Electric Passenger Cars Market Size, Share & Industry Analysis, By Powertrain (BEV and PHEV), By Price (Entry, Mid, and Premium), and By Customer (Private and Commercial), By Charging Capability (AC Only and AC & DC), By Range (Short, Mid, and Long), and Regional Forecast, 2026-2034

Electric Passenger Cars Market Size and Future Outlook

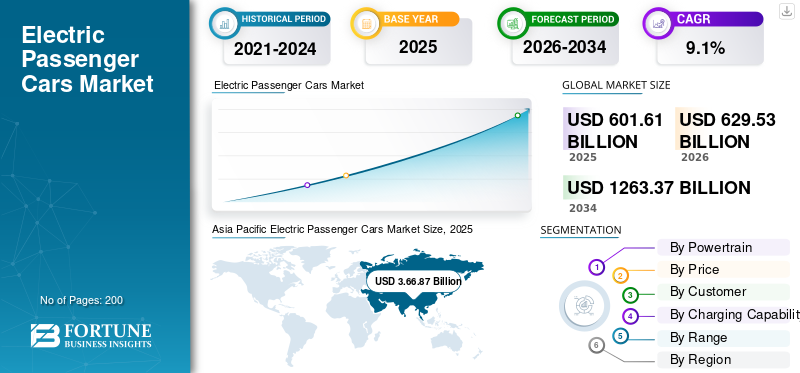

The global electric passenger cars market size was valued at USD 601.61 billion in 2025. The market is projected to grow from USD 629.53 billion in 2026 to USD 1,263.37 billion by 2034, exhibiting a CAGR of 9.1% during the forecast period. Asia Pacific dominated the global electric passenger cars market with a market share of 60.98% in 2025.

The electric passenger cars market represents the shift from combustion engine mobility to vehicles powered entirely or partly by electricity. It includes battery-electric and plug-in hybrid models designed for personal transport, supported by charging networks, battery suppliers, and related services. Over the next few years, this market is expected to expand steadily as more countries tighten emissions rules, carmakers roll out broader electric line-ups, and battery prices gradually ease. Consumers are also becoming more confident in electric driving as real-world range improves and charging becomes faster and easier to access. Growth will be shaped by government incentives, corporate fleet electrification, and rising investment in domestic lithium-ion battery manufacturing. Although regional adoption will vary, the overall trend indicates that electric cars are becoming toward mainstream choice rather than a niche option, driven by technology gains and long-term commitments to cleaner transportation.

Key players in the market include Tesla, BYD, SAIC Motor, Volkswagen Group, Hyundai-Kia, Stellantis, BMW Group, Mercedes-Benz, and Geely. These companies compete through a mix of technology leadership, localized production, and expansion of EV lineups across price segments. Many are securing long-term battery supply agreements, investing in solid-state technologies, and building integrated manufacturing ecosystems to reduce costs. Others focus on software, over-the-air upgrades, and connected-vehicle services to differentiate their offerings. Strategic partnerships, charging infrastructure collaborations, and targeted market entries are further strengthening competitive positions as global EV adoption accelerates.

Download Free sample to learn more about this report.

Electric Passenger Cars Market Key Takeaways

- 2025 Market Size: USD 601.61 billion

- 2026 Market Size: USD 629.53 billion

- 2034 Forecast Market Size: USD 1,263.37 billion

- CAGR: 9.1% from 2026–2034

- Asia Pacific dominated the electric passenger cars market with a 60.98% share in 2025.

- The Battery Electric Vehicle (BEV) segment held the largest market share in 2025.

- The private customer segment accounted for the leading market share in 2025.

Asia Pacific

Asia Pacific led the global market in 2025, driven by strong EV manufacturing capabilities and supportive government policies.

Europe

Europe recorded steady growth, supported by strict emission regulations and expanding charging infrastructure.

North America

North America maintained a significant market position due to federal incentives and investments in EV charging networks.

U.S.

The market is expanding rapidly, supported by tax incentives, domestic EV production, and growing charging infrastructure.

