Engine Bush Market Size, Share & Industry Analysis, By Vehicle Type (Passenger cars (Hatchback/Sedan, and SUVs), and Commercial Vehicles (LCV (Light Commercial Vehicles), Heavy Trucks, Buses & Coaches, and Others)), By Material (Rubber, Polyurethane, Brass, Aluminum, Bronze, and Others), By Sales Channel (OEM and Aftermarket), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

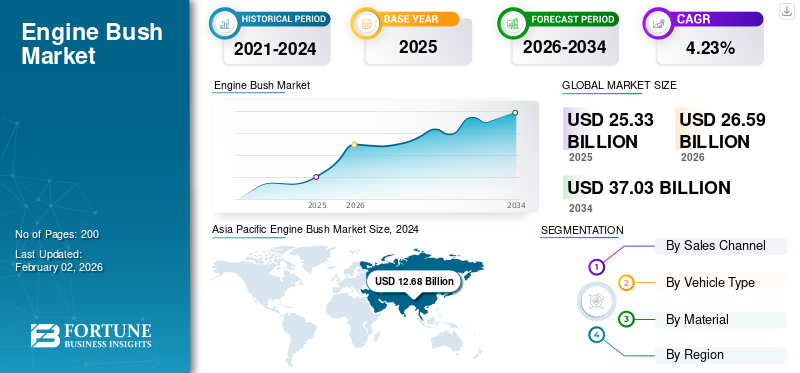

The global engine bush market size was valued at USD 25.33 billion in 2025. The market is projected to grow from USD 26.59 billion in 2026 to USD 37.03 billion by 2034, exhibiting a CAGR of 4.23% during the forecast period. Asia Pacific dominated the engine bush market with a market share of 52.90% in 2025.

Engine bushes, also known as engine mounts or bushings, are rubber or metal components that absorb vibrations, shocks, and impacts between the engine and the vehicle frame or chassis. They play a vital role in reducing noise and ensuring smoother engine operation. These bushes also help stabilize engine movement and prevent excessive wear and tear on other mechanical components. Engine bushes are made from rubber, polyurethane, or metal composites, each offering specific performance benefits regarding durability and comfort.

The global market growth is driven by increased automotive production, the need for better vehicle performance, and rising consumer demand for noise reduction in automobiles. Key players in the market include global automotive suppliers such as Federal-Mogul, NTN Corporation, and SKF. These companies are focused on developing high-performance, durable engine bush components catering to passenger and commercial vehicle segments. Manufacturers are also emphasizing product innovation to meet stringent environmental and regulatory standards. The growth in electric vehicle production further influences demand, as these vehicles require specialized engine bush designs for optimal performance.

The COVID-19 pandemic significantly impacted the market due to disruptions in automotive production and supply chains. Factory closures, labor shortages, and logistical challenges hindered engine bush manufacturing, leading to vehicle production delays. Additionally, vehicle demand fell during lockdowns, affecting the automotive industry's overall performance. As a result, the market witnessed a temporary slowdown. However, as economies reopened and demand for vehicles rebounded, the market gradually recovered, and manufacturers adapted to new consumer trends, such as an increased focus on electric vehicles.

Download Free sample to learn more about this report.

Engine Bush Market Key Takeaways

- 2025 Market Size: USD 25.33 billion

- 2026 Market Size: USD 26.59 billion

- 2034 Forecast Market Size: USD 37.03 billion

- CAGR: 4.23% from 2026–2034

- Asia Pacific dominated the engine bush market with a market share of 52.90% in 2025.

- The passenger cars segment will account for 63.22% market share in 2026.

- The Rubber segment is expected to account for 62.59% of the market in 2026.

Asia Pacific

Asia Pacific generated USD 13.4 billion in 2025 and is projected to reach USD 14.14 billion in 2026, driven by the robust expansion of the automotive sector across key countries such as China, India, and Japan.

North America

North America generated USD 5.37 billion in 2025 and is projected to reach USD 5.6 billion in 2026, supported by a mature automotive industry, increasing EV adoption, and advanced engine bush technologies.

