High Performance Elastomers Market Size, Share & Industry Analysis, By Type (Silicone Elastomers, Polyurethane Elastomers (TPU), Thermoplastic Elastomers (TPE), Hydrogenated Nitrile Butadiene Rubber, Acrylic Elastomers (ACE), Fluoroelastomers (FKM), and Others), By End Use (Automotive, Industrial Manufacturing, Oil & Gas, Electronics, Healthcare, Aerospace & Defense, and Others), and Regional Forecast, 2026-2034

High Performance Elastomers Market Size and Future Outlook

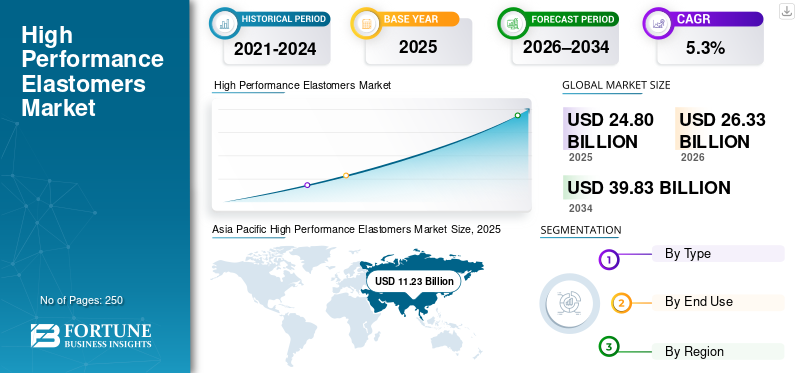

The global high performance elastomers market size was valued at USD 24.80 billion in 2025. The market is projected to grow from USD 26.33 billion in 2026 to USD 39.83 billion by 2034, exhibiting a CAGR of 5.3% during the forecast period. Asia Pacific dominated the global high performance elastomers market with a market share of 45.28% in 2025.

High Performance Elastomers (HPEs) are engineered polymeric materials formulated to retain elasticity while delivering exceptional resistance to heat, aggressive chemicals, fuels, steam, and oxidation. Its exceptional properties offer long-life mechanical cycling under conditions where conventional rubbers rapidly harden, swell, crack, or lose sealing force. They are critical in high-stress sealing and protection roles across automotive and electric vehicles, oil & gas and chemical processing, aerospace, and electronics. As operating temperatures rise, fluid chemistries diversify, and reliability requirements tighten, the demand for HPEs will naturally rise as these materials directly reduce leakage risk, unplanned downtime, and warranty-driven failures.

The global market is driven by a relatively concentrated set of specialty polymer producers and compounders with strong expertise in fluorochemistry, silicone chemistry, and high-durability rubber design. Key players across major HPE families include Avient Corporation, Chemours, Dow, and Evonik AG in fluoroelastomers and perfluoroelastomers. Competitive positioning is strengthened through close collaboration with OEMs and component makers, faster qualification support, and continuous investment in application-specific formulations that reduce leakage risk and improve uptime in critical systems.

Download Free sample to learn more about this report.

HIGH PERFORMANCE ELASTOMERS MARKET TRENDS

Shift Toward Thermoplastic and Fluoroelastomer Grades in Harsh-Environment Accelerates Product Consumption

In harsh environments, customers are increasingly choosing thermoplastic elastomers, where redesign and processing speed matter, and fluoroelastomer families, where chemical resistance is critical. Thermoplastic elastomers can enable faster molding cycles, easier recycling in select use cases, and lighter designs, making them attractive for high-volume parts where moderate performance requirements meet cost and productivity goals. Fluoroelastomers and related high-end grades are preferred for demanding sealing applications exposed to fuels, oils, solvents, and elevated temperatures, where failure risks are costly. This mix shift supports product demand by expanding the use of engineered elastomers across both high-volume and premium components.

- For instance, in January 2026, the prime minister of India said that the nation plans to invest over USD 100 billion in the oil and gas sector by 2030, driving demand for high performance elastomers.