Japan

Rising investments in electric mobility and advancements in battery technology are supporting market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

High Investments in Public Charging Networks to Drive Market Growth

Governments across major automotive markets are steadily tightening CO2 emissions rules, offering tax benefits, and setting clear timelines for the phase out of internal combustion vehicles. Financial incentives such as purchase subsidies, reduced registration fees, and lower road taxes help narrow the upfront price gap between electric and conventional models, making EVs more accessible to a wider range of buyers. At the same time, national and regional authorities are investing heavily in public charging networks to ease range concerns and promote long-distance travel. Regulatory pressure on automakers to meet fleet-level CO2 targets is also reshaping product strategies, prompting companies to accelerate EV development and expand their electric portfolios. Over the next decade, sustained government backing is expected to remain a foundational driver of EV adoption, ensuring EV demand grows even in periods of economic uncertainty.

MARKET RESTRAINTS

Insufficient Charging Infrastructure May Restrain Market Growth

A significant restraint on the electric passenger cars market growth is the slow and uneven development of the charging infrastructure. While major cities are expanding public charging networks, many regions still lack reliable, widely distributed networks that support daily commuting and long-distance travel. This inconsistency creates uncertainty for potential buyers, particularly worry about access to fast charging during peak hours or in less-developed areas. Local grids in several countries are not equipped to handle concentrated charging demand, especially as EV adoption accelerates. Utilities need to invest in capacity upgrades, smart metering, and load management systems; however, these improvements require time and coordination among government bodies and private stakeholders. This gap between EV growth and supporting infrastructure remains a strong restraint, slowing adoption in regions where electrical and charging networks lag behind vehicle availability.

MARKET OPPORTUNITIES

Budget-Conscious Buyers to Offer Significant Market Opportunities

As battery technology improves and production scales up, manufacturers are finding ways to reduce costs without compromising essential performance. This opens the door for a broader range of compact, entry, and mid-segment electric cars that appeal to budget-conscious buyers, especially in emerging economies where price remains the primary purchase driver. Automakers are increasingly localizing battery manufacturing, adopting modular vehicle platforms, and using simplified drivetrain architectures to further lower production expenses. These shifts enable companies to offer competitively priced models while maintaining acceptable range, charging speed, and safety standards. Governments can further support this opportunity by supporting local supply chains and offering incentives targeted at lower-income buyers.

Electric Passenger Cars MARKET TRENDS

Increasing Inclination of Software-Defined Features to Drive Market Growth

The shift toward software-defined vehicles, where digital capabilities play a role in mechanical performance, is one of the significant electric passenger cars market trends. Automakers are redesigning EV platforms to support over-the-air updates, advanced driver-assistance functions, and real-time performance optimization. This approach allows manufacturers to introduce new features long after a vehicle is sold, creating ongoing revenue streams through subscription services or one-time upgrades. Connected ecosystems are also expanding, linking vehicles with home energy systems, public charging networks, and cloud-based diagnostics. Drivers can monitor charging behavior, schedule energy use to align with off-peak electricity rates, and access remote support for troubleshooting. These digital layers enhance convenience and help differentiate brands in an increasingly crowded EV landscape.

MARKET CHALLENGES

Volatility in Battery Raw Material Supply and Pricing Challenges Market Growth

One of the most complex challenges in the market is the unpredictable supply and pricing of key battery raw materials such as lithium, nickel, cobalt, and graphite. As global EV production accelerates, demand for these minerals has surged, outpacing the speed at which new mines, refining capacity, and processing technologies can be brought online. This imbalance often leads to sudden price spikes, creating uncertainty for automakers that rely on long-term cost stability to plan product portfolios and pricing strategies. In addition, many essential materials are sourced from a few regions, making the industry vulnerable to export restrictions, political unrest, or environmental regulations that disrupt mining operations. To navigate this challenge, manufacturers are exploring battery chemistries with reduced reliance on high-cost materials and investing in recycling systems to recover valuable minerals. Until supply chains become more diversified and resilient, raw material volatility will remain a significant hurdle, potentially limiting the global pace of electric passenger cars.

Download Free sample to learn more about this report.

