Electroencephalography (EEG) Devices Market Size, Share & Industry Analysis, By Product Type (EEG Systems and EEG Accessories & Consumables), By Application (Epilepsy Diagnosis & Monitoring, Sleep Disorder Diagnosis, Critical Care & Emergency Monitoring, Intraoperative Monitoring, and Others), By End-user (Hospitals & Clinics, Diagnostic Centers & EEG Labs, Academic & Research Institutes, and Others), and Regional Forecast, 2026-2034

Electroencephalography (EEG) Devices Market Size and Future Outlook

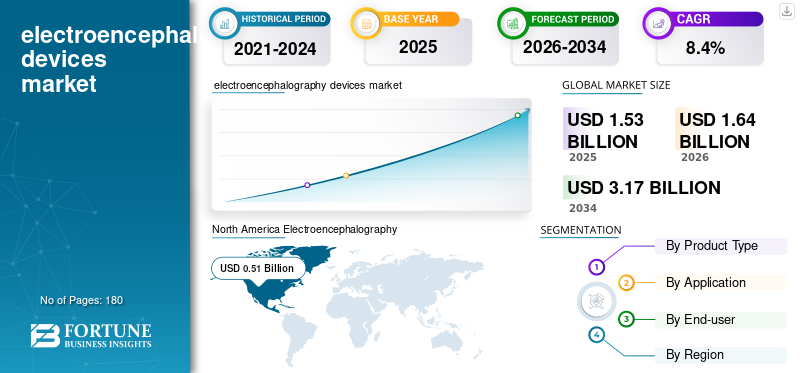

The global electroencephalography (EEG) devices market size was valued at USD 1.53 billion in 2025. The market is projected to grow from USD 1.64 billion in 2026 to USD 3.17 billion by 2034, exhibiting a CAGR of 8.4% during the forecast period. North America dominated the electroencephalography (EEG) devices market with a market share of 33.33% in 2025.

Electroencephalography (EEG) devices are non-invasive diagnostic systems used to record the electrical activity of the brain, primarily for detecting neurological disorders such as epilepsy, brain tumors, sleep disorders, and encephalopathies. The market is witnessing significant growth due to the increasing prevalence of neurological disorders, increasing awareness regarding early diagnosis, and advancements in portable and wearable EEG technologies.

Natus Medical, Inc., Nihon Kohden Corporation, and Compumedics Limited held the highest market share in 2025 due to their strong global distribution and new product launches.

Download Free sample to learn more about this report.

Electroencephalography Devices Market Key Takeaways

- 2025 Market Size: USD 1.53 Billion

- 2026 Market Size: USD 1.64 Billion

- 2034 Forecast Market Size: USD 3.17 Billion

- CAGR: 8.40% from 2026–2034

- North America dominated the electroencephalography (EEG) devices market with a 33.33% share in 2025.

- The epilepsy diagnosis & monitoring segment is projected to hold a 41.40% share in 2026.

- The EEG systems segment is projected to grow at a CAGR of 7.50% during the forecast period.

Asia Pacific

Asia Pacific is projected to reach USD 0.43 billion in 2026.

North America

North America generated USD 0.51 billion in 2025.

Europe

Europe is projected to reach USD 0.45 billion in 2026, growing at a 7.80% CAGR.

U.S.

The electroencephalography (EEG) devices market is projected to reach USD 0.47 billion in 2026.

Japan

The electroencephalography (EEG) devices market is projected to reach USD 0.12 billion in 2026.

Read More

ELECTROENCEPHALOGRAPHY (EEG) DEVICES MARKET TRENDS

Integration of AI and Cloud-Based EEG Analytics to Emerge as a Key Trend

Currently, there has been an increase in the integration of artificial intelligence (AI) and cloud-based platforms in electroencephalography (EEG) devices. These systems enhance diagnostic accuracy by automating seizure detection and reducing interpretation time. As a result, prominent companies are pursuing strategic initiatives, such as acquisitions and partnerships, to build expertise in EEG systems.

- For instance, in November 2024, Nihon Kohden Corporation acquired a 71.4% stake in NeuroAdvanced Corp., parent of Ad-Tech Medical, to enhance epilepsy diagnostics by integrating its EEG systems with Ad-Tech's specialized intracranial electrodes.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Incidence of Neurological Disorders to Fuel Market Expansion

Over the past few years, there have been an increasing number of cases of epilepsy, Alzheimer’s disease, and sleep disorders, and EEG remains a gold standard for diagnosis and monitoring of such diseases, supporting its widespread adoption. Additionally, the growing population of aged individuals, who are more prone to neurological conditions, is further expected to accelerate the demand for EEG diagnostics in both hospital and outpatient settings. This is anticipated to drive the global electroencephalography (EEG) devices market growth.

