ESG in Manufacturing Market Size, Share & Industry Analysis, By Service Type (ESG Strategy & Consulting, Environmental Services, ESG Reporting & Disclosure, Implementation & Integration, Risk, Compliance & Governance, Supply Chain ESG Services, Managed ESG Services, and Others), By Type (Environmental, Social, and Governance), By Industry (Automotive, Metals & Mining, Chemicals, Electronics, Food & Beverages, Industrial Machinery & Equipment, Plastics & Packaging, and Others), and Regional Forecast, 2026 – 2034

ESG in Manufacturing Market Size and Future Outlook

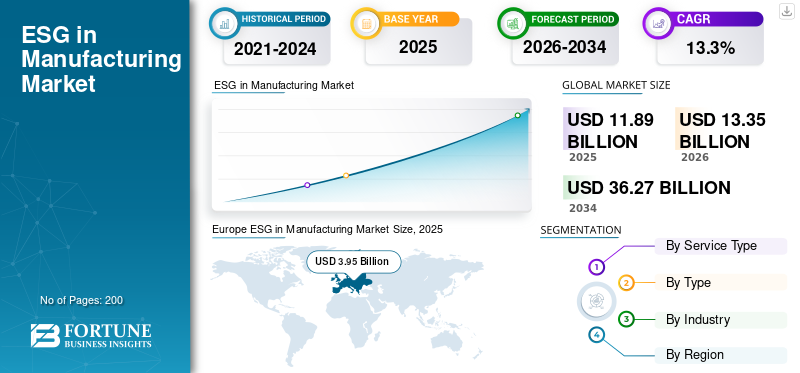

The global ESG in manufacturing market size was valued at USD 11.89 billion in 2025. The market is projected to grow from USD 13.35 billion in 2026 to USD 36.27 billion by 2034, exhibiting a CAGR of 13.3% during the forecast period. Europe dominated the ESG in the manufacturing market with a market share of 33.22% in 2025.

ESG in manufacturing refers to the services required to design, implement, manage, measure, and report Environmental, Social, and Governance (ESG) practices across the company’s operations and supply chains. Stringent regulatory policies, environmental regulations, and increasing investment in carbon accounting are all fueling the market demand for ESG frameworks. Several manufacturing firms, due to their legacy infrastructure, have huge carbon emissions, as a result, key players are committed toward net-zero emissions and waste management. Accelerating investment in ESG performance, green bonds, sustainability-linked financing, growing importance of Scope 3 emissions are all driving the market growth. Rising carbon price and energy costs are further pushing companies to integrate with ESG practices.

- For instance, in February 2025, TÜV SÜD expanded its industrial sustainability certification and audit services across Southeast Asia.

Key players such as Accenture, Ernst & Young, Deloitte, etc. are a few of the key players in the market. Key players are focusing on supply chain ESG integration, digitalization of ESG, and investment in advanced ESG reporting. Several such strategic moves by the market players to enhance ESG in the manufacturing market share in diverse regions.

Download Free sample to learn more about this report.

ESG IN MANUFACTURING MARKET TRENDS

Rising Focus on Scope 3 Emissions Management to Bolster the Market Growth

There are several indirect emissions across the value chain, which are relatively complex and difficult to measure. Scope 3 emissions account for more than two-thirds of the total carbon footprint, generating huge market demand for emissions management. Regulatory pressures, ESG frameworks, such as greenhouse gas emissions protocols-based target initiatives, are all increasingly demanding a reduction in Scope 3 emissions. Large manufacturing firms and corporations are all pushing ESG requirements across the value chain, mandating, reporting, and limiting emissions.

- For example, in September 2025, Ecolab entered a five-year ESG-focused collaboration with Siam Cement Group (SCG) to enhance water efficiency, emissions reduction, and sustainable manufacturing processes. The partnership integrates digital monitoring and circular resource management solutions across SCG’s industrial facilities.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

End-to-End ESG Strategies are Driving the Market Demand

Manufacturing requires deep operational transformation, where ESG strategies must be tailored to plant-level activities and industrial processes. This drives demand for process re-engineering services, sustainability roadmaps, and cross-functional ESG integration consulting. Additionally, firms need support in aligning ESG goals with business KPIs, ensuring that sustainability initiatives contribute to both compliance and profitability. Manufacturing firms operate through complex workflows involving procurement of raw materials, production processes, logistics, and distribution, all of which have distinct environmental and social impacts. As manufacturers expand globally, there is a need to maintain consistency in ESG practices across multiple facilities, which further increases reliance on advisory and managed services. Overall, this trend reflects a shift from isolated ESG efforts to a holistic, enterprise-wide ESG transformation, making integration services a critical and recurring revenue driver in the ESG in manufacturing market growth.

