Electric Vehicle Charging Infrastructure Market Size, Share & Industry Analysis, By Vehicle Type (Passenger Cars and Commercial Vehicles), By Charger Type (AC Charging and DC Fast Charging), By Connector Type (CCS, CHAdeMO, GB/T, Tesla Supercharger, and Others), By Charging Location (Residential, Commercial, and Public), By Power Output (Slow, Fast, and Ultra-fast), By Component (Hardware and Software), and Regional Forecast, 2026-2034

Electric Vehicle Charging Infrastructure Market Size and Future Outlook

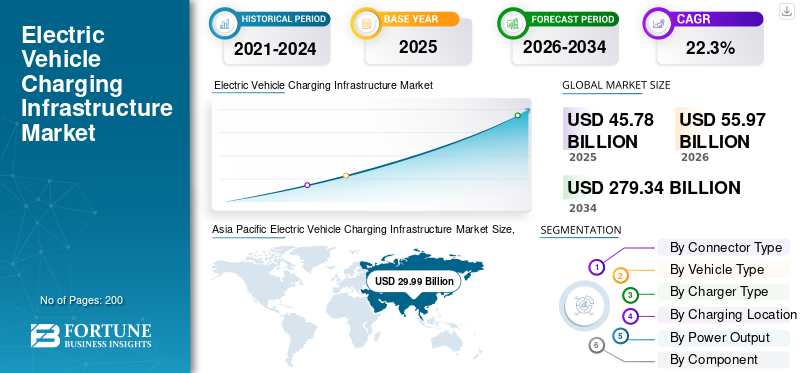

The electric vehicle charging infrastructure market size was valued at USD 45.78 billion in 2025. The market is projected to grow from USD 55.97 billion in 2026 to USD 279.34 billion by 2034, exhibiting a CAGR of 22.3% during the forecast period. Asia Pacific dominated the electric vehicle charging infrastructure market with a market share of 65.51% in 2025.

Electric vehicle charging infrastructure comprises AC and DC charging stations, software platforms, grid connectivity systems, and energy management technologies supporting electric vehicle charging across residential, commercial, and public transportation networks globally. Market growth is driven by rising adoption of electric vehicles, government incentives, expanding fast-charging networks, battery technology advancements, emission reduction targets, increasing fuel prices, and growing demand for sustainable transportation solutions.

Major players in the market include Tesla Inc., ChargePoint Holdings Inc., ABB Ltd., Siemens AG, Schneider Electric SE, and EVgo Inc., competing through ultra-fast charging technologies, network expansion, smart energy management, software integration, and strategic partnerships supporting market growth and evolving demand.

Download Free sample to learn more about this report.

ELECTRIC VEHICLE CHARGING INFRASTRUCTURE MARKET Key Takeaways

- 2025 Market Size: USD 45.78 billion

- 2026 Market Size: USD 55.97 billion

- 2034 Forecast Market Size: USD 279.34 billion

- CAGR: 22.3% from 2026–2034

- Asia Pacific dominated the electric vehicle charging infrastructure market with a market share of 65.51% in 2025.

- The commercial vehicles segment is projected to expand at a CAGR of 24.7% during the market forecast period.

- The residential segment accounted for the second-largest market share and is projected to expand at a CAGR of 19.6% during the market forecast period.

Asia Pacific

The region accounted for USD 29.99 billion in 2025 (65.51% share) and continues to lead the global market, supported by rapid EV adoption, large-scale charging infrastructure expansion.

Europe

Europe accounted for the second-largest market share and is projected to expand at a CAGR of 18.6% during the market forecast period, supported by strong carbon neutrality targets, EV subsidies, and expanding charging infrastructure.

North America

North America accounted for the third-largest market share due to rising electric vehicle adoption, expanding public charging infrastructure, and strong investments from utilities, automakers, and charging network providers.

U.S.

The U.S. market is estimated at USD 5.35 billion in 2026, accounting for approximately 9.6% of global revenue, driven by federal infrastructure funding, commercial fleet electrification, and highway fast-charging expansion.

Japan

The Japan market is estimated at USD 1.89 billion in 2026, representing around 3.4% of global revenue, supported by increasing EV adoption, smart charging technologies, and continued investment in urban charging infrastructure.