Segmentation Analysis

By Powertrain

Tightening Emission Standards to Drive the Growth of the BEV Segment

Based on powertrain, the market is divided into Battery Electric Vehicles (BEV) and Plug-in Hybrid Electric Vehicle (PHEV).

BEV holds the largest market share and will grow at the highest CAGR during the forecast period. Growth in the BEV segment is being propelled by a combination of technological advances, supportive policies, and shifting consumer expectations. One of the strongest drivers is the rapid improvement in battery performance. Higher energy density, faster charging capabilities, and longer cycle life are making BEVs more practical for daily use and long-distance travel. Many countries are tightening emission standards, offering incentives, and setting clear timelines for phasing out internal-combustion engines. These measures encourage buyers to consider BEVs and push manufacturers to prioritize fully electric platforms. Expanding charging networks, especially the growth of fast-charging corridors, reduces range anxiety and enhances the convenience of owning a BEV.

By Price

Steady Decrease in Battery Prices to Boost the Growth of the Mid Segment

In terms of price, the market is divided into entry, mid, and premium.

The mid segment is expected to dominate the market, as technology improvements and manufacturing scale make well-equipped EVs more accessible. One major factor driving this growth is the steady decline in battery costs, which allows automakers to offer strong performance, practical range, and modern features without premium-level pricing. Consumer expectations are also shifting toward vehicles that balance affordability with advanced technology. Mid-price electric passenger cars often include competitive driving range, faster charging capability, and improved safety systems.

The entry segment is expected to display the highest CAGR during the forecast period. Streamlined vehicle architectures, shared components, and localized production are further helping companies lower manufacturing expenses and introduce competitively priced electric models. Subsidies targeting first-time EV buyers, reduced registration fees, and preferential financing options make entry-level electric cars attractive to cost-conscious households. The growing electric passenger cars market demand from ride-sharing drivers, delivery fleets, and micro-mobility services also supports this segment. Together, these factors create a strong foundation for the rapid expansion of entry-price electric passenger cars, accelerating widespread EV adoption.

To know how our report can help streamline your business, Speak to Analyst

Technological Development to Boost the Private Segment Growth

By customer, the market is segmented into private and commercial.

The private segment will dominate the market due to a combination of economic, technological, and lifestyle factors. With fewer mechanical components, lower maintenance needs, and reduced dependence on fluctuating fuel prices, EVs provide a more predictable ownership experience. Modern EVs offer improved driving ranges, faster charging times, and enhanced safety features, making them practical alternatives to traditional vehicles. Government incentives such as purchase rebates, reduced road taxes, and priority parking further encourage private EV purchases.

The commercial segment is expected to grow at the highest CAGR during the forecast period. Many organizations are adopting emissions-reduction targets and integrating EVs into their mobility strategies to demonstrate environmental responsibility. This shift is reinforced by government initiatives offering tax benefits, fleet-specific incentives, and priority access to low-emission zones, particularly in congested urban areas. The rapid expansion of electric vehicle charging infrastructure tailored for fleet use, such as depot charging, workplace stations, and dedicated fast-charging hubs, also accelerates commercial adoption. Growing demand from ride-hailing services, rental companies, and last-mile delivery operators further boosts momentum. Combined, these economic, regulatory, and operational advantages position commercial customers as key contributors to the broader adoption of electric passenger cars.

By Charging Capability

Ease of Use and Accessibility to Drive the Growth of AC Only Segment

On the basis of charging capability, the market is divided into AC only and AC & DC.

The AC only segment is expected to dominate the market, driven by a combination of cost efficiency, practical charging behavior, and expanding access to slow and moderate EV charging infrastructure. Most private users charge their vehicles at home, workplaces, or community stations where AC charging is the standard option. As residential complexes and commercial buildings increasingly install AC chargers, daily charging becomes convenient and inexpensive, reinforcing demand for AC-compatible models.