Europe

Europe reached USD 5.04 billion in 2025 and is expected to reach USD 5.25 billion in 2026, supported by premium automotive manufacturing and continuous innovation in bushing materials and design.

U.S.

The market is projected to reach USD 3.84 billion by 2026, supported by growing demand for vehicle comfort, electric vehicles, and autonomous driving technologies.

Japan

The market is projected to reach USD 1.63 billion by 2026, driven by the country's advanced automotive manufacturing capabilities and continued focus on high-performance vehicle components.

Read More

Impact of Tariff on the Market

Tariff surges on vehicles and parts have a direct, measurable impact on the global engine bush market by raising import costs, disrupting established supplier networks, and incentivizing near-shoring. Higher duties (recent measures range from around 25% on autos/parts to ad-hoc higher rates applied to specific trading partners) increase landed costs for precision metal components like engine bushes, squeeze margins for tier-2 suppliers, and prompt OEMs to re-source locally or redesign assemblies to reduce imported content. Short-term effects include order deferrals, inventory front-loading, and lost export volumes; medium-term outcomes are supplier consolidation, localized manufacturing investment, and longer purchasing cycles as fleets and assemblers rebalance supply chains to avoid tariff exposure.

Engine Bush Market Trends

Emergence of High-Performance, Noise and Vibration-Damping Bushes is a Driving Trend in Market

The global market is experiencing steady growth, driven by several key trends shaping the automotive sector. One prominent trend is the growing demand for high-performance, noise, vibration, and harshness (NVH)-reducing components as consumers increasingly prioritize comfort in their vehicles. Engine bushes, designed to reduce vibration and improve engine stability, are crucial in enhancing NVH levels. According to the International Organization of Motor Vehicle Manufacturers (OICA), the global automotive production (CV and PC) reached 92 million units in 2024, significantly recovering after the pandemic-induced slowdown. This surge in vehicle production directly impacts the demand for engine bushes.

In addition, the rise of electric vehicles (EVs) is influencing the engine bush market trend. Although EVs do not have traditional internal combustion engines, they still require engine mounts for their electric motors and other components, which drives demand for specialized bushings. As of 2023, EV production is growing rapidly, with a reported 10.5 million EVs produced globally in 2022, a 55% increase compared to the preceding year.

Manufacturers also focus on innovation, creating more durable and lightweight engine bushes. Leading companies such as SKF, NTN Corporation, and Federal-Mogul have been actively investing in R&D to improve the performance of these components. For instance, SKF has introduced advanced engine mount technology designed to meet the rigorous demands of modern vehicles while offering greater durability and environmental sustainability. Additionally, major OEMs including Toyota, Ford, and Volkswagen are integrating these next-gen bushes into their vehicles to comply with environmental regulations and enhance vehicle performance.

In conclusion, the global market is benefiting from technological advancements, increasing vehicle production, and the rise of electric mobility, positioning it for sustained growth over the coming years.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increased Requirement of Specialized Engine Bushings with Growing Hybrid and Electric Vehicles is Driving Market Growth

A unique and significant driving factor for the global engine bush market growth is the increasing adoption of hybrid and electric vehicles (EVs), which require specialized engine bushings for their powertrains and electric motors. As the automotive industry undergoes a transformative shift toward electrification, the demand for engine bushings is evolving to meet the unique needs of these advanced powertrains. Unlike traditional internal combustion engines, hybrid and electric vehicles require highly durable, vibration-damping components to handle the specific forces and motions associated with electric motors and regenerative braking systems. This shift creates greater demand for custom-engineered engine bushes made from advanced materials such as polyurethane, carbon fiber, and high-performance elastomers.

According to the International Energy Agency (IEA), global electric vehicle sales increased by 55% in 2023, with over 10.5 million EVs sold globally, a trend expected to continue as automakers and governments push for higher electrification targets. For example, the European Union’s Green Deal mandates a ban on the sale of new internal combustion engine vehicles by 2035, significantly accelerating the adoption of electric and hybrid vehicles. As this transition unfolds, hybrid and electric vehicles require specialized components, including engine bushings, to meet the operational requirements of their powertrains, which typically have different vibration characteristics compared to traditional engines.

