Embolic Protection Devices Market Size, Share & Industry Analysis, By Device Type (Distal Filter Devices, Distal Occlusion Devices, and Proximal Occlusion Devices), By Procedure (Percutaneous Coronary Intervention, Carotid Artery Stenting, Peripheral Vascular Interventions, and Others), By End-user (Hospitals & ASCs and Standalone Cath Labs), and Regional Forecast, 2026-2034

Embolic Protection Devices Market Size and Future Outlook

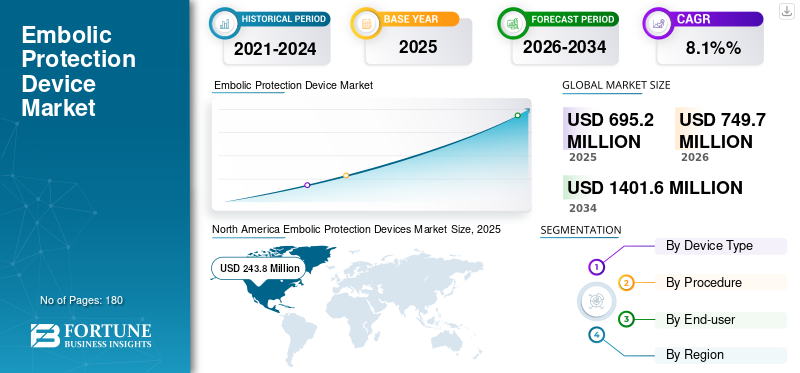

The global embolic protection devices market size was valued at USD 695.2 million in 2025. The market is projected to grow from USD 749.7 million in 2026 to USD 1,401.6 million by 2034, exhibiting a CAGR of 8.1% during the forecast period. North America dominated the global embolic protection devices market with a market share of 35.07% in 2025.

Embolic protection devices (EPDs) are specialized catheters designed to capture or remove debris, such as blood clots or plaque fragments, during vascular procedures such as angioplasty or stenting. The market growth is attributed the increasing chronic conditions such as coronary artery disease, and valvular heart diseases, which is driving the need for minimally invasive procedures, involving the use of embolic protection devices.

The market is dominated by major players, including Medtronic, Boston Scientific Corporation, and others. These players have a strong brand reputation globally, with a diversified portfolio of embolic protection devices.

Download Free sample to learn more about this report.

EMBOLIC PROTECTION DEVICES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 695.2 million

- 2026 Market Size: USD 749.7 million

- 2034 Forecast Market Size: USD 1,401.6 million

- CAGR: 8.1% from 2026–2034

- North America dominated the embolic protection devices market with a 35.07% share in 2025.

- The distal filter devices segment accounted for the largest market share in 2025

- Carotid artery stenting segment and is expected to hold a 43.6% share in 2026.

North America

North America maintained its leading position, reaching USD 243.8 million in 2025.

Europe

Europe is projected to grow at a notable pace, recording an 8.1% CAGR during the forecast period and reaching USD 220.8 million by 2026.

Asia Pacific

Asia Pacific is expected to reach USD 178.6 million by 2026.

U.S.

The market is projected to reach USD 242.3 million by 2026.

Japan

Japan market growth driven by aging population and cardiovascular care.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Increasing Number of Key Procedures to Drive Market Growth

Over the past few years, there has been a significant rise in key procedures such as percutaneous coronary intervention, peripheral vascular intervention, and more, due to increasing vascular complications globally.

- For instance, according to data from the Centers for Disease Control & Prevention (CDC) in September 2022, more than 6.0 million percutaneous coronary interventions (PCIs) are performed annually at over 1,600 healthcare facilities in the U.S.

Some of these procedures require embolic protection devices, which is increasing their demand in hospitals and ASCs. Furthermore, this trend is influencing key players to increase the supply of these devices, which is expected to drive the global embolic protection devices market growth.

MARKET RESTRAINTS:

Limited Reimbursement in Certain Countries to Restrict Market Expansion

In several countries, embolic protection devices (EPDs) are not widely utilized for percutaneous coronary intervention (PCI) or peripheral vascular procedures due to limited or inconsistent reimbursement scenarios.

As a result, hospitals, ambulatory surgery centers (ASCs), and cardiac catheterization labs, especially in emerging countries, are often required to absorb the full device cost. This is expected to result in lower utilization despite proven clinical benefits, thereby hindering market growth.

