Fine Chemicals Market Size, Share & Industry Analysis, By Supply Structure (Captive and Merchant), By Application (Pharmaceuticals, Agrochemicals, Flavors & Fragrances, Pigments & Dyes, Electronics, and Others) and Regional Forecast, 2026-2034

FINE CHEMICALS MARKET SIZE AND FUTURE OUTLOOK

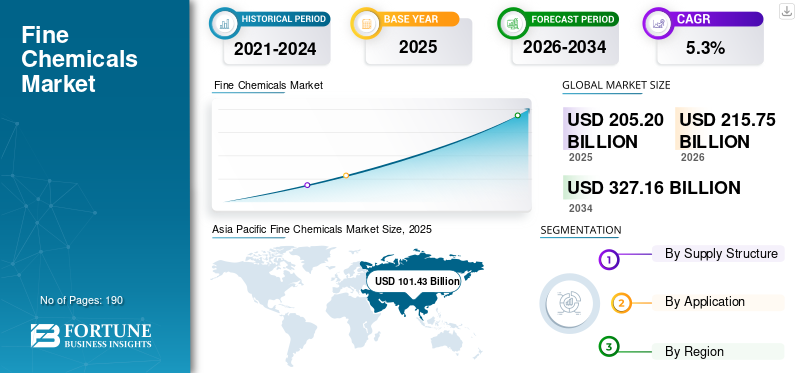

The global fine chemicals market size was USD 205.20 billion in 2025. The market is projected to grow from USD 215.75 billion in 2026 to USD 327.16 billion by 2034 at a CAGR of 5.3% during the forecast period. Asia Pacific dominated the fine chemicals market with a market share of 49.43% in 2025.

Fine chemicals are high-purity, complex chemical substances produced in relatively low volumes for specific end uses, typically through multi-step synthesis under tight quality control standards. They are usually sold as single, well-defined molecules rather than broad formulations and are widely used in pharmaceuticals, agrochemicals, flavors and fragrances, pigments, and electronic chemicals. Unlike commodity chemicals, their value is driven by purity, performance, and technical complexity rather than production scale. One of the major drivers is the growth of the pharmaceutical industry, as rising drug development activities, API manufacturing, and outsourcing of custom synthesis continue to increase demand for high specification fine chemical intermediates and active pharmaceutical ingredients.

WuXi STA, Asymchem Inc., Siegfried Holding AG, Divi's Laboratories Limited, and Lonza are the key players operating in the market.

Download Free sample to learn more about this report.

FINE CHEMICALS MARKET TRENDS

Smarter and Greener Manufacturing to Fuel Industry Growth

A major global trend in fine chemicals is the move toward smarter, cleaner, and more flexible manufacturing processes. Producers are increasingly improving process design, automation, data visibility, and quality control systems to improve yields, reduce waste, and shorten development cycles. There is also a growing shift toward green chemistry, continuous processing, and more selective synthesis routes. This trend is further reinforced by customer expectations for reliability, traceability, and sustainability. As a result, fine chemical companies are no longer competing only on cost or chemistry capability; they are also competing on operational agility, process efficiency, environmental performance, and speed-to-market.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Dependency on Specialized Partners for High-Purity Intermediates to Fuel Market Growth

A prominent driver for the industry is the continued growth of pharmaceutical innovation and outsourced manufacturing. As drug molecules become more complex and development timelines become more demanding, pharmaceutical companies increasingly rely on specialized partners for high-purity intermediates, custom synthesis, and advanced manufacturing support. This expands demand for the product with stringent quality and performance requirements. In parallel, healthcare needs continue to grow across developed and emerging markets, supporting long-term demand for active ingredients and their upstream intermediates, boosting fine chemicals market growth.

MARKET RESTRAINTS

Tighter Profitability Margins to Restrain Market Growth

A major restraint in the market is the growing pressure from high operating costs and tighter profitability margins. Energy, raw materials, compliance, labor, and capital investments have become more demanding, especially in regions with stricter regulatory and environmental standards. At the same time, customers remain highly price-sensitive in non-differentiated product categories, which limits the ability of suppliers to fully pass on cost increases. This creates pressure on profit margins and slows capacity expansion decisions. Even when demand remains healthy, producers may hesitate to scale operations aggressively if returns are uncertain, making cost competitiveness a critical constraint on market growth.

