Ethylene Vinyl Acetate (EVA) Market Size, Share & Industry Analysis, By Grade (Low Density, Medium Density, and High Density), By Application (Films, Adhesives, Foams, Solar Cell Encapsulation, and Others), and Regional Forecast, 2026-2034

Ethyl Vinyl Acetate (EV) Market Insights

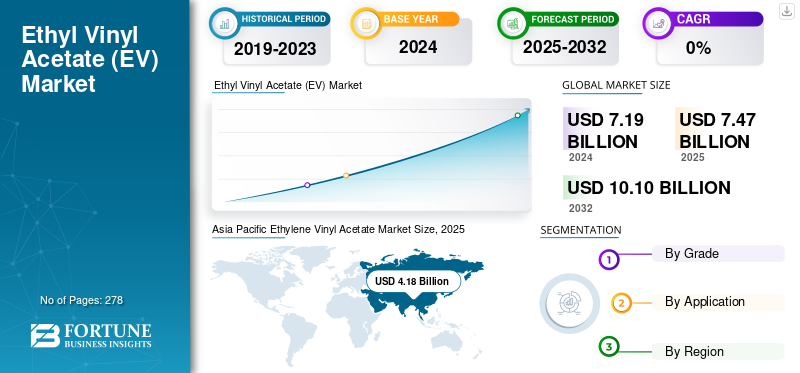

The global Ethylene Vinyl Acetate (EVA) market size was valued at USD 7.19 billion in 2024. The market is projected to grow from USD 7.47 billion in 2025 to USD 10.10 billion by 2032, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global ethylene-vinyl acetate market with a market share of 58.13% in 2024.

Ethylene Vinyl Acetate (EVA) is a versatile thermoplastic copolymer of ethylene and vinyl acetate, known for its flexibility, low-temperature toughness, clear appearance, and stress-crack resistance. EVA is widely used in applications such as footwear, packaging films, sporting goods, hot-melt adhesives, and even as a medical-grade material for devices and drug delivery systems. Compared to traditional plastics such as polyethylene, EVA is softer, more flexible, and can withstand lower temperatures without becoming brittle. This low-density, lightweight material also exhibits excellent impact and shock-absorbing qualities, along with resistance to UV radiation, making it highly durable and suitable for both indoor and outdoor use. Its combination of flexibility, durability, and processing ease has made EVA a popular choice across various sectors, driving market growth.

The market is dominated by several major players, including ExxonMobil, Hanwha Chemical, Dow, Asia Polymer Corp (APC), Formosa Plastics Corp (FPC), and LG Chem. Their broad portfolios, innovative product launches, and strong geographic expansion have supported their dominance in the global market.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS:

Accelerated Growth in Solar Photovoltaics (PV) to Drive the Demand for EVA

Solar photovoltaics (PV) is a highly flexible technology that can be mass-produced, leading to economies of scale. It can also be implemented in small amounts, making it suitable for various applications ranging from modest residential rooftop systems to large-scale utility power generation projects. Such flexibility has spurred the adoption of solar technology among a variety of end users, thereby increasing its overall global popularity. The rapid growth of the solar photovoltaic (PV) industry will directly drive the demand for ethylene vinyl acetate, as it is a crucial component in solar panel manufacturing. EVA films protect delicate solar cells from environmental factors such as moisture, dust, UV radiation, and mechanical stress, ensuring the long-term efficiency and durability of the panels. Thus, the global shift toward solar-powered energy, combined with the exceptional properties offered by the product, is expected to drive the global ethylene vinyl acetate market growth throughout the assessment period.

- In 2024 alone, the world added approximately 597 GW of new PV capacity, with China alone contributing around 329 GW. Additionally, solar technology is projected to account for 80% of the growth in global renewable capacity by 2030.