MARKET OPPORTUNITIES:

Growth in Cath Labs to Offer Lucrative Growth Opportunities

In recent years, there has been an increase in cardiac catherization labs globally, which has led to a substantial rise in peripheral vascular procedures. These standalone labs often drive higher throughput due to shorter waiting times, flexible scheduling, and rapid adoption of minimally invasive interventions.

- For instance, in February 2024, Koninklijke Philips N.V. announced the installation of more than 1,500 cath labs in the Indian subcontinent.

This expansion in cath labs is expected to drive the demand for safety devices, including embolic protection devices (EPDs), which are anticipated to offer a lucrative opportunity for key players in the upcoming years.

EMBOLIC PROTECTION DEVICES MARKET TRENDS:

Increasing Use of Embolic Protection in Coronary Bypass Graft (SVG) Interventions to Emerge as a Key Market Trend

Currently, there is an increasing use of EPDs in saphenous vein graft (SVG) interventions due to improved outcomes associated with their utilization. Additionally, a high volume of coronary bypass surgeries performed globally, which carries a higher embolic risk and further supports the utilization of EPDs.

- For instance, according to data from ScienceDirect in July 2022, more than 600,000 coronary artery bypass (CABG) procedures are performed annually worldwide.

Furthermore, this trend is supported by guideline recommendations for safety devices and increasing awareness among interventional cardiologists.

Download Free sample to learn more about this report.

MARKET CHALLENGES:

Limited Awareness and Skilled Personnel to Challenge Market Growth

In emerging and low-income markets, there is a lack of awareness about embolic protection devices due to limited access to care. Additionally, there are insufficiently trained healthcare professionals, which is reducing adoption rates and procedural success.

- For instance, according to data from the World Journal of Surgery in July 2024, the College of Surgeons of East, Central, and Southern Africa (COSECSA) region faces a severe shortage, approximately one cardiothoracic surgeon for every five million people.

Moreover, the limited availability of skilled professionals is leading to delayed procedures, such as peripheral vascular intervention and percutaneous coronary intervention, thereby restricting the use of EPDs and challenging market growth.

Segmentation Analysis

By Device Type

Significant Advantages of Distal Filter Devices to Drive Segmental Growth

Based on device type, the market is classified into distal filter devices, distal occlusion devices, and proximal occlusion devices.

To know how our report can help streamline your business, Speak to Analyst

The distal filter devices segment accounted for the largest global embolic protection devices market share in 2025. The growth is primarily due to the combination of clinical, technical, and operational advantages of distal filter devices, which make them the preferred choice among interventional cardiologists.

The distal occlusion devices segment is projected to grow at a CAGR of 8.4% during the forecast period.

By Procedure

Increasing Procedure Volume Propelled the Carotid Artery Stenting Segment’s Growth

Based on procedure, the market is segmented into percutaneous coronary intervention, carotid artery stenting, peripheral vascular interventions, and others.

The carotid artery stenting segment accounted for the largest share in 2025. The segment’s growth is attributed to an increasing number of related procedures, such as carotid revascularization procedures, which are driving the adoption of embolic protection devices. Furthermore, the segment is expected to hold a 43.6% share in 2026.

- For instance, a study published in the Journal of the American Medical Association in September 2022 found that there was an annual increase of 13.0% in the number of carotid revascularization procedures from 2015 to 2019.

The peripheral vascular interventions segment is projected to grow at a CAGR of 8.3% during the forecast period.

By End-user

Increasing Number of Percutaneous Coronary Intervention Procedures Performed Boosted the Hospitals Segment Growth

Based on end-user, the market is segmented into hospitals & ASCs and standalone cath labs.

In 2025, the global market was dominated by hospitals & ASCs. The growth is attributed to a higher volume of percutaneous coronary intervention procedures in the ambulatory surgery centers (ASCs), which is expected to increase the utilization of EPDs. Furthermore, the segment is set to hold 82.3% share in 2026.

- For instance, according to data published by TCTMD in May 2025, a study at the Society for Cardiovascular Angiography and Interventions (SCAI) reported that from 2018 to 2022, the rate of PCI procedures performed in ASCs increased from 0.01 to 0.87 cases per 10,000 person-years.