OEMs including Tesla, Volkswagen, and General Motors increasingly design their vehicles with advanced engine bushings to improve performance, durability, and comfort. For instance, Tesla’s Model 3 and Model Y incorporate lightweight, high-performance bushings to optimize energy efficiency and reduce wear on key drivetrain components. This increasing need for specialized bushings for EV powertrains and hybrids is a major driver, as it pushes suppliers to innovate and produce bushings that meet the unique challenges of these next-generation vehicles, positioning the market data for continued growth.

As countries including the U.S., China, and those in the European Union push for stringent emissions regulations, the adoption of electric and hybrid vehicles is set to accelerate. For example, the European Union's Green Deal mandates a phase-out of ICE vehicle sales by 2035, underscoring the rapid shift toward electric mobility. As a result, automakers are increasingly integrating specialized engine bushings into EVs to handle the unique forces associated with electric motors, including torque delivery, regeneration, and high-frequency vibrations.

In addition, hybrid vehicles, which combine internal combustion engines and electric powertrains, drive demand for sophisticated bushings. These vehicles require bushings that absorb vibrations from the engine and electric motor, ensuring smooth operation across the hybrid system’s entire performance spectrum. As more automakers expand their electric vehicle offerings and hybrids become more common, the need for advanced, high-performance engine bushings will continue to grow, positioning electrification as a major driver for the market. This trend shapes vehicle design and encourages innovation in material science, further expanding the market's scope.

Market Restraints

High Cost and Volatility in Raw Material Prices and Supply Chain Disruptions to Hamper Growth of Market

A restraining factor is the high cost of advanced materials and manufacturing for developing specialized engine bushings. As automotive technology evolves, particularly with the rise of electric vehicles (EVs) and hybrid vehicles, there is a growing need for more sophisticated engine bushings made from high-performance materials such as polyurethane, carbon composites, and advanced elastomers. While these materials offer improved durability, efficiency, and vibration damping, they have significantly higher production costs than traditional rubber or metal bushings. This cost factor poses a challenge, particularly for mid- and low-tier OEMs, who may struggle to incorporate these materials into their supply chains without raising vehicle prices.

Transitioning to electric vehicles and the required advanced components, including engine bushings, puts additional strain on automakers' budgets. As demand for high-performance bushings increases, OEMs must balance the desire for innovation with cost-effectiveness. Manufacturers also face rising raw material costs in the hybrid and EV segments, including rare-earth elements essential for producing certain specialized components such as high-performance bushings. The European Union’s Green Deal and stricter regulatory standards have driven automakers toward adopting more sustainable technologies. Still, the upfront investment in materials and technologies has slowed adoption for some players in emerging markets.

The complexity of producing lightweight and durable engine bushings that can meet performance and regulatory standards has led to longer development cycles, increasing R&D costs for manufacturers. Consequently, while innovation drives demand, the high initial cost of production and the need for cost-effective solutions remain significant barriers to market growth, especially in regions with cost-sensitive markets.

Ongoing volatility in raw material prices, compounded by supply chain disruptions, has intensified production costs and operational uncertainties. Engine bushings, predominantly made from natural, polyurethane, or synthetic rubber, heavily rely on commodity markets and global logistics networks. Recent geopolitical tensions, climate-related challenges, and post-pandemic economic shifts have aggravated price fluctuations and supply instability, directly impacting manufacturers' profitability and capacity to meet the growing demand.

Natural rubber, a primary material for bushings, has experienced significant price surges due to constrained supply from major producers such as Thailand, Indonesia, and Vietnam. In March 2023, Rubber News reported a 30% year-on-year increase in natural rubber prices, driven by adverse weather conditions, labor shortages, and rising fertilizer costs. For instance, Thailand, responsible for 35% of global natural rubber output, faced prolonged monsoon rains in 2022–2023, reducing latex yields. Simultaneously, Indonesia contended with deforestation policies limiting plantation expansion. Synthetic rubber, an alternative derived from petroleum, is similarly vulnerable. Crude oil price instability, influenced by the Russia-Ukraine conflict and OPEC+ production cuts, has elevated synthetic rubber costs. This dual dependency on natural and synthetic rubber leaves bushing manufacturers with limited flexibility, as substitution or inventory hedging strategies are costly and logistically complex.

