Electroceuticals Market Size, Share & Industry Analysis, By Device (Cardiac Rhythm Management (CRM) Devices, Neuromodulation Devices, Cochlear & Auditory Implants, Retinal & Vision Implants, and Others), By Modality (Implantable and Non-Implantable), By Application (Cardiology, Neurology, Pain Management, Otolaryngology, and Others), By End-user (Hospitals, Specialty Clinics, Homecare Settings, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

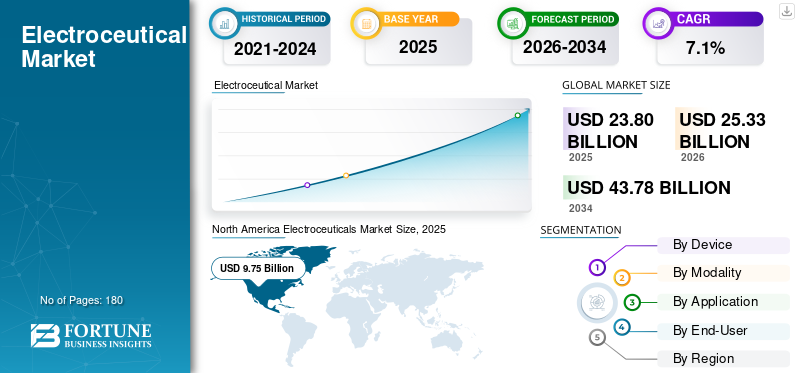

The global electroceuticals market size was valued at USD 23.80 billion in 2025 and is projected to grow from USD 25.33 billion in 2026 to USD 43.78 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the global market with a share of 40.97% in 2025.

Electroceuticals are a type of medical treatments that use small, controlled electrical signals to help the body work better. Instead of using drugs to change body functionality, these devices use electric signals for the treatment of disease symptoms. Market growth is attributed to the increasing prevalence of cardiac conditions, hearing abnormalities, and technological advancements in electrical implants. In addition, continual investments and research & development activities conducted by market players for innovating superior devices are also projected to have a positive impact on the market growth.

- For instance, in May 2023, Medtronic received FDA approval for its next-generation Micra systems, which allow leadless pacing functionalities. In addition, the new devices offer 40% more battery

Moreover, Medtronic plc, Abbott, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, and MicroPort Scientific Corporation are major market participants. They emphasize creating numerous state-of-the-art technologies to provide better products with better precision and efficacy.

Download Free sample to learn more about this report.

ELECTROCEUTICALS MARKET TRENDS

Shift Toward Simpler, Patient-Friendly Electroceutical Solutions is a Key Trend

The market is witnessing a gradual shift toward simpler and more patient-friendly devices. Moreover, companies are focusing on designs that are smaller, more comfortable, and easier for patients to manage in daily life. In addition, there is also growing interest in therapies that require less frequent hospital visits, supported by better device monitoring and follow-up options. In addition, an increasing number of product approvals is further boosting this trend in the global market.

- For instance, in February 2024, Medtronic received FDA approval for its world’s first adaptive deep brain stimulation for the treatment of Parkinson’s disease.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Burden of Cardiac Conditions to Accelerate Market Growth

The rising prevalence of cardiac conditions across the globe is estimated to accelerate market growth during the forecast period. Heart rhythm issues are common and often need long-term management. Electroceutical devices such as pacemakers and defibrillators are widely used as they can continuously support the heart without daily medicine dependence. This makes them a practical choice for hospitals treating large patient loads. New product upgrades keep demand strong.

- For instance, according to data published by the Centers for Disease Control and Prevention, an estimated 12.1 million people in the U.S. will be suffering from atrial fibrillation.

MARKET RESTRAINTS

High Upfront Cost and Reimbursement Dependence are Estimated to Hamper Market Growth

Electroceutical devices can be expensive as they involve devices, procedures, and follow-up care. Many hospitals need clear reimbursement support to adopt new systems widely. Cost concerns are stronger in smaller hospitals and emerging markets, where budgets are tighter. Even when devices show strong clinical value, purchasing decisions may be delayed if payers do not cover the full cost.

