Europe Thermoplastic Polyurethane Market Size, Share & Industry Analysis, By Type (Polyester, Polyether, Polycaprolactone, and Others), By Application (Automotive, Construction, Engineering, Footwear, Hose & Tubing, Wire & Cable, Medical, Synthetic Leather, and Others), and Regional Forecast, 2026-2034

Europe Thermoplastic Polyurethane Market Size and Future Outlook

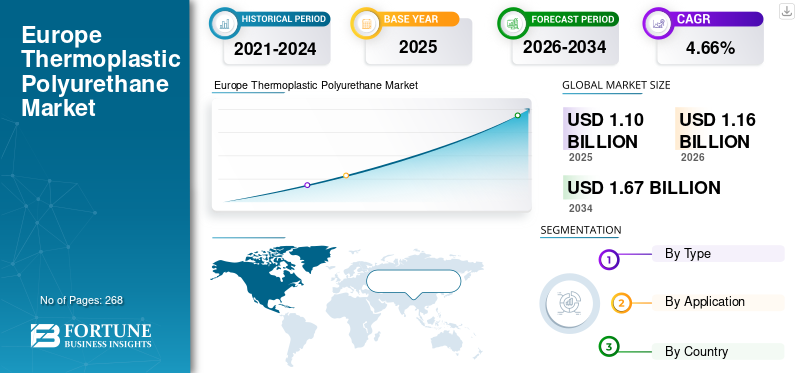

The Europe thermoplastic polyurethane market size was valued at USD 1.10 billion in 2025. The market is projected to grow from USD 1.16 billion in 2026 to USD 1.67 billion by 2034, exhibiting a CAGR of 4.66% during the forecast period.

Thermoplastic Polyurethane (TPU) is a thermoplastic elastomer produced by reacting diisocyanates with polyols and chain extenders to form a segmented polyurethane structure, thereby imparting a combination of elasticity as rubber and processability as plastic. As it softens upon heating and hardens upon cooling, it can be processed by methods such as extrusion, injection molding, and calendaring. This material exhibits notable properties, including abrasion resistance, toughness, flexibility, and strong adhesion to various substrates. Consequently, it is widely used in the manufacturing of automotive parts, footwear, hoses and tubing, cable jacketing, and specialized engineered components. In Europe, the TPU demand is shaped by high-value manufacturing and stringent performance requirements across automotive, engineering components, wire & cable jacketing, hose & tubing, footwear, medical, and specialty applications.

Furthermore, the market is dominated by several major players, including BASF SE, Covestro AG, The Lubrizol Corporation, Huntsman Corporation, and Wanhua Chemical, which are at the forefront. A broad portfolio, innovative product launches, and initiatives aimed at expanding geographical presence have supported the dominance of these companies in the European market.

Download Free sample to learn more about this report.

EUROPE THERMOPLASTIC POLYURETHANE MARKET TRENDS

Premiumization toward Engineered Grades and Circular-Ready Formulations

A prominent trend in Europe involves the ongoing transition from general-purpose thermoplastic polyurethane acquisitions to engineered grades specifically designed to meet end-use performance specifications, including abrasion and hydrolysis resistance, low-temperature flexibility, flame retardancy, process stability, and long-term compression set. This evolution facilitates higher average selling prices (ASPs) and promotes greater collaboration among resin manufacturers, compounders, and converters on formulation development, color/masterbatch application, and process optimization.

Concurrently, sustainability requirements are progressively integrated into commercial qualification processes, with increasing focus on circular-ready structures (mechanically recyclable formulations where feasible), mass-balance or bio-attributed feedstocks, and comprehensive documentation that supports customer ESG initiatives and regulatory reporting.

MARKET DYNAMICS

MARKET DRIVERS

Growth in Footwear and Performance Goods to Accelerate Adoption

The demand for footwear manufacturing and performance goods across Europe significantly sustains thermoplastic polyurethane consumption, as it provides abrasion resistance, flexibility, rebound, and design versatility for various components such as soles, midsoles, heel counters, overlays, and films/coatings. Brands are increasingly seeking materials that facilitate differentiated performance and aesthetics, including transparency, colorability, and tactile qualities, while ensuring durability in high-wear areas. Consequently, TPU remains a favored material in the performance footwear sector and select lifestyle categories.

