Cosmetic Chemicals Market Size, Share & Industry Analysis, By Type (Surfactants, Emollients & Moisturizers, Preservatives, and Others), By Application (Skincare, Haircare, Oral Care, Makeup, and Others), and Regional Forecast, 2026-2034

Cosmetic Chemicals Market Size and Future Outlook

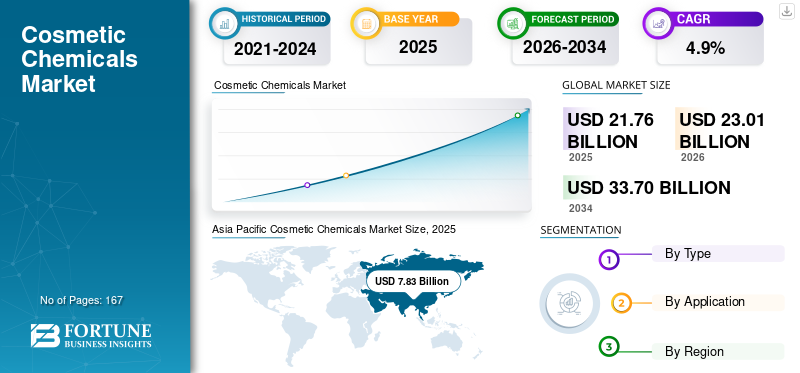

The global cosmetic chemicals market size was valued at USD 21.76 billion in 2025. The market is projected to grow from USD 23.01 billion in 2026 to USD 33.70 billion by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the cosmetic chemicals market with a market share of 35.98% in 2025.

Cosmetic chemicals are specialized ingredients employed in personal care and beauty formulations to provide cleansing, conditioning, preservation, moisturization, emulsification, sensory enhancement, coloration, UV protection, and performance improvements. Practically, the market encompasses surfactants, emollients and moisturizers, preservatives, as well as an extensive range of other components, including rheology modifiers, conditioning polymers, active ingredients, UV filters, color agents, and formulation auxiliaries. The demand for these substances is driven by increasing product complexity, expedited formulation cycles, the proliferation of “clean” and high-efficacy beauty formats, and more intensive ingredient incorporation in premium skincare, scalp care, sun care, and multifunctional cosmetic systems.

Furthermore, the market is characterized by the dominance of several major specialty-ingredient suppliers, including BASF, Croda, Symrise, Clariant, Evonik, and DSM-Firmenich. These entities benefit from extensive formulation portfolios, robust application laboratories, regulatory support, and international customer relationships. Croda emphasizes its comprehensive Consumer Care offerings and its substantial product and customer base, while Symrise positions itself as a global provider of cosmetic active ingredients and raw materials, emphasizing the significance of innovation depth and collaborative development with clients.

Download Free sample to learn more about this report.

COSMETIC CHEMICALS MARKET Key Takeaways

- 2025 Market Size: USD 21.76 Billion

- 2026 Market Size: USD 23.01 Billion

- 2034 Forecast Market Size: USD 33.70 Billion

- CAGR: 4.9% from 2026–2034

- Asia Pacific dominated the cosmetic chemicals market with a 35.98% share in 2025.

- The surfactants segment held the largest market share in 2025.

- The skincare segment accounted for 40.7% of the global market share in 2025.

Asia Pacific

Asia Pacific led the global market with a valuation of USD 7.83 billion in 2025.

Europe

Europe is projected to reach USD 5.16 billion in 2026, driven by premium skincare demand.

Latin America

Latin America is projected to reach USD 1.96 billion in 2026, driven by beauty product demand.

U.S.

The cosmetic chemicals market is projected to reach USD 5.38 billion by 2026.

Japan

The cosmetic chemicals market is estimated to reach USD 1.26 billion by 2026.

Read More

COSMETIC CHEMICALS MARKET TRENDS

Usage of Biotechnology, Clean Formulation, and Multifunctionality Are Reshaping Ingredient Demand

A significant development within the market is the shift from traditional commodity formulation systems to biotechnology-derived, multifunctional ingredients that emphasize sustainability. Suppliers are progressively introducing ingredients that integrate efficacy with natural-origin attributes, enhanced biodegradability, reduced formulation complexity, and stronger substantiation for claims. This trend is particularly evident in areas such as skin barrier support, scalp and hair health, microbiome-friendly preservation, and sensory systems capable of providing multiple benefits within a single ingredient platform.