Read More

ELECTRIC VEHICLE CHARGING INFRASTRUCTURE MARKET TRENDS

Government Incentives and Emission Policies Accelerate Charging Infrastructure Deployment

Governments across major economies are introducing subsidies, tax credits, zero-emission vehicle mandates, and infrastructure funding programs to accelerate adoption of electric vehicles charging deployment. Regulatory initiatives supporting carbon neutrality and transportation electrification are increasing investments in public and private charging networks. National programs across the U.S., Europe, China, and India are encouraging utilities, automakers, and charging operators to expand infrastructure coverage. These initiatives are significantly improving market growth by supporting large-scale installation of fast-charging stations and strengthening long-term market expansion for accessible EV charging solutions globally.

- In January 2026, India accelerated EV charging infrastructure expansion through the PM E-DRIVE scheme, targeting 72,000 new public chargers nationwide with government funding, highway corridor deployment, smart charging integration, and unified digital charging platform development to support rising number of EV adoption and reduce range anxiety.

Integration of Smart Charging and Energy Management Technologies Emerges as Key Trend

The market is witnessing increasing adoption of smart charging technologies integrated with artificial intelligence, IoT platforms, cloud monitoring, and energy management software. Operators are deploying intelligent systems capable of dynamic load balancing, predictive maintenance, remote monitoring, and optimized electricity consumption. Vehicle-to-grid integration and renewable energy synchronization are also becoming important market trends across commercial and public charging ecosystems. These technologies improve operational efficiency, reduce energy costs, and enhance user experience while supporting grid stability, creating advanced digital charging ecosystems during market forecast period.

- In May 2026, Driivz partnered with Dunamis Charge to accelerate U.S. EV charging infrastructure expansion through smart energy management platforms, AI-enabled charging optimization, and scalable Level-2 and DC fast-charging deployments across commercial, residential, fleet, and public charging stations networks nationwide.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Electric Vehicle Adoption Drives Charging Infrastructure Expansion

The rapid increase in global electric vehicle adoption is directly driving demand for extensive charging infrastructure networks. Automakers are expanding EV production portfolios across passenger and commercial vehicle categories, increasing the requirement for reliable public and residential charging solutions. Consumers are also increasingly shifting toward electric mobility due to environmental awareness, fuel savings, and supportive government policies. Growing EV sales volumes are encouraging utilities, oil companies, and private investors to accelerate charging station deployment, strengthening overall electric vehicle charging infrastructure market growth and supporting long-term infrastructure investments across developed and emerging economies.

Expansion of Ultra-Fast Charging Networks Supports Long-Distance Mobility

Charging infrastructure providers are rapidly expanding DC fast-charging and ultra-fast charging networks to reduce charging time and improve convenience for EV users. High-power charging systems capable of delivering rapid energy replenishment are becoming essential for highways, logistics fleets, and urban transportation hubs. Automakers and charging operators are collaborating to deploy interoperable high-speed charging corridors supporting long-distance travel. This trend is improving consumer confidence in electric mobility while supporting market growth for scalable and efficient charging ecosystems that address range anxiety and increase electric vehicle usability globally.

- In May 2026, BYD strengthened its European EV charging infrastructure presence by expanding dealership-based ultra-fast charging networks in Hungary, introducing flash charging technology capable of rapid battery charging, and accelerating charging ecosystem expansion alongside rising electric vehicle sales and market growth across Europe.

MARKET RESTRAINTS

High Initial Infrastructure Investment Restrains Market Penetration in Emerging Economies

The deployment of electric vehicle charging infrastructure requires substantial capital investment in equipment, grid upgrades, installation, land acquisition, and maintenance. Emerging economies often face financial limitations, inconsistent electricity supply, and inadequate urban planning, slowing infrastructure expansion. Smaller charging operators encounter difficulties achieving profitability due to high operational expenses and uncertain utilization rates during early adoption phases. These challenges restrict widespread deployment in cost-sensitive regions, limiting market growth potential despite increasing adoption of electric vehicles and rising interest in sustainable transportation infrastructure development.

MARKET OPPORTUNITIES

Fleet Electrification Creates Opportunities for Commercial Charging Infrastructure Providers

The increasing electrification of logistics fleets, public transportation, ride-hailing services, and corporate mobility operations is creating major opportunities for commercial charging infrastructure providers. Fleet operators require dedicated high-capacity charging stations capable of supporting large vehicle volumes and minimizing operational downtime. Charging companies are developing depot charging solutions, energy optimization systems, and subscription-based charging services, targeting commercial customers. The transition toward electric delivery vans, buses, and freight vehicles is expected to generate substantial market opportunities while accelerating infrastructure investments throughout the market forecast period.

