Fatty Methyl Ester Sulfonate Market Size, Share & Industry Analysis, By Application (Laundry Detergents, Dishwashing Detergents, Institutional & Industrial Cleaners, Personal Care & Specialty, and Others), and Regional Forecast, 2026-2034

FATTY METHYL ESTER SULFONATE MARKET SIZE AND FUTURE OUTLOOK

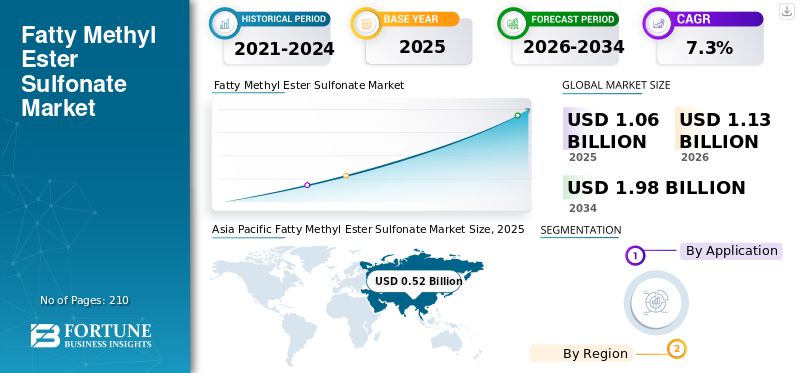

The global fatty methyl ester sulfonate market size was USD 1.06 billion in 2025. The market is projected to grow from USD 1.13 billion in 2026 to USD 1.98 billion by 2034 at a CAGR of 7.3% during the forecast period. Asia Pacific dominated the fatty methyl ester sulfonate market with a market share of 49.06% in 2025.

Fatty Methyl Ester Sulfonate (FMES) is a biodegradable anionic surfactant derived from sulfonated methyl esters of natural fatty acids, primarily sourced from palm or coconut oil. It serves as a sustainable alternative to petrochemical-based surfactants, offering excellent detergency, calcium hardness tolerance, and environmental compatibility. FMES is widely used in laundry detergents, dishwashing agents, and industrial cleaners, particularly in powder and bar formulations. A key demand driver is the global shift toward sustainable and bio-based ingredients, fueled by environmental regulations, corporate ESG commitments, and consumer preference for eco-friendly cleaning products that reduce reliance on fossil-derived chemicals. KLK Oleo, Wilmar International, Lion Corporation, Stepan Company, and Chemithon Enterprises are the few of the major player in the market.

Download Free sample to learn more about this report.

FATTY METHYL ESTER SULFONATE MARKET TRENDS

Sustainability Mandates Accelerate FMES Shift as LAS Faces Regulatory Pressure

Tightening global regulations on biodegradability and carbon footprint reduction are compelling detergent manufacturers to replace conventional petrochemical surfactants such as Linear Alkylbenzene Sulfonate (LAS) with bio-based alternatives such as FMES. Europe’s Detergents Regulation, the EU Green Deal, and U.S. EPA Safer Choice standards are creating a compliance-led transition to biodegradable surfactants. As a result, FMES, produced from renewable methyl esters, is becoming the preferred option in powder and bar formulations. This regulatory-driven trend is reshaping formulation strategies, especially in Europe and Asia, where environmental compliance and product eco-labeling are becoming core to product differentiation and export viability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Consumer Demand for Plant-Based Products Boosts Product Adoption in Mainstream Detergents

Growing global consumer preference for environmentally friendly, sulfate-free, and plant-based products is driving higher FMES inclusion in household and personal care segments. Brands are responding by reformulating detergent and personal care products to align with these expectations, with FMES delivering strong cleaning performance while supporting green marketing claims. The increasing demand is particularly strong in North America and Europe, where premium brands lead adoption. FMCG giants are scaling FMES use to meet corporate sustainability targets and tap into the "clean label" trend. This pull from downstream demand is reinforcing fatty methyl ester sulfonate market growth as a driver in surfactants.

MARKET RESTRAINTS

Volatile Palm Oil Supply Chains Raise Input Cost Risk for FMES Producers

The FMES industry remains heavily exposed to feedstock volatility, particularly fluctuations in palm oil and methyl ester prices. Geopolitical events, climate impacts, and trade restrictions, such as Indonesia's past export bans, have historically disrupted palm oil supply and driven price spikes. These cost surges directly affect FMES production economics, especially for small and non-integrated manufacturers. The inability to hedge raw material risks in emerging markets creates price instability across regions. As a result, FMES loses competitiveness against petroleum-based surfactants during feedstock surges, limiting its penetration in price-sensitive segments and delaying broader formulation conversion by cost-focused brands.