- For instance, in April 2025, LEGO opened one of its most sustainable, renewables-powered manufacturing plants, designed to minimize emissions and resource consumption.

MARKET RESTRAINTS

Limited In-House Expertise and Resistance to Operational Change

Many manufacturing firms, particularly traditional and mid-sized players, operate on legacy systems and established processes that have been optimized for cost and efficiency rather than sustainability. Introducing ESG practices often requires fundamental changes in production workflows, procurement policies, and compliance structures, which can face internal pushback. Employees and plant-level management may interpret ESG initiatives as disruptive or non-essential, especially when immediate financial benefits are not evident. Overall, this combination of limited expertise and resistance to change slows down ESG integration and acts as a key barrier to the growth of ESG services in the manufacturing sector.

MARKET OPPORTUNITIES

Increasing Demand for ESG Assurance, Audit, and Certification Services to Bring Market Opportunities

As manufacturers increasingly publish sustainability reports and ESG metrics, stakeholders such as investors, regulators, and customers are demanding verified and reliable data rather than self-reported claims. This has created a strong need for third-party validation services that can independently assess ESG performance and ensure compliance with global standards.

Manufacturing industries, particularly those with high environmental and social risks such as chemicals, metals, and automotive, are under greater scrutiny, making regular ESG audits and certifications essential. Companies are seeking services that can validate emissions data, assess compliance with frameworks such as GRI and TCFD, and provide certifications related to environmental and social practices.

MARKET CHALLENGES

Managing ESG Across Multi-Tier Global Supply Chains Might Limit the Market Growth

One of the most critical challenges in ESG adoption for manufacturing is managing compliance across multi-tier, globally dispersed supply chains. Many suppliers, especially in emerging markets, may lack the resources, awareness, or infrastructure to track and report ESG data accurately. As a result, manufacturers face challenges in collecting reliable data, enforcing ESG standards, and ensuring consistent compliance across all tiers. Additionally, enforcing ESG compliance can strain supplier relationships, particularly when cost pressures are high, and suppliers prioritize operational efficiency over sustainability investments.

Segmentation Analysis

By Service Type

Environmental Services Dominate the Market Owing to Wide Array of Industry Applications

Based on service type, the market is divided into ESG strategy & consulting, environmental services, ESG reporting & disclosure, implementation & integration, risk, compliance & governance, supply chain ESG services, managed ESG services, and others.

Environmental services account for the highest ESG in manufacturing market share, primarily due to the direct and immediate regulatory pressure on environmental compliance. Manufacturing industries such as chemicals, metals, automotive, and food processing are highly resource-intensive and are subject to strict regulations related to carbon emissions, waste management, water usage, and pollution control. As a result, manufacturers are compelled to invest significantly in services such as carbon accounting, energy audits, Lifecycle Assessments (LCA), and sustainability consulting.

Supply chain ESG services are witnessing the highest growth rate of about 12.7% during 2026-2034, driven by the increasing focus on Scope 3 emissions and value chain accountability. A significant portion of a manufacturer’s environmental and social impact lies beyond its direct operations, within its supplier network and downstream activities. As global regulations and frameworks such as CSRD and SBTi emphasize full value chain transparency, manufacturers are under growing pressure to monitor and manage ESG performance across all tiers of suppliers.

- For instance, in June 2025, Amcor partnered with Alter Eco to launch recyclable paper-based packaging, reducing material usage by 60%+ compared to conventional solutions.

To know how our report can help streamline your business, Speak to Analyst

By Type

Environmental Segment Dominate the Market Owing to Direct Impact on Manufacturing Activities

Based on type, the market is segmented into environmental, social, and governance.

Environmental segment to dominate the market revenue share in the global market primarily due to the direct impact of manufacturing activities on natural resources and emissions. Industries such as chemicals, metals, automotive, and food processing are highly energy- and resource-intensive, leading to significant carbon emissions, water consumption, and waste generation. This makes environmental compliance a core operational priority rather than a discretionary initiative. Additionally, stringent environmental regulations across major regions, particularly in Europe and North America, are compelling companies to continuously monitor and reduce their environmental impact.

