Energy Efficient Glass Market Size, Share & Industry Analysis, By Coating Type (Soft Coat and Hard Coat), By Glazing (Single Glazing, Double Glazing, and Triple Glazing), By End-use Industry (Building & Construction, Automotive, Solar Panels, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

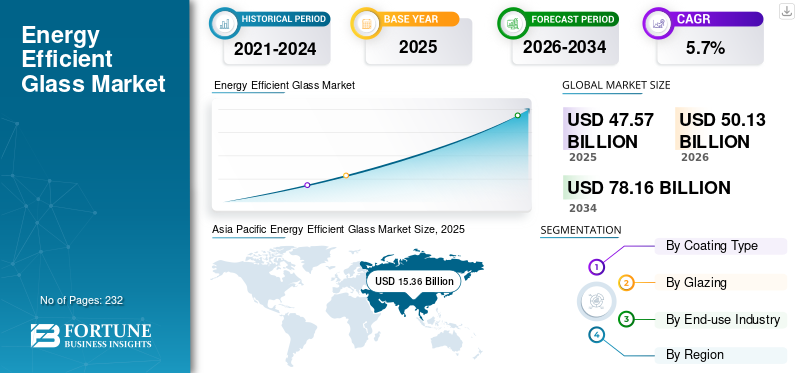

The global energy efficient glass market size was valued at USD 47.57 billion in 2025. The market is projected to grow from USD 50.13 billion in 2026 to USD 78.16 billion by 2034, exhibiting a CAGR of 5.7% during the forecast period. Asia Pacific dominated the global market with a market share of 32.29% in 2025.

Energy-efficient glass refers to advanced glazing solutions, such as low-emissivity (low-E) coated glass, double- or triple-pane assemblies with inert gas fills, and solar-control tints, designed to minimize heat transfer, block unwanted infrared radiation, and optimize visible light transmission. These technologies reduce energy consumption for heating, cooling, and lighting in buildings and vehicles by improving thermal insulation and solar heat gain coefficients, helping structures comply with global energy codes such as IECC or EU EPBD while enhancing occupant comfort. The market growth is fueled by stringent green building regulations (e.g., LEED, BREEAM), rising energy costs, urbanization in Asia Pacific, and innovations such as dynamic smart glass. Key drivers include policy incentives for net-zero buildings, retrofit demands in aging infrastructure, and construction booms in commercial/residential sectors are likely to propel market growth over the study period. Saint-Gobain Glass, AGC Inc., Guardian Glass, NSG Group, Vitro Architectural Glass, and Xinyi Glass Holdings Ltd. are the key players operating in the market.

Download Free sample to learn more about this report.

ENERGY EFFICIENT GLASS MARKET TRENDS

Rapid Shift toward High-Performance and Smart Glazing to Propel Market Growth

The market is witnessing a clear shift from basic low-E coatings toward higher-performance, multifunctional glazing solutions. The demand is increasingly moving toward double and triple glazing with advanced low-E and solar-control coatings that simultaneously improve thermal insulation, manage solar heat gain, reduce glare, and enhance occupant comfort. In commercial buildings, especially high-rise offices and institutional structures, façade designs are becoming more glass-intensive, making performance-optimized glazing a standard specification rather than a premium add-on.

Alongside this, smart and dynamic glass technologies such as electro chromic and thermo chromic glazing are gradually gaining traction in niche applications, including premium commercial buildings, transportation, and specialty architectural projects. While these technologies still represent a small share of total volume, they signal a broader trend toward intelligent building envelopes that respond dynamically to environmental conditions. This evolution reflects a market trend where value growth is increasingly driven by functional performance and system integration, not just glass volume.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Building Energy Regulations and Climate Policies to Boost Product Demand

One of the strongest drivers for the energy efficient glass market growth is the tightening of building energy efficiency regulations across major economies. Governments are prioritizing reductions in building-related energy consumption and carbon emissions through stricter thermal performance requirements for windows, façades, and building envelopes. Regulations and codes increasingly favor or mandate the use of low-E and insulated glazing systems, directly stimulating the demand for energy efficient glass in both new construction and renovation projects.

In addition to regulatory mandates, national and regional climate-neutrality targets are reinforcing the long-term demand visibility for high-performance glazing. Energy-efficient glass is widely recognized as one of the most cost-effective ways to reduce heating and cooling loads in buildings without compromising design flexibility. As a result, policymakers, developers, and building owners increasingly view advanced glazing as a core compliance solution, making regulation a structural, long-term growth driver rather than a short-term policy effect.

