Enteral Feeding Devices Market Size, Share & Industry Analysis, By Product (Instruments [Enteral Feeding Tubes {Nasogastric Tubes, Gastrostomy Tubes, Jejunostomy Tubes, and Others}, Enteral Feeding Pumps, and Others] and Accessories), By Age Group (Adults and Pediatrics), By Application (Oncology, Neurological Disorders, Gastrointestinal Disorders, Diabetes, and Others), By End User (Hospitals & ASCs, Specialty Clinics, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Enteral Feeding Device Market Size and Future Outlook

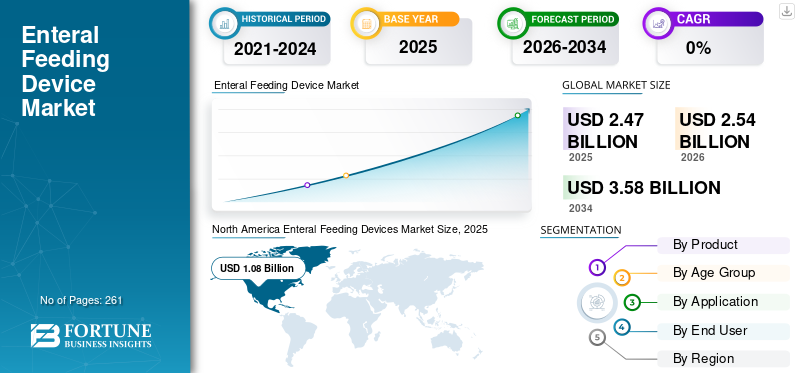

The global enteral feeding devices market size was valued at USD 2.47 billion in 2025 and is projected to grow from USD 2.54 billion in 2026 to USD 3.58 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. North America dominated the global enteral feeding devices market with a market share of 43.72% in 2025.

Enteral feeding devices refer to medical devices used to deliver liquid nutrition directly into the gastrointestinal tract for patients who are unable to ingest an adequate number of calories. The increasing prevalence of chronic conditions, including gastrointestinal disorders, neurological disorders, and others, is resulting in a growing number of patient admissions in healthcare settings. The rising number of patient admissions requiring nutritional support, combined with the technological advancements in these devices, is supporting the adoption rate of enteral feeding devices in the market.

- For instance, according to the 2023 data published by the Cleveland Clinic, it was reported that an estimated 10,000 to 20,000 people are affected by short bowel syndrome in the U.S.

Furthermore, the growing geriatric population, rising home enteral nutrition (HEN), advancements in tube materials and connectors, and the continuing rollout of ISO 80369‑3 (ENFit) standards for safer enteral connections are some of the other significant factors contributing to the rising number of enteral feeding cases in the market. This, along with the growing focus on research and development activities among key players, including Abbott, Fresenius Kabi, and others, is expected to support the global market growth.

Download Free sample to learn more about this report.

ENTERAL FEEDING DEVICES MARKET KEY TAKEAWAYS

Market Size & Forecast

Market Size & Forecast

- 2025 Market Size: USD 2.47 billion

- 2026 Market Size: USD 2.54 billion

- 2034 Forecast Market Size: USD 3.58 billion

- CAGR: 4.4% from 2026–2034

Market Share

Market Share

- North America dominated the global enteral feeding devices market with a market share of 43.72% in 2025.

- The pediatrics segment is anticipated to grow at a CAGR of 5.3% through 2034.

- The neurological disorders segment is expected to witness a CAGR of 5.0% over the study period.

Key Regional Highlights

Key Regional Highlights

North America

North America held the dominant share in 2024, valued at USD 1.05 billion, and also took the leading share in 2025 with USD 1.08 billion.

Europe

Europe is projected to reach USD 0.82 billion in 2026, driven by growing ENFit adoption, increasing patient populations, and expanding home-based enteral care.

Asia Pacific

Asia Pacific is expected to attain USD 0.42 billion in 2026, supported by improving healthcare access and rising demand for nutritional support therapies.

U.S.

The market is estimated to reach USD 0.96 billion in 2026, fueled by an aging population, increasing chronic disease burden, and technological advancements in enteral feeding devices.

Japan

Market growth is expected to be supported by a rapidly aging population, rising healthcare expenditure, and increasing demand for long-term nutritional care solutions.