In addition, bio-based elastomers are gaining attention as industries look to reduce dependence on fossil-based raw materials without compromising performance. These materials use renewable feedstocks and are increasingly adopted across the automotive, consumer goods, and selected industrial sectors. While current volumes remain limited, ongoing R&D is improving heat resistance, durability, and processing compatibility.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand from Automotive Industry for High Temperature and Chemical-Resistant Materials to Drive Market Growth

Automotive systems are running hotter and using more aggressive fluids than before, increasing the need for high performance products. Turbocharged engines, advanced transmissions, and tighter under-hood packaging expose seals and hoses to high temperatures, oils, coolants, and fuel blends for long periods. At the same time, e-mobility introduces new stress points, including battery cooling loops, thermal management modules, and electrical insulation requirements, where leakage or swelling can pose safety and warranty risks. OEMs and tier suppliers therefore prefer elastomer grades that maintain elasticity, low compression set, and stable sealing force over long service cycles. Hence, there will be steady growth in premium elastomer products for gaskets, O-rings, hoses, and molded seals in the automotive industry, driving global high performance elastomers market growth during the forecast period.

MARKET RESTRAINTS

Regulatory Pressure and Need for Low-VOC and Sustainable Formulations May Limit Market Expansion

Regulations and customer standards are pushing suppliers to reduce VOCs, hazardous additives, and emissions from elastomer processing and finished parts. While this creates a clear direction, it can also slow market expansion in the short term. Reformulating compounds to meet low-VOC and sustainability targets often requires new raw materials, updated curing systems, and additional testing, which raises development cost and extends qualification timelines. In sensitive applications such as cabin interiors, medical devices, and electronics, buyers may demand low extractables and strict documentation, further increasing compliance efforts. Smaller processors may delay switching due to cost, and some high performance chemistries can face tighter scrutiny. As a result, adoption may be uneven until supply chains stabilize and compliant grades scale efficiently.

MARKET OPPORTUNITIES

Growing Adoption in Aerospace and Medical to Create Lucrative Opportunities in Market

Aerospace and medical applications reward materials that deliver high reliability with strict compliance. In aerospace, elastomers are used in fuel systems, hydraulic seals, door and window seals, vibration isolation, and thermal protection parts, where performance must remain consistent across wide temperature swings, pressure changes, and exposure to fuels and hydraulic fluids. In medical applications, demand is supported by drug-delivery and fluid-handling components, wearable devices, seals, and tubing, where cleanliness, biocompatibility, and low extractables are critical. These sectors typically require lengthy qualification cycles but also offer strong margins once materials are approved. As aircraft production rises and healthcare devices expand, the need for application-specific products and compliant grades can create attractive long-term opportunities in the market.

Segmentation Analysis

By Type

Silicone Elastomers Segment Led Due to Broad Use across Thermal, Sealing, and Electrical-Insulation Applications

Based on type, the market is segmented into silicone elastomers, Polyurethane Elastomers (TPU)

Thermoplastic Elastomers (TPE), hydrogenated nitrile butadiene rubber, Acrylic Elastomers (ACE), Fluoroelastomers (FKM), and others.

The silicone elastomers segment accounted for the largest global high performance elastomers market share in 2025, supported by its wide adoption in high-temperature sealing, electrical insulation, and long-life flexible parts. It serves a wide array of end-use areas, including, but not limited to, automotive, industrial equipment, electronics, and medical. Its ability to maintain elasticity over a broad temperature range, resist weathering/UV exposure, and deliver stable performance in dynamic sealing applications makes it a preferred choice in these areas. As electrification increases and thermal-management systems become more demanding, silicone elastomers continue to remain a core material family, sustaining steady growth through 2034.

Polyurethane Elastomers (TPU) represent the fastest-growing segment, expanding at a 6% CAGR during the forecast period, driven by rising demand for abrasion resistance, toughness, and lightweight design flexibility in automotive interiors/exteriors, cable jacketing, industrial belts/rollers, and select medical and consumer applications. TPU’s processability and design versatility support faster part conversion and higher functional integration, which is increasingly valued as OEMs push for durability, reduced part weight, and improved lifecycle performance.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Automotive Segment Led Due to High-Volume Use in Sealing, Thermal Management, and Under-the-Hood Durability

Based on end use, the market is segmented into automotive, industrial manufacturing, oil & gas, electronics, healthcare, aerospace & defense, and others.

The automotive segment accounted for the largest share in 2025, supported by the heavy use of elastomers in gaskets, O-rings, hoses, boots, mounts, and weather seals across powertrain and chassis systems. Demand is further strengthened by e-mobility, where elastomers are critical in battery cooling circuits, thermal interface sealing, and high-reliability fluid handling. With rising heat loads, stricter leak-prevention requirements, and longer warranty expectations, OEMs continue to prioritize materials that maintain sealing force and resist oils, coolants, and fuels.