The governance segment is witnessing the highest growth rate of about 14.1% during 2026-2034, driven by the increasing need for transparency, accountability, and standardized ESG reporting. As regulatory frameworks such as CSRD, TCFD, and other global disclosure standards become more stringent, manufacturers are required to provide accurate, auditable, and comprehensive ESG data. This is significantly increasing demand for services related to ESG reporting, compliance management, risk assessment, and internal governance structuring.

By Industry

Chemicals Segment Dominate the Market Owing to Refinery Upgrades and New Infrastructure Development

Based on industry, the market is segmented into automotive, metals & mining, chemicals, electronics, food & beverages, industrial machinery & equipment, plastics & packaging, and others.

The chemicals segment dominated the market share in 2025 primarily due to the high environmental and regulatory risk associated with chemical production processes. The industry involves the handling of hazardous substances, emissions of Volatile Organic Compounds (VOCs), and significant waste generation, making it one of the most heavily regulated sectors globally. As a result, chemical manufacturers are required to invest extensively in ESG-related services such as environmental compliance consulting, emissions monitoring, waste management advisory, and lifecycle assessments.

The electronics segment is witnessing the highest growth rate of 15.4% during 2026-2034, driven by the increasing emphasis on supply chain transparency, resource sustainability, and regulatory compliance in global electronics production. The industry is highly globalized, with complex, multi-tier supply chains spanning multiple countries, making it particularly exposed to Scope 3 emissions and supplier ESG risks.

ESG in Manufacturing Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Europe

Europe ESG in Manufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe represents the most advanced and regulation-driven ESG market for manufacturing, driven by stringent policies such as the Corporate Sustainability Reporting Directive (CSRD), EU Taxonomy, and Carbon Border Adjustment Mechanism (CBAM). Owing to several such factors, Europe dominates the global market. These regulations mandate comprehensive ESG disclosures, making ESG services essential for compliance rather than merely optional. European manufacturers are also under pressure to ensure supply chain transparency, driving growth in supplier ESG audits and Scope 3 consulting. The market is highly mature, with widespread adoption of ESG frameworks and reporting standards, leading to steady as well as stable growth.

U.K. ESG in Manufacturing Market

The U.K. market in 2026 is expected to reach a value of USD 0.62 billion, representing roughly 4.6% of global market revenues.

Germany ESG in Manufacturing Market

Germany’s market is projected to reach USD 1.01 billion in 2026, equivalent to around 7.5% of the global sales.

North America

North America is characterized by strong institutional frameworks, investor-driven pressure, and advanced consulting ecosystems. A key growth driver is the increasing emphasis on ESG-linked financing and investor scrutiny, where companies are required to demonstrate transparency and accountability in sustainability practices. Additionally, regulatory developments such as SEC climate disclosure requirements are pushing manufacturers to adopt structured ESG reporting and governance frameworks. Moreover, the presence of large multinational manufacturers with global supply chains is driving demand for supply chain ESG services and Scope 3 emissions management.

U.S. ESG in Manufacturing Market

The U.S. market is one of the most mature markets in North America and is estimated to reach a value of USD 3.50 billion in 2026. The growth is driven primarily by investor pressure, regulatory developments, and corporate sustainability commitments. Large manufacturing firms across sectors such as chemicals, automotive, and industrial machinery are actively investing in ESG strategies, risk management, and reporting services to meet stakeholder expectations. Increasing focus on decarbonization, energy efficiency, and corporate governance are accelerating demand for environmental and advisory services.

Asia Pacific

Asia Pacific is the fastest-growing market, driven by its position as the global manufacturing hub and increasing integration into international supply chains. Countries such as China, India, Japan, and ASEAN nations are witnessing rapid ESG adoption due to export-driven compliance requirements, particularly from Europe and North America. The region’s large and diverse industrial base creates strong demand for implementation, integration, and supply chain ESG services. The complexity of multi-tier supply chains in Asia Pacific is also fueling demand for Scope 3 emissions management and supplier ESG audits. Overall, Asia Pacific offers high growth potential with strong demand for operational and supply chain ESG services.

