Flexible Intermediate Bulk Container Market Size, Share & Industry Analysis, By Product Type (Type A, Type B, Type C, and Type D), By End-use Industry (Chemicals & Fertilizers, Food & Beverages, Building & Construction, Pharmaceutical, Agriculture, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

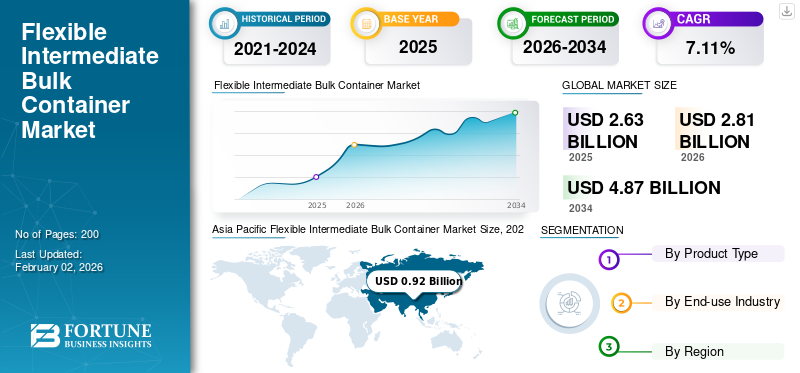

The global flexible intermediate bulk container market size was valued at USD 2.63 billion in 2025 and is projected to grow from USD 2.81 billion in 2026 to USD 4.87 billion by 2034, exhibiting a CAGR of 7.11% during the forecast period. Asia Pacific dominated the flexible intermediate bulk container market with a market share of 37.25% in 2024.

A flexible intermediate bulk container (FIBC) is a large container or sack designed for the storage or transport of different products or materials. These bags present a cost-effective alternative to the high costs associated with shipping or transporting materials such as plastic and wooden pallets and containers.

There is growing adoption of bulk containers for the packaging and transportation of agricultural products such as grains, seeds, sugar, and flour. As the global trade of food expands, particularly in developing areas such as Southeast Asia and Africa, the demand for economical, lightweight, and sturdy packaging options becomes essential, driving the growth of the global flexible intermediate bulk container market.

- The Food and Agriculture Organization of the United Nations states that the global monetary value of food exports rose by 4.4 times in nominal terms from 2000 to 2021, increasing from USD 380 billion in 2000 to USD 1.66 trillion in 2021, with significant growth across all groups of food commodities, particularly in fats and oils. Fruits and vegetables represented 19 percent of the overall value of food exports in 2021, while cereals and preparations made up 15 percent.

Grief Inc. and Amcor Plc are the leading manufacturers, accounting for the largest share of the global flexible intermediate bulk container market.

Download Free sample to learn more about this report.

FLEXIBLE INTERMEDIATE BULK CONTAINER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.63 billion

- 2026 Market Size: USD 2.81 billion

- 2034 Forecast Market Size: USD 4.87 billion

- CAGR: 7.11% from 2026–2034

- Asia Pacific dominated the market with a 37.25% share in 2024.

- The Type A segment held the largest market share in 2024.

- The Chemicals & Fertilizers segment dominated the market in 2024.

North America

North America ranked second, supported by growing demand from the food, chemical, and construction industries.

Europe

Europe is witnessing steady growth due to rising demand for sustainable packaging and pharmaceutical applications.

Asia Pacific

Asia Pacific led the market, driven by strong demand from China and India.

U.S.

The flexible packaging industry is the second-largest packaging segment, supporting strong FIBC demand.

Japan

Rising demand for high-quality bulk packaging from industrial and manufacturing sectors is supporting market growth.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapidly Growing E-commerce Sector Drives the Global Market Growth

The rapidly expanding global e-commerce sector is playing a major role in the flexible intermediate bulk container market growth. Increasing disposable income among consumers and higher lifestyle standards are propelling the consumer goods sector, which in turn, is boosting the e-commerce industry. The rise of both e-commerce and consumer goods is intensifying the need for economical and durable packaging solutions, thereby promoting the uptake of the product. Moreover, the increasing need for pharmaceuticals and chemical products has strengthened the adoption of these containers due to their adaptability to different forms and ability to offer customized protection. At present, online retail businesses and e-commerce platforms require around fifty percent more FIBC packaging compared to conventional retail outlets. This increase is attributed to the need for securing products during transportation and shipping individual items.

- According to a recent study by the United Nations Conference on Trade and Development, in the 43 developed and developing economies analyzed, sales from business-to-business e-commerce surpassed total exports of goods and services. It is estimated that exports ordered digitally amounted to approximately USD 2.5 trillion in 2021, with a range between USD 1.6 trillion and USD 4.9 trillion.

