Fleet Management & Mobility Services Market Size, Share & Industry Analysis, By Service Type (Fleet Management Solutions [Vehicle tracking & Telematics, Maintenance & Diagnostics, Fuel & Energy Management, Compliance & Safety Management], Mobility Services [Ride-hailing & Ride-Sharing, Car-sharing & vehicle subscription, Corporate Mobility Services and MaaS Platforms), By Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium & Heavy Commercial Vehicles and Two-wheelers & Micro-mobility), By Propulsion Type, By End-user, By Deployment Model, and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

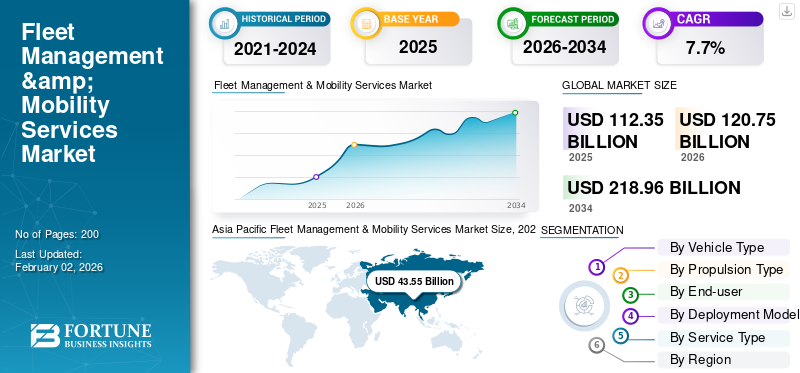

The global Fleet Management & Mobility Services market size was valued at USD 112.35 billion in 2025. The market is projected to grow from USD 120.75 billion in 2026 to USD 218.96 billion by 2034, exhibiting a CAGR of 7.7% during the forecast period. Asia Pacific dominated the global market with a market share of 38.76% in 2025.

Fleet management & mobility services involve digital platforms that manage vehicle fleets and provide shared, on-demand transportation solutions, improving efficiency, safety, cost control and flexible movement of people and goods. Key market drivers include rising fleet operating costs, digitalization and regulatory compliance needs, demand for real-time tracking, electrification, urban mobility growth, sustainability goals and adoption of shared and connected mobility solutions.

Major players in the market include Verizon Connect, Geotab, Trimble, Samsara, Omnitracs and Fleet Complete, competing through advanced telematics, data analytics, digital platforms, automation and safety-focused mobility solutions.

Download Free sample to learn more about this report.

Fleet Management & Mobility Services Market Key Takeways

- 2025 Market Size: USD 112.35 billion

- 2026 Market Size: USD 120.75 billion

- 2034 Forecast Market Size: USD 218.96 billion

- CAGR: 7.7% from 2026–2034

- Asia Pacific dominated the Fleet Management & Mobility Services market with a 38.76% share in 2025.

- The passenger cars segment accounted for the largest market share in 2025.

- The ICE segment held the dominant market share due to its extensive global vehicle base.

Asia Pacific

Asia Pacific dominated the market and is the fastest-growing region, driven by urbanization and digital mobility adoption.

Europe

Europe witnessed steady growth supported by stringent vehicle safety, emissions, and sustainability regulations.

North America

North America held the second-largest market share and is projected to grow at a CAGR of 7.2%.

U.S.

U.S. The market reached approximately USD 26.81 billion in 2026, representing around 22.2% of global revenue.

Japan

Japan The market reached approximately USD 3.05 billion in 2026, accounting for about 2.5% of global revenue.

Read More

FLEET MANAGEMENT & MOBILITY SERVICES MARKET TRENDS

Integration of AI, IoT, and Data Analytics to Reshape Market Growth

Artificial intelligence, IoT sensors and advanced data analytics are reshaping fleet management & mobility services market growth. Real-time data from connected vehicles enables predictive maintenance, automated compliance reporting and dynamic route optimization. AI-driven insights support smarter decision-making and improved safety outcomes. In mobility services, data-driven demand forecasting enhances service availability and customer experience. This technology integration trend is redefining operational efficiency and scalability across the market.

- In August 2025, Blues launched new fleet management capabilities, including Smart Fleets, Fleets to Exclude and Batch Jobs, to simplify large-scale IoT device orchestration. These tools improve automation, data quality, and operational control that are key needs for connected fleets, telematics deployments, and asset-heavy mobility services.

