Electric Propulsion Satellite Market Size, Share & Industry Analysis, By Satellite Type (Hybrid & All-Electric), By Satellite Size (Small, Medium, & Heavy Satellites), By Propulsion (Electrothermal, Electrostatic, & Electromagnetic Propulsion), By Subsystem (Structure & Mechanisms, Thermal Control System, Electric Power System, Altitude Control System, Telemetry Tracking & Command, Flight Software, Propulsion System), By Application (Earth Observation & Sciences, Navigation, Telecommunications, Astronomy,), & Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

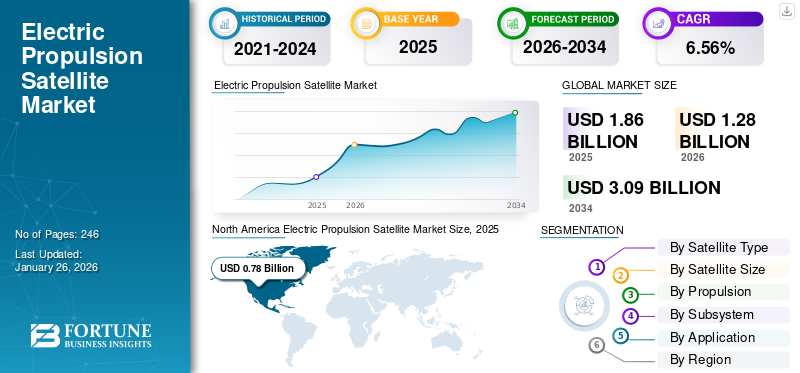

The global electric propulsion satellite market size was valued at USD 1.86 billion in 2025 and is projected to grow from USD 1.28 billion in 2026 to USD 3.09 billion by 2034, registering a CAGR of 6.56% over the forecast period. North America dominated the electric propulsion satellite market with a market share of 42.08% in 2025.

Electric propulsion satellite uses either a hybrid or an entirely electrical propulsion system. This is a type of space propulsion that uses electrical power to accelerate or ignite the combustion of fuel through different types of electric and electromagnetic energy. Electrothermal propulsion, electrostatic propulsion, and electromagnetic propulsion are some of the types of propulsion used in satellites. It may be used for a variety of space applications, such as Earth observation, navigation and telecommunications, astronomy, environment studies, and space research, according to their respective utilities.

For instance, in February 2023, Starfish Space announced that it would launch its electric propulsion Otterpower Pup satellite in the middle of 2023. This satellite is expected to dock with another satellite in late 2023, marking a significant milestone toward achieving high-performance, low-friction electric propulsion for commercial satellite docking in low Earth orbit. The high adoption of small satellites is driven by the demand for satellite constellations, threats of cyber-attacks, commercialization of the space industry, and the emphasis on new market entrants for small satellites, facilitated by the availability of commercially off-the-shelf spare parts.

The COVID-19 crisis significantly affected the space sector, leading to the suspension or deferral of contracts related to satellites and essential components and subsystems. According to the Organization for Economic Co-operation and Development (OECD), many medium & small enterprises that held a large share in the space industry were heavily impacted. The outbreak led to market concentration within the space industry, with smaller companies and startups, which played a crucial role in supporting innovation, job creation, and economic growth, being eliminated due to large entry barriers to the market.

Download Free sample to learn more about this report.

Electric Propulsion Satellite Market Overview & Key Metrics

Market Size & Forecast:

- 2025 Market Size: USD 1.86 billion

- 2026 Market Size: USD 1.28 billion

- 2034 Forecast Market Size: USD 3.09 billion

- CAGR: 6.56% from 2026–2034

Market Share:

- North America dominated the electric propulsion satellite market with a 42.27% share in 2024. This dominance is supported by high federal budget allocations for military, civil, and commercial satellite launches, along with the presence of key players such as Lockheed Martin, Northrop Grumman, and Boeing. The region leads in adopting electric propulsion technologies for small and large satellite constellations, driven by defense requirements and broadband connectivity initiatives.

- By satellite type, hybrid propulsion systems hold the largest share due to their combined fuel and electric capabilities, while all-electric propulsion satellites are projected to grow fastest, owing to reduced launch mass and cost advantages. Heavy satellites continue to dominate the size segment, but small satellites are emerging as the fastest-growing due to rising demand for low-Earth orbit (LEO) constellations for communications and Earth observation.

Key Regional Highlights:

- United States: Accelerating launches of small and hybrid electric satellites for defense and commercial use; government funding such as the U.S. Space Force’s USD 584 million space-tracking budget supports propulsion R&D.

- Europe: ESA’s investment in reducing satellite mass and launch costs through next-gen electric propulsion technology drives regional growth; Airbus and Thales lead innovation in hybrid and all-electric satellites.