- For instance, in February 2024, the World Health Organization (WHO) mentioned that an estimated 5.0 million people are diagnosed with epilepsy each year.

MARKET RESTRAINTS

High Cost and Skilled Workforce Requirement to Restrict Market Growth

Despite technological advancements, sophisticated EEG devices with AI integration and high-channel capabilities involve significant capital investment, which is expected to limit adoption in smaller healthcare facilities. Additionally, interpreting EEG data requires specialized neurologists, and the shortage in emerging countries is expected to hinder market expansion.

- For instance, according to LabXNew data from March 2026, EEG and EMG systems typically cost between USD 20,000 and USD 150,000, varying by factors such as channel count, complexity, and extras such as software compatibility or portability.

MARKET OPPORTUNITIES

Growth of Portable and Wearable EEG Devices to Create Significant Growth Opportunities

In recent years, the emergence of portable and wearable EEG devices has enabled continuous monitoring outside traditional clinical settings, supporting telemedicine and home-based care models. Also, the shift toward remote patient monitoring and increasing demand for point-of-care diagnostics are encouraging manufacturers and researchers to develop compact, user-friendly EEG systems.

- For instance, according to the article published by Springer Nature Limited in May 2022, a group of researchers at Sungkyunkwan University created a wireless, earbud-style EEG device. It integrates tattoo-like electrodes and connectors for continuous, high-quality EEG signal recording.

MARKET CHALLENGES

Data Complexity and Standardization Issues to Challenge Market Expansion

EEG data is complex and requires standardized protocols for accurate interpretation, which is expected to pose a significant challenge. Variability in electrode placement and lack of uniform data formats impact diagnostic consistency. Moreover, managing large volumes of EEG data requires a robust IT infrastructure, which several healthcare facilities often lack. This is also expected to challenge the market expansion in the coming years.

Segmentation Analysis

By Product Type

Advances in Wireless and Home-Use EEG Systems Boosted Demand for EEG Accessories & Consumables

Based on product type, the market is segmented into EEG systems and EEG accessories & consumables.

The EEG accessories & consumables systems segment accounted for the largest global electroencephalography (EEG) devices market share in 2025. The segment’s growth is attributed to advances in wireless and home-use EEG systems, which are expected to increase demand for accessories to enhance convenience and hygiene.

The EEG systems segment is projected to grow at a 7.5% CAGR during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Growing Prevalence of Epilepsy Fueled Epilepsy Diagnosis & Monitoring Segment Growth

By application, the market is classified into epilepsy diagnosis & monitoring, sleep disorder diagnosis, critical care & emergency monitoring, intraoperative monitoring, and others.

The epilepsy diagnosis & monitoring segment accounted for the largest market share in 2025. The growth is attributed to the growing prevalence of epilepsy, the EEG’s critical role in detecting abnormal brain activity associated with seizures. Moreover, the segment is projected to hold a 41.4% share in 2026.

- For instance, according to the data from the World Health Organization (WHO) in February 2024, around 50.0 million individuals were living with epilepsy globally.

The sleep disorder diagnosis segment is expected to grow at a CAGR of 7.8% during the forecast period.

By End-user

Increasing Launches of Neurology Departments by Hospitals & Clinics Propelled Segment Growth

On the basis of end-user, the market is segmented into hospitals & clinics, diagnostic centers & EEG labs, academic & research institutes, and others.

In 2025, hospitals & clinics dominated the market. The growth is attributed to the rising number of neurology hospitals, which require effective brain-monitoring solutions such as EEG devices. In response, major players are likely to increase the supply of advanced products to boost penetration in these facilities. This is expected to fuel the segment’s growth. Furthermore, the segment is set to hold 65.0% share in 2026.

- For instance, in June 2025, KEM Hospital launched its Comprehensive Department of Neurosciences as a centralized hub for neurological, mental health, and neurosurgical care.

The diagnostic centers & EEG labs segment is projected to grow at a CAGR of 9.2% during the forecast period.

Electroencephalography (EEG) Devices Market Regional Outlook

Based on geography, the market is divided into Europe, Asia Pacific, Latin America, North America, and the Middle East & Africa.

North America

North America Electroencephalography (EEG) Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.48 billion, and touched USD 0.51 billion by 2025. Rising healthcare spending is fueling growth by driving the adoption of advanced diagnostics, such as EEG devices. Moreover, favorable reimbursement policies for non-invasive monitoring in epilepsy and brain injury are expected to accelerate EEG utilization in the region further.

- For instance, Medicare in the U.S. covers ambulatory EEG via CPT codes 95812, 95813, 95816, 95819, or 95822, supporting reimbursement for monitoring neurological disorders.

U.S. Electroencephalography (EEG) Devices Market

In 2026, the U.S. is expected to attain a valuation of USD 0.47 billion, representing roughly 28.6% of the global market share.