Geopolitical disruptions have further fragmented the supply chains. The Russia-Ukraine war, for example, disrupted shipments of critical chemicals such as carbon black used in rubber reinforcement and hindered logistics routes through Eastern Europe. A February 2023 Supply Chain Dive analysis highlighted that 40% of European automotive suppliers faced delays in raw material deliveries, extending lead times for components such as bushings by 20–30 days. Similarly, U.S.-China trade tensions continue to reverberate, thus hampering market growth.

Market Opportunities

Smart Bushings Integrated with IoT and Sensor Technology Present a Transformative Growth Opportunity in Global Market

The market is undergoing a paradigm shift, driven by the rapid adoption of electric vehicles (EVs), autonomous mobility solutions, and the increasing emphasis on predictive maintenance and real-time performance monitoring. A transformative opportunity lies in integrating Internet of Things (IoT) capabilities and advanced sensor technologies into traditional engine bushings, evolving them into "smart bushings" capable of continuous condition monitoring and adaptive performance.

These intelligent bushings are embedded with micro-sensors that monitor real-time parameters such as wear, vibration, temperature, and stress. By transmitting this data to vehicle control systems, smart bushings enable predictive maintenance, reduce unplanned downtime, and optimize overall powertrain performance and durability, especially critical in commercial and high-utilization vehicles such as fleets, trucks, and ride-hailing services.

For example, Continental AG introduced its Active Vibe Bushings in April 2024, featuring integrated sensors that dynamically assess degradation and suspension stress, resulting in a 30% reduction in unplanned maintenance for commercial fleets. Similarly, in March 2024, ZF Friedrichshafen unveiled its Next-Generation Intelligent Bushings, engineered for autonomous vehicles. These bushings employ smart materials and embedded sensors to enhance NVH (Noise, Vibration, Harshness) isolation and deliver cleaner data streams to vehicle LiDAR and camera systems critical for the safety and stability of self-driving technologies.

Beyond comfort and safety, smart bushings also offer benefits in thermal management and material longevity, particularly in EV powertrains, which face unique vibration and load profiles due to fewer moving parts and high torque characteristics. These smart components can adapt in real time, compensating for shifting loads or wear. They can even communicate with vehicle ECUs (Electronic Control Units) to dynamically adjust suspension or drivetrain parameters.

As OEMs and Tier-1 suppliers push toward connected, autonomous, shared, and electric (CASE) mobility, smart engine bushings are poised to become standard in next-generation vehicle architectures. This creates substantial growth potential for engine bush supply chain players, from raw material providers and sensor developers to integrated systems manufacturers.

Segmentation Analysis

By Vehicle Type

Increasing Demand, Rising Disposable Incomes, and Urbanization Enhanced Adoption of SUVs

The market is segmented by vehicle type into passenger cars (hatchback/sedan, suvs) and commercial vehicles (lcv (light commercial vehicles), heavy trucks, buses & coaches, and others).

The passenger cars segment will account for 63.22% market share in 2026. The passenger cars segment is expected to dominate the market due to the high demand for passenger vehicles globally and the increasing integration of bushings for NVH reduction, leading to a smoother and more comfortable ride. The demand for bushings in hatchbacks and sedans is rising due to increased consumer expectations for comfort and noise reduction. Hatchback and sedan vehicles prioritize comfort, fuel efficiency, and affordability, necessitating high-quality bushings to reduce noise, vibration, and harshness (NVH). Integrating advanced bushing materials, such as polyurethane and composites, enhances ride quality and extends component lifespan.

- For instance, in January 2024, Renault SA announced the launch of five new passenger cars in India, including C SUV, B+ SUV, and electric vehicles, integrating high-performance engine bushes to meet the increasing comfort standards.

