Elastomers Market Size, Share & Industry Analysis, By Type (Thermoset Elastomers and Thermoplastic Elastomers (TPEs)), By Application (Automotive, Industrial, Consumer Goods, Medical, and Others), and Regional Forecast, 2026-2034

ELASTOMERS MARKET SIZE AND FUTURE OUTLOOK

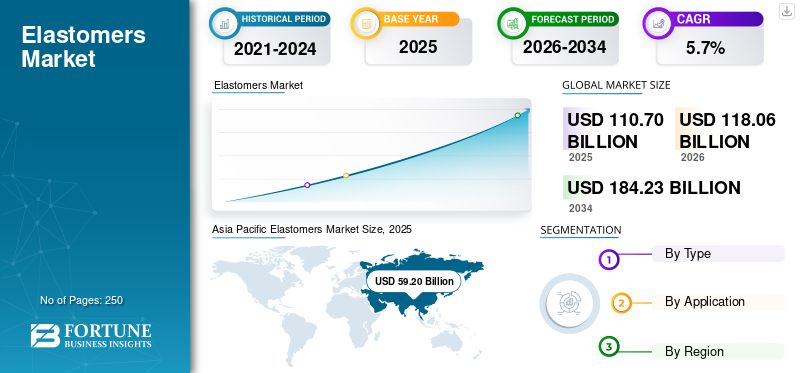

The global elastomers market size was valued at USD 110.70 billion in 2025. The market is projected to grow from USD 118.06 billion in 2026 to USD 184.23 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the elastomers market with a market share of 53.47% in 2025.

Elastomers are polymeric materials characterized by their ability to undergo significant deformation under stress and return to their original shape upon release. This elastic recovery property makes them essential in applications requiring flexibility, resilience, impact resistance, and sealing performance. They are broadly categorized into thermoset elastomers and Thermoplastic Elastomers (TPEs), each offering distinct processing and performance characteristics. Thermoset elastomers provide superior heat and chemical resistance, while TPEs offer recyclability and easier processing. The market is driven by strong demand from automotive, industrial machinery, consumer goods, and medical sectors. Increasing emphasis on lightweight materials, durability, and sustainability further strengthens adoption. As industries seek materials that combine flexibility with mechanical strength, it continues to play a critical role across diverse applications, thus reinforcing the market’s long-term growth trajectory. The major players operating in the market are ExxonMobil Corporation, Dow Inc., BASF SE, LANXESS AG, and Arlanxeo Holding B.V.

Download Free sample to learn more about this report.

Elastomers Market Key Takeaways

- 2025 Market Size: USD 110.70 billion

- 2026 Market Size: USD 118.06 billion

- 2034 Forecast Market Size: USD 184.23 billion

- CAGR: 5.7% from 2026–2034

- Asia Pacific dominated the elastomers market with a 53.47% share in 2025.

- The thermoplastic elastomers (TPEs) segment is projected to grow at a CAGR of 6.4% during the forecast period.

- The medical segment is expected to record the highest CAGR of 6.8% during the forecast period.

Asia Pacific

Asia Pacific led the market, driven by strong automotive manufacturing, industrialization, and infrastructure development.

Europe

Europe maintained a significant position, supported by automotive electrification and demand for sustainable elastomer solutions.

North America

North America showed stable growth, backed by EV production, aerospace applications, and industrial automation.

U.S.

The market was valued at approximately USD 16.53 billion in 2025, supported by EV and aerospace demand.

Japan

The market reached around USD 8.6 billion in 2025, driven by advanced automotive engineering and specialty industrial applications.

Read More

ELASTOMERS MARKET TRENDS

Focus on Sustainability Awareness and Lightweighting Requirements Reshaping Product Innovation

The market is evolving due to growing sustainability awareness and lightweighting initiatives across industries. A key trend is the rising adoption of TPEs as recyclable alternatives to traditional thermoset rubbers. Automotive manufacturers are increasingly incorporating TPEs to reduce vehicle weight and improve fuel efficiency. Additionally, bio-based and recycled elastomer formulations are gaining traction as companies aim to reduce carbon footprints. Advancements in polymer blending technologies are enhancing material performance, expanding use in high-temperature and chemically demanding environments. In the medical sector, demand for hypoallergenic and sterilization-resistant elastomers is rising. These evolving regulatory and performance requirements are reshaping product development strategies, thus driving innovation within the market.