The AC & DC segment will grow at a rapid CAGR during the forecast period. One of the strongest drivers is the expansion of high-power DC fast-charging networks along highways and major travel routes. As these stations become more widespread, buyers increasingly prefer vehicles capable of rapid charging to minimize downtime during long trips. This dual compatibility enhances convenience and broadens the appeal of EVs to families, commuters, and frequent travelers. Commercial operators and shared mobility providers favor dual compatible vehicles as well, since fast charging allows them to maximize fleet utilization and reduce operational gaps. Government policies promoting fast-charging corridors and offering incentives for high-capacity infrastructure installation further reinforce the shift.

By Range

Mid-Range Segment to Dominate due to Advancements in Battery Efficiency

On the basis of range, the market is divided into short, mid, and long.

The mid segment is expected to capture the largest market share during the forecast period. A major driver behind the growth is the steady improvement in battery efficiency, enabling vehicles in this segment to deliver 250-400 km of real-world range sufficient for daily commuting and occasional long trips. Automakers are increasingly focusing on this segment by adopting modular EV platforms and shared components that reduce development and manufacturing expenses.

The long range segment will grow at a rapid CAGR during the forecast period. The expansion of fast charging corridors further accelerates demand. As more highways and major routes are fitted with high-power DC chargers, drivers are confident that long trips can be completed with short, predictable charging stops. Automakers are also optimizing thermal management and charging architectures, enabling faster charging without compromising battery durability.

Electric Passenger Cars Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the Rest of the World.

Asia Pacific captured the largest market share in 2025 and will grow at the highest CAGR during the forecast period. The region is expanding rapidly, driven by strong policy support, accelerating domestic manufacturing, and rising consumer interest in cost-efficient, low-emission mobility. A major driver is the region’s well-established battery and EV component supply chain. Localized production reduces costs and improves vehicle availability, supporting a diverse range of models across entry, mid, and premium segments. Urbanization and worsening air quality in large cities further strengthen demand for cleaner transportation.

Asia Pacific Electric Passenger Cars Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America holds the third-largest electric passenger cars market share. The market is expanding steadily, supported by strong federal policies, growing state-level commitments, and rising consumer interest in cleaner mobility. Government initiatives such as tax credits under the Inflation Reduction Act, zero-emission vehicle mandates, and funding for domestic battery production significantly strengthen the overall market environment. Public and private investments are enabling the development of fast-charging corridors across major highways and urban centers, making long-distance travel more practical and improving day-to-day usability for EV owners.

The U.S. market is growing rapidly, supported by a combination of federal incentives, expanding manufacturing capacity, and shifting consumer expectations. Government incentives lower ownership costs and stimulate investment in domestic supply chains, resulting in more affordable and accessible electric models for U.S. consumers. Public and private organizations are accelerating the installation of fast charging stations along interstate highways, urban hubs, and commercial centers. This expanding network reduces range anxiety and improves confidence in long-distance travel, making EVs more practical for everyday use.

Europe is experiencing steady growth during the forecast period. One of the most influential factors is the region’s ambitious emissions reduction agenda. The European Union’s CO₂ targets, phase-out timelines for internal combustion vehicles, and incentives for zero-emission mobility create a clear pathway that encourages both consumers and automakers to shift toward electric models. Many countries also offer tax reductions, purchase grants, and lower toll or parking fees, making EV ownership more financially attractive. Europe’s well-developed public charging infrastructure further accelerates adoption. Dense networks of AC and fast DC chargers across highways, urban centers, and residential areas give drivers confidence in the practicality of electric mobility.

In the rest of the world, the market across Latin America and the Middle East & Africa exhibits strong growth potential over the next few years. A key driver is the growing recognition of the economic benefits associated with EVs. Several countries, including Chile, Brazil, the UAE, and Saudi Arabia, are introducing incentives, reduced import duties, and pilot programs to support early adoption. Investments in public charging networks, supported by energy companies and private developers, are gradually reducing concerns about charging accessibility. Major cities in these regions are also adopting sustainability strategies that include electrifying public transport and promoting low-emission zones, indirectly boosting demand for passenger EVs.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Developments and Cost Reduction Will Form the Basis of Market Expansion

The competitive landscape of the electric passenger cars market is characterized by intense rivalry among global automakers, emerging EV specialists, and technology-driven entrants. Established brands such as Tesla, BYD, Volkswagen Group, Hyundai-Kia, and Stellantis are expanding their EV portfolios across multiple price segments, from entry-level to premium models. Many companies are prioritizing battery innovation, investing in next-generation chemistries, and forming long-term partnerships with cell manufacturers to secure supply and reduce costs. Automakers are also accelerating localized production to meet regional regulatory requirements while improving affordability and reducing delivery times.