MARKET RESTRAINTS:

Presence of Substitutes May Hamper Demand for EVA in the Long Term

Many players across the value chain are exploring substitutes for EVA to leverage measurable gains in reliability, processing efficiency, compliance, and risk control. For instance, in solar energy, polyolefin elastomer (POE) and multi-layered encapsulants are exerting downward pressure on the demand for traditional EVA. POE and multi-layered encapsulants offer superior moisture resistance and higher anti-PID capacity compared to traditional EVA films and sheets, making them preferable for manufacturers seeking to improve module reliability and lifespan in challenging environments. Furthermore, the growing popularity of bifacial and glass-glass solar modules requires encapsulants that can perform on both sides and withstand increased operational stress. POE and multi-layered films are better suited for these designs, which represent a major trend in the solar industry. Hence, while EVA remains dominant due to its cost-effectiveness, the shift toward more advanced and sensitive solar technologies is driving the adoption of superior materials, potentially hampering the demand for EVA.

MARKET OPPORTUNITIES:

Specialty EVA Grades for High-Performance Foams to Create Lucrative Opportunity

The shift toward specialty EVA grades presents a strong value-creation opportunity as end-use industries increasingly demand performance-enhanced materials over commodity alternatives. High-performance EVA foams used in footwear midsoles, sports equipment, safety gear, and automotive interiors require controlled VA content, improved resilience, and superior energy absorption. Such product features command higher margins and help differentiate suppliers from low-cost commodity producers. The most significant value driver is the global solar PV sector, where high-density, encapsulant-grade EVA offers exceptional cross-linking behavior, UV resistance, transparency, and long-term durability. As industries prioritize durability, sustainability, and application-specific performance, specialty EVA grades will increasingly outpace commodity volumes, offering manufacturers stronger pricing power and long-term growth opportunities.

ETHYLENE VINYL ACETATE MARKET TRENDS:

Momentum toward Circularity and Low-Carbon EVA to Propel Market Growth

Circular and low-carbon EVA is gaining traction as brands and converters seek materials that reduce emissions without compromising product performance. Buyers in sectors such as footwear, packaging, and solar are incorporating carbon and recycling criteria into their tenders and rewarding suppliers that can demonstrate lower footprints and credible end-of-life pathways. Moreover, the use of EVA derived from renewable resources, such as sugarcane, is gaining popularity. This transition helps reduce dependency on fossil fuels, appealing to environmentally conscious consumers and brands that aim to meet their sustainability goals. As governments implement stricter regulations on plastic waste and set higher recycling targets, companies that excel in circular EVA solutions can gain a competitive edge and benefit from government incentives. For example, the EU's Circular Economy Action Plan and mandates, such as Extended Producer Responsibility (EPR), are strong motivators for this transition. Products that include recycled or bio-based EVA can be marketed with a "green premium" that customers increasingly value. Therefore, the shift toward circular and low-carbon EVA is expected to propel the Ethylene Vinyl Acetate (EVA) market growth over the forecast period.

Download Free sample to learn more about this report.

Segmentation Analysis

By Grade

High Density Segment Led the Market due to its Properties

On the basis of grade, the market is classified into low density, medium density, and high density.

The high density segment dominated the global ethylene vinyl acetate market share in 2024 due to its superior strength, higher stiffness, and enhanced thermal stability. These properties make it the preferred grade for solar PV encapsulants, durable foams, multilayer packaging, and high-performance industrial components. The solar photovoltaic sector is the largest demand center for high-density EVA, as it delivers strong cross-linking capability, UV resistance, and long-term reliability in module lamination. Its growing dominance reflects accelerating solar installations, rising demand for robust industrial materials, and advancements in EVA modification technologies supporting high-performance formulations.

Medium-density EVA offers a balanced combination of toughness, processability, and mechanical strength. This grade is commonly used in injection-molded parts, wire & cable insulation, cross-linked foams, and certain solar encapsulant structures. Medium-density EVA is increasingly adopted in athletic footwear, automotive interiors, and industrial adhesives due to its blend of elasticity and structural rigidity. Its demand trajectory is supported by expanding infrastructure electrification, cable manufacturing, and growth in sports and leisure products.

Low-density EVA is primarily valued for its superior flexibility, clarity, and resilience. Its lower crystallinity and softness make it ideal for applications requiring high elasticity and transparency, such as film extrusion, hot melt adhesives, and foamed products. In packaging, low-density EVA is widely used for stretch and shrink films, food packaging layers, and sealing applications. The demand for low-density EVA is driven by the growth of flexible packaging, footwear midsoles, and low-temperature adhesive formulations in emerging markets.

By Application

Foams Segment DominatedDue to its Properties

Based on application, the market is segmented into films, adhesives, foams, solar cell encapsulation, and others.