Read More

Market Dynamics:

Market Drivers

Increasing Prevalence of Chronic Conditions to Boost Market Growth

The increasing prevalence of chronic conditions, such as neurological diseases, cancer, and others, is resulting in the growing adoption of nutritional support devices among individuals who are unable to ingest adequate calories, subsequently driving the demand for these products in the market.

- For instance, according to 2023 data published by the Alzheimer's Association, it was reported that more than 6 million Americans are living with Alzheimer’s Disease in the U.S.

Moreover, the growing geriatric population is a major factor contributing to the increasing prevalence of chronic conditions among the patient population, thereby further boosting the global demand for these devices. Therefore, the factors mentioned above, along with the growing research and development activities to launch technologically advanced devices among the key market players, are expected to boost the adoption rate, thereby supporting the global enteral feeding devices market growth.

Market Restraints

High Cost Associated with Advanced Products to Hinder Market Growth

There is a growing demand for these devices owing to their benefits, including improve immune function, and others. However, the high cost associated with the novel devices is anticipated to hinder their adoption rate, especially in developing countries such as India, South Africa, and others.

Limited public healthcare funding, intense competition, and high patient volumes are some of the factors resulting in the high cost of these devices in the market. Growing technological advancements in these devices, including smart pumps with real-time data tracking and remote monitoring capabilities, among others, are some of the additional factors supporting the increasing cost of these devices in the market.

- For instance, according to 2025 data published by Curemed, it was reported that the price of feeding pumps ranges from USD 720.0 to USD 1800.0.

Furthermore, the recurring costs for administration sets, nutrition formulas, feeding tubes, and others also add up to a financial burden among the patient population, especially in home care settings. Therefore, high costs, limited reimbursement policies, and others are expected to limit the adoption rate of these devices in the market.

Market Opportunities

Technological Advancements in these Devices to Create Market Opportunities

There is a growing emphasis on integrating technological advancements into enteral nutrition devices on the market. The advancements in technology, including smart pumps with real-time monitoring features, precision sensors, and standardized, safer connectors, among others, have improved patient safety, device functionality, and ease of use among the patient population in clinical settings.

These technological advancements are enabling the provision of accurate feeding services to patients and widening the use of enteral feeding services in homecare settings. This, along with the growing focus of prominent players on R&D activities to integrate artificial intelligence in these devices, is anticipated to boost demand for personalized patient care and adoption of these devices, thereby supporting the growth of the market for enteral feeding devices globally.

- In September 2023, Cardinal Health introduced the Kangaroo OMNI Enteral Feeding Pump, designed to offer patients advanced options tailored to their personalized needs in the U.S.

Market Challenges

Restricted Reimbursement Policies for Enteral Nutrition to Hamper Market Growth

Reimbursement frameworks for Foods for Special Medical Purposes (FSMPs) differ widely across countries and healthcare environments. As reported by ScienceDirect in 2019, European countries, including Germany, the Netherlands, and France, offer comparatively higher reimbursement rates across outpatient, hospital, and other clinical settings. In contrast, many other developed and developing economies provide only restricted reimbursement support.

Furthermore, 2023 data from the Centers for Medicare & Medicaid Services (CMS) indicate that while enteral nutrition products qualify under the Prosthetic Device benefit, coverage excludes associated equipment, supplies, and temporary impairments, and orally administered enteral nutrition products.

Additionally, several developed and emerging nations categorize enteral feeding as an ancillary or dietary care, which further leads to partial or no coverage for enteral nutrition products, such as feeding pumps and feeding tubes, resulting in growing out-of-pocket costs among hospitals, long-term care facilities, and patients.

Other Prominent Challenges:

- Placement complications (aspiration risk, tube occlusion, dislodgement) necessitating training, protocols, and accessories.

- Supply chain and raw‑material constraints for polymers and specialty components affecting lead times and costs.

- Transition management from legacy to ENFit connectors across mixed inventories in large provider networks.

- Training gaps for caregivers and patients in home settings, elevating support and education requirements.

