Electric Car Rental Market Size, Share & Industry Analysis, By Rental Duration (Short-term, Medium-term, and Long-term / Subscription), By Vehicle Type (Hatchbacks & Compact Cars, Sedans, and SUVs & Crossovers), By End User (Leisure & Tourism Users, Corporate & Enterprise Clients, and Ride-hailing & Mobility Operators), By Fleet Operator Type (Traditional Car Rental Companies, EV-Focused Rental & Subscription Providers, and OEM-Owned / OEM-Backed Rental Fleets) and Regional Forecast, 2026-2034

Electric Car Rental Market Size and Future Outlook

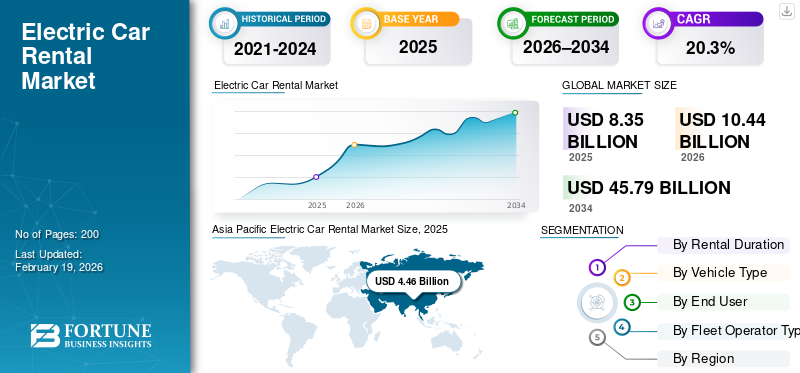

The global electric car rental market size was valued at USD 8.35 billion in 2025. The market is projected to grow from USD 10.44 billion in 2026 to USD 45.79 billion by 2034, exhibiting a CAGR of 20.3% during the forecast period. Asia Pacific dominated the electric car rental market with a market share of 53.41% in 2025.

Electric car rental is a mobility service that lets customers rent battery-electric vehicles for hourly, daily, weekly, or subscription periods. It typically includes insurance and maintenance, enabling EV access without ownership and reducing upfront cost barriers. The electric car rental market is driven by rising EV adoption, expanding charging networks, and stricter emissions rules in cities and corporate fleets. Lower operating and maintenance costs improve fleet economics, while subscription models attract users seeking flexibility. Tourism recovery, ride-hailing electrification, and OEM incentives further accelerate global demand for electric rentals.

Major players include Hertz, Avis Budget, Enterprise, Sixt, Europcar, and EV-first subscription providers. Trends include rapid EV fleet expansion, app-based bookings, bundled charging/insurance subscriptions, partnerships with OEMs and charging stations, and targeting airports, corporate accounts, and ride-hailing drivers for higher utilization.

Download Free sample to learn more about this report.

ELECTRIC CAR RENTAL MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 8.35 billion

- 2026 Market Size: USD 10.44 billion

- 2034 Forecast Market Size: USD 45.79 billion

- CAGR: 20.3% from 2026–2034

- Asia Pacific dominated the electric car rental market with a 53.41% share in 2025.

- The short-term (hourly–daily) rental segment accounted for the largest market share in 2025.

- The hatchbacks & compact cars segment held the largest market share in 2025.

Asia Pacific

Asia Pacific dominated the market, driven by China’s EV ecosystem and expanding ride-hailing electrification.

North America

North America is expected to witness strong growth, supported by early EV adoption and airport-based rentals.

Europe

Europe is expected to witness strong growth, driven by strict emission regulations and fleet electrification.

U.S.

The market reached USD 1.13 billion in 2025, fueled by airport rentals and corporate EV fleet adoption.

Japan

The market reached USD 0.29 billion in 2025, supported by growing urban mobility and EV adoption.