MARKET OPPORTUNITIES

Emerging Markets’ Detergent Boom Opens Scalable FMES Demand Pathway

Rising detergent consumption in emerging markets, particularly in Asia Pacific, Africa, and Latin America, is unlocking a significant volume-driven opportunity for FMES. Powder detergents and laundry bars, the formats where FMES excels, dominate these regions due to affordability and infrastructure constraints. As income levels rise and detergent usage increases, manufacturers are adopting FMES as a cost-effective, bio-based surfactant aligned with sustainability trends. Local oleochemical capacity, especially in Indonesia, India, and Brazil, further enhances the feasibility of scaling FMES use regionally. This volume growth potential is positioning FMES as a core ingredient in the next wave of affordable, high-performing cleaning products.

MARKET CHALLENGES

Solubility Limitations Constrain FMES Penetration in Liquid and Cold-Water Formats

Despite its strong performance in powders and bars, FMES faces technical challenges in liquid and low-temperature detergent applications due to poor solubility and cold-water clarity. These limitations restrict FMES use in premium liquid detergents, especially in mature markets such as North America and Europe, where liquid formats dominate. Formulators often require additional co-surfactants or solubilizers, raising formulation complexity and cost. While R&D is ongoing to improve FMES derivatives or blends, these constraints limit its versatility compared to ethoxylated surfactants such as SLES or AES. Overcoming these technical bottlenecks is critical for FMES to achieve broader functional parity and market penetration.

SEGMENTATION ANALYSIS

By Application

To know how our report can help streamline your business, Speak to Analyst

Laundry Detergents Regulatory Compliance and Powder Format Dominance Fuel Demand

Based on the application, the market is segmented into laundry detergents, dishwashing detergents, institutional & industrial cleaners, personal care & specialty, and others.

The laundry detergents segment is anticipated to hold the dominant fatty methyl ester sulfonate market share during the forecast period. In laundry detergents, FMES demand is driven by its superior detergency, biodegradability, and calcium hardness tolerance, making it ideal for powder and bar formats prevalent in Asia, Africa, and Latin America. Regulatory pressure to phase out non-biodegradable surfactants such as LAS is accelerating FMES adoption, especially in Europe. Its compatibility with enzymes and eco-label standards enables brands to reformulate for sustainability without compromising wash performance, positioning FMES as a key ingredient in the green laundry transition and driving market growth in tandem.

In personal care & specialty, FMES demand is rising due to the global shift toward sulfate-free and mild surfactant formulations in skin and hair care. Consumers increasingly seek plant-based, non-irritating ingredients, prompting brands to replace harsher surfactants such as SLS/SLES. FMES offers a renewable, biodegradable alternative with good foaming and cleansing properties. Its growing use in face washes, body cleansers, and premium personal care lines is fueled by clean-label positioning, allergen sensitivity trends, and compliance with natural cosmetic certifications.

The personal care & specialty segment is anticipated to rise with a CAGR of 7.9% over the forecast period.

FATTY METHYL ESTER SULFONATE MARKET REGIONAL OUTLOOK

By region, the market is segmented into Asia Pacific, North America, Europe, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Fatty Methyl Ester Sulfonate Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific region is expected to dominate the market during the forecast period. Asia Pacific leads FMES consumption globally, with laundry detergents, especially powders and bars, being the dominant driver. Countries such as China, India, and Indonesia rely heavily on FMES for cost-effective, high-foaming laundry formulations. Strong palm oil supply, domestic methyl ester production, and supportive government green chemistry initiatives create an ideal foundation for FMES scaling. Dishwashing detergents also show future growth potential, especially in India and Southeast Asia where bar formats are prominent. Rapid urbanization and eco-conscious middle-class consumption trends will reinforce FMES use across these cleaning categories.

Japan Fatty Methyl Ester Sulfonate Market

Japan’s market reached approximately USD 0.06 billion in 2025, equivalent to around 5.7% of global sales.

China Fatty Methyl Ester Sulfonate Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 0.21 billion, representing roughly 19.8% of global sales.

India Fatty Methyl Ester Sulfonate Market

India’s market reached approximately USD 0.14 billion in 2025, equivalent to around 13.2% of global sales.

North America

In North America fatty methyl ester sulfonate market, rising consumer preference for sulfate-free, plant-based products is the primary driver for FMES adoption, especially in personal care and premium liquid laundry detergents. Large brands are reformulating to meet EPA Safer Choice and clean-label criteria, which FMES satisfies due to its renewable origin and mild profile. While limited local FMES production constrains immediate supply, increased imports and partnerships with Asian suppliers are bridging the gap. FMES demand in dishwashing is growing as natural-positioned home care brands expand into biodegradable formats.