MARKET DYNAMICS

MARKET DRIVERS

Production and Industrial Expansion Primarily Drive Sustained Market Growth

The primary driver of the market is the sustained growth of automotive production worldwide. Elastomers are widely used in tires, seals, gaskets, hoses, and vibration control components. Increasing vehicle production and rising demand for durable and lightweight materials directly support market expansion. Additionally, industrial machinery and construction equipment rely heavily on elastomer components for flexibility and impact resistance. Growth in consumer goods such as footwear and electronics further reinforces demand. Infrastructure development and expanding manufacturing activity in emerging markets also contribute to increased consumption. These structural industrial and consumer trends ensure steady demand, thus supporting sustained growth in the market.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

Raw Material Price Volatility and Environmental Regulations Limiting Profitability

The market faces restraints primarily related to raw material price volatility and environmental regulations. Many elastomers are derived from petrochemical feedstocks, making them sensitive to fluctuations in crude oil prices. Additionally, stringent environmental policies regarding synthetic rubber production and waste management increase compliance costs. Disposal challenges associated with thermoset elastomers limit recyclability and sustainability appeal. Regulatory restrictions on certain additives and chemical components also impact formulation flexibility. These cost and regulatory pressures may reduce profit margins and limit expansion opportunities, hence moderating the overall growth rate of the market.

MARKET OPPORTUNITIES

Electrification and Healthcare Expansion Creating New Growth Avenues

The global shift toward electric mobility and healthcare expansion presents significant opportunities for the market. Electric vehicles require advanced sealing, vibration damping, and thermal management components, increasing elastomer demand. Additionally, growth in renewable energy infrastructure drives applications in cable insulation and industrial equipment. The healthcare sector offers further potential, as they are widely used in medical tubing, syringes, and protective equipment. Emerging economies experiencing rapid industrialization and urbanization are also generating new demand. Technological advancements in specialty elastomers with enhanced durability and chemical resistance broaden application possibilities. These expanding end-use industries create strong elastomers market growth potential, therefore strengthening long-term prospects for the market.

MARKET CHALLENGES

Performance Optimization and Competitive Substitution Influencing Market Dynamics

A key challenge in the market is balancing performance optimization with cost efficiency. End users increasingly demand elastomers that offer high heat resistance, chemical stability, and mechanical durability. Achieving these characteristics often requires advanced formulations and higher production costs. Additionally, competition from alternative materials such as advanced plastics and composites influences purchasing decisions. Ensuring recyclability while maintaining performance also presents technical hurdles. Manufacturers must continuously invest in R&D to remain competitive in evolving application environments. These technological and competitive challenges shape product development cycles, therefore influencing long-term market dynamics.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D efforts focus on developing bio-based elastomers, recyclable TPE formulations, and high-performance specialty rubbers. Innovations aim to improve heat resistance, chemical durability, and lightweight properties. These advancements enhance competitiveness and sustainability positioning.

SEGMENTATION ANALYSIS

By Type

Cross-Linked Molecular Structure of Thermoset Elastomers Delivering Superior Mechanical Stability

Based on type, the market is segmented into thermoset elastomers and Thermoplastic Elastomers (TPEs).

Thermoset elastomers are characterized by a cross-linked molecular structure formed during curing, which provides excellent heat resistance, chemical stability, and long-term mechanical integrity. These materials are widely used in demanding applications such as automotive seals, industrial hoses, gaskets, and vibration dampers. Their resistance to deformation under stress and ability to maintain performance in extreme environments make them suitable for high-temperature and heavy-duty applications. However, thermosets cannot be remelted or reshaped, limiting recyclability. Despite sustainability challenges, performance-driven demand from automotive and industrial sectors sustains strong adoption, thus maintaining thermoset elastomers as a significant segment in the global market.

Thermoplastic elastomers combine the elasticity of rubber with the processing advantages of thermoplastics. Unlike thermosets, TPEs can be melted and reprocessed, supporting sustainable manufacturing and recyclability goals. They are increasingly used in automotive interiors, consumer electronics, medical devices, and footwear due to their lightweight nature and design flexibility. TPEs also offer cost-efficient processing through injection molding and extrusion techniques. Growing environmental awareness and demand for recyclable materials are accelerating their adoption. As industries prioritize lightweight and sustainable solutions, TPEs continue gaining traction, therefore expanding their share within the market. The segment is growing at a CAGR of 6.4% during the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Rapid EV Production and High Energy Density Requirements Driving Automotive Segment Demand

Based on application, the market is segmented into automotive, industrial, consumer goods, medical, and others.

The automotive segment represents the leading elastomers market share in 2025, due to their extensive use in tires, seals, gaskets, hoses, bushings, and vibration control components. They enhance durability, flexibility, and resistance to heat and chemicals in vehicles. Increasing global vehicle production, including electric vehicles, supports sustained demand. Lightweighting initiatives to improve fuel efficiency further drive adoption of advanced elastomer materials. Additionally, stringent safety and performance standards require high-quality sealing and damping components. As electrification and mobility solutions expand, elastomer usage in battery seals and cable insulation increases, thus maintaining automotive as the dominant application segment.

