Electric Locomotive Market Size, Share & Industry Analysis by Component (Rectifier, Alternator, Motor, and Others), By Technology (IGBT Module, GTO Module, and SiC Module), By End User (Passenger and Freight), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

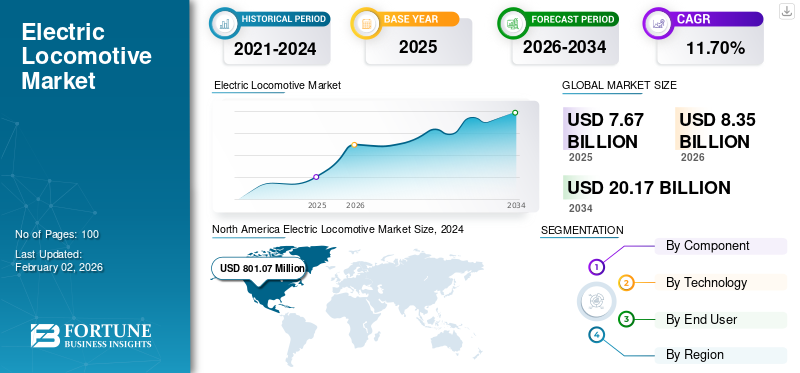

The global electric locomotive market size was valued at USD 7.67 billion in 2025. The market is projected to grow from USD 8.35 billion in 2026 to USD 20.17 billion by 2034, exhibiting a CAGR of 11.70% during the forecast period.

The market is evolving steadily as rail operators and governments prioritize cleaner, more energy-efficient transportation. Electric locomotives are favored for their lower emissions, quieter operation, and higher energy efficiency compared to diesel counterparts. Many countries with established rail networks are investing in the electrification of key routes, especially those with high traffic volumes, to improve sustainability and reduce long-term operating costs. In parallel, emerging technologies such as battery-electric and hybrid locomotives are being explored to address the limitations of non-electrified tracks and expand the reach of cleaner rail solutions

Key players in the market include a mix of established global rail manufacturers and regionally dominant firms. Companies such as Siemens, Alstom, and Hitachi are at the forefront, offering a range of advanced locomotives for both freight and passenger applications.

Download Free sample to learn more about this report.

ELECTRIC LOCOMOTIVE MARKET TRENDS

Expansion of Rail Electrification Projects is a Prominent Market Trend

The expansion of rail electrification projects is a prominent trend shaping the market, driven by a global push toward cleaner, more efficient, and sustainable transportation. Governments and rail operators are increasingly investing in the electrification of existing and new rail lines to reduce the dependence on diesel-powered locomotives, lower greenhouse gas emissions, and improve energy efficiency. Electrified rail networks contribute to national climate goals and also offer long-term operational benefits such as lower fuel costs, reduced maintenance, and higher reliability.

MARKET DYNAMICS

MARKET DRIVERS

Growing Focus on Environmental Sustainability to Drive the Market

The growing focus on environmental sustainability is a key driver fueling the adoption of electric locomotives worldwide. As concerns over climate change and air pollution intensify, governments, industries, and the public are pushing for cleaner transportation alternatives. Railways, already one of the most energy-efficient modes of transport, are becoming even greener through the shift from diesel to electric locomotives, which produce zero tailpipe emissions and contribute significantly to reducing overall carbon footprints.

Electric locomotives support this sustainability agenda by enabling lower greenhouse gas emissions, especially when powered by renewable or cleaner electricity sources. This aligns with global commitments to reduce emissions under international climate agreements and national policies targeting net-zero goals.

MARKET RESTRAINTS

Limited Interoperability across Regions and Countries to Hamper the Market Growth

The limited interoperability of electric locomotives across various regions and countries poses a significant challenge to the growth of the market. Rail networks vary widely in terms of technical standards, including track gauge, electrification voltage, signaling systems, and communication protocols. These differences make it difficult to deploy standardized locomotives across multiple regions, limiting the efficiency and scalability of operations, especially in cross-border freight and passenger services. This lack of uniformity means that manufacturers often need to design and produce locomotives customized to specific regional requirements, increasing costs, and complicating maintenance and spare parts management.