- In May 2026, Amazon India partnered with Eicher Trucks to deploy 1,000 electric trucks by 2028, accelerating commercial fleet electrification and increasing demand for depot charging infrastructure, smart fleet energy management systems, and high-capacity EV charging networks across India’s logistics sector.

Renewable Energy Integration Opens Opportunities for Sustainable Charging Ecosystems

The integration of renewable energy sources such as solar and wind power with EV charging infrastructure is creating new growth opportunities across the industry. Charging operators are increasingly deploying solar-powered charging stations, battery energy storage systems, and microgrid solutions to reduce electricity costs and carbon emissions. Renewable-integrated charging ecosystems support energy independence and improve grid resilience while aligning with global sustainability targets. This transition is attracting investments from utilities, governments, and private companies seeking environmentally sustainable charging solutions and supporting long-term market growth and innovation.

- In December 2025, Exicom launched Exicom One, an end-to-end EV charging infrastructure deployment platform integrating installation, remote monitoring, predictive maintenance, and energy optimization capabilities, supporting faster charging network expansion, reduced operational costs, and scalable deployment of AC and DC fast-charging solutions across India.

MARKET CHALLENGES

Grid Capacity Limitations and Power Management Complexities Impact Infrastructure Scalability

Rapid expansion of EV charging infrastructure is increasing pressure on electricity grids, particularly in densely populated urban regions and high-demand transportation corridors. Large-scale deployment of fast chargers requires substantial power capacity, creating challenges related to peak electricity demand, grid stability, and energy distribution efficiency. Utilities and charging operators must invest heavily in grid modernization, energy storage, and smart load management systems to avoid power disruptions. These infrastructure challenges may delay deployment timelines and affect the scalability of high-speed charging networks in several regional markets.

Segmentation Analysis

By Connector Type

Expanding Public Fast-Charging Deployment and Government Support Leads to GB/T Segment Dominance

Based on connector type, the market is segmented into CCS, CHAdeMO, GB/T, tesla supercharger, and others.

The GB/T segment dominates the market and is projected to witness the fastest growth due to China’s extensive electric vehicle ecosystem, strong government support, and large-scale public charging infrastructure deployment. China continues expanding nationwide fast-charging corridors and urban charging stations compatible with GB/T standards. High domestic EV production volumes, increasing commercial fleet electrification, and integration of ultra-fast charging technologies further strengthen market growth, supporting the segment’s leading market share throughout the market forecast period.

The CCS segment accounted for the second-largest electric vehicle charging infrastructure market share and is projected to expand at a CAGR of 20.1% during the market forecast period. Increasing adoption of European and North American electric vehicles, combined with rising deployment of high-power DC fast chargers and cross-border charging compatibility initiatives, is accelerating CCS infrastructure expansion globally.

- In November 2025, Servotech Power Systems secured a patent for its CCS2-to-GB/T EV charging converter technology, enabling seamless compatibility between charging standards, improving charging infrastructure utilization, and supporting scalable deployment across electric buses, commercial fleets, and public fast-charging networks in India.

To know how our report can help streamline your business, Speak to Analyst

By Vehicle Type

Rising Passenger EV Ownership and Expanding Urban Charging Networks Leads to Passenger Cars Segment Growth

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment dominates the market due to rising electric passenger vehicle adoption, expanding residential and public charging infrastructure, and increasing consumer preference for sustainable mobility solutions. Governments across major economies are supporting passenger EV adoption through subsidies, tax incentives, and emission reduction policies, accelerating charging station deployment. High daily charging frequency, growing urban EV penetration, and continuous expansion of fast-charging networks further strengthen market growth, enabling the segment to maintain its leading market share during the market forecast period.

The commercial vehicles segment is projected to expand at a CAGR of 24.7% during the market forecast period. Rapid electrification of delivery fleets, public buses, and logistics vehicles is increasing demand for high-capacity charging infrastructure, depot charging systems, and ultra-fast commercial charging networks globally.

By Charger Type

Expanding Ultra-Fast Charging Corridors and Reduced Charging Time leads to DC Fast Charging Segment Dominance

Based on charger type, the market is segmented into AC charging and DC fast charging.

The DC fast charging segment dominates the market and is projected to witness the fastest market growth due to increasing demand for rapid vehicle charging, expanding highway charging corridors, and rising adoption of long-range electric vehicles. Governments, utilities, and private charging operators are heavily investing in ultra-fast public charging infrastructure to reduce charging duration and improve EV convenience. Growing commercial fleet electrification, higher charging capacities, and advancements in high-power charging technologies are further accelerating segment growth and strengthening the segment’s leading share globally.