Enteral Feeding Devices Market Trends

Shifting Preference toward Homecare Settings to Boost Product Demand

There is an increasing trend toward home-based enteral nutrition (HEN) among the patient population. This shift is driven by certain factors, such as the growing prevalence of chronic conditions requiring long-term enteral support, an increasing aging population, advanced portable devices, and remote patient monitoring, among others. Moreover, the increasing emphasis on patient comfort, shorter hospital stays, fewer tube dislodgements, lower infection rates, reduced readmissions, and improved quality of life are additional factors contributing to the growing preference for home-based therapies in the market.

This shift is augmenting the demand for these enteral nutrition devices across various indications among patients. The key players are focusing on research and development activities to develop and launch technologically advanced products that can be optimized for home use, such as simpler administration sets, and others.

- For instance, according to data published by the National Home Infusion Association (NHIA) in 2024, approximately 234,070 patients utilized home enteral nutrition that year.

Other Prominent Trends:

- Widespread adoption of ISO 80369‑3 (ENFit) connectors to reduce misconnections; migration from legacy connectors nearing completion in many markets.

- User‑centric tube innovations: anti‑kink, antimicrobial coatings, balloon/low‑profile gastrostomy designs, and radiopaque markings for placement verification.

- Expanded indications in oncology, stroke, head‑and‑neck surgery, and neurodegenerative diseases support long‑term feeding plans.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Product

Increasing Product Approvals Led to Instruments Segment Dominance

Based on type, the market is classified into instruments and accessories. Instruments are bifurcated into enteral feeding tubes, enteral feeding pumps, and others. Furthermore, enteral feeding tubes are segmented into nasogastric tubes, gastrostomy tubes, jejunostomy tubes, and others.

The instruments segment held the largest market share in 2025. The growth is due to the increasing prevalence of chronic conditions such as gastrointestinal disorders and others among patients, resulting in a growing demand for enteral nutrition devices globally. This, along with the growing focus of key players toward research and development activities to launch innovative devices, is further anticipated to support the segmental growth.

- For instance, in October 2022, Rockfield Medical Devices received U.S. FDA approval for the Mobility + Enteral Feeding System in the U.S.

The accessories segment is expected to grow at a CAGR of 4.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Age Group

Increasing Prevalence of Chronic Conditions Led to the Dominance of Adults Segment

Based on age group, the market is bifurcated into adults and pediatrics.

The adults segment dominated the market in 2025. In 2026, the segment is anticipated to dominate with an 87.9% share. The dominant share is owing to its increasing prevalence of chronic disorders such as neurological disorders, cancer, gastrointestinal disorders, and others, resulting in a rising adoption rate of enteral nutrition devices among adults globally.

- For instance, according to 2024 data published by the Centers for Disease Control and Prevention, it was reported that about 3.1 million adults are suffering from inflammatory bowel disease in the U.S.

The pediatrics segment is expected to grow at a CAGR of 5.3% over the forecast period.

By Application

Growing Prevalence of Cancer Led to Dominance of Oncology Segment

On the basis of application, the market is segmented into oncology, neurological disorders, gastrointestinal disorders, diabetes, and others.

The oncology segment dominated the global market in 2025. By application, the oncology segment held the share of 29.9% in 2025. The growth is primarily owing to the growing prevalence of various types of cancer, including neck cancer, stomach cancer, among others, resulting in rising demand for novel enteral nutrition devices in the market.

- For instance, according to 2025 data published by the American Cancer Society (ACS), about 2.0 million new cancer cases are estimated to occur in the U.S.

The neurological disorders segment is set to flourish with a growth rate of 5.0% over the forecast period.

By End User

Growing Number of Patient Admissions Boosted Hospitals & ASCs Segment Growth

Based on end user, the market is segmented into hospitals & ASCs, specialty clinics, homecare settings, and others.

The hospitals and ASCs segment dominated the market in 2025. The increasing prevalence of chronic conditions, the growing number of patient admissions, and the rising number of healthcare settings, such as hospitals & ASCs, are some of the major factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 49.5% share in 2026.

- For instance, according to data published by the Statistisches Bundesamt in 2023, there are approximately 1,874 hospitals in Germany.

In addition, homecare settings end users are projected to grow at a CAGR of 4.7% during the study period.

Enteral Feeding Devices Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Enteral Feeding Devices Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 1.05 billion, and also took the leading share in 2025 with USD 1.08 billion. The dominance of the region is owing to distinct factors, such as increasing prevalence of chronic conditions, rising number of patient admissions, robust healthcare infrastructure, adequate reimbursement policies, and rising product launches among the prominent players, among others.