Industrial manufacturing is another major end-use segment as elastomers directly support equipment reliability and plant uptime. They are widely used in pumps, valves, compressors, rotating equipment, conveyors, seals, and vibration control parts, where failure can cause shutdowns and high maintenance costs. Growth stays steady at a CAGR of 4.7% during the forecast period as industries modernize equipment, increase automation, and adopt higher-efficiency systems that operate under tighter tolerances.

The healthcare segment continues to expand as medical devices and fluid-handling systems require elastomers with clean performance, low extractables, and consistent mechanical behavior. Applications include seals, diaphragms, tubing interfaces, wearables, and device housings, where material stability is critical for safety and product performance. With a 5.4% CAGR over the projected years, healthcare offers attractive growth for suppliers that can meet compliance requirements and support qualification with device manufacturers.

High Performance Elastomers Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific High Performance Elastomers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 11.23 billion, and is expected to maintain its leading share in 2026, valued at USD 12.00 billion. Asia Pacific’s dominance in the market is underpinned by its large manufacturing base and high downstream consumption across China, Japan, South Korea, and Taiwan, supported by strong clusters in automotive, electronics, industrial manufacturing, and chemical processing. The region benefits from scale-driven production, deep component supply chains, and expanding local OEM output.

China High Performance Elastomers Market

Based on Asia Pacific’s strong contribution and China’s manufacturing strength, the China market is anticipated to record USD 0.51 billion in 2026, accounting for roughly 26% of global revenues.

India High Performance Elastomers Market

The Indian market in 2026 is set to secure USD 1.33 billion. India’s market is driven by rising demand from automotive and EV manufacturing, where durable sealing and thermal-management materials are needed for long-life performance.

North America

North America remains a significant regional market, reaching USD 5.78 billion in 2025. North America’s market is supported by strong demand from the automotive, aerospace, and industrial manufacturing sectors, where high-temperature, chemical-resistant sealing is essential. Growth is reinforced by expanding electronics and medical production, as well as the increasing use of premium elastomers in high-reliability, compliance-driven components.

U.S. High Performance Elastomers Market

The U.S. market in 2026 is estimated at USD 5.51 billion, accounting for approximately 21% of global revenues.

Europe

Europe is projected to grow at CAGR of 4.8% over the coming years, and reached a valuation of USD 5.04 billion in 2025. The region represents a mature, technology-driven market characterized by moderate demand for automotive and industrial machinery, where heat- and chemical-resistant sealing materials are critical for reliability. Industries including aerospace and medical, along with tighter sustainability norms, are further driving the adoption of higher-performance, lower-emission elastomer formulations.

Germany High Performance Elastomers Market

The Germany market is projected to reach USD 1.34 billion in 2026, equivalent to around 5% of global revenues. Germany’s leadership in automotive and industrial engineering relies on high-temperature, long-life sealing and hose materials.

U.K. High Performance Elastomers Market

The U.K. market in 2026 is estimated to record USD 0.74 billion, accounting for roughly 3% of global revenues. Growth is supported by demand in the aerospace, automotive, and industrial maintenance sectors for durable sealing and vibration-control materials.

Latin America

Latin America’s market valuation was worth USD 1.44 billion in 2025. The region’s demand is tied to oil & gas, mining, and heavy industry, where elastomers are subject to abrasion, pressure, and harsh field fluids. Automotive demand exists, but growth is more replacement- and maintenance-led, as plants prioritize reliability and cost-effective durability.

Brazil High Performance Elastomers Market

The Brazil market in 2026 is projected to record USD 0.72 billion, accounting for roughly 3% of global revenues. Brazil’s high performance elastomer demand is supported by the oil & gas industry, where seals and hoses must withstand heat, fuels, and aggressive chemicals.