Download Free sample to learn more about this report.

MARKET RESTRAINTS

High Initial Cost Compared with Conventional Glass May Hinder Market Growth

Despite its long-term energy-saving benefits, the adoption of energy-efficient glass is constrained by its higher upfront cost relative to conventional clear or basic coated glass. Advanced low-E coatings, multi-glazing units, inert gas fills, and precision manufacturing processes increase production and installation costs. In cost-sensitive markets, especially in developing regions, this price premium can slow adoption, particularly in residential construction where buyers often prioritize initial affordability over lifecycle energy savings.

This restraint is further amplified in regions where energy prices are subsidized or relatively low, reducing the immediate economic incentive to invest in higher-performance glazing. In such markets, the payback period for energy-efficient glass can appear longer, limiting penetration beyond premium or regulatory-driven projects.

MARKET OPPORTUNITIES

Large Retrofit and Building Renovation Potential to Propel Industry Expansion

A major opportunity for the energy-efficient glass market lies in the vast global stock of existing buildings that still rely on outdated, inefficient glazing systems. In many mature markets, windows installed decades ago no longer meet current energy performance standards, creating a substantial replacement and retrofit opportunity. Since windows and glazing systems typically have long service lives, their replacement cycle aligns well with government-supported renovation programs aimed at improving building energy efficiency.

This retrofit opportunity is particularly strong in Europe and North America, where policy frameworks increasingly emphasize renovation over new construction to achieve emissions-reduction targets. Energy efficient glass plays a central role in these renovation strategies as it delivers measurable energy savings without requiring major structural changes. As renovation activity accelerates, especially in residential and public buildings, the retrofit segment is expected to become a key growth engine for the market over the medium to long term.

MARKET CHALLENGES

Manufacturing Complexity and Supply Chain Intensity May Hinder Market Growth

The market faces ongoing challenges related to manufacturing complexity and capital intensity. Producing high-performance coated glass requires advanced float glass lines, sophisticated coating technologies, and strict quality control, leading to high capital expenditure and limited flexibility. Any disruption in raw materials, energy supply, or production capacity can significantly impact output, costs, and delivery timelines.

In addition, the market is highly sensitive to energy costs, as glass manufacturing is energy-intensive. Volatility in natural gas and electricity prices can pressure margins and lead to price fluctuations, which are difficult to pass through in competitive construction markets. These structural challenges create barriers to entry for new players and make capacity expansion a carefully timed decision, potentially limiting the industry’s ability to respond quickly to sudden demand surges.

Regulatory Compliance May Create Hurdles for Market Expansion

While regulatory frameworks are a key driver for energy efficient glass adoption, compliance with complex and evolving regulations can also act as a hurdle, particularly for manufacturers and project developers. Energy performance standards, building codes, and product certification requirements vary significantly across regions and countries, covering aspects such as thermal transmittance (U-values), solar heat gain coefficients, safety glazing norms, and environmental declarations. Navigating these fragmented regulatory regimes increases compliance costs, lengthens product approval timelines, and complicates the cross-border trade of energy-efficient glass products, especially for manufacturers operating at a global scale.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Rising trade protectionism and geopolitical tensions have emerged as significant headwinds for the market by disrupting cross-border trade flows and increasing cost uncertainty. Anti-dumping duties, safeguard measures, and tariffs on flat glass and processed glass products in key regions have altered competitive dynamics, particularly affecting imports of coated and high-performance glass. Such measures are often introduced to protect domestic glass manufacturers but can raise procurement costs for downstream fabricators, façade contractors, and construction companies that rely on imported energy-efficient glass or specialty coatings not readily available locally.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

Research and development efforts in the market are increasingly focused on enhancing thermal performance while maintaining high optical clarity and durability. Manufacturers are investing in advanced Low-E and solar-control coatings that deliver lower emissivity and improved solar heat management without compromising visible light transmission. These developments aim to meet stricter building energy codes and evolving architectural requirements, particularly for large glass façades where balancing daylighting and energy efficiency is critical. Continuous improvements in coating uniformity, scratch resistance, and long-term performance are also key R&D priorities, as durability directly influences lifecycle cost and customer acceptance.