The trend is reinforced by shifting end-market demand. L’Oréal’s 2024 analysis of the beauty industry highlights the resilience of premium beauty and the sustained prominence of science-backed segments. Additionally, Cosmetics Europe’s 2024 data indicate that Europe alone achieved retail sales of USD 120 billion in cosmetics and personal care, with skin care and toiletries representing some of the largest categories. This trend underscores the ongoing commitment to investing in higher-value ingredients rather than solely pursuing volume-driven growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Usage of Premium Skincare and Ingredient-Led Innovation Are Accelerating Ingredient Consumption

The cosmetic chemicals market growth is driven by the ongoing expansion of the broader beauty and personal care sector, particularly in skincare, premium haircare, dermocosmetics, and fragrance-related formats. As product claims become increasingly specific and consumer expectations elevate regarding texture, efficacy, gentleness, and transparency, formulators are employing more specialized surfactants, sensory emollients, preservation systems, and active-support ingredients. This trend is contributing to an increase in both the number of ingredients in each formulation and the value added by specialty chemicals in finished products.

Macro demand signals support this trajectory. The Personal Care Products Council describes the global beauty and personal care industry as a USD 535.7 billion market, while Cosmetics Europe reports major 2024 market sizes of USD 107 billion, China’s value accounts for USD 65 billion, Japan’s market value accounts for USD 25 billion, Brazil exhibits a value of USD 27 billion, and India accounts for USD 15 billion, demonstrating that both mature and emerging markets provide a substantial consumption base for specialty cosmetic ingredients. Consequently, the demand for ingredients is increasing not only due to higher sales of beauty products but also through premiumization and more formulation-intensive product architectures.

MARKET RESTRAINTS

Regulatory Complexity and Preservative/Formulation Constraints Can Slow Commercial Flexibility

Cosmetic chemicals function within a rigorously regulated formulation framework, where the choice of ingredients is governed by safety regulations, claim substantiation requirements, regional legal standards, and retailer of brand-specific exclusion lists. This regulatory complexity can impede reformulation efforts and limit the utilization of certain preservatives, ultraviolet filters, colorants, or sensory materials—particularly when companies aspire to develop globally harmonized formulations. These compliance requirements are especially pertinent in Europe, where the regulatory environment remains highly stringent and continues to evolve with an increased emphasis on sustainability, transparency in labeling, and chemical regulation.

Furthermore, the transition towards “free-from,” naturally derived, or microbiome-sensitive formulations constricts the spectrum of available techniques in certain applications. Suppliers are frequently required to reconcile efficacy, shelf life, sensory attributes, compatibility, and cost concurrently, potentially prolonging development durations and diminishing formulation flexibility. This challenge is particularly pronounced in the area of preservation, where alternatives must continue to operate effectively under rigorous real-world conditions.

MARKET OPPORTUNITIES

Biotechnology, Natural Preservation, and High-Claim Actives Are Opening New Market Opportunities

A considerable opportunity exists within high-performance, bio-based ingredients, next-generation preservation systems, and scientifically validated active platforms that enable brands to merge efficacy with sustainability and cleaner label positioning. Suppliers are proactively investing in biotechnology and innovative active compounds supporting collagen synthesis, skin repair, well-aging, barrier health, and emotional and sensorial aspects, while also providing formulators with stronger narratives concerning origin and functionality.

This opportunity is reinforced by supplier innovation pipelines. In 2025, Clariant introduced its expanded Clariant Beauty positioning alongside several new solutions; Symrise unveiled the Mindera plant-based product-protection platform; and Evonik emphasized the increasing demand for environmentally friendly, high-performance personal care solutions at in-cosmetics Global 2025. Consequently, the market is anticipated to generate disproportionate value within ingredient niches capable of addressing both performance and sustainability requirements simultaneously.

MARKET CHALLENGES

Raw-Material Volatility, Speed-to-Market Pressure, and Proof-of-Performance Demands Are Creating Execution Challenges

The cost structure of cosmetic chemicals is shaped by oleochemicals, petrochemical intermediates, botanical extracts, fermentation inputs, solvents, specialty additives, packaging interactions, and quality-control requirements. Volatility in feedstocks and logistics can pressure profit margins, particularly for ingredients that occupy intermediary positions between commodity and specialty categories, such as surfactants, emollients, and preservation blends. Concurrently, suppliers must adapt to expedited launch cycles dictated by beauty brands, which shorten development timelines and increase commercialization pressures.