Middle East & Africa

Middle East & Africa’s market valuation was worth USD 1.30 billion in 2025. The region’s demand is led by petrochemicals, refining, and gas processing, where high temperatures and aggressive chemicals require premium sealing materials. Growth also comes from desalination and water infrastructure, which uses elastomers in membranes, pumps, and chemical-dosing systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Application Engineering and Reliability-Driven Formulation Define Competitive Positioning

The global high performance elastomers industry is shaped by a concentrated group of specialty material suppliers with strong expertise in polymer chemistry, compounding, and end-use application engineering. Competitive differentiation is increasingly driven by long-term sealing reliability, resistance to heat and aggressive media, and stable performance over extended service life, rather than production scale alone. Key players such as Chemours, Solvay, AGC, Dow, and Evonik AG maintain strong market positions through broad elastomer portfolios, custom compound development, and close technical collaboration with OEMs, Tier suppliers, and seal manufacturers. Across the market, innovation focuses on higher-temperature and longer-life grades, clean and low-extractables materials for electronics and medical use, and low-VOC, more sustainable formulations that help customers meet regulatory and reliability targets.

LIST OF KEY HIGH PERFORMANCE ELASTOMERS COMPANIES PROFILED IN REPORT

- Avient Corporation (U.S.)

- Chemours (U.S.)

- Dow (U.S.)

- Envalior (Netherlands)

- Evonik AG (Germany)

- ExxonMobil (U.S.)

- First Graphene (Australia)

- Mitsubishi Chemical Group Corporation (Japan)

- Mitsui Plastics, Inc. (U.S.)

- Radici Group (Italy)

KEY INDUSTRY DEVELOPMENTS

- July 2025: At major industry events, Wacker Chemie AG showcased advanced silicone elastomer solutions for e-mobility, power grids, sensors, and high performance industrial applications, highlighting innovation in high-temperature, UV-resistant elastomer grades.

- October 2024: Daikin Industries expanded its Fluoroelastomer (FKM) production capacity in Asia to support rising demand from automotive electrification and semiconductor fluid-handling applications, thereby strengthening supply security for high-temperature, chemical-resistant sealing materials.

- July 2024: Chemours advanced new low-emission and low-extractables elastomer grades under its Viton™ portfolio, targeting automotive, electronics, and clean industrial environments, in response to tighter regulatory and customer performance requirements.

- March 2024: Wacker Chemie AG announced capacity and formulation upgrades for specialty silicone elastomers, focusing on thermal management, e-mobility components, and medical devices, reflecting increased demand for long-life and high-purity elastomer solutions.

- September 2023: Solvay strengthened its specialty elastomers platform by expanding application-development capabilities for fluoroelastomers and high performance thermoplastics, aiming to support OEM-specific sealing solutions in aerospace, automotive, and industrial processing.

REPORT COVERAGE

The global high performance elastomers market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.3% from 2026-2034 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Segmentation |

By Type, End Use, and Region |

|

By Type |

· Silicone Elastomers · Polyurethane Elastomers (TPU) · Thermoplastic Elastomers (TPE) · Hydrogenated Nitrile Butadiene Rubber · Acrylic Elastomers (ACE) · Fluoroelastomers (FKM) · Others |

|

By End Use |

· Automotive · Industrial Manufacturing · Oil & Gas · Electronics · Healthcare · Aerospace & Defense · Others |

|

By Region |

· North America (By Type, By End Use, and Country) o U.S. (By End Use) o Canada (By End Use) · Europe (By Type, By End Use, and Country/Sub-region) o Germany (By End Use) o U.K. (By End Use) o France (By End Use) o Italy (By End Use) o Spain (By End Use) o Rest of Europe (By End Use) · Asia Pacific (By Type, By End Use, and Country/Sub-region) o China (By End Use) o India (By End Use) o Japan (By End Use) o South Korea (By End Use) o Rest of Asia Pacific (By End Use) · Latin America (By Type, By End Use, and Country/Sub-region) o Brazil (By End Use) o Mexico (By End Use) o Rest of Latin America (By End Use) · Middle East & Africa (By Type, By End Use, and Country/Sub-region) o GCC (By End Use) o South Africa (By End Use) o Rest of Middle East & Africa (By End Use) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 24.80 billion in 2025 and is projected to reach USD 39.83 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 11.23 billion.

Recording a CAGR of 5.3%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The automotive segment led the market in 2025.

Rising demand from the automotive industry for high-temperature, chemically resistant materials is expected to drive market growth.

Chemours, Solvay, AGC, Dow, and Evonik AG are some of the top players in the market.

Asia Pacific held the highest market share in 2025.

Shift toward thermoplastic and fluoroelastomer grades in harsh-environment applications accelerates high performance elastomer consumption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us