The standalone cath labs segment is projected to grow at a CAGR of 8.3% during the forecast period.

Embolic Protection Devices Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America Embolic Protection Devices Market Size, 2025 (USD million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 225.4 million, and also maintained its lead in 2025, with USD 243.8 million. The growth is attributed to the increasing number of ASCs in the U.S., which supports the growing volume of cardiac catheterization procedures, thereby increasing the utilization of embolic protection devices. In 2026, the U.S. market is estimated to reach USD 242.3 million.

- For instance, according to the data from the Centers for Medicare & Medicaid Services (CMS) in March 2025, there are over 6,500 Medicare-certified ASCs in the S.

Europe is projected to expand at a notable rate in the forthcoming years. During the forecast period, the region is projected to record a growth rate of 8.1%, the second-highest among all regions, and reach a valuation of USD 220.8 billion by 2026. This growth is attributed to the significant presence of key market players. Due to such factors, countries including the U.K. are anticipated to record the valuation of USD 36.6 million, Germany to record USD 61.2 million, and France to record USD 30.7 million in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 178.6 million in 2026 and secure the position of the third-largest region in the market. Within the region, India and China are both estimated to reach USD 29.9 million and USD 45.0 million, respectively, in 2026.

The Latin America and Middle East & Africa regions are expected to showcase moderate growth in the market over the forecast period,. The Latin America market in 2026 is set to reach a valuation of USD 55.8 million. The growth is attributed to increasing awareness of embolic risk in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 24.6 million by 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Key Players Focus on Product Commercialization to Extend their Marketing Reach

In 2025, Medtronic, Boston Scientific Corporation, and Abbott accounted for the largest global embolic protection devices market share. The share is attributed to the increasing focus of key players on product commercialization globally.

Other prominent companies, including Cardinal Health, Transverse Medical Inc., and W. L. Gore & Associates, Inc., are involved in key collaborations, partnerships, and acquisitions, which are expected to help these companies gain substantial market share.

LIST OF KEY EMBOLIC PROTECTION DEVICES MARKET COMPANIES PROFILED:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Edwards Lifesciences Corporation (U.S.)

- Abbott (U.S.)

- Cardinal Health (U.S.)

- Transverse Medical Inc. (U.S.)

- L. Gore & Associates, Inc. (U.S.)

- Contego Medical, Inc. (U.S.)

- Cordis (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Medtronic launched full distribution of the Neuroguard IEP System, featuring a unique 3-in-1 design that combines a stent, post-dilation balloon, and embolic filter to improve the treatment of carotid artery disease.

- October 2025: AorticLab announced that the FDA approved the investigational device exemption (IDE) for AorticLab's FLOWer system, a full-body embolic protection device used during transcatheter intracardiac procedures.

- April 2025: Transverse Medical Inc. completed its Series B2 financing round, raising over USD 10.0 million to support the clinical validation and development of its Point-Guard cerebral embolic protection (CEP) device aimed at preventing stroke during transcatheter procedures such as TAVR.

- May 2025: Terumo Corporation launched the Roadsaver carotid stent system, which provides a significant opportunity for embolic protection devices in carotid artery stenting procedures.

- February 2025: InspireMD commenced the CGUARDIANS II pivotal clinical trial to evaluate the safety and efficacy of their CGuard Prime 80 cm carotid stent system in transcarotid artery revascularization (TCAR) procedures, which involve the usage of embolic protection devices.

REPORT COVERAGE

The global embolic protection devices market covers an in-depth analysis of all segments included in the report. It covers the key drivers, trends, opportunities, challenges, and restraints for the market. Additionally, it includes key insights such as the number of key procedures, prevalence of key conditions, new product launches, key industry developments, and technological advances. Moreover, the report covers market share analysis and profiles of key companies operating in the market.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.1% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Device Type, Procedure, End-user, and Region |

|

By Device Type |

|

|

By Procedure |

|

|

By End-user |

|

|

By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 695.2 million in 2025 and is projected to reach USD 1,401.6 million by 2034.

In 2025, the market value stood at USD 243.8 million.

The market is expected to exhibit a CAGR of 8.1% during the forecast period (2026-2034).

The distal filter devices segment led the market by device type.

The key factors driving the market are the increasing number of key procedures worldwide.

Medtronic, Boston Scientific Corporation, and Abbott are some of the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us