MARKET DYNAMICS

MARKET DRIVERS

Rising Operating Costs and Need for Fleet Optimization to Drive Market Growth

Increasing fuel prices, maintenance expenses, and labor costs are pushing fleet operators and mobility providers to adopt digital fleet management and mobility solutions. Companies seek real time tracking, predictive maintenance and route optimization to reduce downtime and improve asset utilization. Advanced analytics help optimize driver behavior, fuel consumption and scheduling, directly improving profitability. This cost-efficiency focus is a primary driver accelerating adoption of fleet management solutions across logistics, public transport and shared mobility fleets globally.

- In December 2025, Verizon released its Verizon Connect Fleet Technology Report, highlighting fleet operators’ increasing adoption of real-time telematics, AI analytics, safety automation, and cloud platforms. The findings emphasize that data-driven tools and connectivity investments are accelerating operational performance and cost efficiency across global fleets.

MARKET RESTRAINTS

High Initial Implementation and Integration Costs to Restrain Market Adoption

The deployment of fleet management and mobility platforms often requires significant upfront investment in hardware, software licenses, system integration and employee training. Small and medium fleet operators may find these costs challenging, especially while integrating new platforms with legacy IT systems. Additionally, customization needs across diverse fleet types increase complexity and expenses. These financial and technical barriers can slow adoption, particularly in cost-sensitive markets and developing regions.

MARKET OPPORTUNITIES

Growing Electrification and EV Fleet Adoption to Create New Market Opportunities

The rapid adoption of electric vehicles (EVs) across commercial fleets and shared mobility services presents strong growth opportunities. Fleet management platforms are increasingly used to monitor battery health, charging schedules, energy consumption and total cost of ownership. Mobility service providers also rely on digital tools to manage EV availability and charging infrastructure efficiently. As governments promote zero-emission fleets, demand for EV-focused fleet management and mobility solutions will accelerate significantly. As a result, growing electrification and EV fleet adoption create fleet management & mobility services demand.

- In December 2025, Greaves Electric Mobility (GEML) strengthened its partnership with Alt Mobility to accelerate EV fleet adoption through leasing-led deployment of purpose-built e2Ws and an ecosystem approach (including battery-swapping infrastructure). It supports last-mile fleets with higher uptime and scalability.

MARKET CHALLENGES

Data Security and Privacy Concerns to Remain a Key Market Challenge

Fleet management & mobility services rely heavily on continuous data collection, including vehicle location, driver behavior and customer usage patterns. Ensuring data security, privacy compliance and protection against cyberattacks remains a major challenge for service providers. Increasing regulatory scrutiny around data usage further adds to the complexity. Failure to address these concerns can lead to operational risks, legal penalties and reduced trust among fleet operators and mobility service users.

Download Free sample to learn more about this report.

Segmentation Analysis

By Vehicle Type

Extensive Urban Passenger Car Parc and Digital Fleet Adoption to Propel Passenger Cars Segmental Dominance

Based on vehicle type, the market is segmented into passenger cars, light commercial vehicles, medium & heavy commercial vehicles, and two-wheelers & micro-mobility.

The passenger cars segment held highest Fleet Management & Mobility Services market share due to its vast global vehicle parc and high penetration of connected technologies. Urbanization, corporate fleets, ride-hailing and car-sharing services drive large-scale deployment of telematics, tracking, and compliance solutions. Fleet operators prioritize real-time monitoring, predictive maintenance, and driver analytics to control costs and improve utilization. Regulatory compliance, insurance integration and data-driven mobility optimization further sustain recurring software and service demand across OEMs, fleet owners and mobility platforms.

- In December 2025, Hyundai introduced its Prime Taxi range (Prime HB/Prime SD) aimed at fleet operators and cab drivers, emphasizing predictable maintenance, uptime and low operating costs. This expands OEM participation in organized fleet mobility, supporting professionalized vehicle deployment and lifecycle programs.

The two-wheelers & micro-mobility is the fastest-growing segment, expanding at a CAGR of 10.0% over the forecast period. Rapid growth of last-mile delivery, shared mobility platforms, and urban congestion management accelerates adoption of lightweight telematics, asset tracking and fleet optimization solutions.

By Propulsion Type

Large Installed ICE Fleet and Legacy Infrastructure to Propel ICE Segment

Based on propulsion type, the market is segmented into ICE and electric.

The ICE segment dominates the market, due to its massive global installed base across passenger, commercial and shared mobility fleets. Fleet operators rely on telematics, fuel management, maintenance analytics, and compliance solutions to optimize operating costs and extend vehicle life. Mature servicing ecosystems, regulatory monitoring needs, and widespread adoption across logistics, corporate fleets, and ride-hailing platforms ensure sustained demand for ICE-focused fleet management solutions.