MARKET OPPORTUNITIES

High Demand for Purity Chemicals to Create Several Growth Opportunities

A major opportunity for the market lies in the expanding demand for high-purity chemicals used in electronics and advanced materials applications. Semiconductor fabrication, display technologies, energy storage, and other precision industries require chemicals with extremely tight purity, consistency, and performance specifications. These applications offer attractive growth potential as they reward technical expertise, quality assurance, and long-term customer qualification rather than just scale alone. For fine chemical manufacturers, this creates a pathway to diversify beyond traditional pharmaceutical and agrochemical markets. Companies that can develop strong positions in electronic-grade and other high specification specialty segments are likely to capture premium-margin growth during the forecast period.

MARKET CHALLENGES

Concentrated Supply Chains to Limit Market Growth

One of the challenges facing the market is the concentration of supply chains across a limited number of countries, suppliers, and production hubs. While global specialization has improved cost efficiency, it has also increased vulnerability to geopolitical disruptions, logistics shocks, regulatory shifts, and raw-material shortages. Customers are now demanding quality and price competitiveness, along with resilience and supply security. This is forcing producers to rethink sourcing strategies, inventory models, and manufacturing footprints. The challenge is no longer limited to producing efficiently; it now involves building supply networks that are reliable, diversified, compliant, and resilient under changing market conditions.

SEGMENTATION ANALYSIS

By Supply Structure

Captive Segment to Lead due to Need for Greater Control Over Quality

Based on supply structure, the market is segmented into captive and merchant.

The captive segment is anticipated to hold the dominant fine chemicals market share during the forecast period. A major factor driving demand in the segment is the need for greater control over quality, supply continuity, and intellectual property. In industries such as pharmaceuticals and agrochemicals, producers increasingly prefer in-house fine chemical manufacturing for critical intermediates to reduce dependence on external suppliers and manage regulatory risk more effectively. Captive production also helps improve coordination across the value chain, optimize costs for strategic molecules, and ensure consistent product specifications, especially where reliability, confidentiality, and process control are central to competitiveness.

The merchant segment is anticipated to rise with a CAGR of 5.8% over the forecast period. Demand in the merchant segment is growing due to preference for outsourcing specialized fine chemical production to external manufacturers. Customers seek merchant suppliers to access complex chemistry capabilities, flexible capacity, and faster scale-up without making heavy capital investments. This model allows companies to remain asset-light while focusing on core activities such as research, formulation, and commercialization. As product complexity rises and supply chains globalize, demand for reliable third-party partners continues to strengthen segment growth.

By Application

To know how our report can help streamline your business, Speak to Analyst

Pharmaceuticals Segment to Dominate due to Rising Complexity of Drug Development

Based on application, the market is segmented into pharmaceuticals, agrochemicals, flavors & fragrances, pigments & dyes, electronics, and others.

The pharmaceuticals segment is anticipated to hold the dominant fine chemicals market share during the forecast period. A major factor driving demand in the segment is the increasing complexity of drug development and manufacturing. As new therapies require high-purity intermediates, specialized synthesis routes, and tighter regulatory compliance, pharmaceutical companies depend on sophisticated fine chemicals to support production. Demand is further reinforced by the growing preference for reliable, high specification inputs that ensure product consistency and process control. This makes fine chemicals essential for the efficient development and large-scale manufacturing of advanced pharmaceutical ingredients.

The electronics segment is anticipated to rise with a CAGR of 7.9% over the forecast period. Demand in the segment is due to the rising need for ultra-high-purity chemicals in semiconductor and advanced electronic manufacturing. As devices become smaller, more powerful, and more complex, manufacturers require fine chemicals with extremely tight impurity control and consistent performance. These materials are critical in processes such as etching, cleaning, deposition, and photoresist formulation. The push toward advanced chips, displays, and electronic components, therefore, continues to increase demand for precision-engineered fine chemicals that can meet exacting technical and quality standards.