The foams segment held the largest global ethylene vinyl acetate market share in 2024 due to the EVA’s cushioning, shock absorption, and lightweight properties. These foams are used in the midsoles of footwear, sports equipment, automotive interiors, and packaging inserts. The footwear industry remains the major driver, particularly in Asia. Growing demand for comfort materials, fitness products, and impact-resistant packaging continues to strengthen this segment.

To know how our report can help streamline your business, Speak to Analyst

The solar cell encapsulation segment is poised to expand rapidly during the forecast period due to the surging demand for solar energy, where EVA is proven to be the critical material in the production of solar PV modules due to its excellent transparency and UV resistance. EVA sheets protect cells from moisture, mechanical stress, and weathering, making them essential in crystalline silicon PV modules. Strong growth in solar installations across China, India, Europe, and the U.S. will further stimulate demand for encapsulant-grade EVA.

Adhesives represent a small share of the EVA market, yet remain an important consumer in the global market. EVA’s strong bonding ability, low VOC profile, and compatibility with various substrates make it suitable for a wide range of applications. Hot-melt adhesives based on EVA are extensively used in packaging, bookbinding, hygiene products, and woodworking. Rising consumption of e-commerce packaging, disposable hygiene goods, and low-cost industrial adhesives supports steady demand for this segment.

The "others" category (8.9%) includes wire & cable compounds, injection-molded items, medical products, and sealants. These applications benefit from EVA’s flexibility, insulating properties, and chemical resistance. Growth in electrical infrastructure, consumer goods manufacturing, and healthcare packaging contributes to stable demand across these niche segments.

Ethylene Vinyl Acetate Market Regional Outlook

Asia Pacific Ethylene Vinyl Acetate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

The Asia Pacific held the largest market share in 2024, valued at USD 4.18 billion, and is expected to continue leading the regional share in 2025. Demand is driven by large-scale manufacturing, abundant feedstock availability, and rapidly expanding end-use industries. Countries such as China, India, South Korea, Japan, and those in Southeast Asia contribute significantly due to growing demand for adhesives, foams, and electrical applications. Rapid urbanization, population growth, and the expansion of e-commerce are driving strong demand for EVA films and hot-melt adhesives. Substantial investment in solar module production and the regional integration of EVA supply chains further reinforce Asia Pacific’s leadership.

In 2025, the China market is estimated to reach USD 2.31 billion. China is identified as the largest consumer in the region, supported by its massive solar PV industry, footwear manufacturing hubs, and packaging industry.

- China dominates the global EVA market, serving as both the largest producer and consumer. The market's immense size is driven by two primary sectors: the PV (Photovoltaic) industry and general manufacturing. China's aggressive renewable energy targets and heavy investment in solar farm construction create demand for vast quantities of EVA films for solar panel encapsulation.

To know how our report can help streamline your business, Speak to Analyst

Europe contributes a notable share of the global EVA market, led by demand from packaging films, industrial adhesives, and renewable energy applications. Countries such as Germany, Italy, and Spain exhibit strong adoption of EVA-based solar encapsulants due to supportive clean energy policies. The region also witnesses significant demand for footwear, wire & cable insulation, and high-performance foams used in sports and automotive applications. Continued investment in solar capacity, sustainable packaging formats, and higher-value specialty EVA products supports stable demand across Europe.

North America is projected to grow moderately during the forecast period, driven by strong demand from the packaging, footwear, solar energy, and industrial adhesives sectors. The U.S. leads regional consumption due to its mature manufacturing base and the expansion of solar PV installations, particularly in utility-scale projects. Growth in flexible packaging, hot-melt adhesives for e-commerce, and specialty foams used in sports and medical products continues to drive EVA usage. Regional availability of ethylene feedstock and stable manufacturing infrastructure also support competitive EVA production in the U.S. and Canada.

The Latin America and Middle East & Africa regions would witness a moderate growth in the market during the forecast period. Latin America’s key major application areas include footwear manufacturing, packaging films, and hot-melt adhesives for consumer goods. Solar PV adoption is gradually increasing across Chile, Brazil, and Mexico, supporting the use of EVA encapsulants. Growth in food packaging, construction adhesives, and consumer product manufacturing contributes to steady market expansion.