The electric segment is the fastest-growing, expanding at a CAGR of 17.7% over the forecast period. Rapid EV adoption drives demand for battery monitoring, charging optimization, energy management and predictive maintenance solutions across commercial and shared mobility fleets.

- In June 2025, BearingPoint launched an integrated e-mobility platform (with SAP) for fleet managers, combining EV operations, charging and data-driven planning in one system. It supports scalable fleet electrification workflows, improving utilization, cost visibility and operational control for large fleets.

By End-user

Large-Scale Fleet Operations and Cost Optimization Needs Boosts Commercial Fleets Growth

By end-user, the market is divided into commercial fleets, corporate fleets, mobility service providers and government & municipal fleets.

Commercial fleets dominate the market of fleet management & mobility services due to their large vehicle volumes and continuous focus on operational efficiency. Logistics companies, corporate fleets, utilities and service providers heavily deploy telematics, fuel management, compliance and maintenance solutions to reduce costs, improve uptime and meet regulatory requirements. High vehicle utilization rates, recurring software subscriptions, and long-term contracts with fleet solution providers ensure stable, repeat demand across regions and vehicle categories.

- In November 2025, Samsara launched its Commercial Navigation solution, offering safe, compliant, turn-by-turn GPS guidance tailored for commercial fleets with height, weight, and hazmat restrictions. Integrated into the Samsara Driver App, it enhances safety, efficiency, and operational routing within fleet operations.

Mobility service providers are the fastest-growing end-user segment, expanding at a CAGR of 8.9% over the forecast period. This growth is driven by ride-hailing, car-sharing, subscription models and MaaS platforms, which require real-time tracking, dynamic pricing and data-driven fleet optimization.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Model

Scalability, Real-Time Analytics and Lower IT Overheads to Drive Cloud-Based (SaaS) Segment

By deployment model, the market is categorized into cloud-based (SaaS), on premise, and hybrid.

Cloud-based (SaaS) solutions dominate the market due to their scalability, rapid deployment, and lower upfront IT costs. Fleet operators favor SaaS platforms for real-time vehicle tracking, analytics, remote updates and seamless integration with IoT devices and third-party systems. Subscription-based pricing, frequent feature upgrades, cybersecurity enhancements, and suitability for multi-location fleets further reinforce widespread adoption across commercial fleets and mobility service providers.

- In September 2025, the UAE unveiled its first Sovereign Mobility Cloud to accelerate autonomous transport while keeping mobility data hosted and governed locally. It supports HD mapping, telematics, fleet operations and traffic management, strengthening national infrastructure for connected and autonomous mobility services.

On premise deployment holds the second-largest share and is expected to grow at a CAGR of 7.2% over the forecast period. Adoption remains strong among large enterprises and government fleets prioritizing data control, legacy system integration, and customized security architectures.

By Service Type

Operational Efficiency, Compliance and Cost Control Augments Fleet Management Solutions Demand

By service type, the market is categorized into fleet management solutions & mobility services. The fleet management solutions is further divided vehicle tracking & telematics, maintenance & diagnostics, fuel & energy management, compliance & safety management. The mobility services is further sub-segmented to ride-hailing & ride-sharing, car-sharing & vehicle subscription, corporate mobility services, and MaaS (Mobility-as-a-Service) platforms.

Fleet management solutions dominates the market. The growth of the segment is due to their critical role in optimizing daily fleet operations. Vehicle tracking, telematics, maintenance, fuel management and compliance tools enable fleet operators to reduce costs, improve uptime, and enhance driver safety. Strong adoption across logistics, corporate fleets, public sector fleets, and utilities, along with recurring subscription models and regulatory requirements, ensures stable and sustained demand globally.

- In January 2025, ZF unveiled SCALAR, an AI-driven fleet management platform in India to optimize commercial fleet operations through performance insights, monitoring, and smarter planning. The development highlights rising adoption of data-led fleet orchestration tools to reduce costs and improve productivity.

Mobility services are the fastest-growing service type, expanding at a CAGR of 8.4% over the forecast period. This segment growth is driven by ride-hailing, car-sharing, vehicle subscriptions, and MaaS platforms that require real-time demand management, dynamic fleet allocation and seamless digital user experiences.

Fleet Management & Mobility Services Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific and the rest of the world.