SUVs, known for their off-road capabilities and heavier structures, require robust bushing solutions to handle increased loads and stresses. The growing popularity of SUVs globally has led to a surge in demand for specialized bushings that can withstand these conditions. The SUV segment's fastest growth contributes to the overall market expansion by enabling advancements in bushing technology to meet the demands of heavier and more performance-oriented vehicles.

The commercial vehicle segment is expected to experience substantial growth, driven by increasing manufacturing and sales, especially in the LCV and heavy truck sectors. LCVs, such as vans and pickup trucks, are used for various transportation needs and require bushings for durability and longevity, especially in crucial conditions. Heavy-duty trucks require robust bushings to withstand heavy loads and rough terrains, contributing to a significant portion of the demand in this segment. Buses and coaches require bushings for passenger comfort and stability, especially during long-distance travel. This category includes specialized vehicles, military vehicles, and other niche applications where bushings play a significant role. The trend toward electric vehicles (EVs) and hybrid vehicles also influences the bushing market, as these vehicles require different bushing materials and designs to optimize performance and NVH.

By Material

Significant Vibration-Damping Properties and Cost-Effectiveness of Rubber Contribute to Segmental Growth

The market is segmented by material, with rubber, polyurethane, brass, aluminum, bronze, and others.

The Rubber segment is expected to account for 62.59% of the market in 2026. Rubber remains a dominantly used material for bushings due to its excellent vibration-damping properties and cost-effectiveness. However, rubber technology advancements are leading to high-damping rubber components.

- For example, in February 2024, Sumitomo Rubber Industries announced a USD 50 million investment to increase the production of high-damping rubber components at their facilities in Thailand, addressing the growing need for vibration control in the automotive industry within the Asia Pacific region.

Polyurethane bushings are expected to grow at a higher CAGR during the forecast period as they offer superior durability, chemical resistance, and better load performance than rubber. They are increasingly used in performance and heavy-duty applications. Manufacturers, including Vibracoustic, offer steering column bushings made of polyurethane to help reduce vibrations and give drivers a more secure and comfortable driving experience.

Aluminum bushings are experiencing significant growth as they are lightweight and offer good corrosion resistance, making them suitable for applications where weight reduction is crucial. The automotive industry's focus on fuel efficiency and emission reduction encourages the adoption of aluminum bushings in vehicle manufacturing. Brass, bronze, and other segments have seen considerable growth in the market.

To know how our report can help streamline your business, Speak to Analyst

By Sales Channel

Rise in Production of New Vehicles such as Electric Vehicles to Support OEM’s Dominance

Market is segmented into two primary sales channels, OEM and aftermarket.

The OEM segment is the dominant segment primarily due to the high volume of new vehicles produced globally. OEMs place bulk orders for engine bushings to equip vehicles during manufacturing. With the global automotive production consistently growing, particularly in China, Europe, and North America, OEMs remain the largest demand source. Furthermore, the rise in the production of electric vehicles (EVs), which require specialized bushings for motor mounts and powertrains, has further cemented the dominance of this segment. As per the International Energy Agency (IEA), global EV sales surged by 55% in 2022, driving more demand for specialized OEM components.

The Aftermarket segment is the fastest-growing segment of the market. As the global vehicle fleet ages, particularly in developed markets where vehicles are kept longer, the demand for replacement parts, including engine bushings, is rising. This is especially true for older vehicles that require maintenance and component replacements. The aftermarket is expanding rapidly in markets including North America and Europe, where vehicle ownership and longevity are high. The growing awareness of vehicle maintenance and the increasing adoption of EVs for repairs and replacements further fuels this segment’s growth.

ENGINE BUSH MARKET REGIONAL OUTLOOK

China and Japan’s Mature Automotive Component Industries Fuel Asia Pacific Market Development

Regionally, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Engine Bush Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 13.4 billion, contributing 52.90% to global market revenue, and is projected to grow to USD 14.14 billion in 2026, driven by the robust expansion of the automotive sector across key countries such as China, India, and Japan. The region benefits from a well-established automotive components industry, particularly in China and Japan, which continues to innovate and scale production capabilities. Government initiatives such as India’s ‘Make in India’ and ‘Startup India’ programs are accelerating investments in advanced manufacturing technologies and infrastructure, fostering the development of high-quality automotive components. Furthermore, the escalating demand for heavy commercial vehicles—spurred by rapid industrialization, infrastructure development, and urbanization—is significantly propelling market growth. The rise of the region's electric vehicles (EVs) also boosts demand for advanced engine bush technologies that enhance powertrain efficiency and durability.