In 2026, the U.S. market is estimated to reach USD 0.96 billion. Increasing prevalence of chronic diseases, rising aging population, growing nutritional awareness and technological advancements in these products are some of the factors supporting the growth of the market in the country.

- For instance, according to 2024 statistics published by the American Parkinson Disease Association, it was reported that about 1 out of every 336 million people is living with Parkinson's Disease in the U.S.

Europe

During the study period, the European region is projected to record a growth rate of 4.2% and reach the valuation of USD 0.82 billion in 2026. This is due to the increasing prevalence of chronic conditions, growing patient pool, rising number of healthcare settings, growing ENFit adoption, a preferential shift toward home-based enteral therapies, and the improving reimbursement frameworks in the region. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.13 billion, Germany to record USD 0.15 billion, and France to record USD 0.12 billion in 2026.

Asia Pacific

The market in Asia Pacific is estimated to reach USD 0.42 billion in 2026 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.05 billion while China is estimated to reach USD 0.13 billion in 2026.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market in the coming years. The Latin America market in 2026 is expected to reach a valuation of USD 0.11 billion. The rising tertiary care capacity, neonatal/critical care investments, gradual expansion through private insurance and public tenders, and increasing focus on home‑based nutrition support are anticipated to boost product adoption in these regions. In the Middle East & Africa, GCC is set to attain the value of USD 0.04 billion in 2026.

Competitive Landscape

Key Industry Players

Growing R&D Facilities Establishments Among Key Players to Support Their Dominance

A robust product portfolio of novel devices, coupled with a strong global geographical presence, is one of the crucial factors contributing to the dominance of producers of enteral feeding devices in the market. Abbott, Fresenius Kabi, and Cardinal Health are major players in the market. Moreover, the rising focus of prominent players on R&D facilities establishments is likely to support the global enteral feeding devices market share.

- For instance, in June 2025, Fresenius Kabi established a new Enteral Nutrition Research and Development (EN R&D) center in India with an aim to expand its geographical presence.

Other manufacturers of enteral feeding devices, including B. Braun SE, are also growing in the market, primarily due to their increased focus on product launches to strengthen their brand presence.

List of Key Enteral Feeding Device Companies Profiled:

- Abbott (U.S.)

- Cardinal Health (U.S.)

- Fresenius Kabi (Germany)

- Braun SE (Germany)

- BD (U.S.)

- Boston Scientific Corporation (U.S.)

- AVNS (U.S.)

- Moog Inc. (U.S.)

- CONMED Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- June 2025 – NanoVibronix, Inc. announced that a regional acute care hospital signed an agreement to acquire two ENvue Navigation Systems through its ENvue Medical division in the U.S., helping the company strengthen its presence.

- June 2025 – NanoVibronix, Inc., received a new U.S. patent for its pediatric feeding tube guidance system. This helped the company to increase its brand presence.

- April 2025 – Amsino International, Inc., launched Amsino Scientific, a new medical device manufacturing and R&D facility in the U.S., with an aim to increase its brand presence in the market.

- February 2025 – NanoVibronix, Inc., acquired ENvue Medical Holdings Corp., a private player dedicated to enteral feeding products, with an aim to widen its product portfolio.

- November 2024 – Gravitas Medical, Inc., received U.S. FDA approval for the Entarik system, which supports the placement of feeding tubes and continuously monitors feeding tube position, gastric and esophageal temperature, and gastrointestinal impedance and reflux.

REPORT COVERAGE

The market report provides a detailed global enteral feeding devices market analysis and focuses on key aspects such as leading companies, product, age group, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2019-2024 |

|

Growth Rate |

CAGR of 4.4% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Age Group, Application, End User, and Region |

|

By Product |

|

|

By Age Group |

|

|

By Application |

|

|

By End User |

|

|

By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2.47 billion in 2025 and is projected to reach USD 3.58 billion by 2034.

In 2025, the North America regional market value stood at USD 1.08 billion.

Growing at a CAGR of 4.4%, the market will exhibit steady growth over the forecast period (2026-2034).

By product, the instruments segment led the market.

The introduction of technologically advanced enteral feeding devices is one of the major factors driving the market's growth.

Abbott and Fresenius Kabi are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions and the rising number of product launches are expected to drive the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us