Asia Pacific

Asia Pacific Fleet Management & Mobility Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates and is the fastest-growing region in the global market. The regional market growth is supported by rapid urbanization, expanding commercial vehicle fleets and strong adoption of digital mobility solutions. Growth in e-commerce, logistics, ride-hailing, and shared mobility across key markets such as China, India, and Southeast Asia also fuels demand. Government-backed smart city initiatives, rising smartphone penetration, and increasing EV adoption further accelerate telematics, cloud-based fleet platforms and mobility service deployment across the Asia Pacific market.

- In September 2024, myTVS launched a Pan-India Mobility-as-a-Service platform for last-mile EV fleets, bundling leasing, telematics, servicing, spares, charging support, insurance, and roadside assistance. The integrated offering targets higher uptime and lower operating disruption for fleet operators.

China Fleet Management & Mobility Services Market

The China market in 2026 is estimated at around USD 16.24 billion, accounting for roughly 13.4% of global revenues. China holds the largest share in the Asia Pacific region, driven by large commercial fleets, logistics digitalization, EV fleet adoption, and smart city initiatives.

Japan Fleet Management & Mobility Services Market

The Japan market in 2026 is estimated at around USD 3.05 billion, accounting for roughly 2.5% of global revenues. Japan’s growth is supported by connected vehicle penetration, aging workforce automation, telematics upgrades, and strong OEM-led mobility platforms.

India Fleet Management & Mobility Services Market

The India market in 2026 is estimated at around USD 15.70 billion, accounting for roughly 13.0% of global revenues. Fast growth is fueled by e-commerce logistics, ride-hailing expansion, GPS adoption, cost optimization needs, and government-backed digital transport initiatives.

Europe

Europe’s market growth is supported by strict vehicle safety, emissions and data compliance regulations that encourage the adoption of advanced fleet management systems. The region’s strong focus on sustainability, electrification and multimodal mobility drives demand for energy management, compliance and mobility-as-a-service platforms. High penetration of connected vehicles, mature logistics networks and early adoption of smart mobility solutions ensure consistent and regulation-driven market expansion.

- In September 2025, Targa Telematics partnered with Conneqtech to advance connected mobility solutions in Central Europe, combining telematics, IoT and cloud-based fleet management services. The collaboration enhances scalability, real-time data insights and integrated mobility platforms for fleet operators across the region.

Germany Fleet Management & Mobility Services Market

The Germany market in 2026 is estimated at around USD 4.71 billion, accounting for roughly 3.9% of global revenues. Growth is driven by enterprise fleet electrification, regulatory compliance, advanced telematics, sustainability targets, and strong logistics and leasing sectors.

U.K Fleet Management & Mobility Services Market

The U.K. market in 2026 is estimated at around USD 3.66 billion, accounting for roughly 3.0% of global revenues. The U.K. market is supported by EV fleets, congestion management, SaaS-based telematics, urban mobility services, and emission-reduction policies.

North America

North America holds the second-largest market share and is projected to grow at a CAGR of 7.2%. The regional market growth is driven by its extensive commercial fleet base and advanced telematics adoption. High demand from logistics, construction and long-haul transportation fleets supports steady growth. Increasing focus on fuel efficiency, driver safety, regulatory compliance and integration of AI-driven analytics strengthens ongoing investments in fleet management and mobility platforms.

- In August 2025, Samsara launched a Pre-Delivery Installation (PDI) Program to streamline fleet technology deployment by pre-installing telematics hardware before vehicles reach operators. This reduces installation time, speeds onboarding and improves fleet readiness for real-time tracking and data insights at scale.

U.S. Fleet Management & Mobility Services Market

The U.S. market in 2026 is estimated at around USD 26.81 billion, accounting for roughly 22.2% of global revenues. The U.S. dominates the North American market due to extensive commercial fleet operations, early adoption of telematics, strong logistics infrastructure, regulatory compliance needs and growing investments in digital fleet optimization technologies.

Rest of the World

The Rest of the World region is witnessing gradual market growth, due to expanding transportation infrastructure and increasing digitalization of fleet operations. Rising adoption of fleet tracking and mobility solutions in Latin America and the Middle East & Africa is driven by logistics expansion, urban mobility initiatives and growing awareness of operational efficiency. Improving connectivity and supportive government programs further enhance long-term market potential.

- In October 2025, V Zone International launched V Zone AI, the world’s first conversational AI assistant for fleet management, enabling operators to query vehicle data by voice/text. It simplifies decision-making, advances efficiency and delivers real-time actionable insights for logistics, public transport and corporate fleets.