The Japan market is projected to reach USD 1.63 billion by 2026, the China market is projected to reach USD 8.24 billion by 2026, and the India market is projected to reach USD 2.67 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 5.04 billion in 2025, accounting for 19.88% share, and is expected to reach USD 5.25 billion in 2026, supported by renowned automotive manufacturers including Volkswagen AG, Stellantis NV, Mercedes-Benz Group AG, BMW AG, and Renault SA. These manufacturers are heavily investing in developing premium and luxury vehicles that prioritize passenger safety, comfort, and superior driving experiences. Integrating advanced bushings in these vehicles plays a critical role in minimizing noise, vibration, and harshness (NVH), elevating overall vehicle refinement and safety standards. Europe’s stringent environmental regulations and push toward electrification and autonomous driving technologies drive continuous innovation in bushing materials and design.

The UK market is projected to reach USD 0.8 billion by 2026, while the Germany market is projected to reach USD 0.95 billion by 2026.

North America

The North America region captured 21.20% of the global market in 2025, generating USD 5.37 billion in revenue, and is projected to reach USD 5.6 billion in 2026. The North American market is characterized by a mature automotive industry emphasizing research and development. This has led to the adopting of sophisticated engine bush solutions that improve vehicle performance, fuel efficiency, and emissions standards. The U.S., as a major automotive hub, is experiencing rapid market growth propelled by increasing consumer demand for enhanced vehicle comfort, rising penetration of electric vehicles, and substantial investments in autonomous vehicle technologies. Moreover, the well-established supply chain network and the presence of key automotive OEMs and Tier-1 suppliers further strengthen the region’s market position. Emerging trends such as connected and smart vehicle technologies are also influencing the evolution of engine bush components in this region.

The U.S. market is projected to reach USD 3.84 billion by 2026.

Rest of the World

Rest of the World contributed 6.01% to the global market in 2025, with a valuation of USD 1.52 billion, and is projected to reach USD 1.6 billion in 2026. The Rest of the World, including regions such as South America, the Middle East and Africa, is witnessing notable market growth. This expansion is fueled by rising vehicle production volumes, growing adoption of electric and hybrid vehicles, and increasingly stringent environmental and safety regulations. Manufacturers in these regions invest in developing advanced bushing technologies and lightweight durable materials to meet evolving market demands. Infrastructure development, urbanization, and increasing disposable incomes further drive vehicle sales, creating new growth opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Borgwarner Inc. is Poised to be Leading Market Player, Driven by its Innovative Technology with Sustainability and Global Presence

BorgWarner Inc. is the leading manufacturer of engine mountings and engine bushes globally. The company profile stands out due to their innovative technology, global presence, and commitment to sustainability. BorgWarner’s diverse product portfolio, including engine bushes, is designed to meet the demands of internal combustion engines (ICE) and electric vehicles (EVs). The company produces highly durable, performance-driven components to minimize vibration, noise, and harshness (NVH), critical for improving vehicle comfort and efficiency. BorgWarner’s engine bushings are engineered using advanced elastomeric materials and polymer-based compounds, offering superior vibration isolation and durability. The company's extensive research and development capabilities have allowed it to design bushings that cater to a wide range of vehicle applications, including electric powertrains, where special bushings are required to handle regenerative braking and high-frequency vibrations. BorgWarner’s high-performance engine bush models, including the Engine Torque Rod Bushings and Motor Mount Bushings, are known for their longevity, reliability, and ability to withstand high stress while delivering excellent vibration reduction. Their continued focus on electrification and global manufacturing capabilities positions BorgWarner as a leader in the engine bush market, especially in evolving vehicle technology and stricter emission regulations.