China ESG in Manufacturing Market

China’s market is projected to remain dominant in the Asia Pacific region in 2026 with revenues reaching USD 1.53 billion, representing roughly 11.4% of global sales.

India ESG in Manufacturing Market

The Indian market size in 2026 is projected to be valued at USD 0.56 billion, accounting for roughly 4.2% of the global market.

ASEAN ESG in Manufacturing Market

The ASEAN market in 2026 is expected to reach a value of USD 0.56 billion, accounting for roughly 4.2% of revenue.

South America

The market in South America is driven by resource-based industries and export-oriented manufacturing, particularly in countries such as Brazil and Argentina. The region’s strong presence in mining, agriculture, and food processing industries creates a need for ESG services focused on environmental compliance, sustainability, and supply chain transparency. While regulatory frameworks are still evolving compared to developed regions, there is a growing focus on ESG disclosures and sustainability initiatives. The market is also benefiting from rising awareness among manufacturers and increasing investor interest in sustainable operations.

Brazil ESG in Manufacturing Market

The Brazil market is projected to reach USD 0.55 billion in 2026, representing roughly 4.1% of the global market.

Middle East & Africa

The market in the Middle East & Africa region is emerging but rapidly evolving, driven by economic diversification and sustainability initiatives. In the Middle East, countries within the GCC are investing heavily in sustainable industrial infrastructure and energy transition programs, such as Saudi Vision 2030 and UAE sustainability strategies. These initiatives are creating demand for ESG consulting, environmental services, and implementation support. In Africa, South Africa leads ESG adoption due to its established industrial base and regulatory frameworks, particularly in mining and heavy industries.

GCC ESG in Manufacturing Market

The GCC market is expected to reach USD 0.33 billion in 2026, representing roughly 2.5% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaboration and Advanced Product Launch to Propel the Market Penetration

Key players in the ESG in manufacturing market are adopting a range of strategic moves to strengthen their market position, expand service offerings, and capture long-term value. Many firms are also pursuing mergers and acquisitions (M&A) to acquire niche expertise in areas such as carbon accounting, lifecycle assessment, and ESG reporting, thereby strengthening their domain capabilities. Growing emphasis on expanding geographic presence, particularly in high-growth regions such as the Asia Pacific and the Middle East, to tap into emerging ESG demand. Furthermore, players are adopting recurring revenue models through managed ESG services, offering continuous monitoring, reporting, and compliance support to clients.

- For instance, in February 2025, Bureau Veritas acquired SPIN360, a sustainability advisory firm specializing in lifecycle analysis and supply chain traceability.

LIST OF KEY ESG IN MANUFACTURING COMPANIES PROFILED

- Accenture plc (Ireland)

- Deloitte Touche Tohmatsu Limited (U.K.)

- PricewaterhouseCoopers (PwC) (U.K.)

- Ernst & Young (EY) (U.K.)

- KPMG International (Netherlands)

- Environmental Resources Management (U.K.)

- SLR Consulting (U.K.)

- Bureau Veritas (France)

- SGS SA (Switzerland)

- Mckinsey & Company (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Accenture partnered with a consortium of global industrial manufacturers to deliver end-to-end ESG transformation services, including decarbonization roadmaps and operational sustainability integration.

- July 2025: Deloitte expanded its ESG assurance and reporting services tailored for manufacturing clients to comply with CSRD and ISSB standards.

- June 2025: ERM acquired a boutique sustainability advisory firm specializing in industrial decarbonization and lifecycle assessments. The acquisition strengthens ERM’s ability to provide end-to-end ESG advisory services for manufacturing clients.

- May 2025: PwC partnered with a global automotive OEM network to provide supplier ESG risk assessment and compliance services.

- April 2025: SGS launched enhanced ESG verification and certification services for manufacturers, including carbon footprint validation and sustainability labeling.

REPORT COVERAGE

The global ESG in manufacturing market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.3% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Service Type, Type, Industry, and Region |

| By Service Type |

|

| By Type |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 11.89 billion in 2025 and is projected to reach USD 36.27 billion by 2034.

In 2025, the market value stood at USD 3.95 billion.

The market is expected to exhibit a CAGR of 13.3% during the forecast period.

By service type, the environmental services segment dominates the market revenue.

End-to-End ESG strategies are driving the market demand.

Accenture, Deloitte, PwC, Ernst & Young, and KPMG international are the major players in the global market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us