COMPETITIVE LANDSCAPE

Key Industry Players

Platform-Centric Software Innovation and Data-Driven Mobility Integration to Shape Competitive Dynamics

The fleet management & mobility services market is moderately fragmented, with the presence of global telematics leaders and numerous regional and niche solution providers. Competition is driven by rapid digitalization, cloud-based platforms, and data-driven fleet optimization. Key players such as Verizon Connect, Geotab, Trimble, Samsara, Omnitracs, and Fleet Complete compete through advanced telematics, AI-based analytics, real-time tracking and integrated mobility platforms. Companies differentiate through scalable SaaS offerings, EV fleet management capabilities, compliance automation and API-based integrations.

- In December 2025, Geotab and Verizon Connect announced a strategic collaboration to integrate Geotab’s telematics platform with Verizon Connect’s fleet solutions, enhancing data sharing, analytics and scalability for shared customers and improving operational insights across mixed fleets.

LIST OF KEY FLEET MANAGEMENT & MOBILITY SERVICES COMPANIES PROFILED

- Verizon Connect (U.S.)

- Geotab (Canada)

- Samsara (U.S.)

- Trimble (U.S.)

- Omnitracs (U.S.)

- Teletrac Navman (U.S.)

- Fleet Complete (Canada)

- Webfleet / TomTom Telematics (Netherlands)

- Quartix (U.K.)

- Masternaut (France)

- Gurtam (Lithuania)

- Wheelseye (India)

- iTriangle Infotech (India)

- G7 Networks (China)

- MapmyIndia (India)

KEY INDUSTRY DEVELOPMENTS

- In December 2025, Carota introduced a MaaS smart mobility service built around three core product lines, aiming to help operators orchestrate trips, users, and assets via a unified digital layer. The launch reinforces platform-based mobility bundling across fleets, shared mobility and partners.

- In November 2025, WeRide and Uber began fully driverless robotaxi commercial operations in Abu Dhabi on the Uber platform, starting with defined routes including Yas Island. The milestone strengthens the mobility-services stack around autonomous fleet operations, monitoring, charging, and safety governance.

- In August 2025, Mahindra Logistics launched Alyte, a premium, tech-enabled B2C mobility service starting in Delhi NCR, with expansion planned to more cities and airport corridors. The move reflects intensifying competition in app-driven urban mobility and service differentiation via reliability and transparency.

- In May 2025, Zen Mobility launched Zen Flo (a full-stack EV platform) and the Micro Pod Ultra, enabling MaaS-style leasing, usage-based billing, and real-time fleet analytics for last-mile logistics. The launch underscores fleet operators’ shift toward integrated financing + operations platforms.

- In September 2024, myTVS stated it would add 10,000 electric two-wheelers to its MaaS platform by March-end, pairing leasing with real-time fleet management and servicing. The expansion signals growing platform scale in EV fleet operations and stronger demand for bundled lifecycle services.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.7% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Vehicle Type, Propulsion Type, End-user, Deployment Model, By Service Type, and Region |

|

By Vehicle Type |

· Passenger Cars · Light Commercial Vehicles · Medium & Heavy Commercial Vehicles · Two-wheelers & Micro-mobility |

|

By Propulsion Type |

· ICE · Electric |

|

By End-user |

· Commercial Fleets · Corporate Fleets · Mobility Service Providers · Government & Municipal Fleets |

|

By Deployment Model |

· Cloud-based (SaaS) · On-premise · Hybrid |

|

By Service Type |

· Fleet Management Solutions o Vehicle tracking & telematics o Maintenance & diagnostics o Fuel & energy management o Compliance & safety management · Mobility Services o Ride-hailing & ride-sharing o Car-sharing & vehicle subscription o Corporate mobility services o MaaS (Mobility-as-a-Service) platforms |

|

By Geography |

· North America (By Vehicle Type, Propulsion Type, End-user, Deployment Model, Service Type, and Country) o U.S. o Canada o Mexico · Europe (By Vehicle Type, Propulsion Type, End-user, Deployment Model, Service Type, and Country) o Germany o U.K. o France o Rest of Europe · Asia Pacific (By Vehicle Type, Propulsion Type, End-user, Deployment Model, Service Type, and Country) o China o Japan o India o South Korea o Rest of Asia Pacific · Rest of the World (Vehicle Type, Propulsion Type, End-user, Deployment Model, Service Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 112.35 billion in 2025 and is projected to reach USD 218.96 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 43.55 billion.

The market is expected to exhibit a CAGR of 7.7% during the forecast period of 2026-2034.

The passenger cars segment leads the market in terms of vehicle type.

Rising operating costs and the need for fleet optimization to drive market growth.

Key players in the market include Verizon Connect, Geotab, Trimble, Samsara, Omnitracs, and Fleet Complete, among others.

Asia Pacific holds the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us