MARKET OPPORTUNITIES

Smart Mobility and Digital Rail Systems to Create Market Opportunity

The rise of smart mobility and digital rail systems presents a significant market opportunity for electric locomotives by transforming traditional rail operations into more efficient, safe, and customer-centric networks. Advanced digital technologies such as real-time monitoring, predictive maintenance, and automated controls are being integrated into electric locomotives, enabling operators to optimize performance, reduce downtime, and lower maintenance costs. These innovations allow rail companies to move from reactive to proactive management, improving reliability and extending the lifespan of expensive assets.

MARKET CHALLENGES

Technological Complexity of Integration Constraints to Create Challenges for the Market

The technological complexity of integrating electric locomotives with existing rail infrastructure presents a significant market challenge. Compatibility issues arise due to varying power systems, signaling protocols, and control technologies across different networks. Ensuring seamless operation on mixed traffic routes, where both diesel and electric trains run, adds further complexity. Additionally, coordinating with legacy systems and upgrading infrastructure to support advanced features can be costly and time-consuming. This complexity slows adoption, increases project risks, and requires specialized expertise, making it difficult for rail operators and manufacturers to implement electric locomotive solutions efficiently and uniformly across diverse rail environments.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Motor Segment to Display the Highest Growth Rate due to Technological Advancements

Based on component, the market is segmented into rectifier, alternator, motor, and others.

The motor segment is likely to grow at the highest CAGR during 2025-2032. Manufacturers are looking to innovate and create energy-efficient motors that consume less power. Power losses are decreased and overall power delivery to the wheels has been improved by using motors, which are vital factors anticipated to continue fueling the expansion of this segment.

The others segment led the global electric locomotive market share in the year 2024. The growth is due to the rising number of components used in locomotives to increase the machine's efficiency. The others sector also includes a comprehensive list of all the significant and minor elements necessary for peak operational efficiency. These considerations, which have a wide range, have a big impact on this category's market share compared to other component categories.

By Technology

IGBT Module Segment Led the Market Owing to Increased Power Efficiency and Improved Functions

Based on technology, the market is divided into IGBT module, GTO module, and SiC module.

The IGBT module segment dominated the global market share in 2024. IGBT modules support in mixed traffic and cross-border applications owing to their superior performance, increased power efficiency, and improved cooling. These factors are anticipated to push the segmental dominance.

The SiC module segment is likely to grow at the highest CAGR during 2025-2032. Compared to IGBT and GTO power modules, SiC modules are far more efficient and produce far less power loss. SiC module have such additional advantages over other modules due to which the segment is projected to show the highest growth rate over the forecast period.

By End User

Increasing Demand for Public Transportation Stimulated Passenger Segment Growth

Based on end user, the market is divided into passenger and freight.

The passenger segment held a major market share in 2024 and is expected to retain its dominance throughout the forecast period. This is primarily driven by the higher demand for public transportation across various regions.

The freight segment is the fastest growing segment and is expected to grow at the highest CAGR during the forecast period. This is owing to the increasing demand for freight operations worldwide as a result of the expansion of e-commerce and logistics activities.

Electric Locomotive Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Electric Locomotive Market Size, 2025 (USD Million) To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 2.31% of the global market share, reaching a valuation of USD 0.18 billion, and is projected to grow to USD 0.2 billion in 2026. The market in North America is gradually evolving as environmental concerns and policy shifts encourage a transition toward greener transportation. Rail operators are modernizing fleets with electric alternatives to reduce emissions and improve efficiency. In the U.S., the push for the electrification of rail transport is gaining traction, driven by federal policies emphasizing clean energy and emissions reduction.

Asia Pacific

Other regions such as Europe and Asia Pacific are anticipated to witness a notable electric locomotive market growth in the coming years. During the forecast period, the Asia Pacific region is projected to record the growth rate of 11.1%, which is the highest amongst all the regions.

Europe

The market in Europe reached USD 3.56 billion in 2025, representing 46.47% of total market revenue, and is projected to reach USD 3.77 billion in 2026. This is fueled by population growth, urbanization, and significant investments in rail infrastructure. Countries such as China, India, and Japan are prioritizing electrified rail systems to meet rising transportation needs while addressing pollution. After Asia Pacific, the market in Europe (Western Europe, Eastern Europe) is estimated to reach USD 2,829.81 million in 2025. Governments and private rail operators prioritize electrification to meet climate targets and reduce dependency on fossil fuels. Countries such as Germany, France, and the U.K. are aggressively upgrading rail lines and integrating electric fleets.