The industrial segment is projected to grow at a CAGR of 5.3% over the study period. They are widely used in industrial machinery, construction equipment, conveyor belts, seals, and hoses. Their flexibility and resistance to wear and chemicals make them suitable for demanding industrial environments. Growth in manufacturing output and infrastructure projects in emerging economies supports steady consumption. Additionally, expansion of energy and mining sectors further reinforces demand for durable elastomer components. Industrial automation and modernization also contribute to replacement demand. While growth is moderate compared to automotive, consistent industrial activity ensures reliable consumption, hence strengthening the industrial segment within the market.

The medical segment is growing at the highest CAGR of 6.8% during the forecast period. Medical applications rely on elastomers for tubing, syringes, gloves, seals, and wearable devices. Biocompatibility, chemical resistance, and flexibility are critical performance factors. Growing global healthcare expenditure and expansion of medical infrastructure support rising demand. Additionally, advancements in minimally invasive procedures and wearable health monitoring devices create new application areas. TPEs are increasingly preferred due to sterilization compatibility and reduced allergenic risks. Strict regulatory compliance ensures high material standards. These healthcare-driven requirements support steady segment expansion, hence reinforcing medical as a growing application area in the market.

ELASTOMERS MARKET REGIONAL OUTLOOK

By region, the market is segmented into Asia Pacific, Europe, North America, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Elastomers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market due to strong automotive manufacturing, rapid industrialization, and infrastructure development. China, India, Japan, and South Korea are major production hubs for vehicles, consumer goods, and industrial equipment, driving significant elastomer demand. Growing middle-class populations and rising disposable incomes further support consumption of consumer products and electronics. Additionally, expansion of construction and energy sectors strengthens demand for industrial-grade elastomers. Cost-competitive manufacturing and integrated petrochemical supply chains enhance regional competitiveness. These structural growth drivers collectively position Asia Pacific as the largest and fastest-growing regional market, thus reinforcing its leadership in the global industry.

China Elastomers Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 30.13 billion, representing roughly 27.2% of global market sales. Growth is driven by large-scale automotive production, infrastructure expansion, and strong domestic petrochemical capacity.

India Elastomers Market

The Indian market size in 2025 was valued at around USD 11.86 billion, accounting for roughly 10.7% of global revenues. Expansion is supported by rising vehicle production, construction growth, and increasing industrial manufacturing output.

Japan Elastomers Market

The Japan market value in 2025 was recorded at around USD 8.6 billion, accounting for roughly 7.8% of global market revenues. Demand is fueled by advanced automotive engineering, high-performance elastomer innovation, and specialty industrial applications.

Europe

Europe’s market is shaped by stringent environmental regulations and rapid automotive electrification. Germany, France, and the U.K. are key automotive hubs driving elastomer demand for seals, gaskets, and vibration control systems. Sustainability initiatives encourage adoption of recyclable TPEs and bio-based formulations. Growth in renewable energy and industrial automation further supports demand. However, regulatory compliance costs and slower economic growth moderate expansion. Despite these constraints, strong industrial base and sustainability alignment ensure steady demand, therefore reinforcing Europe’s relevance in the global market.

U.K. Elastomers Market

The U.K. market in 2025 was valued at around USD 2.45 billion, representing 2.2% of global market revenues. Demand is supported by automotive assembly operations and growing industrial automation investments.

Germany Elastomers Market

Germany’s market size reached approximately USD 5.94 billion in 2025, equivalent to around 5.4% of global market sales. Growth is driven by automotive electrification and adoption of sustainable TPEs.

North America

North America represents a mature yet stable market driven by advanced manufacturing and rising electric vehicle production. The U.S. leads demand due to strong automotive, aerospace, and medical industries. Growth in EV production increases product usage in battery seals and cable insulation. Additionally, infrastructure modernization and industrial automation support steady consumption. The region benefits from established petrochemical supply chains and innovation in specialty elastomers. While growth rates are moderate compared to Asia Pacific, high-value applications and technological advancement sustain demand, hence maintaining North America’s strategic position in the market.

U.S. Elastomers Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was analytically approximated at around USD 16.53 billion in 2025, accounting for roughly 14.9% of global sales. Expansion is supported by EV production growth, aerospace demand, and strong petrochemical supply chains.