Europe

Europe is predicted to rise at a CAGR of 7.8% in the coming years, ranking as the third-fastest growing region. The market size is projected to reach USD 0.45 billion in 2026, driven by increased research activities, demographic aging, and supportive regulatory policies.

U.K. Electroencephalography (EEG) Devices Market

The U.K. market is anticipated to reach USD 0.08 billion in 2026, holding an estimated 5.1% of global revenues.

Germany Electroencephalography (EEG) Devices Market

The Germany market is set to reach a valuation of USD 0.09 billion in 2026, accounting for approximately 5.6% of global revenue.

Asia Pacific

In 2026, the Asia Pacific market is expected to attain a valuation of USD 0.43 billion, making it the second-largest market across the globe. The growth is driven by improving healthcare infrastructure, rising awareness of neurological conditions, and increasing investments in countries such as China, India, and Japan in neurology research, which support the adoption of EEG devices.

Japan Electroencephalography (EEG) Devices Market

Japan is anticipated to reach USD 0.12 billion in 2026, representing nearly 7.1% of the global market.

China Electroencephalography (EEG) Devices Market

The Chinese market is expected to attain a valuation of USD 0.14 billion in 2026, accounting for nearly 8.7% of global revenues.

India Electroencephalography (EEG) Devices Market

The market in India is expected to reach approximately USD 0.08 billion in 2026, accounting for around 4.9% of global market revenue.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are expected to register moderate growth. The Latin America market is projected to reach around USD 0.34 billion in 2026. The growth of these regions is supported by greater access to diagnostic care facilities and by key players entering these regions to meet the growing demand.

GCC Electroencephalography (EEG) Devices Market

In 2026, the GCC market is estimated to reach approximately USD 0.05 billion, representing around 2.8% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Distribution Network and Extensive Product Portfolio to Improve Market Positions of Prominent Players

In 2025, Natus Medical, Inc., Nihon Kohden Corporation, and Compumedics Limited held the largest market share. This share is attributed to their strong distribution network, widespread product portfolio, and integration with hospital IT systems. Moreover, other major players are advancing AI-based diagnostics, cloud connectivity, and wearable technologies. Also, they are focusing on FDA approvals and collaborations with healthcare providers, which are expected to enhance their market share.

LIST OF KEY ELECTROENCEPHALOGRAPHY (EEG) DEVICE COMPANIES PROFILED

- Natus Medical, Inc. (U.S.)

- Medtronic (Ireland)

- Nihon Kohden Corporation (Japan)

- Brain Products GmbH (Germany)

- Neurosoft (Russia)

- Compumedics Limited (Australia)

- Mitsar Co., LTD. (Russia)

- Micromed (Italy)

- Cadwell Laboratories, Inc. (U.S.)

- ANT Neuro (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Ceribell, Inc. received FDA 510(k) clearance for its Clarity algorithm to detect electrographic seizures in patients from preterm neonates to adults, making the Ceribell System the first AI-powered point-of-care EEG solution cleared for all age groups.

- September 2025: Natus Medical, Inc. acquired a minority stake in Holberg EEG, thereby achieving full ownership of the Norwegian AI pioneer.

- May 2025: Natus Medical, Inc. introduced BrainWatch, a point-of-care EEG solution designed for use in emergency rooms and ICUs.

- May 2025: Emotiv launched the MW20 EEG Active Noise-Cancelling Earphones at CES 2025, integrating dual-channel EEG sensors, AI-driven cognitive tracking, and BCI capabilities into premium machined-aluminum earphones with Qualcomm chipset audio.

- October 2024: Natus Medical, Inc. launched autoSCORE AI, an innovative tool for efficient and consistent clinical EEG analysis.

- April 2024: Soterix Medical Inc. launched MxN-GO EEG, a research-oriented system combining high-definition transcranial electrical stimulation (HD-tES) with electroencephalography (EEG) for applications involving electrical stimulation.

- April 2023: Cadwell Industries Inc. launched Arc Voyager, a wireless remote monitoring system for in-home EEG with synchronized HD video.

REPORT COVERAGE

The report provides a comprehensive analysis of all market segments, highlighting key drivers, emerging trends, growth opportunities, major restraints, and challenges shaping the market landscape. It further examines technological innovations, prevalence of key diseases, recent product launches, notable industry developments, market share insights, and detailed profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.4% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Application, End-user, and Region |

| By Product Type |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 1.53 billion in 2025 and is projected to reach USD 3.17 billion by 2034.

In 2025, the market value in North America stood at USD 0.51 billion.

The market is expected to exhibit a CAGR of 8.4% during the forecast period of 2026-2034.

The EEG accessories & consumables segment led the market by product type.

The key factor driving the market is the rising incidence of neurological disorders globally.

Natus Medical, Inc., Nihon Kohden Corporation, and Compumedics Limited are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us