Furthermore, the demand for durable sporting goods, protective equipment, and consumer products underpins TPU, attributable to comparable performance specifications, including tear resistance, flex fatigue resistance, and abrasion resistance. These adjacent industries frequently share converter capabilities and supply chains with the footwear sector, thereby enhancing material standardization and procurement efficiency for TPU grades. Consequently, the application scope of TPU extends beyond footwear into wider consumer and performance realms, thereby reinforcing fundamental demand. These factors are likely to drive the Europe thermoplastic polyurethane market growth.

MARKET RESTRAINTS

Price Volatility and Feedstock-linked Cost Pressure to Limit Volume Growth

TPU pricing is intricately linked to the upstream petrochemical and isocyanate value chains, which are susceptible to volatility driven by energy costs, supply chain disruptions, and cyclical demand fluctuations. A rapid increase in input costs may lead converters to experience margin pressure and pass these costs downstream, potentially resulting in decelerated order rates or temporary destocking. Consequently, intervals marked by significant raw material volatility can inhibit TPU consumption growth, even when end-use demand remains steady.

Thus, feedstock-driven cost fluctuations and procurement defensiveness establish a structural restraint on the smooth expansion of TPU volumes in Europe. Although the market retains growth potential, this growth increasingly relies on end-use performance stimuli and producers’ capacity to stabilize pricing through contractual agreements, supply security, and differentiation of value-added grades. Consequently, managing cost volatility remains a principal challenge for maintaining momentum in TPU volume expansion.

MARKET OPPORTUNITIES

Circularity and Compliance-driven Innovation to Open Premium Growth Lanes

Europe’s rising performance and sustainability expectations, along with the consumer demand for reduced environmental impact, present an opportunity for TPU suppliers to expand their offerings aligned with circular-economy principles, including recycled-content, mass-balance, and bio-attributed grades, which are technically feasible. As brands and OEMs articulate formal sustainability targets, they are increasingly seeking materials that support emissions-reduction narratives without compromising performance, particularly in footwear, automotive interiors, and consumer goods. Consequently, TPU producers who can provide verified circularity pathways and maintain consistent quality can access premium demand.

Furthermore, regulatory and customer demands can incentivize investments in recycling technologies and take-back initiatives for TPU-containing products, such as footwear components, industrial belts, and specific molded parts. Although mechanical recycling may be constrained by contamination and multi-material assemblies, targeted streams and enhanced sorting techniques can establish effective circular loops in certain applications. Consequently, the development of purpose-built circular systems can enhance TPU’s competitiveness and safeguard its market share from alternative materials

MARKET CHALLENGES

Feedstock Volatility, Energy Costs, and Compliance Complexity to Increase Operational Risk

The Europe TPU market faces significant challenges due to fluctuations in upstream feedstock and energy prices. These price variances impact manufacturers' cost structures and pricing strategies. Furthermore, stringent compliance requirements, such as detailed documentation, product stewardship, and customer audits, add operational complexity.

Effective freight and inventory management is also vital, as TPU demand varies across numerous stock-keeping units (SKUs) and converters, each with different lead-time needs. This complexity necessitates strategic logistics to ensure timely deliveries while minimizing excess inventory and costs, posing both challenges and opportunities for manufacturers in the TPU sector.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High Demand for Polyether owing to Superior Properties Contribute to Segmental Growth

Based on type, the market is segmented into polyester, polyether, polycaprolactone, and others.

The polyether segment accounted for the largest Europe thermoplastic polyurethane market share in 2025. Polyether TPU is primarily driven by applications requiring hydrolysis resistance, low-temperature flexibility, and long-term durability in humid or wet environments. There is a strong demand from sectors such as hose and tubing, outdoor goods, and specific medical and consumer applications, where performance stability is critical. The trends toward electrification and industrial maintenance further support the use of polyether TPU for protective, moisture-resistant, and flexible components. The market growth is closely linked to Europe’s high standards for reliability and warranties within industrial sectors. The level of competitive intensity remains lower than that of commodity grades, given the performance-critical nature of the specifications involved.