Integration of connected services, subscription-based upgrades, and digital ecosystems helps build long-term customer relationships and new revenue streams. Players are also investing heavily in charging collaborations and infrastructure expansion to enhance user convenience. Reduction of carbon footprints across supply chains and increasing the use of recycled materials further reinforce brand positioning. As competition intensifies, companies that successfully balance technological innovation, cost efficiency, and strong customer engagement are emerging as leaders in the global electric passenger cars market.

LIST OF KEY ELECTRIC PASSENGER CARS COMPANIES PROFILED

- Tesla, Inc. (U.S.)

- BYD Auto (China)

- Volkswagen Group (Germany)

- SAIC Motor Corporation Limited (China)

- BMW Group (Germany)

- Hyundai Motor Company (South Korea)

- Stellantis N.V. (Netherlands)

- Ford Motor Company (U.S.)

- General Motors Company (U.S.)

- Mercedes-Benz Group AG (Germany)

- Nissan Motor Corporation (Japan)

- Renault Group (France)

- Toyota Motor Corporation (Japan)

- Great Wall Motor Company Limited (China)

- Chery Automobile Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS

- March 2025- Kia confirmed that it would start producing hybrid models at Hyundai’s new Georgia factory from mid-2026, shifting a plant originally planned as all EV to a mixed output of hybrids and electric vehicles. The move raises capacity to 500,000 vehicles annually and reflects a more flexible electrification strategy for the U.S. market.

- June 2024- BMW detailed its next wave of high-voltage battery plants, confirming that its Debrecen facility would build sixth-generation batteries in parallel with Neue Klasse EV production from 2025, with additional capacity in Shenyang, China. The strategy ties battery and vehicle production closely together to support the global rollout of its new EV architecture.

- March 2025- Volkswagen’s PowerCo division highlighted progress on gigafactories in Salzgitter, Valencia, and Ontario, building a vertically integrated battery value chain. These plants are central to VW’s plan to secure cell supply and scale electric passenger car production across Europe and North America.

- January 2024- Tesla made its refreshed 2024 Model 3 Highland available in the U.S., after first rolling it out in other regions. The update simplified the lineup to Long Range AWD and Rear-Wheel Drive versions, with revised styling, quieter cabin, and feature upgrades aimed at keeping the sedan competitive in the crowded mid-size EV segment.

- December 2025- Tesla launched a lower-priced Model 3 Standard variant in Europe after introducing it in the U.S. earlier in the year. The new trim is priced to undercut many rivals and is part of Tesla’s effort to defend market share as European and Chinese competitors push aggressively into the affordable EV space.

REPORT COVERAGE

The global electric passenger cars market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers & acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.1% from 2026-2034 |

|

Unit |

Value (USD Billion) Volume (Units) |

|

Segmentation |

By Powertrain, By Price, By Customer, By Charging Capability, By Range, and By Region |

|

By Powertrain |

|

|

By Price |

|

|

By Customer |

|

|

By Charging Capability |

|

|

By Range |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 601.61 billion in 2025 and is projected to reach USD 1,263.37 billion by 2034.

In 2025, the market value stood at USD 366.87 billion.

The market is expected to exhibit a CAGR of 9.1% during the forecast period (2026-2034).

The AC only segment is expected to lead the market by charging capability.

Rising consumer interests along with government incentives are the key factors driving market growth.

Key players in the global electric passenger cars market include Tesla, Inc., BYD Auto, Volkswagen Group, BMW Group, Hyundai Motor Company, Ford Motor Company, and General Motors Company.

Asia Pacific held the largest share in the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us