Read More

ELECTRIC CAR RENTAL MARKET TRENDS

Platform Partnerships Accelerate EV Access for Ride-Hailing and Everyday Mobility

Large-scale collaborations between mobility platforms, automakers, and rental fleets are reshaping how EVs reach high-mileage users. Instead of waiting for private ownership to catch up, fleets place EVs directly into daily service through bundled weekly rentals, financing support, and targeted programs for professional drivers. This model improves utilization, spreads charging learning across repeat users, and creates a practical try-before-you-buy pathway that scales faster than showroom conversion alone. As these partnerships mature, fleets can standardize vehicle types, negotiate charging benefits, and optimize depot operations around predictable demand, making EV rentals a feeder system for broader EV adoption rather than a niche option. In July 2024, Uber announced a partnership with BYD to help deploy up to 100,000 EVs for drivers.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

City Decarbonization Policies and Infrastructure Mandates Expand Rental EV Feasibility

As public policy shifts from encouraging EVs to requiring readiness, electric car rental becomes easier to scale. Infrastructure mandates reduce the most significant adoption friction, uncertain access to reliable public charging, by forcing minimum coverage, interoperability, and more explicit payment rules. For rental customers, this matters more than home charging because trips often span unfamiliar routes. For operators, predictable infrastructure reduces service exceptions, towing incidents, and customer support costs tied to low charge or incompatible networks. Policy alignment also improves corporate procurement: enterprise clients can electrify travel and project fleets with lower operational risk when charging availability is no longer optional or patchy across corridors. In April 2024, the EU’s Alternative Fuels Infrastructure Regulation became applicable, setting binding requirements for public charging deployment and user-friendly access.

MARKET RESTRAINTS

Repair Cost and Fleet Economics Volatility Constrain Aggressive EV Fleet Expansion

Operational economics can slow, even as electric car rental market growth and demand rise. Compared with mature ICE fleet playbooks, EV rentals introduce greater uncertainty around repair cycles, parts availability, workshop capacity, and downtime after damage, all of which directly reduce revenue days per vehicle. When combined with residual value swings, some operators pause procurement, limit model diversity, or redirect EVs to lower-risk customer segments. This restraint is structural: until repair networks, insurer pricing, and resale markets stabilize, fleet planners will prefer measured rollouts with tight utilization control rather than rapid, headline-scale EV buying. In February 2024, reports noted that Hertz had paused planned Polestar purchases and cited high repair costs as it scaled back EV ambitions.

MARKET OPPORTUNITIES

Integrated Charging Bundles Create a Clear Path to Premium Pricing and Higher Conversion

A significant growth lever is turning charging anxiety into a managed service. When rental companies bundle charging access, route planning, and unified payment into the booking flow, EV rental becomes closer to an ICE-like experience, reducing customer friction and increasing repeat usage. This opens premium opportunities: higher-margin EV categories, corporate accounts that demand predictable duty cycles, and subscription plans that include charging benefits. It also improves brand outcomes because first-time EV renters often treat the experience as a proxy for EV ownership. Operators that own the customer journey vehicle, app, charging access, and support can convert occasional renters into long-term subscribers and capture incremental revenue via partnerships with charging networks. In September 2025, Europcar Mobility Group U.K. partnered with Octopus Electroverse to give EV renters access to over one million chargers via a single platform.

MARKET CHALLENGE

Profitability Pressure from Depreciation, Insurance, and Impairments Tests EV Rental Scalability

Sustained expansion requires EV rental profitability that holds up through market cycles. Even with substantial utilization, fleet operators face a complex cost stack: depreciation sensitivity to used-EV pricing, insurance headwinds, and periodic impairments when fleet values reset. These pressures are amplified in EVs because technology refresh cycles can be faster, and pricing changes can ripple quickly into resale values. The challenge is not simply adding EVs, it’s designing fleet rotation, customer targeting, and remarketing strategies that protect margins while maintaining high availability. Operators that misjudge the cost curve may cut back abruptly, creating supply whiplash and slowing the momentum of electric vehicles. In February 2025, Hertz reported insurance cost headwinds and referenced fleet impairment impacts in its 2024 results, underscoring the complexity of margin management.

Segmentation Analysis

By Rental Duration

Short-Term Mobility Preference Anchors Rental Duration Leadership

Based on rental duration, the market is segmented into short-term (hourly–daily), medium-term (weekly), and long-term or subscription (monthly–annual).