The polyester segment is expected to grow significantly at a CAGR of 4.35% during the forecast period. Polyester TPU is driven by the demand for high abrasion resistance, toughness, and oil- and solvent-resistance across various industrial and wear applications. There is significant demand from sectors such as footwear outsoles and components, engineered parts, and technical films and sheets, where durability is paramount. Additionally, automotive interior and exterior trims, as well as protective components, benefit from polyester TPU when mechanical strength is a key consideration.

By Application

To know how our report can help streamline your business, Speak to Analyst

Medical Segment to Grow at the Fastest CAGR due to Soaring Demand for Medical Devices and Consumables

In terms of application, the market is segmented into automotive, construction, engineering, footwear, hose & tubing, wire & cable, medical, synthetic leather, and others.

The medical segment is expected to grow at the fastest CAGR during the analysis period. The medical sector is driven by the rising demand for medical devices and consumables that require biocompatibility, cleanliness, flexibility, and reliable performance. TPU is employed in products such as tubing, catheters, films, and housings, where elastomeric properties and precise processing control are paramount. The demand within this sector demonstrates relative resilience compared to cyclical industrial markets. Growth is the most pronounced in regions near major medical device manufacturing hubs and among suppliers providing validated grades. While qualification cycles tend to be longer, customer retention rates are notably high. Furthermore, this segment is projected to grow at a CAGR of 5.97% over the study period.

The construction segment is expected to experience significant growth during the forecast period. Construction activities are driven by infrastructure refurbishment and the demand for durable materials in sealant-related systems, protective coatings, films, and waterproofing-associated applications, where TPU is selected. Growth correlates with projects that prioritize durability, flexibility, and resistance to weathering. TPU faces competition from lower-cost polymers. Consequently, its adoption is the most prevalent in applications that require toughness and extended service life. Furthermore, the construction segment accounted for a 5.47% market share in 2025. Additionally, it is projected that this segment will expand at a CAGR of 3.19% over the analysis period.

The automotive segment is also projected to grow moderately during the forecast period. Advancements in the automotive industry are driven by lightweight construction, enhanced durability, and greater design flexibility in interior surfaces, protective profiles, and functional components. The rise of electrification necessitates improved cable protection, abrasion-resistant jacketing, and resistance to vibration and impact. Original Equipment Manufacturer (OEM) qualification processes favor suppliers that provide consistent quality, comprehensive technical support, and reliable supply chains.

Europe Thermoplastic Polyurethane Market Regional Outlook

By country, the market is categorized into Germany, Italy, France, the U.K., Turkey, Spain, Belgium, Austria, the Czech Republic, Finland, Albania, the Netherlands, Poland, Sweden, Hungary, Romania, Russia, Switzerland, Portugal, Slovakia, Greece, and the rest of Europe.

Germany Thermoplastic Polyurethane Market

Germany held the dominant share in 2024, valued at USD 0.19 billion, and also led in 2025, with USD 0.20 billion. Germany's largest industrial base and automotive production footprint support TPU demand across automotive, engineering, wire and cable, and industrial components. A robust converter ecosystem facilitates rapid qualification and scale-up of specialty grades. Investments in electrification increase the demand for cable protection and technical parts. High standards for performance and durability underpin premium TPU formulations. In 2026, the Germany market is estimated to reach USD 0.21 billion.

To know how our report can help streamline your business, Speak to Analyst

Italy Thermoplastic Polyurethane Market

Italy is expected to see notable growth in the market in the coming years. During the forecast period, the European region is projected to grow at a 4.63% rate and reach a valuation of USD 0.12 billion in 2026. Italy is a prominent player in the footwear, fashion, leather goods, and industrial manufacturing sectors. The country supports the use of TPU in footwear components, synthetic leather, films, and engineered parts. The automotive and machinery industries drive the demand for abrasion-resistant, durable components. A significant number of medium-sized converters underscore the need for extensive grade portfolios and technical assistance. Premium consumer markets endorse specialized aesthetics and high performance. Circularity initiatives are gaining importance in branded applications.