SEGMENTATION ANALYSIS

By Coating Type

Soft Coat Segment Dominated the Market Due to High Performance and Widespread Use

Based on coating type, the market is segmented into soft coat and hard coat.

The soft coat segment held the largest market share in 2025. Soft coat glass, typically produced using magnetron sputtering (vacuum deposition), offers superior thermal insulation and solar-control performance due to its multilayer metallic coating structure. This type of glass exhibits very low emissivity, making it highly effective in reducing heat loss and controlling solar heat gain. As a result, soft coat glass is widely used in double and triple glazing units for residential and commercial buildings, particularly in regions with stringent building energy regulations and higher performance requirements.

The hard coat segment registers notable growth and is set to exhibit a CAGR of 5.5% over the forecast period. It is often preferred in cost-sensitive markets and applications where moderate energy efficiency is sufficient. Together, these two coating types allow manufacturers and end users to balance performance, durability, and cost considerations, enabling energy-efficient glass adoption across a wide range of climatic conditions, building standards, and price segments.

By Glazing

Double Glazing Segment Led the Market with Increasing Demand due to Significant Reduction of Heat Transfer

Based on glazing, the market is segmented into single glazing, double glazing, and triple glazing.

Among these, the double glazing segment registered dominating energy efficient glass market share in 2025. Double glazing offers a strong balance between performance and cost. By incorporating two glass panes separated by an air or inert gas-filled cavity, double-glazed units significantly reduce heat transfer and improve indoor comfort.

The single glazing segment is expected to grow at a CAGR of 5.7% during the forecast period. Single glazing, when combined with energy-efficient coatings such as Low-E or solar-control layers, provides basic improvements in thermal performance compared with uncoated glass. This glazing type is commonly used in warm or moderate climates, retrofit applications, and cost-sensitive markets where building energy regulations are less stringent and lightweight window systems are preferred.

Triple glazing, which adds a third glass pane and an additional insulating cavity, delivers the highest level of thermal insulation and is increasingly used in cold climates and energy-efficient or near-zero-energy buildings. Although triple glazing involves higher material and installation costs, its superior energy-saving potential makes it an important solution in regions with strict building codes and ambitious carbon-reduction targets.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Segment Leads due to Widespread Adoption in Residential, Commercial, and Institutional Buildings

Based on end-use industry, the market is segmented into building & construction, automotive, solar panels, and others.

The building & construction segment represents the largest end-use segment, driven by the widespread adoption of energy-efficient glazing in residential, commercial, and institutional buildings. Low-E and solar-control glass are extensively used in windows, façades, curtain walls, and skylights to reduce heating and cooling loads while enhancing daylighting and occupant comfort. Stringent building energy codes and large-scale renovation initiatives further reinforce the dominance of this segment.

The automotive segment accounts for a significant share in product demand, as vehicle manufacturers increasingly use solar-control and low-emissivity glass to improve thermal comfort and energy efficiency. In electric and hybrid vehicles, energy-efficient glazing helps reduce air-conditioning load, thereby extending driving range. These factors are anticipated to positively impact the growth of the segment, which is expected to grow at a CAGR of 5.2% over the analysis period.

The solar panels segment relies on high-transparency and anti-reflective energy-efficient glass to maximize light transmission and overall system efficiency, supporting the rapid expansion of solar power installations.

The others segment includes applications such as appliances, transportation infrastructure, and specialty architectural uses, where energy-efficient glass is adopted to meet performance, safety, or sustainability requirements across niche markets.

ENERGY EFFICIENT GLASS MARKET REGIONAL OUTLOOK

Based on region, the market has been analyzed across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Energy Efficient Glass Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for the leading market share in 2025. The growth is underpinned by rapid urbanization, large-scale infrastructure development, and expanding construction activity in countries such as China and India. Although average selling prices are lower in some Asia Pacific markets, the increasing awareness of energy efficiency and tightening building standards are steadily boosting the demand for energy efficient glass.

To know how our report can help streamline your business, Speak to Analyst

North America

North America follows closely, driven by the strong adoption of low-E glazing in both residential and commercial construction, supported by building codes and energy-efficiency standards. The U.S. represents the largest and most influential market in North America for energy-efficient glass, driven primarily by strong demand from the residential and commercial construction sectors. The widespread adoption of low-E coated glass has become a standard practice in new residential construction and window replacement projects, supported by national and state-level building energy codes.