- In September 2025, Tata Power and Tata Passenger Electric Mobility Ltd. inaugurated India’s largest TATA.ev MegaCharger hub in Mumbai with 16 fast-charging bays and charging speeds of up to 120 kW.

The AC charging segment is projected to expand at a CAGR of 17.9% during the market forecast period. Rising residential EV adoption, lower installation costs, and increasing deployment across workplaces, apartments, and commercial parking facilities continue supporting AC charging infrastructure expansion worldwide.

By Charging Location

Expanding Public Charging Networks and Urban EV Adoption Propel Segment Growth

Based on charging location, the market is segmented into residential, commercial, and public.

The public charging segment dominates the market and is projected to witness the fastest market growth due to increasing deployment of fast-charging stations across highways, urban centers, retail hubs, and transportation corridors. Governments and private operators are investing heavily in accessible public charging infrastructure to support rising adoption of EVs and reduce range anxiety. Expansion of ultra-fast charging networks, smart payment integration, and growing utilization by ride-hailing and commercial fleets are further strengthening the segment’s leading share globally.

- In May 2026, Maharashtra state in India announced plans to establish around 200 EV charging stations under a public-private partnership model to support the electrification of the entire MSRTC bus fleet by 2035.

The residential segment accounted for the second-largest market share and is projected to expand at a CAGR of 19.6% during the market forecast period. Rising home EV ownership, convenience of overnight charging, and increasing installation of smart home charging systems continue to support residential charging infrastructure industry growth worldwide.

By Power Output

Increasing High-Power Charging Deployment and Highway Infrastructure Expansion Augment Fast Charging Deployment

Based on power output, the market is segmented into slow, fast, and ultra-fast charging.

The fast charging segment dominates the market due to its balanced charging speed, wider infrastructure availability, and compatibility with both urban and intercity electric vehicle usage. Charging network operators are increasingly deploying fast chargers across commercial centers, public parking areas, highways, and fleet depots to improve charging accessibility and reduce vehicle downtime. Growing electric passenger vehicle adoption, expanding public charging corridors, and rising investments from utilities and automakers are further supporting the segment’s leading share globally.

The ultra-fast charging segment is projected to expand at a CAGR of 24.5% during the market forecast period. Increasing demand for minimal charging time, long-distance EV travel convenience, and large-scale deployment of high-capacity charging stations are accelerating the adoption of ultra-fast charging infrastructure worldwide.

- In March 2025, BYD unveiled its Super e-Platform featuring megawatt flash charging technology capable of delivering 400 kilometers of driving range in five minutes with 1000 kW charging power.

By Component

Expanding Charging Station Deployment and Equipment Investments Boost Hardware Segment Growth

Based on the component, the market is segmented into hardware and software.

The hardware segment dominates the market due to increasing installation of charging stations, connectors, power modules, transformers, and energy management equipment across residential, commercial, and public charging networks. Governments and private charging operators are heavily investing in physical charging infrastructure expansion to support rising electric vehicle adoption globally. Growing deployment of DC fast chargers, ultra-fast charging systems, and smart grid-compatible hardware solutions is further strengthening segment growth and enabling it to maintain its leading market share throughout the market forecast period.

The software segment is projected to expand at a CAGR of 26.7% during the market forecast period. Rising adoption of smart charging platforms, remote monitoring systems, payment integration software, and AI-based energy optimization technologies is accelerating software demand across connected charging ecosystems globally.

- In May 2026, the Government of India announced the development of a unified EV charging application to integrate charging stations nationwide, enabling real-time charger discovery, slot booking, digital payments, and improved accessibility for electric vehicle users across the country.

Electric Vehicle Charging Infrastructure Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America and Middle East & Africa.

Asia Pacific

Asia Pacific Electric Vehicle Charging Infrastructure Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the market and is projected to witness the fastest growth due to large-scale electric vehicle adoption, strong government incentives, and rapid charging infrastructure expansion across China, Japan, South Korea, and India. China leads regional market through aggressive public charging deployment and domestic EV manufacturing growth. Rising investments in ultra-fast charging corridors, smart charging technologies, and commercial fleet electrification are further accelerating market growth. Increasing urbanization, supportive emission regulations, and expanding renewable energy integration continue to strengthen the region’s long-term market growth potential during the market forecast period.

- In April 2024, Hubject launched Plug&Charge technology in the Asia Pacific region, expanding its global EV charging interoperability network across over 600,000 connected charging points in 60 countries.