U.S. Fatty Methyl Ester Sulfonate Market

The U.S. market analytically approximated at around USD 0.10 billion in 2025, accounting for roughly 9.4% of global sales.

Europe

Europe’s stringent biodegradability and carbon footprint regulations are propelling FMES adoption, particularly in powder laundry detergents where it replaces LAS to meet EU Detergents Regulation requirements. Leading FMCG companies in France, Germany, and the Nordics have made FMES integral to their ESG-compliant product lines. The institutional cleaner segment is also adopting FMES, driven by EU-wide mandates for safer industrial chemicals. Continued expansion in sustainable personal care could further support FMES demand, especially as European consumers increasingly scrutinize surfactant origin and toxicity in daily-use products.

U.K. Fatty Methyl Ester Sulfonate Market

U.K.’s market reached approximately USD 0.05 billion in 2025, equivalent to around 4.7% of global share.

Germany Fatty Methyl Ester Sulfonate Market

Germany’s market reached approximately USD 0.07 billion in 2025, equivalent to around 6.6% of global sales.

Latin America

In Latin America fatty methyl ester sulfonate market, demand is primarily driven by affordable powder laundry detergents and laundry bars, where FMES offers an optimal cost-performance blend. Brazil and Mexico are leading markets due to detergent format preferences and increasing adoption of bio-based surfactants by local and multinational brands. The dishwashing segment, especially bar soaps, is also expanding FMES use due to its grease-cutting efficiency and foaming. As detergent penetration increases across the region’s emerging economies, FMES is poised to benefit from both volume growth and growing bio-based product positioning.

Brazil Fatty Methyl Ester Sulfonate Market

Brazil’s market reached approximately USD 0.04 billion in 2025, equivalent to around 3.8% of global product sales.

Middle East & Africa

In the Middle East & Africa, demand for FMES is growing rapidly, led by laundry detergents, following Saudi Arabia’s SASO regulation requiring biodegradable surfactants. This mandate has prompted regional detergent brands and importers to shift toward FMES to maintain market access. South Africa is also showing increased FMES integration in institutional cleaners and bar soap formats. As other Middle East & Africa countries adopt similar green standards or follow multinational reformulation trends, FMES demand is expected to rise steadily, supported by expanding import channels and regional awareness of environmental surfactants.

Saudi Arabia Fatty Methyl Ester Sulfonate Market

Saudi Arabia’s market reached approximately USD 0.03 billion in 2025, equivalent to around 2.8% of global product sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Asia’s Feedstock Advantage Reshapes Market as Top Producers Drive Global Scale and Specialization

The global fatty methyl ester sulfonate industry is moderately consolidated, with competition shaped by vertical integration, feedstock access, and regional distribution networks. Asian producers dominate due to proximity to palm oil and large-scale sulfonation capacity, while Western players focus on high-purity grades for premium applications. Innovation around powder handling, low-temperature solubility, and RSPO-certified sourcing differentiates key players. Strategic partnerships with FMCG brands and expansion in emerging markets are critical to long-term positioning. The top producers globally include KLK Oleo, Wilmar International, Lion Corporation, Stepan Company, and Chemithon Enterprises.

LIST OF KEY FATTY METHYL ESTER SULFONATE COMPANIES PROFILED

- KLK OLEO (Malaysia)

- Wilmar International Ltd (Singapore)

- Lion Corporation (Japan)

- Stepan Company (U.S.)

- Chemithon Corporation (U.S.)

- Ecogreen Oleochemicals (Singapore)

- Shanghai Kunruy Chemical Co., Ltd. (China)

- Guangzhou Zhonghai Chemical Co., Ltd. (China)

- Henan Jiahe Biotechnology Co., Ltd. (China)

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Volume (Kiloton); Value (USD Billion) |

| Growth Rate | CAGR of 7.3% during 2026-2034 |

| Segmentation | By Application, and Region |

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.06 billion in 2025 and is projected to record a valuation of USD 1.98 billion by 2034.

In 2025, Asia Pacific stood at USD 0.52 billion.

Registering a CAGR of 7.3%, the market will exhibit steady growth during the forecast period.

The laundry detergents application is expected to lead this market during the forecast period.

The consumer demand for plant-based products boosts product adoption in mainstream detergents to drive market growth.

KLK Oleo, Wilmar International, Lion Corporation, Stepan Company, and Chemithon Enterprises are the major players operating in the market.

Asia Pacific dominated the market in terms of share in 2025.

Sustainability mandates accelerate FMES shift as LAS faces regulatory pressure creating market growth opportunities.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us