MARKET OPPORTUNITIES

Rising Demand for Pain and Nerve-related Therapies to Offer Favorable Market Growth Opportunities

The increasing benefits of electroceuticals for pain therapies are offering a favorable opportunity for the global electroceuticals market growth. Many patients live with long-term pain and nerve problems that do not improve fully with medicines alone. Back pain, nerve pain, and pain after surgery are becoming more common, especially as people live longer and lifestyles become more stressful. In addition, electroceutical devices offer a practical solution by using gentle electrical signals to control pain signals in the body. These therapies can work continuously and can be adjusted based on patient response.

- For instance, in October 2025, Boston Scientific Corporation announced the acquisition of Nalu Medical, Inc. to consolidate its position in the pain therapies market.

MARKET CHALLENGES

Pricing Pressure is Likely to Pose a Critical Challenge to Market Growth

Electroceutical devices must work reliably for years, and hospitals expect strong safety records and service support. Any device issue can affect trust and slow adoption. Also, these therapies often need long clinical follow-up, which makes product rollouts slower than many consumer or short-cycle healthcare products. Hospitals also require trained staff for implantation and follow-ups.

Segmentation Analysis

By Device

Wide Utilization of Cardiac Rhythm Management (CRM) Devices Due to Superior Benefits to Drive Segment Growth

In terms of device, the market is categorized into cardiac rhythm management (CRM) devices, neuromodulation devices, cochlear & auditory implants, retinal & vision implants, and others.

The cardiac rhythm management (CRM) devices segment is anticipated to account for the largest electroceutical market share. Hospitals regularly treat patients with slow or irregular heartbeats, and pacemakers/defibrillators are standard tools in cardiology care. Moreover, many CRM devices also create repeat demand through upgrades and replacements over time. Innovation keeps this segment strong. In addition, an increasing number of product launches coupled with technological advancements is also projected to leverage segment growth during the forecast period.

- For instance, in September 2023, Abbott received FDA approval for its world’s first dual-chamber leadless pacemaker system.

The retinal & vision implants devices segment is anticipated to rise with a CAGR of 7.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Modality

High Volume of Implantable Devices to Accelerate Segment Growth

By modality, the market is bifurcated into implantable and non-implantable.

In 2025, the implantable segment dominated the global market. The market growth is attributed to the substantial volume of implantable devices across the globe. Implantable electroceuticals provide continuous therapy without relying on daily patient action. In addition, hospitals prefer implantable options for serious conditions as these devices can work 24/7 and are monitored over time.

- For instance, in October 2023, Medtronic received FDA approval for its extravascular defibrillator for the treatment of sudden cardiac arrest and abnormal heart rhythms.

The non-implantable segment is anticipated to rise with a CAGR of 8.4% over the forecast period.

By Application

Rising Prevalence of Cardiac Conditions Accelerated Cardiology Segment Growth

Based on application, the market is segmented into cardiology, neurology, pain management, otolaryngology, and others.

In 2025, the cardiology segment dominated the global market, attributed to the substantial prevalence of chronic cardiac conditions across the globe. Pacemakers and related systems are commonly used in hospitals, and cardiology departments have established clinical workflows for such devices. In addition, demand is steady as heart rhythm care is long-term and often requires device follow-up.

The pain management segment is anticipated to rise with a CAGR of 8.2% over the forecast period.

By End-User

Higher Patient Visits in Hospitals Boosted Segment Growth

Based on end-user, the market is segmented into hospitals, specialty clinics, homecare settings, and others.

In 2025, hospitals held the highest electroceuticals market share. Hospitals lead as many electroceutical therapies involve procedures, device programming, and ongoing monitoring—services typically delivered in hospital settings. Hospitals also manage complications and long-term follow-up, making them the main buyers and users. Large hospitals treat higher volumes of cardiac and chronic pain patients, increasing device demand. Furthermore, the segment is set to hold a 61.1% share in 2026.

In addition, the homecare settings segment is projected to grow at a CAGR of 8.4% during the study period.

Electroceuticals Market Regional Outlook

By geography, the market is segmented into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Electroceuticals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America emerged as the clear market leader, commanding a valuation of USD 22.40 billion in 2024 and expanding further to USD 23.80 billion in 2025. This sustained dominance is driven by the region’s strong focus on advanced cardiac implants, the rapid adoption of minimally invasive surgical procedures, and the rising prevalence of cardiovascular disorders.

