packaging Type, End-use Industry, and Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Germany (By End-use Industry) o U.K. (By End-use Industry) o France (By End-use Industry) o Italy (By End-use Industry) o Spain (By End-use Industry) o Russia (By End-use Industry) o Poland (By End-use Industry) o Romania (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o China (By End-use Industry) o Japan (By End-use Industry) o India (By End-use Industry) o Australia (By End-use Industry) o Southeast Asia (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Latin America (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Brazil (By End-use Industry) o Mexico (By End-use Industry) o Argentina (By End-use Industry) o Rest of Latin America (By End-use Industry) · Middle East & Africa (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Saudi Arabia (By End-use Industry) o UAE (By End-use Industry) o Oman (By End-use Industry) o South Africa (By End-use Industry) o Rest of the Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 362.01 billion in 2025 and is projected to reach USD 732.33 billion by 2034.

In 2025, Europes market value stood at USD 116.13 billion.

The market is expected to exhibit a CAGR of 8.20% during the forecast period.

By material, the paper & paperboard segment is expected to lead the market.

Environmental regulations and consumer sustainability are the key factors that drive market growth.

Amcor plc, Sonoco Products Company, Tetra Pak, and Sealed Air are the major players in the global market.

Europe dominated the market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us