- China & India: Rapid expansion of indigenous electric propulsion systems; initiatives like India’s GSAT and China’s LEO constellation programs support significant demand.

- Japan: Focused on advanced space research and interplanetary missions, driving demand for high-thrust electric propulsion solutions.

- Rest of the World: Emerging adoption in South America and the Middle East, with Argentina’s INVAP and Roscosmos partnerships marking strategic developments.

Electric Propulsion Satellite Market Trends

Recurring Demand for Small Satellites and their Constellations to Aid Electric Propulsion Satellite Market Growth

Over the past decade, there has been a significant increase in reliance on smaller satellites and their constellations for various defense and economic applications, driven by the development of the space industry. Small satellites, due to their affordability and the high availability of commercial off-the-shelf spare parts, are attracting new entrants to the space sector.

The number of smaller satellites will increase by around 1,000 from 2020 to 2022. From 2012 to 2022, more than 1,700 smaller satellites were placed in orbit. By 2025, around 1,000 little satellites will be launched into orbit every year.

- North America witnessed electric propulsion satellite market growth from USD 6.73 Billion in 2023 to USD 7.55 Billion in 2024.

For instance, in February 2023, the market evolved from analog to digital software satellites. MDA, one of the world's largest technology and services suppliers for the global space industry, launched a new line of Software Defined Digital Satellite Products.

Download Free sample to learn more about this report.

Electric Propulsion Satellite Market Growth Factors

Rising Number of Space Launches for Defense & Commercial Applications to Bolster Market Growth

The continued demand for satellites in defense and business applications, Including ISR activities, command & control operations, energy industry or government operations, is driving market growth. In addition, armed forces around the world use defense applications such as communications, navigation, intelligence, reconnaissance, and surveillance, further fueling demand.

Due to their high performance and efficiency, electric propulsion satellites are being used in a broad range of sectors, which will drive market developments. The all-electric small satellites are being increasingly utilized owing to their low cost and commercial availability of off-the-shelf systems & spare parts for satellite assembly. In addition, they are being used in a variety of sectors, such as banking, aviation, retail, energy and power, oil and gas, mining, telecommunications, and others, which further expands the market size.

This trend is anticipated to intensify, according to U.S. GAO, which projects the launch of 58,000 new satellites by the end of the decade, more than doubling the present number of operational spacecraft. The ongoing and projected launches of massive constellations aim to deliver critical services such as broadband internet access to underserved rural communities and so on.

Industry Investment in Advanced Technology and Government Funding for Space Surveillance to Promote Growth of the Market

Major market players such as Thales Group, OHB SE, Boeing Company, and others are investing in the high demand for electric propulsion satellites due to their strong thrust and efficiency and commercialization of space-based services. For instance, in February 2023, Thales Alenia Space was awarded a contract by the Korea Aerospace Research Institute (KARI) to supply its electric propulsion system for assembled onboard GEOKOMPSAT-3 satellites, which will be launched by 2027.

In April 2023, in order to raise awareness of the space domain, U.S. Space Forces invested in ground and surface sensors, surveillance systems, and data from business-tracking satellites. To improve the detection, tracking, and identification of objects orbiting Earth, the military branch's budget for fiscal year 2024 includes USD 584 million for space-tracking activities, such as the development of optical telescopes and surveillance satellites.

RESTRAINING FACTORS

High Cost of RDT&E to Develop Electric Propulsion System and Malfunctioning and High Cost of Sensors are Expected to Hinder the Market Growth

The process of developing electric propulsion satellites presents a technical challenge, requiring long-term, high-risk capital investments, according to a European Commission report on the electric propulsion and satellite sector. Private entities often collaborate with government agencies due to the significant financial resources required for such endeavors. Moreover, strict product and quality assurance standards, compulsory for all satellites, contribute to rising R&D costs.

The success of a space mission may be directly affected by malfunctioning satellite sensors. In order to make informed decisions throughout the mission, the accuracy and reliability of sensor data are essential. Failure of the sensors may result in insufficient data collection, a decline measurement accuracy, and more severe decisions.

Electric Propulsion Satellite Market Segmentation Analysis

By Satellite Type Analysis

High Adoption of All Electric Propulsions to Accelerate Satellite Manufacturing will drive Market Growth

Based on satellite type, the market is divided into hybrid and all-electric.

The all-electric segment was estimated to be the fastest-growing in 2024 to 2032. Increasing applications of space-based services in commercial and military domains are projected to surge the demand for all-electric propulsion satellites. These satellites are lightweight and incur low launch costs/kg due to the absence of conventional propellant storage systems.

The hybrid segment is projected to reach 61.59% of the global market share in 2026, fueled by the growing adoption of laser designation technology for airborne platforms. The growing fleet of a combination of electric propulsion and fuel-based propulsion systems is also one of the factors boosting the segment dominance.