France Thermoplastic Polyurethane Market

The French market is estimated to reach USD 0.12 billion in 2026, securing its position as the third-largest market. France's automotive supply chain, consumer goods, and aerospace-adjacent manufacturing support engineering TPU applications. A strong emphasis on sustainability and premium consumer markets supports higher-value grades in footwear, synthetic leather, and specialty films. Industrial hubs sustain the demand for hoses, tubing, and engineered parts. The healthcare and medical device sectors contribute to stable specialty consumption. Construction activity underpins some TPU usage in protective films and coatings. Overall, the product demand is diversified across various industrial and consumer end-use sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

Product Innovation and Recyclability are Key Strategies Influencing the Growth of Companies Operating in the Market

The European TPU market is characterized by structural fragmentation, with smaller manufacturers accounting for the majority of revenue. This signifies a long tail of regional compounders, distributors, and private-label suppliers, smaller importers, and niche processors that handle significant volumes, particularly in footwear, films and sheets, synthetic leather, and general-purpose industrial grades. The prominent market leaders include BASF SE, Covestro AG, The Lubrizol Corporation, Huntsman Corporation, and Wanhua Chemical. Product innovation and circularity-oriented solutions, such as recyclability pathways, recycled-content formulations, and lower-footprint grades, are becoming progressively central to supplier differentiation within Europe’s TPU market, especially in engineered applications that are subject to rigorous performance and sustainability standards.

LIST OF KEY EUROPE THERMOPLASTIC POLYURETHANE COMPANIES PROFILED

- BASF SE (Germany)

- Covestro AG (Germany)

- The Lubrizol Corporation (U.S.)

- Huntsman Corporation (U.S.)

- Wanhua Chemical (China)

- Ravago (Turkey)

- COIM Group (Italy)

- Epaflex Polyurethanes Spa (Italy)

- Expafol (Spain)

KEY INDUSTRY DEVELOPMENTS

- October 2024: BASF launched Elastollan 1400, a new ether-based thermoplastic polyurethane. The new TPU series integrates good compression set properties with stable processing behavior and offers exceptional microbial resistance and hydrolysis.

- February 2023: Covestro AG announced plans for the construction of its largest thermoplastic polyurethane production unit in Zhuhai, South China. The company plans to complete the expansion in three phases, with the first phase scheduled for late 2025. After completion, the plant is anticipated to have a total manufacturing capacity of 20,000 tons of TPU per year.

- August 2022: The Lubrizol Corporation announced a new thermoplastic polyurethane (TPU) line at the Shanghai Songjiang Site. The new production line is intended to enhance the company's TPU production capacity and strengthen its business in Asia Pacific.

- May 2022: Huntsman, in close collaboration with BRUGG Pipes, developed a next-generation polyurethane foam system with excellent insulation properties that can be used for the creation of thermally efficient, highly flexible, pre-insulated pipes for connecting local heating units and ground source heat pumps to commercial and domestic buildings.

- September 2021: BASF collaborated with Hotter, a leading shoes manufacturing company, to provide its first expanded thermoplastic polyurethane (E-TPU) product called Infinergy (E-TPU) for the manufacturing of shoes, which offers exceptional cushioning and greater energy return. The move is anticipated to help the company in situations of market volatility.

- September 2021: Huntsman’s Polyurethanes and Performance Products divisions participated in the 63rd CPI’s (Center for the Polyurethanes Industry) 2021 Technical Conference. Topics covered included low-aldehyde catalysts for rigid and flexible polyurethane foams, sustainability in raw materials, and innovations in automotive seating.

REPORT COVERAGE

The Europe thermoplastic polyurethane market analysis provides an in-depth study of the market size & forecast across all market segments included in the report. It contains details on the market dynamics and market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also includes a detailed competitive landscape, with market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.66% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, Application, and Country |

| By Type |

|

| By Application |

|

| By Country |

|

Frequently Asked Questions

Fortune Business Insights estimates that the European market size was USD 1.10 billion in 2025 and is projected to reach USD 1.67 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 4.66% during the forecast period of 2026-2034.

The medical application segment is the fastest-growing segment in the market.

Germany held the highest market share in 2025.

The rising demand for footwear and performance goods, along with sustained TPU uptake, is a key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 268

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us