Another challenge is the increasing demand for comprehensive substantiation. Ingredient suppliers are anticipated to support claims with safety and performance data, as well as sustainability metrics, natural-origin documentation, biodegradability positioning, and more advanced efficacy narratives. This escalation in requirements elevates research and development, as well as application-support costs, especially for smaller suppliers competing against larger international entities with more extensive scientific and regulatory infrastructure.

Segmentation Analysis

By Type

Surfactants Segment Dominated the Market Owing to Their Broad Use Across Cleansing and Emulsification Systems

Based on type, the market is segmented into surfactants, emollients & moisturizers, preservatives, and others.

The surfactants segment held the leading cosmetic chemicals market share in 2025, supported by its indispensable role in facial cleansers, shampoos, body washes, micellar systems, oral-care adjacencies, and a wide range of emulsified personal care products. Surfactants remain high-volume ingredients because they provide cleansing, foaming, solubilization, emulsification, and formulation stability across both mass-market and premium categories. The segment also benefits from reformulation activity toward milder systems, sulfate alternatives, and more sustainable feedstock options rather than only basic volume growth.

Emollients & moisturizers are projected to register the fastest CAGR of 4.9% during the forecast period. Growth is being driven by skin barrier repair, moisturization claims, sensorial enhancement, scalp care, sun care, and premium skin treatment formats where feel, absorbency, and multifunctionality are critical. As skincare remains one of the most resilient beauty categories and premiumization continues, demand for high-value emollient systems, esters, oils, and active-support moisturizing ingredients is expected to remain strong.

By Application

To know how our report can help streamline your business, Speak to Analyst

Skincare Segment Held the Dominant Position Owing to Employing a Broader and Value-Added Selection of Ingredients

In terms of application, the market is categorized into skincare, haircare, oral care, makeup, and others.

The skincare segment held 40.7% of the market share in 2025, driven by the substantial ingredient content of serums, creams, sun care products, masks, dermocosmetics items, and barrier-repair formulations. This category tends to employ a broader and more value-added selection of ingredients, including emollients, humectants, emulsifiers, preservation systems, active ingredients, delivery systems, and sensorial modifiers. Market data from Cosmetics Europe for 2024 further indicates that skincare remains one of the largest beauty sectors in Europe, reinforcing its pivotal role in global ingredient demand. Furthermore, it is forecasted that this segment will grow at a CAGR of 5.4% during the forecast period.

The haircare sector is projected to experience substantial CAGR of 4.6% throughout the forecast period. This expansion will be driven by premium scalp care, bond-repair systems, textured-hair products, anti-hair-fall positioning, and an increasing integration of skincare science within haircare formulations. Suppliers are progressively focusing on hair wellness through the development of specialty conditioning systems, biofunctional ingredients, and gentler cleansing platforms. Consequently, this trend is enhancing both the complexity of formulations and the ingredient value per product.

Cosmetic Chemicals Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Cosmetic Chemicals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, the Asia Pacific region held the dominant share valued at USD 7.36 billion, and it continued to led in 2025 with a valuation of USD 7.83 billion. The region benefits from the expansive markets of China, Japan, South Korea, India, and Southeast Asia, as well as from dense manufacturing ecosystems supporting both domestic and export-oriented beauty products. According to Cosmetics Europe’s 2024 market performance data, China, Japan, India, and South Korea are already among the world’s leading beauty markets, underpinning the region’s prominence in cosmetic-ingredient consumption.

China Cosmetic Chemicals Market

By 2026, the Chinese market is projected to reach USD 3.33 billion. China serves as the primary demand hub within the Asia Pacific region, underpinned by its extensive presence in skincare, facial care, sun protection, premium domestic beauty brands, and a progressively advanced local manufacturing sector. The expansion is further bolstered by domestic innovation ecosystems and investments from suppliers; for instance, Clariant announced the establishment of a new production facility in China scheduled for 2025 to cater to demand in the Asian market.

To know how our report can help streamline your business, Speak to Analyst

Japan Cosmetic Chemicals Market

The Japan market in 2026 is estimated to be around USD 1.26 billion, accounting for roughly 5.5% of the global revenues.

India Cosmetic Chemicals Market

The India market in 2026 is estimated at around USD 0.92 billion, accounting for roughly 4.0% of global revenues.