By Satellite Size Analysis

Heavy Satellites Segment Dominated due to High Adoption of Small Satellites

Based on satellite size, the electric propulsion satellite market is classified into small satellites, medium satellites, and heavy satellites.

The heavy satellites segment held the largest market share in 2023 and is likely to grow at a significant CAGR during the forecast period owing to the considerable demand for heavy satellite from governments and armed forces globally.

The small satellites is estimated to be the fastest-growing segment during the forecast period, fueled by a notable rise in R&D investments for small, micro, and nano-satellites-based constellations. These investments aim to support various applications in areas such as armed forces, environmental research, in-flight communication, and satellite-based internet. Amid the Russia-Ukraine war, Starlink provided critical satellite-based support to the Ukrainian armed forces for military intelligence. The rise in the usage of commercial Low Earth Orbit (LEO) small satellite networks for military applications is anticipated to drive the demand for installation of small-sized electric propulsion satellites during the forecast period. The Heavy Satellites segment led by satellite mass, capturing 44.38% of the market share in 2026.

- The small satellites segment is expected to hold a 44% share in 2024.

To know how our report can help streamline your business, Speak to Analyst

By Propulsion Analysis

Electrothermal Propulsion Segment Led due to High Demand for Electrothermal Propulsion of Satellites

By propulsion, the market is classified into electrothermal propulsion, electrostatic propulsion, and electromagnetic propulsion.

The electrothermal propulsion segment captured the highest market share in 2023, and is expected to maintain its dominance during the forecast period. Key players globally have invested in the R&D of electrothermal propulsion for satellites, owing to the high demand for electrothermal propulsion of satellites.

The electrostatic propulsion segment is anticipated to be the fastest-growing during the forecast period. Rising requirements for various ion thruster engines in satellite manufacturing are bolstering market development. Government investment in electrostatic propulsion systems on satellite platforms is anticipated to drive market growth during the forecast period.

By Subsystem Analysis

Propulsion System Segment Dominates due to Increased Investment in Propulsion Systems

Based on subsystem, the market is divided into structure & mechanisms, Thermal Control System (TCS), Electric Power System (EPS), Altitude Control System (ACS), telemetry tracking & command, flight software, propulsion system, and others.

The propulsion system segment is anticipated to be the fastest-growing segment during the forecast period. Space agencies and key market players across the globe have been investing in and adopting next-generation electric propulsion systems, allocating funds from their federal budgets for space propulsion, driven by high demand for satellite services for various applications.

The Electric Power System (EPS) segment is also estimated to register a significant CAGR during the analysis timeline. The rising adoption of subsystems onboard satellite buses under government modernization programs will propel the market progress during the forecast period. Government investment in military, civilian, and commercial platforms against various threats is anticipated to drive market growth in the coming years.

By Application Analysis

Earth Observation & Sciences Segment Dominated Owing to Development of Next-Generation Earth Observation Satellites

In terms of application, the market is segmented into earth observation & sciences, navigation, telecommunication, astronomy, interplanetary & space exploration, and others.

The earth observation & sciences segment is projected to reach 34.50% of the market share in 2026. Space agencies are developing cutting-edge earth observation & environmental sciences satellites, particularly for Low Earth Orbit (LEO) systems, which is anticipated to boost the market outlook.

The telecommunication segment is also estimated to be the fastest-growing during the study period. This surge is fueled by high usage of satellite-based telecommunication, including in-flight communication & entertainment and other telecommunication services. Government investment in military and commercial telecommunication infrastructure is also anticipated to propel the market during the forecast period.

REGIONAL INSIGHTS

Based on region, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America Electric Propulsion Satellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, North America held 42.08% of the global market share, reaching a valuation of USD 0.78 billion, and is projected to grow to USD 0.54 billion in 2026. High federal budget allocation for new-generation military, civilian, and commercial satellite launches due to the growing need for satellite-based services will boost regional market development. Since the commercialization of the space industry in 2008, many new entrants have flourished in the North American space sector. Additionally, an increased number of small satellite launches is anticipated to bolster the market growth during the forecast period. The U.S. market is projected to reach USD 0.51 billion by 2026.

Europe

The market in Europe reached USD 0.35 billion in 2025, representing 18.82% of total market revenue, and is projected to reach USD 0.24 billion in 2026. The European Union member states have planned to invest in the European Space Agency (ESA) to make next-generation satellites for electric propulsion systems to reduce the launch mass and cost. This factor will propel the electric propulsion satellite market growth over the coming years. The UK market is projected to reach USD 0.06 billion by 2026 and the Germany market is projected to reach USD 0.03 billion by 2026.