China Electric Vehicle Charging Infrastructure Market

The China market in 2026 is estimated at around USD 25.45 billion, accounting for roughly 45.5% of global revenues. Market growth is driven by extensive public charging deployment, strong domestic EV production, government incentives, and rapid expansion of ultra-fast charging corridors supporting large-scale electric mobility adoption nationwide.

Japan Electric Vehicle Charging Infrastructure Market

The Japan market in 2026 is estimated at around USD 1.89 billion, accounting for roughly 3.4% of global revenues. Rising hybrid-to-EV transition, smart charging technology adoption, and increasing investments in urban fast-charging infrastructure continue supporting steady market growth and infrastructure modernization across the country.

India Electric Vehicle Charging Infrastructure Market

The India market in 2026 is estimated at around USD 1.92 billion, accounting for roughly 3.4% of global revenues. Rapid electric mobility adoption, government subsidy programs, expanding commercial fleet electrification, and increasing investments in public charging networks are accelerating market growth throughout urban and highway transportation corridors.

Europe

Europe accounted for the second-largest market share and is projected to expand at a CAGR of 18.6% during the market forecast period. Strong carbon neutrality targets, extensive EV subsidies, and stringent vehicle emission regulations are accelerating charging infrastructure deployment across Germany, the U.K., France, and the Nordic countries. Public and private investments in cross-border charging corridors and ultra-fast charging stations are supporting regional market growth. Rising electric passenger vehicle adoption, increasing renewable energy integration, and expanding partnerships between utilities, automakers, and charging operators continue to strengthen overall market growth throughout Europe.

- In May 2026, Fastned and Places for London received approval for London’s largest ultra-rapid EV charging hub in Ealing, featuring 36 charging bays powered entirely by renewable energy.

Germany Electric Vehicle Charging Infrastructure Market

The Germany market in 2026 is estimated at around USD 2.82 billion, accounting for roughly 5.0% of global revenues. Strong emission regulations, expanding renewable energy integration, and rising deployment of ultra-fast charging stations continue driving infrastructure expansion and long-term market growth across the country.

U.K. Electric Vehicle Charging Infrastructure Market

The U.K. market in 2026 is estimated at around USD 2.16 billion, accounting for roughly 3.9% of global revenues. Increasing electric passenger vehicle adoption, government net-zero initiatives, and investments in public rapid-charging networks are strengthening market growth and supporting nationwide charging accessibility improvements.

North America

North America accounted for the third-largest market share due to rising electric vehicle adoption, expanding public charging infrastructure, and strong investments from utilities, automakers, and charging network providers. The U.S. leads regional market growth through federal infrastructure funding programs and increasing deployment of fast-charging stations across highways and urban areas. Growing electrification of commercial delivery fleets and ride-hailing services is further increasing charging infrastructure demand. Advancements in smart charging technologies, grid modernization initiatives, and partnerships supporting interoperable charging networks continue contributing to the region’s market growth and infrastructure expansion.

- In April 2026, XCharge North America and JOJO Superfast EV Charging partnered to deploy a high-power EV charging network across Illinois, featuring 800 kW ultra-fast charging capacity at nine strategic locations.

U.S. Electric Vehicle Charging Infrastructure Market

The U.S. market in 2026 is estimated at around USD 5.35 billion, accounting for roughly 9.6% of global revenues. Federal infrastructure funding, expanding EV adoption, commercial fleet electrification, and growing deployment of highway fast-charging corridors continue accelerating overall market growth and infrastructure investments nationwide.

South America

South America is experiencing steady market growth driven by increasing electric mobility adoption, government sustainability initiatives, and the gradual expansion of public charging infrastructure across Brazil, Chile, and Colombia. Rising fuel prices and growing environmental awareness are encouraging investments in electric transportation and charging station deployment. Several regional governments are introducing policies supporting EV imports and clean transportation infrastructure development. Private companies and utilities are also investing in highway charging corridors and urban charging networks. Expanding commercial fleet electrification is expected to further strengthen market growth across the region during the forecast period.

- In April 2026, Power2Drive South America highlighted that Brazil’s public and semi-public EV charging infrastructure reached 21,061 charging points, including 6,479 DC fast chargers, with the fast-charging segment growing 167% year-on-year.