Rest of the World

The Rest of the World market accounted for USD 0.11 billion in 2025, representing 1.46% of the global industry, and is expected to reach USD 0.15 billion in 2026. Over the forecast period, the market in the rest of the world would witness a moderate growth in this market. The rest of the world market valuation is estimated to be USD 0.76 billion in 2025. Regions such as the Middle East & Africa are exploring electrified rail to diversify transportation and reduce reliance on oil. South America shows potential, with several countries seeking to modernize outdated rail systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Ongoing Strategic Partnerships and R&D Activities by Leading Firms to Drive their Prevailing Market Presence

The electric locomotive market is characterized by the presence of several established global players, regional manufacturers, and emerging technology providers competing to capture market share. Leading companies focus on innovation, energy efficiency, and technological integration to meet the evolving demands of rail operators and regulatory bodies. Key players often engage in strategic partnerships, joint ventures, and mergers to expand their geographic footprint and strengthen R&D capabilities. Manufacturers are prioritizing sustainable solutions, including battery-electric and hybrid-electric locomotives, to align with global emissions targets.

LIST OF KEY ELECTRIC LOCOMOTIVE COMPANIES PROFILED

- Progress Rail (U.S.)

- General Electric Company (U.S.)

- Anglo Belgian Corporation NV (Belgium)

- Toshiba Corporation (Japan)

- CRRC Corporation Limited (China)

- Alstom SA (France)

- Siemens AG (Germany)

- Kawasaki Heavy Industries, Ltd. (Japan)

- Kolomensky Zavod (Russia)

- Bharat Heavy Electricals Limited (BHEL) (India)

- Chittaranjan Locomotive Works (India)

- CAF, Construcciones y Auxiliar de Ferrocarriles, S.A. (Spain)

- Hyundai Rotem Company (South Korea)

- Stadler, Inc. (Switzerland)

- Hitachi Rail Limited (U.K.)

- Wabtec Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Bulgaria signed a USD 580.65 million contract with Alstom for 35 zero-emission electric multiple units. The initiative aims to reduce the carbon footprint of Bulgaria's railway sector, with deliveries scheduled to begin in August 2026.

- March 2025: Alstom signed a contract worth USD 175.41 million to deliver 30 Traxx electric locomotives to Slovenia, enhancing the country's rail infrastructure and supporting its transition to more sustainable transportation options.

- December 2024: Stadler Rail AG and LTG Cargo signed a contract for the delivery of seventeen Co'Co' electric locomotives. The agreement has a 3-year maintenance term, spare components, and an option for 17 more units. For the Lithuanian market, this is Stadler's first locomotive deal.

- December 2024: Olavion, a Polish transportation business, signed a contract with Newag for 12 locomotives. The objective of this agreement is to improve infrastructure development and increase transportation capacity.

- September 2024: Stadler was awarded a contract by Swiss Federal Railways (SBB Cargo) for up to 129 multi-system electric locomotives. The first 36 units ordered, designed to operate on 15 kV AC, 25 kV AC, and 3 kV DC systems, would replace older models and enhance operational efficiency.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.70% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Component · Rectifier · Alternator · Motor · Others |

|

By Technology · IGBT Module · GTO Module · SiC Module |

|

|

By End User · Passenger · Freight |

|

|

By Geography North America (By Component, Technology, End User, and Country) · U.S. · Canada Europe (By Component, Technology, End User, and Country) · U.K. · Germany · France · Rest of Europe Asia Pacific (By Component, Technology, End User, and Country) · China · Japan · India · South Korea · Rest of Asia Pacific Rest of the World (By Component, Technology, End User, and Country) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.35 billion in 2026 and is projected to reach USD 20.17 billion by 2034.

In 2025, the North America market value stood at USD 0.18 billion.

The market is expected to exhibit a CAGR of 11.70% during the forecast period of 2026-2034.

The growing focus on environmental sustainability is a key factor driving the market.

Progress Rail (U.S.), General Electric Company (U.S.), Anglo Belgian Corporation NV (Belgium), Toshiba Corporation (Japan), Alstom SA (France), and Siemens AG (Germany), among others, are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 100

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us