Latin America & Middle East & Africa

Latin America shows gradual growth supported by automotive assembly operations and infrastructure projects in Brazil and Mexico. Industrial expansion and consumer goods manufacturing contribute incremental elastomer demand. Although local production capacity is limited, import-driven supply supports consumption. Economic fluctuations may influence growth pace, but long-term infrastructure investments provide stability. These factors contribute to moderate regional expansion, hence strengthening Latin America’s position as a developing market. The Middle East & Africa region is witnessing steady demand driven by infrastructure development, construction growth, and industrial diversification initiatives. They are used in construction materials, industrial hoses, and energy applications. GCC countries are investing in downstream manufacturing and petrochemical expansion, supporting local demand. While automotive production remains limited, industrial and energy sectors provide consistent consumption. These structural developments contribute to gradual regional growth, therefore enhancing the role of the Middle East & Africa region in the market.

GCC Elastomers Market

The GCC market reached a valuation of around USD 2.56 billion in 2025, representing 2.3% of global market revenues. Growth is driven by construction expansion and downstream petrochemical diversification initiatives.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Focus on Sustainable TPEs and Innovation Accelerating Industry Competition

The market is moderately consolidated, characterized by the presence of large multinational chemical companies with vertically integrated petrochemical operations. Competition is driven by product performance, cost efficiency, and innovation in specialty elastomers. Leading players focus on sustainable TPEs and high-performance synthetic rubbers to meet evolving automotive and industrial requirements. Strategic collaborations with OEMs and long-term supply agreements strengthen competitive positioning. Additionally, regional capacity expansions in Asia and the Middle East intensify global competition. High capital investment and feedstock integration create entry barriers, therefore reinforcing the dominance of established manufacturers in the market.

LIST OF KEY ELASTOMERS COMPANIES PROFILED

- ExxonMobil Corporation (U.S.)

- Dow Inc. (U.S.)

- BASF SE (Germany)

- LANXESS AG (Germany)

- Arlanxeo Holding B.V. (Netherlands)

- Kraton Corporation (U.S.)

- Sinopec Corporation (China)

- JSR Corporation (Japan)

- LG Chem Ltd. (South Korea)

- SABIC (Saudi Arabia)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Syensqo launched the industry’s first certified portfolio of elastomers and lubricant fluids produced using renewable and circular raw materials. The initiative supports carbon footprint reduction and enhances sustainability transparency, reinforcing the company’s commitment to circular, high-performance material solutions for mobility and industrial markets.

- July 2025: AGC announced the launch of an innovative fluoroelastomer manufactured without the use of surfactants or fluorinated polymerization solvents. The new product enhances environmental performance while maintaining high heat, chemical, and oil resistance. This development supports sustainable manufacturing practices and strengthens AGC’s advanced elastomer portfolio for automotive and industrial applications.

- March 2025: Nordmann announced a new partnership with WACKER to strengthen distribution and technical support for silicone elastomers. The collaboration aims to expand market reach and enhance customer access to high-performance silicone materials across industrial and specialty applications, reinforcing joint expertise in elastomer solutions.

- February 2025: Prism Worldwide partnered with Sherwood Industries to introduce sustainable TPEs into the extruded rubber market. The collaboration focuses on incorporating recycled content materials to reduce environmental impact while maintaining performance standards, supporting circular economy initiatives within elastomer applications.

- September 2022: Arkema announced an increase in its Pebax elastomer production capacity to meet rising demand from sports, consumer, and advanced mobility applications. The expansion supports growth in lightweight, high-performance materials and strengthens Arkema’s position in specialty elastomers for sustainable and high-value markets.

- May 2021: ENEOS announced the establishment of a new company focused on advanced elastomer materials to strengthen its specialty synthetic rubber The move aims to enhance R&D, production efficiency, and commercialization capabilities, particularly for automotive and industrial applications, supporting long-term competitiveness in high-performance elastomers.

- May 2021: Avient announced the launch of GLS thermoplastic elastomers featuring built-in antimicrobial technology designed to inhibit microbial growth on product surfaces. The new materials target medical, consumer, and high-touch applications requiring enhanced hygiene performance, while maintaining flexibility and durability typical of TPEs.

REPORT COVERAGE

The elastomers market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Additionally, it provides valuable insights into the market and current industry trends, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Million Ton) |

| Growth Rate | CAGR of 5.7% from 2026 to 2034 |

| Segmentation | By Type, Application, Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 110.70 billion in 2025 and is projected to reach USD 184.23 billion by 2034.

Recording a CAGR of 5.7%, the market is slated to exhibit steady growth during the forecast period.

The automotive segment led by application in 2025.

Asia Pacific held the highest market share in 2025.

The production and industrial expansion is the key factor sustaining the market growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us