Continental AG is the second-largest manufacturer of engine mountings and engine bushes, owing to its strong position in automotive components and a broad global market presence. Continental excels due to its cutting-edge engineering, innovation in materials, and ability to supply high-quality, durable components to a wide range of automakers. The company’s engine bushings are designed to meet high-performance standards, focusing on noise reduction, vibration isolation, and engine stability, all while adapting to the growing trend of electric mobility. Continental's engine bush models, such as Engine Mounting Systems and Hydraulic Engine Mounts, utilize advanced viscoelastic materials that deliver superior performance in vibration damping and enhance durability for both traditional ICE vehicles and emerging electric vehicle platforms. Their hydraulic engine mounts, in particular, offer precise damping characteristics, reducing NVH levels significantly. Continental’s focus on advanced material science and integrating electronic systems for active vibration control in its products, mergers, and acquisitions of related sector manufacturers makes it a key player in the market. With a strong commitment to sustainability and innovation, Continental continues to lead the charge in producing high-quality, technologically advanced engine bushes.

LIST OF KEY ENGINE BUSH COMPANIES PROFILED

- Continental AG (Germany)

- BorgWarner Inc. (U.S.)

- Federal-Mogul Corporation (U.S.)

- ZF Friedrichshafen AG (Germany)

- Dana Incorporated (U.S.)

- Magna International Inc. (Canada)

- Tenneco Inc. (U.S.)

- KYB Corporation (Japan)

- JTEKT Corporation (Japan)

- NHK Spring Co., Ltd. (Japan)

- Sumitomo Riko Company Limited (Japan)

- ElringKlinger AG (Germany)

- Faurecia (France)

- Delphi Technologies (U.S.)

- Hutchinson SA (France)

KEY INDUSTRY DEVELOPMENTS

- In June 2025, Setco Automotive Limited launched Load Cushion and Torque Rod Bush. This strategic expansion strengthens Setco’s presence in the commercial vehicle space, reinforcing its commitment to engineering excellence, durability, and performance.

- In May 2025, DuPont de Nemours, Inc. (DD, Financial) revealed a major restructuring of its management and reporting structure, effective from the first quarter of 2025. This strategic change is part of the company's preparation for its intended electronics separation, allowing DuPont to focus more effectively on its core business areas. The newly formed segments are ElectronicsCo and IndustrialsCo.

- In April 2025, Vibracoustic, a leading global automotive noise, vibration, and harshness (NVH) expert, engineered state-of-the-art solutions that significantly enhance the driving comfort and experience of a premium electric pickup truck. Air springs, jounce bumpers, and hydro bushings tackle unwanted excitations and support the performance of the all-electric pickup truck.

- In March 2025, DuPont Interconnect Solutions (ICS), a leading partner in materials solutions and system design within DuPont Electronics & Industrial, addressed key signal integrity, power, and thermal management challenges.

- In January 2024, the tech enterprise Rheinmetall received an important new order for engine components from a well-known, globally operating vehicle maker. The parts ordered are rocker arm bushings for use in different engine variants in the heavy transport segment. The order is worth a figure in the lower two-digit million-euro range.

REPORT COVERAGE

The market analysis provides detailed market analysis and focuses on key aspects such as leading companies, vehicle types, design, and technology. Besides this, the report offers insights into the latest market trends and highlights key industry developments. In addition to the abovementioned factors, the report encompasses several factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 4.23% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Million Units) |

|

Segmentation |

By Sales Channel

By Vehicle Type

By Material

By Region

|

Frequently Asked Questions

Fortune Business Insights says the market will reach USD 37.03 billion by 2034.

The market is expected to grow at a CAGR of 4.23% during the forecast period.

The increased requirement of specialized engine bushings with the growing hybrid and electric vehicles drives the market.

Asia Pacific led the market in 2025.

Asia Pacific market size share was USD 13.40 billion in 2025.

Continental AG, BorgWarner Inc., Vibracoustic SE, and ZF Friedrichshafen AG are a few of the leading market players operating in the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us