Asia Pacific

Asia Pacific contributed approximately USD 0.49 billion to the global market in 2025, accounting for 26.46% share, and is expected to reach USD 0.34 billion in 2026. This growth is attributed to increased R&D investment in indigenous electric propulsion capabilities by regional space agencies and market key players. These systems are also being widely used in defense and homeland security operations, coupled with rising budgetary allocation, driving market development in the region. The Japan market is projected to reach USD 0.05 billion by 2026, the China market is projected to reach USD 0.15 billion by 2026, and the India market is projected to reach USD 0.07 billion by 2026.

Rest of the world

The Rest of the World market accounted for USD 0.24 billion in 2025, representing 12.64% of the global industry, and is expected to reach USD 0.16 billion in 2026. The rest of the world is expected to hold a significant market share. Still, it will record a lower-than-average CAGR during the forecast period due to a lack of financial support from the governments and demand for space programs.

KEY INDUSTRY PLAYERS

Increase in Joint Ventures by Key Players to Boost the Market Growth

The global market is growing at a substantial pace due to the presence of key market players such as Lockheed Martin Corporation, The Boeing Company, Thales Group, Aerojet Rocketdyne Holdings Inc., Airbus S.A.S., Northrop Grumman Corporation and others. In order to gain competitive advantage, the growing adoption of electrical propulsion over fossil fuels is a key element in the electric propulsion satellite market share. The reduction of overall costs and the acquisition of more ride share missions will be supported by additional factors, e.g. technical advances and collaboration.

List of Top Electric Propulsion Satellite Companies:

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Thales Group (France)

- The Boeing Company (U.S.)

- Airbus S.A.S. (France)

- OHB S.E. (Germany)

- INVAP S.E. (Argentina)

- Accion Systems Inc.

- Aerojet Rocketdyne Holding Inc. (U.S.)

- ArianeGroup GmbH (France)

- AeroAstro Inc. (U.S.)

- SSC Roscosmos (Russia)

- Safran Group (France)

- Sitael S.p.A. (Italy)

KEY INDUSTRY DEVELOPMENTS:

- February 2023 – Thales Alenia Space awarded a contract by the Korea Aerospace Research Institute (KARI) to supply electric propulsion systems for the GEO-KOMSAT-3 multi-band communication satellite equipped with Satellite-based Augmentation System (SBAS), scheduled to launch by 2027.

- April 2023 –Exotrail unveiled a new contract with the satellite manufacturer Satrec Initiative to embark on a spaceware electric propulsion system for a Korean governmental mission. The Satrec Initiative is the global leader in Earth observation solutions, and it operates from Korea. To meet the needs of an Earth observation satellite for space mobility, which would serve as a government research and development mission in Korea, they chose to use the Exotrails Spaceware product.

- June 2023 – A Memorandum of Understanding (MoU) signed between Safran Electronics & Defense and Terran Orbital to study and validate the requirements for the production of a new generation of electric propulsion systems for satellites in the U.S., based on Safran PPSX00 plasma thrusters.

- September 2023 – A contract with ENPULSION to supply their CONNECT Internet of Things (IoT) constellation with electric propulsion systems signed by PlanSys, one of the largest private initiatives in the satellite and space technology sector in Turkey. The ENPULSION NANO propulsion system, which has more than 200 of its units already in space, combines heritage with an optimal design for a tiny spacecraft.

- December 2023 – Neutron Star Systems (NSS) announced the signing of its second contract with the European Space Agency to deliver “Very High Thrust Density for Space Transportation.” Under the agreement, NSS and its partners are to develop and produce a prototype of high-power HPEP electric propulsion technology, which would lay the foundations for future missions carrying out the deployment of these technologies to ensure European independence and operational capacity.

REPORT COVERAGE

The research report analyzes various aspects, such as key players, regional analysis, product offerings, and end-users of electric propulsion satellites. It also offers market insights into advanced technologies, trends, competitive landscape, and product pricing and highlights key industry developments. In addition to the aspects mentioned above, it encompasses several direct and indirect factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 6.56% from 2026 to 2034 |

|

Segmentation |

By Satellite Type

|

|

By Satellite Size

|

|

|

By Propulsion

|

|

|

By Subsystem

|

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 1.86 billion in 2025 and is projected to grow from USD 1.28 billion in 2026 to USD 3.09 billion by 2034.

Registering a CAGR of 6.56%, the market will exhibit steady growth in the forecast period.

The small satellite segment was the leading segment in the market.

Lockheed Martin Space, Thales Group, The Boeing Company, Airbus S.A.S., OHB S.E., Aerojet Rocketdynem, Northrop Grumman Corporation are the leading players in the global market.

North America held a dominant market share in 2024.

- 2021-2034

- 2025

- 2021-2024

- 246

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us