Short-term rentals dominate due to strong airport demand, urban commuting, and tourism recovery, where customers prefer flexible, pay-per-use access without long commitments. High fleet turnover and frequent bookings make this segment the most significant revenue contributor. Meanwhile, long-term and subscription rentals are gaining traction among professionals and fleets seeking predictable costs and EV exposure without ownership, driving sustained expansion.

The Long-term/Subscription segment is projected to grow at a 24.4% compound annual growth rate CAGR over the forecast period.

- In March 2023, Sixt SE announced the expansion of its short-term EV rental offerings across central European and U.S. airport locations.

By Vehicle Type

Urban Efficiency Sustains Compact Vehicles While SUVs Accelerate Adoption

Based on vehicle type, the market is segmented into hatchbacks & compact cars, sedans, and SUVs & crossovers.

Hatchbacks and compact EVs dominate electric car rental market share due to affordability, ease of charging, and suitability for dense urban travel, especially in city and airport locations. Their lower acquisition and operating costs support high utilization. However, growing consumer preference for space, comfort, and longer driving range is accelerating demand for transitioning to electric SUVs, particularly for leisure and intercity use.

The SUVs & Crossovers segment is projected to grow at a CAGR of 24.1% over the forecast period.

- In January 2024, Avis Budget Group highlighted increasing deployment of electric SUVs within its rental fleet to meet rising customer demand.

To know how our report can help streamline your business, Speak to Analyst

By End User

Platform-Driven Utilization Keeps Mobility Operators in the Lead

Based on end user, the market is segmented into leisure & tourism users, corporate & enterprise clients, and ride-hailing & mobility operators.

Ride-hailing and mobility operators dominate the market because EVs deliver substantial cost advantages under high utilization, including lower fuel and maintenance costs. Fleet-based rentals for drivers ensure consistent demand and predictable revenue for operators. At the same time, corporate and enterprise clients are increasingly adopting EV rentals to meet sustainability targets and reduce fleet ownership risks.

The corporate & enterprise clients segment is projected to grow at a 22.3% CAGR over the forecast period.

- In June 2023, Lyft expanded its EV rental programs for drivers across multiple U.S. cities to support fleet electrification.

By Fleet Operator Type

Established Networks Lead While EV-First Models Reshape Fleet Economics

Based on fleet operator type, the market is segmented into traditional car rental companies, EV-focused rental & subscription providers, and OEM-owned or OEM-backed rental fleets.

Traditional car rental companies dominate due to their extensive branch networks, airport presence, and large fleet management capabilities, allowing faster EV integration at scale. However, EV-focused rental and subscription providers are growing rapidly by offering flexible plans, bundled charging, and digital-first user experiences tailored to EV users.

The EV-focused rental & subscription providers segment is projected to grow at a 22.4% CAGR over the forecast period.

- In October 2023, Onto (U.K.) expanded its EV-only subscription fleet to address rising long-term rental demand.

ELECTRIC CAR RENTAL MARKET REGIONAL OUTLOOK

By region, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

North America

Asia Pacific Electric Car Rental Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America represents a mature yet fast-evolving/growing electric car rental market, driven by early EV adoption, strong airport-based rentals, and rapid electrification of ride-hailing fleets. The U.S. leads regional demand due to high mobility intensity, corporate travel, and government incentives supporting EV fleets. Canada contributes through urban sustainability initiatives and growing charging infrastructure, while Mexico shows emerging growth from a lower base, supported by tourism recovery and cross-border mobility. Subscription-based EV rentals and electric SUVs are gaining traction as consumers seek flexibility and range suited to long-distance travel.

U.S. Electric Car Rental Market

The U.S. dominates with USD 1.13 billion in 2025. North America’s market is expected to grow due to large-scale airport operations, the electrification of ride-hailing, and corporate fleet adoption. The high availability of electric SUVs, extensive charging networks, and the strong presence of global rental operators accelerate market expansion across leisure and enterprise use cases.

Europe

Strict emissions regulations, urban low-emission zones, and a well-established company car culture strongly support the growth of Europe’s market. Countries such as the U.K., Germany, and France are driving demand as rental operators electrify fleets to comply with sustainability mandates. Corporate and long-term rental demand is robust, while compact EVs dominate urban usage. Europe’s dense charging infrastructure and government-led decarbonization policies make EV rentals a practical alternative to internal combustion rental vehicles across both short-term and subscription-based models.