The Middle East & Africa

The Middle East & Africa accounted for the fourth-largest market share due to growing investments in sustainable transportation infrastructure and rising government focus on economic diversification and carbon reduction strategies. Countries including the UAE, Saudi Arabia, and South Africa are expanding public charging networks to support increasing electric vehicle adoption. Smart city projects, tourism-driven infrastructure modernization, and renewable energy integration are contributing to charging infrastructure deployment. Partnerships between utilities, governments, and private charging operators are further supporting regional market growth and improving accessibility of electric vehicle charging solutions across the region.

- In March 2026, Chaevi partnered with Emirates Electrical Engineering to supply 1,000 EV charging units across the UAE, supporting the expansion of electric vehicle charging infrastructure throughout the Middle East and North Africa region.

COMPETITIVE LANDSCAPE

Key Industry Players

Fast-Charging Expansion, Smart Energy Integration, and Network Partnerships Define Market Competition

The market is moderately fragmented, with global technology providers, charging network operators, utilities, and energy management companies competing through charging speed, software capabilities, and infrastructure scalability. Key players, including Tesla Inc., ChargePoint Holdings Inc., ABB Ltd., Siemens AG, Schneider Electric SE, and EVgo Inc., focus on ultra-fast charging deployment, smart charging software, and renewable energy integration. Companies are expanding partnerships with automakers, governments, and commercial fleet operators to strengthen market share and regional presence.

- In April 2026, ABB E-mobility launched the modular M-Series EV charging system, scalable from 200 kW to 1.2 MW, supporting up to 24 charge points for public fast-charging, retail, and commercial fleet charging applications.

LIST OF KEY ELECTRIC VEHICLE CHARGING INFRASTRUCTURE COMPANIES PROFILED

- Tesla, Inc. (U.S.)

- ChargePoint Holdings, Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Siemens AG (Germany)

- Schneider Electric SE (France)

- EVgo Inc. (U.S.)

- BP Pulse (U.K.)

- Shell Recharge Solutions (Netherlands)

- Blink Charging Co. (U.S.)

- Tritium DCFC Limited (Australia)

- Delta Electronics, Inc. (Taiwan)

- Star Charge / Wanbang Digital Energy Co., Ltd. (China)

- TELD New Energy Co., Ltd. (China)

- Webasto Group (Germany)

- Wallbox N.V. (Spain)

KEY INDUSTRY DEVELOPMENTS

- April 2026: ENGIE Vianeo announced plans to install nearly 3,000 EV charging points across Wallonia, strengthening its position as one of Belgium’s leading public electric vehicle charging infrastructure operators.

- March 2026: ChargePoint launched Premier Care and the Support Portal, introducing advanced EV charger management solutions featuring proactive monitoring, analytics, case management, and self-service technical support capabilities for charging station operators.

- September 2025: VE Commercial Vehicles and Jio-bp pulse partnered to expand EV charging infrastructure for commercial vehicles, enabling access to over 6,000 charging points across India through integrated fleet charging solutions.

- June 2025: Tritium launched its TRI-FLEX EV charging architecture in Europe, designed to support next-generation DC fast-charging infrastructure and address rising EV charging demand across the European market.

- April 2025: Siemens launched the SICHARGE FLEX distributed EV charging system, delivering scalable charging capacity from 480 kW to 1.68 MW with dynamic power distribution and support for megawatt charging applications.

- March 2025:ev partnered with Shell to launch 21 mega EV charging hubs across Bengaluru, Chennai, Vadodara, Pune, and major Indian highways to expand high-speed public charging infrastructure nationwide

- April 2024: EVgo opened its first prefabricated public EV charging station in Texas, aiming to reduce charging station construction costs by 15% and installation timelines by up to 50%.

REPORT COVERAGE

The global electric vehicle charging infrastructure market analysis provides an in-depth study of the market size & forecast by all the market segments included in the market report. It includes details on the market dynamics and trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key automotive industry developments, and details on partnerships, mergers, and acquisitions. The market report scope also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 22.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Connector Type, By Vehicle Type, By Charger Type, By Charging Location, By Power Output, By Component, and By Region |

| By Connector Type |

|

| By Vehicle Type |

|

| By Charger Type |

|

| By Charging Location |

|

| By Power Output |

|

| By Component |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 45.78 billion in 2025 and is projected to reach USD 279.34 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 29.99 billion.

The market is expected to exhibit a CAGR of 22.3% during the forecast period of 2026-2034.

The public segment leads the market by charging location.

Rising electric vehicle adoption drives charging infrastructure expansion.

Major players in the market include Tesla Inc., ChargePoint Holdings Inc., ABB Ltd, Siemens AG, Schneider Electric SE, and EVgo Inc.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us