FINE CHEMICALS MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Fine Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounts for the largest market share and is expected to maintain its dominance during the forecast period. In the region, pharmaceuticals remain the core driver of product demand, while the electronic industry serves as a powerful supporting application segment. The region benefits from growing healthcare demand, expanding manufacturing capabilities, and strong participation in fine chemical intermediates and active ingredient production. At the same time, the rapid growth of the electronics industry is increasing demand for high-purity and performance-sensitive chemicals used in advanced manufacturing processes. This combination gives the region a broad and dynamic demand base. Pharmaceuticals provide the foundation of market demand, while electronics strengthen future growth by increasing the need for technically advanced and highly consistent fine chemical inputs.

Japan Fine Chemicals Market

Japan’s market reached approximately USD 7.24 billion in 2025, equivalent to around 3.5% of global sales.

China Fine Chemicals Market

China’s market is projected to be one of the largest worldwide, with 2025 revenues standing at around USD 59.08 billion, representing roughly 28.8% of global sales.

India Fine Chemicals Market

India’s market reached approximately USD 11.97 billion in 2025, equivalent to around 5.8% of global sales.

North America

In North America, pharmaceuticals remain the key driver of product demand. The region’s strong focus on innovative drug development, complex therapies, and specialized manufacturing continues to create a sustained need for high-purity intermediates and custom synthesis capabilities. Fine chemicals are essential to ensuring product consistency, regulatory compliance, and efficient scale-up of advanced molecules. The electronic sector also contributes to demand, particularly in high-specification materials; however, pharmaceuticals remain the dominant application as they generate the strongest pull for technically sophisticated and high-value fine chemical inputs across the region.

U.S. Fine Chemicals Market

The U.S. market stood at around USD 44.42 billion in 2025, accounting for roughly 21.6% of global sales.

Europe

In Europe, pharmaceuticals are the primary driver of product demand, supported by the region’s deep expertise in complex synthesis, quality-focused manufacturing, and highly specialized chemical capabilities. Demand is reinforced by the need for reliable intermediates and advanced ingredients used in regulated healthcare applications. In addition, flavors and fragrances provide meaningful support due to Europe’s long-standing legacy in specialty chemicals development and premium formulation. Together, these applications position Europe as a key region in the market driven by technical sophistication, product quality, and high-value end-use applications rather than production scale alone.

U.K. Fine Chemicals Market

The U.K.’s market reached approximately USD 3.53 billion in 2025, equivalent to around 1.7% of global sales.

Germany Fine Chemicals Market

Germany’s market reached approximately USD 10.58 billion in 2025, equivalent to around 5.2% of global sales.

Latin America

In Latin America, agrochemicals are the main driver of product demand. The region’s agricultural emphasis creates a strong need for crop-protection intermediates and related specialty chemical inputs, making agrochemicals the most immediate and structurally important application segment. Pharmaceuticals provide additional support as healthcare demand gradually expands; however, they are not yet the principal force behind market consumption. As a result, product demand in Latin America is shaped primarily by agricultural productivity needs, with pharmaceuticals acting as a secondary contributor that can strengthen the market over the longer term.

Brazil Fine Chemicals Market

Brazil’s market reached approximately USD 5.32 billion in 2025, equivalent to around 2.6% of global sales.

Middle East & Africa

In the Middle East and Africa, agrochemicals remain the leading driver of product demand as agricultural productivity, food security, and crop protection remain critical priorities across much of the region. This creates a steady need for fine chemical inputs linked to farming and agricultural performance. Pharmaceuticals serve as the most important supporting application, particularly as healthcare systems expand and several countries seek to strengthen local manufacturing capabilities. While pharmaceuticals can become a stronger long-term contributor, agrochemicals remain the primary demand anchor shaping the region’s fine chemicals consumption profile.