U.S. Electroceuticals Market

As the cornerstone of North America’s performance, the U.S. continues to lead regional growth. The U.S. market is analytically estimated to reach approximately USD 8.89 billion by 2026, representing nearly 35.1% of global electroceuticals revenue.

Europe

Europe is expected to follow a steady growth trajectory, registering a CAGR of 6.6% in the coming years, and reaching a market size of USD 3.41 billion by 2026. Increased investments in product innovation and a growing burden of cardiac conditions are key factors accelerating market expansion in the region.

U.K. Electroceuticals Market

The U.K. market in 2026 is expected to reach USD 7.09 billion, representing roughly 4.7% of global market revenues.

Germany Electroceuticals Market

The market in Germany is expected to reach USD 1.64 billion in 2026, equivalent to around 6.5% of global market sales.

Asia Pacific

Asia Pacific is projected to touch USD 5.50 billion by 2026, cementing its position as the third-largest regional market. Rapid upgrades in healthcare infrastructure, along with supportive reimbursement frameworks, are expected to act as key growth catalysts across the region.

Japan Electroceuticals Market

The Japan market is anticipated to reach nearly USD 0.97 billion in 2026, contributing about 3.8% of global revenues.

China Electroceuticals Market

China is poised to be among the world’s largest markets, with projected revenues of nearly USD 1.84 billion, translating to about 7.3% of global sales.

India Electroceuticals Market

The India market in 2026 is estimated at around USD 1.24 billion, accounting for roughly 4.9% of global market revenues.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are anticipated to post moderate growth rates. The Latin American market is expected to reach USD 1.61 billion by 2026, while the GCC in the Middle East & Africa is expected to achieve a valuation of USD 0.29 billion.

South Africa Electroceuticals Market

The South Africa market is projected to reach around USD 0.12 billion in 2026, representing roughly 0.48% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Companies Focus on Technological Advancements and Strategic Collaborations to Fuel Market Revenue

The global electroceuticals market exhibits a semi-consolidated landscape, dominated by key industry leaders such as Medtronic plc, Abbott, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, and MicroPort Scientific Corporation. These companies command a substantial share of the market through aggressive strategic initiatives, including large-scale investments, continuous innovation, and timely regulatory approvals.

- For instance, in January 2026, Abbott entered into a strategic collaboration with AtaCor Medical in order to accelerate technological development for extravascular ICD technology.

Cochlear Limited, Sonova Holding AG, LivaNova PLC, and Nevro Corp are other prominent players in the market. They are focusing on partnerships and alliances, positioning themselves to strengthen their global footprint over the projected period.

LIST OF KEY ELECTROCEUTICAL COMPANIES PROFILED

- Medtronic plc (Ireland)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- BIOTRONIK SE & Co. KG (Germany)

- MicroPort Scientific Corporation (China)

- Cochlear Limited (Australia)

- Sonova Holding AG (Switzerland)

- LivaNova PLC (U.K.)

- Nevro Corp. (U.S.)

- Inspire Medical Systems, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Medtronic plc received FDA approval for its SelectSecure Model 3830 pacing lead for the treatment of ventricular tachyarrhythmias, ventricular fibrillation.

- April 2024: Medtronic plc received FDA approval for its Inceptiv spinal cord stimulator.

- April 2024: electroCore, Inc. announced the launch of its Truvaga Plus, which is designed for general wellness.

- February 2024: Boston Scientific Corporation received FDA approval for its spinal cord stimulation system for non-surgical back pain.

- October 2022: Nevro Corp received FDA approval for its HFX iQ spinal cord stimulation system. The new system has been launched for the treatment of chronic pain.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.1% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Device, Modality, Application, End-User, and Region |

|

By Device |

|

|

By Modality |

|

|

By Application |

|

|

By End-User |

|

|

By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 23.80 billion in 2025 and is projected to reach USD 43.78 billion by 2034.

In 2025, the market value stood at USD 9.75 billion.

The market is expected to exhibit a CAGR of 7.1% during the forecast period of 2026-2034.

By device, the cardiac rhythm management (CRM) devices segment is expected to lead the market.

Rising emphasis on minimally invasive surgical procedures, coupled with the rising prevalence of cardiac conditions, is driving market expansion.

Medtronic plc, Abbott, Boston Scientific Corporation, BIOTRONIK SE & Co. KG, and MicroPort Scientific Corporation are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us