U.K. Electric Car Rental Market

The U.K. benefits from aggressive net-zero targets, widespread public charging access, and high corporate sustainability commitments. Electric rentals are increasingly used for business travel and urban mobility, with subscription-based models expanding as users seek predictable costs and emission-free transportation. It is valued at USD 0.45 billion in 2025.

Germany Electric Car Rental Market

Germany’s market is driven by strong automotive manufacturing influence, corporate fleet electrification, and extensive highway charging infrastructure, with an 18.2% CAGR. Demand is rising for premium electric sedans and SUVs, particularly among enterprise clients and long-distance travelers, supported by government incentives and environmental compliance requirements.

Asia Pacific

Asia Pacific is the dominant regional market, led by China’s massive EV ecosystem and expanding ride-hailing electrification. Urban density, government incentives, and cost-conscious consumers favor compact electric vehicles EVs for rental fleets. Japan and India contribute through distinct pathways, Japan via urban mobility and technology adoption, and India through rapid scaling from a low base. Growth is also supported by increasing tourism, app-based mobility platforms, and long-term rental programs for professional drivers, making the region a key engine of global market expansion.

China Electric Car Rental Market

China dominates the Asia Pacific market with a 70.6% share in 2025, driven by its large EV manufacturing base, government-led electrification policies, and widespread adoption by ride-hailing platforms. High availability of affordable EV models and dense urban charging infrastructure enable large-scale rental and subscription deployment.

Japan Electric Car Rental Market

Japan’s market is shaped by urban mobility needs, a preference for compact vehicles, and strong technology integration valued at USD 0.29 billion in 2025. Rentals are increasingly used for short-distance city travel and corporate purposes, supported by reliable infrastructure and growing acceptance of electric mobility among urban users.

India Electric Car Rental Market

India is an emerging market for electric car rentals, with a 27% CAGR, driven by rising electrification in ride-hailing, cost-conscious consumers, and government incentives. Long-term rentals and subscriptions are gaining popularity among drivers and enterprises seeking EV access without high upfront ownership costs.

Rest of the World

The Rest of the World region shows steady but uneven growth, driven by tourism recovery, urban electrification initiatives, and the gradual expansion of charging infrastructure. Markets in Latin America, the Middle East, and parts of Africa are adopting electric rentals mainly in premium tourism hubs and major cities. Short-term rentals dominate due to visitor demand, while corporate and government-led electrification programs are creating long-term opportunities. Although adoption is slower than in developed regions, improving vehicle availability and policy support are expected to drive gradual market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Fleet Electrification, Platform Integration, and Partnerships Define Electric Car Rental Competition

The competitive landscape is shaped by rapid fleet electrification, digital booking ecosystems, and partnerships across automakers, charging providers, and mobility platforms. Leading players such as Hertz, Avis Budget Group, Enterprise Mobility, Sixt, Europcar, and Alphabet compete by expanding EV fleets, prioritizing high-utilization airport and urban locations, and integrating charging access into rental workflows. EV-focused providers and subscription platforms differentiate through flexible monthly plans, bundled charging, telematics-driven fleet optimization, and app-based customer engagement. Competitive advantage increasingly depends on scale, fleet utilization efficiency, charging reliability, and residual value management. Strategic alliances with OEMs and energy companies help reduce acquisition costs and operational risk, while data-driven pricing improves margins. In July 2024, Uber announced a global partnership with BYD to support the deployment of up to 100,000 EVs for ride-hailing drivers, reinforcing the role of platform-fleet collaborations in shaping the competitiveness of electric car rental.

LIST OF KEY ELECTRIC CAR RENTAL COMPANIES PROFILED

- Hertz Global Holdings, Inc. (U.S.)

- Avis Budget Group, Inc. (U.S.)

- Sixt SE (Germany)

- Europcar Mobility Group (France)

- Enterprise Holdings, Inc. (U.S.)

- Alphabet Mobility (Germany)

- LeasePlan (Netherlands)

- Arval (France)

- Uber Technologies, Inc. (U.S.)