Saudi Arabia Fine Chemicals Market

Saudi Arabia’s market reached approximately USD 2.45 billion in 2025, equivalent to around 1.2% of global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Payers Focus on Long-Term Customer Relationships to Gain Competitive Edge

The global fine chemicals industry is highly fragmented; however, competition is increasingly concentrated among a group of large, technically advanced manufacturers with strong regulatory, process development, and custom manufacturing infrastructure. The competitive landscape is shaped by expertise in complex synthesis, high-purity production, reliable scale-up, and long-term customer relationships rather than by commodity-style scale alone. Companies with strong positions in pharmaceuticals, agrochemicals, and high specification specialty applications maintain a competitive advantage. Asia continues to serve as a key production base due to its manufacturing scale and Europe retains leadership in high-value, compliance-driven specialty chemical segments. Key players include WuXi STA, Asymchem Inc., Siegfried Holding AG, Divi's Laboratories Limited, and Lonza.

LIST OF KEY FINE CHEMICALS COMPANIES PROFILED

- WuXi STA (China)

- Asymchem Inc. (China)

- Siegfried Holding AG (Switzerland)

- Divi's Laboratories Limited (India)

- Lonza (India)

- Piramal Pharma Solutions (U.S.)

- Laurus Labs Limited (India)

- CordenPharma (Switzerland)

- Cambrex Corporation (U.S.)

- HIKAL Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- March 2026: CordenPharma Colorado signed a 15-year lease with BioMed Realty for a 64,000-square-foot peptide development lab at Flatiron Park, Boulder. The new facility would strengthen process development and analytical capabilities, supporting rising demand for complex peptide outsourcing and expanding CordenPharma’s integrated global peptide network.

- October 2025: Cambrex announced a USD 120 million investment to expand its U.S. manufacturing footprint, led by a 40% capacity increase at its Charles City, Iowa facility. The move supports rising demand for domestic API production and strengthens Cambrex’s position in the growing peptide therapeutics market.

- October 2025: Hikal opened a cGMP-compliant HPAPI Laboratory at its Pune Integrated Innovation Centre to strengthen its CDMO offering. Built to OEB-5 standards, the facility would support development of potent oncology and specialty molecules, including ADC, PDC, and PROTAC components, for global pharmaceutical customers.

- December 2023: Piramal Pharma Solutions inaugurated its expanded ADC facility in Grangemouth, Scotland. The investment boosts production capacity by up to 80%, adds new manufacturing suites, and creates 40–50 jobs, strengthening end-to-end drug development capabilities amid rising global demand for ADC therapies.

- February 2021: WuXi STA completed the acquisition of Bristol Myers Squibb’s drug product manufacturing facility in Couvet, Switzerland, strengthening its presence in Europe. The state-of-the-art site, opened in 2018, adds tablet, capsule, and packaging capacity, improving supply flexibility for global customers. With this addition, WuXi STA now operates eight R&D and manufacturing sites across Asia, North America, and Europe, supporting broader access to major global markets.

- January 2021: Siegfried completed its acquisition of two Novartis pharmaceutical manufacturing sites near Barcelona. The deal strengthens Siegfried’s drug product capabilities, expands its global network to 11 sites, and deepens its strategic partnership with Novartis through long-term supply and integration agreements.

REPORT COVERAGE

The global market report provides a detailed analysis of the market. It focuses on key aspects such as profiles of leading companies, product types, and leading applications of the product. Besides this, it offers insights into the analysis of key market trends and highlights key industry developments. In addition to the aforementioned factors, it encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Historical Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 5.3% from 2026 to 2034 |

| Segmentation | By Supply Structure, By Application, and By Geography |

| By Supply Structure |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 205.20 billion in 2025 and is projected to record a valuation of USD 327.16 billion by 2034.

In 2025, Asia Pacific stood at USD 101.43 billion.

Registering a CAGR of 5.3%, the market will exhibit steady growth during the forecast period.

By application, the pharmaceuticals segment is expected to lead this market during the forecast period.

Rising dependency on specialized partners for high-purity intermediates is a key factor driving the market.

WuXi STA, Asymchem Inc., Siegfried Holding AG, Divi's Laboratories Limited, and Lonza are the major players operating in the market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us