The Middle East benefits from competitive petrochemical feedstock, supporting EVA production capacity in countries such as Saudi Arabia. Growth in construction, electrical infrastructure, and consumer goods manufacturing boosts demand for adhesives and insulation-grade EVA. In Africa, rising urbanization and increasing FMCG consumption are driving the demand for packaging film applications.

COMPETITIVE LANDSCAPE

Key Industry Players:

Scaling Production and Expansion Initiatives are Essential Aspects for the Growth of Companies Operating in the Market

The global EVA market is moderately consolidated, with competition driven by production capacity, vinyl acetate integration, and strong regional distribution networks. Key players include ExxonMobil, Dow, LG Chem, Formosa Plastics, Hanwha Solutions, and Asia Polymer Corp (APC), each focusing on differentiated EVA grades for films, foams, adhesives, and solar encapsulation. Asian producers, particularly in China and South Korea, continue to expand their capacity to meet the rising regional demand for solar and packaging. Innovation in high-density and encapsulant-grade EVA, process optimization, and the development of bio-based feedstocks are key competitive strategies. Partnerships with solar module manufacturers and converters are also shaping long-term competitiveness in the market.

LIST OF KEY ETHYLENE VINYL ACETATE COMPANIES PROFILED:

- Asia Polymer Corporation (Taiwan)

- BASF-YPC Company Limited (China)

- Borealis GmbH (Austria)

- Braskem (Brazil)

- Celanese Corporation (U.S.)

- Dow, Inc. (U.S.)

- ExxonMobil Corporation (U.S.)

- Hanwha Solutions Chemical Division Corporation (South Korea)

- Henan Jinhe Industry Co., Ltd. (China)

- LG Chem (South Korea)

- LyondellBasell Industries Holdings B.V. (Netherlands)

- Repsol (Spain)

- SABIC (Saudi Arabia)

- Shandong Pulisi Chemical Group (China)

- Sumitomo Chemical (Japan)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: Borealis launched a renewables-based EVA solution for footwear midsoles. This new grade is part of Borealis' Bornewables portfolio, which is made from waste and residue streams, offering a 45% lower carbon footprint compared to fossil-based alternatives.

- May 2024: Sumitomo Chemical announced a collaboration agreement with Lummus Technology, a global provider of process technologies and value-driven energy solutions. Under this collaboration, Lummus Technology would serve as the exclusive global licensor, leveraging its marketing reach and engineering expertise to distribute Sumitomo's technology.

- October 2023: Braskem partnered with bioplastics specialist FKuR Kunststoff GmbH to distribute its bio-based EVA in several European countries, and Switzerland, the U.K., Turkey, and India. This expands the market reach for Braskem's sugarcane-based EVA plastics.

- September 2023: Repsol launched what it claims is the first range of 100% circular EVA copolymers using chemically recycled vinyl acetate (VA). Marketed under the Repsol Reciclex® brand, the product is certified under the ISCC Plus mass balance standard.

- June 2023: BASF-YPC announced plans to build a new EVA manufacturing unit at its Nanjing site with an annual production capacity of 300 Kilotons. The expansion is planned to meet the growing demand for high-quality EVA in China, particularly in high-growth segments such as the photovoltaic (solar) market.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size and forecast by all segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2019-2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Period | 2019-2023 |

| Growth Rate | CAGR of 4.4% from 2025-2032 |

| Unit | Value (USD Billion) and Volume (Kiloton) |

| Segmentation | By Grade, Application, and Region |

| By Grade |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 7.19 billion in 2024 and is projected to reach USD 10.10 billion by 2032.

In 2024, the market value stood at USD 4.18 billion.

The market is expected to exhibit a CAGR of 4.4% during the forecast period (2025-2032).

The high density segment led the market by grade.

The key factors driving the market are the rising demand for solar PV encapsulants, foams, and adhesives due to excellent performance across these application areas.

ExxonMobil, Dow, LG Chem, Formosa Plastics, Hanwha Solutions, and Asia Polymer Corp (APC) are some of the prominent players in the market.

Asia Pacific dominated the market in 2024.

An increased focus on solar energy and high-performance grades of ethylene vinyl acetate will favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 278

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us