- Lyft, Inc. (U.S.)

- Zoomcar Holdings, Inc. (U.S.)

- Turo Inc. (U.S.)

- Free2Move (Stellantis) (France)

- Kinto (Toyota Mobility Services) (Japan)

- Care by Volvo (Sweden)

KEY INDUSTRY DEVELOPMENTS

- January 2026: MBS International Airport (Michigan, U.S.) advanced a USD 9.25 million solar-and-EV-charging buildout that includes EV charging infrastructure in the rental-car area, with Avis/Budget and Hertz/Dollar installing their own EV charging kiosks. The project is designed to reduce energy costs and improve charging availability for EV renters and parkers.

- November 2025: Hertz appointed Ace Drive (Reach Group) as its new franchise partner in Singapore, with operations covering Hertz and Thrifty locally and offering self-drive rentals plus longer-term leasing options. The move strengthens Hertz’s Asia-Pacific footprint and adds capacity for electric car rental services and supported services in a high-travel hub market.

- November 2025: Al-Futtaim BYD Saudi Arabia and SIXT Rent a Car signed an MoU to advance sustainable mobility in the Kingdom, including integrating BYD new-energy vehicles into SIXT’s rental fleet and collaborating on modern mobility solutions. This type of OEM–rental tie-up accelerates EV fleet availability and customer access.

- September 2025: Europcar Mobility Group U.K. partnered with Octopus Electroverse to give EV rental customers access to 1+ million public chargers across the U.K. and Europe via a single charging app and tools, such as route planning, to reduce range anxiety and simplify public charging for first-time EV renters.

- July 2025: Avis Budget Group announced a multi-year strategic partnership with Waymo to support a fully autonomous ride-hailing launch and scale-up in Dallas, where Avis acts as fleet operations partner (vehicle readiness, maintenance, depot operations). This signals rental operators expanding into EV/AV fleet services beyond traditional rentals.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 20.3% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Rental Duration, By Vehicle Type, By End User, By Fleet Operator Type, and By Region. |

|

By Rental Duration |

· Short-term (Hourly–Daily) · Medium-term (Weekly) · Long-term / Subscription (Monthly–Annual) |

|

By Vehicle Type |

· Hatchbacks & Compact Cars · Sedans · SUVs & Crossovers |

|

By End User |

· Leisure & Tourism Users · Corporate & Enterprise Clients · Ride-hailing & Mobility Operators |

|

By Fleet Operator Type |

· Traditional Car Rental Companies · EV-Focused Rental & Subscription Providers · OEM-Owned / OEM-Backed Rental Fleets |

|

By Region |

· North America (By Rental Duration, By Vehicle Type, By End User, By Fleet Operator Type, and By Country) o U.S. (By Vehicle Type) o Canada (By Vehicle Type) o Mexico (By Vehicle Type) · Europe (By Rental Duration, By Vehicle Type, By End User, By Fleet Operator Type, and By Country) o Germany (By Vehicle Type) o U.K. (By Vehicle Type) o France (By Vehicle Type) o Rest of Europe (By Vehicle Type) · Asia Pacific ( By Rental Duration, By Vehicle Type, By End User, By Fleet Operator Type, and By Country) o China (By Vehicle Type) o Japan (By Vehicle Type) o India (By Vehicle Type) o South Korea (By Vehicle Type) o Rest of Asia Pacific (By Vehicle Type) · Rest of the World (By Rental Duration, By Vehicle Type, By End User, By Fleet Operator Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.35 Billion in 2025 and is projected to reach USD 45.79 Billion by 2034.

In 2025, the market value stood at USD 4.46 billion.

The electric car rental market demand is expected to grow at a CAGR of 20.3% during the forecast period from 2026 to 2034.

The short-term (hourly–daily) segment led the electric car rental market share in the rental duration segment.

City decarbonization policies and infrastructure mandates expand rental EV feasibility.

Key market players include Hertz, Avis Budget, Enterprise, Sixt, and Europcar.

Asia Pacific accounted for the largest share in the market in 2025.

North America, Europe, Asia Pacific, and the Rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us