Europe

Europe is expected to witness solid market growth over the coming years. During the forecast period, the European region is projected to record a growth rate of 4.3% and reach the valuation of USD 5.16 billion in 2026. The region remains one of the world’s most important cosmetics and personal care markets, with retail sales valued at USD 120 billion in 2024, according to Cosmetics Europe. Europe is characterized by high regulatory scrutiny, strong premium skincare and fragrance traditions, and significant emphasis on sustainability, preservation strategy, and ingredient transparency. These factors support demand for higher-value and more technically differentiated cosmetic chemicals.

U.K. Cosmetic Chemicals Market

The U.K. market in 2026 is estimated at around USD 0.64 billion, accounting for roughly 2.8% of global revenues.

Germany Cosmetic Chemicals Market

Germany’s market in 2026 is estimated at around USD 0.83 billion, accounting for roughly 3.6% of global revenues.

North America

The region benefits from a substantial premium beauty sector, robust demand for dermocosmetics and prestige skincare products, and extensive formulation activity among both multinational and independent brands. The U.S. is particularly significant due to the scale of its beauty market; according to Cosmetics Europe’s 2024 data, the U.S. personal care and cosmetics industry is valued at USD 107 billion, rendering it one of the largest globally. Projections indicate that by 2026, the U.S. market will reach USD 5.38 billion.

U.S. Cosmetic Chemicals Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is set to reach USD 5.38 billion by 2026, accounting for roughly 23.4% of global sales.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are comparatively smaller markets, yet they are experiencing robust growth driven by increased beauty penetration, haircare market expansion, local-brand proliferation, and the rising consumption of premium and masstige products. Latin America benefits from Brazil’s substantial market size, while the Middle East & Africa region is supported by the premium fragrance and skincare sectors, alongside a gradually expanding local beauty manufacturing industry. According to Cosmetics Europe’s 2024 data, Brazil’s market is valued at USD 27 billion, highlighting Latin America’s significance in the global beauty industry. The Latin America market is projected to reach a valuation of USD 1.96 billion by 2026.

GCC Cosmetic Chemicals Market

The GCC market in 2026 is estimated to be around USD 0.76 billion, accounting for approximately 3.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Application Support, Regulatory Readiness, and Science-Backed Differentiation Are Core Competitive Advantages

The market exhibits moderate fragmentation, comprising a combination of large multinational specialty ingredient suppliers and specialized active/formulation entities. Competitive advantage is contingent upon the diversity of product portfolios, the velocity of innovation, substantiation of claims, formulation support, compliance proficiency, and the capacity to supply across regions with uniform quality. Suppliers capable of integrating functional ingredients, active systems, preservation, and sustainability positioning are strategically better positioned to establish long-term business relationships with global beauty manufacturers and emerging independent brands.

Large incumbent companies also leverage integrated research and development, customer application centers, biotechnology capabilities, and extensive regional manufacturing networks. Notable participants such as BASF, Croda, Symrise, Clariant, Evonik, and DSM-Firmenich are instrumental in shaping advancements in natural-origin ingredients, product preservation, skin and hair actives, and sustainable formulation platforms.

LIST OF KEY COSMETIC CHEMICALS COMPANIES PROFILED

- BASF SE (Germany)

- Croda International Plc (U.K.)

- Symrise AG (Germany)

- Clariant AG (Switzerland)

- Evonik Industries AG (Germany)

- DSM-Firmenich (Netherlands)

- Ashland Inc. (U.S.)

- Solvay SA (Belgium)

- Givaudan Active Beauty (Switzerland)

- Lubrizol Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2025: Clariant launched its new “Clariant Beauty” positioning and introduced fresh solutions spanning skin care, hair care, and sun protection.

- March 2025: Clariant introduced Nipaguard SCE Vita, a fully naturally derived preservation blend for cosmetic formulations.

- March 2025: Lucas Meyer Cosmetics by Clariant launched Melicica, a honey-inspired skin-repair solution aimed at advanced skin care concepts.

- March 2025: Clariant, through Lucas Meyer Cosmetics, introduced GlowCytocin, a skin-care ingredient positioned around skin wellness and science-backed beauty claims.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on the technological advancements, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market shares and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 21.76 billion in 2025 and is projected to reach USD 33.70 billion by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period.

The skincare application segment led in 2025.

Asia Pacific held the highest market share in 2025.

The rising popularity of anti-aging and dermatology-inspired cosmetic products is accelerating the adoption of these products.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us