Europe

Europe represents one of the most mature and value-intensive markets, supported by stringent building energy regulations, ambitious climate targets, and a strong focus on renovation of existing building stock. The widespread implementation of low-E and multi-glazing systems in residential and commercial buildings has positioned Europe as a key hub for high-performance and premium energy-efficient glass products.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa represent emerging markets, where growth is driven by rising construction activity and climate-driven demand for solar-control glazing. Additional factor supporting industry expansion in these regions is the gradual strengthening of building energy codes, particularly in urban and commercial developments.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Leading Companies Emphasize Investments to Meet High Performance Requirements across End-user Industries

Major investments are underway in the energy efficient glass market as manufacturers respond to rising sustainability expectations and higher performance requirements across end-use industries. Leading producers such as Saint-Gobain Glass, AGC Inc., Guardian Glass, NSG Group, Vitro Architectural Glass, and Xinyi Glass Holdings Ltd. are directing their capital toward process optimization, product quality enhancement, and environmentally aligned manufacturing practices. Innovation efforts are increasingly centered on improving purity consistency, reducing environmental footprint, and developing grades suitable for advanced products.

LIST OF KEY ENERGY EFFICIENT GLASS COMPANIES PROFILED

- Saint-Gobain Glass (France)

- AGC Inc. (Japan)

- Guardian Glass (U.S.)

- NSG Group (Japan)

- Vitro Architectural Glass (Mexico)

- Xinyi Glass Holdings Ltd. (China)

- CSG Holding (China)

- Fuyao Glass Industry Group (China)

- Flat Glass Group Co., Ltd. (China)

- Taiwan Glass Industry Corporation (Taiwan)

KEY INDUSTRY DEVELOPMENTS

- January 2025 - Guardian Glass North America began the full-scale sales of SunGuard SNX 70+, a high-VLT and low-SHGC coated glass designed for daylight-rich façades. The product enables maximum natural light while limiting solar heat gain, helping commercial buildings reduce cooling loads and meet stricter energy-performance standards.

- October 2024 - Glaston Corporation and Corning Inc. partnered to develop ultra-thin architectural glass for triple insulating glass units (IGUs). This technology allows higher thermal efficiency without increasing glazing thickness or requiring window frame redesign, supporting the wider adoption of triple glazing in energy-efficient buildings.

- October 2024 - Xinyi Glass invested in the development of advanced low-E coating materials and glass features (incl. low-E and other value-added functionality), signaling continued pipeline/upgrade of energy-saving products.

- July 2022 - Saint-Gobain Glass commercialized low-carbon flat glass (e.g., ORAÉ / low-carbon launches) by combining high cullet, renewable electricity, and industrial trials, supporting embodied-carbon reduction alongside operational energy savings.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, coating type, glazing, and end-use industry. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion), Volume (Kiloton) |

|

Growth Rate |

CAGR of 5.7% from 2026 to 2034 |

|

Segmentation |

By Coating Type, By Glazing, By End-use Industry, By Region |

|

By Coating Type |

· Soft Coat · Hard Coat |

|

By Glazing |

· Single Glazing · Double Glazing · Triple Glazing |

|

By End-use Industry |

· Building & Construction · Automotive · Solar Panels · Others |

|

By Region |

· North America (By Coating Type, By Glazing, By End-use Industry, By Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (By Coating Type, By Glazing, By End-use Industry, By Country) o Germany (By End-use Industry) o U.K. (By End-use Industry) o France (By End-use Industry) o Italy (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (By Coating Type, By Glazing, By End-use Industry, By Country) o China (By End-use Industry) o India (By End-use Industry) o Japan (By End-use Industry) o South Korea (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Latin America (By Coating Type, By Glazing, By End-use Industry, By Country) o Mexico (By End-use Industry) o Brazil (By End-use Industry) o Rest of Latin America (By End-use Industry) · Middle East & Africa (By Coating Type, By Glazing, By End-use Industry, By Country) o GCC (By End-use Industry) o South Africa (By End-use Industry) o Rest of the Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 47.57 billion in 2025 and is projected to reach USD 78.16 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 5.7% during the forecast period of 2026-2034.

By coating type, the soft coat segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

Stringent building energy regulations and climate policies is a key factor driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 232

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us