MARKET RESTRAINTS

Rising Environmental Concerns & Regulatory Compliance to Hamper Market Expansion

A significant challenge is the environmental effects of traditional flexible materials, particularly those produced from petroleum-derived polymers such as polyurethane (PU) and polyethylene (PE). These foams are often non-biodegradable, hard to recycle, and add to persistent plastic pollution. Governments globally are implementing tougher packaging laws aimed at minimizing plastic waste and encouraging recycling. Adhering to these regulations requires companies to invest in research and development, innovative raw materials, and testing to confirm that their foam packaging complies with environmental and safety criteria.

- In April 2024, the European Commission established rules on plastic packaging, primarily aimed at decreasing waste and encouraging a circular economy by 2030. These rules, particularly the Packaging and Packaging Waste Directive (PPWD), which is now being succeeded by the Packaging and Packaging Waste Regulation (PPWR), are designed to minimize the consumption of virgin materials, increase the incorporation of recycled content in packaging, and ensure that recycling all packaging within the EU market is economically feasible.

MARKET OPPORTUNITIES

Rising Demand from the Food Sector to Offer Significant Growth Opportunities

FIBCs are frequently used in the food industry. Often utilized in food processing plants, bulk bags provide an excellent option for securely storing produce while prolonging the shelf life of perishable goods. When food products need to be transported internationally, FIBCs are among the few dependable choices for packaging. Moreover, FIBC bulk bags provide an effective means of storing ingredients and materials used in food production. Even a modest warehouse can easily handle large quantities of stored items, and the stackable design helps reduce space constraints and lower transportation costs. Bulk bags are highly versatile, with customizable features that facilitate the daily operations of food producers and processors. The growing demand for FIBCs in the food sector will create lucrative growth opportunities.

Flexible Intermediate Bulk Container MARKET TRENDS

Integrating RFID Tags with Flexible Intermediate Bulk Container to Boost Market Growth

RFID tags are being integrated into FIBCs to improve tracking, streamline inventory management, and provide real-time visibility of material contents and locations throughout the supply chain. This technology facilitates hands-free bulk scanning, boosts operational efficiency, minimizes human error related to barcodes, and allows automatic tracking without the direct line of sight. RFID tags can hold store details such as product ownership, transaction accounts, or environmental information, and can be read from a distance using specialized readers. Additionally, RFID technology supports better inventory management and quality control by providing accurate and up-to-date information about the contents and condition of the bags. This can help reduce waste and improve efficiency by ensuring that the right products are in the right place at the right time. Henceforth, integrating RFID tags with flexible intermediate bulk containers has emerged as a key trend in the industry.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Significant Benefits Offered by Type A FIBCs Boost the Segment’s Growth

Based on product type, the market is segmented into type A, type B, type C, and type D. The type A segment accounted for the largest share of the market in 2024. Type A FIBC (Flexible Intermediate Bulk Container) bags provide numerous advantages, particularly in terms of their economical nature and adaptability for transporting non-flammable substances. Constructed from plain woven polypropylene, these bags are not meant to dissipate static electricity, which makes them suitable for materials that do not present a fire risk, such as sand, gravel, or other solid substances. They are highly efficient in handling large volumes of materials, thereby streamlining the packaging and transportation process.

Type C will continue to be the second-dominating segment of the market. FIBC Type C bags are classified as conductive. Their woven design and non-conductive materials dissipate electrostatic charges, which makes Type C FIBC bags appropriate for transporting flammable materials. Additionally, they can be utilized in settings where flammable gases, vapors, and dust are found, ensuring greater safety during handling and storage.

By End-use Industry

Chemicals & Fertilizers Segment Led due to Several Advantages offered by FIBCs

Based on end-use industry, the market is divided into chemicals & fertilizers, food & beverages, building & construction, pharmaceuticals, agriculture, and others. Chemicals & fertilizers are the dominating segment of the market in 2024. FIBC (Flexible Intermediate Bulk Container) presents a variety of advantages to the chemical and fertilizer sectors, including improved safety, cost effectiveness, and eco-friendliness. FIBCs ensure secure storage by minimizing the likelihood of spills and leaks, and they also come in anti-static and conductive variants for handling dangerous substances. Their significant capacity and ability to be reused further aid in saving costs and lowering waste.

The food & beverages segment is expected to witness steady growth in the forecast period. Flexible intermediate bulk containers (FIBCs) are favored in this industry due to their adherence to food safety regulations, availability in food-grade options, and efficiency in managing substantial quantities. The increasing worldwide need for processed and packaged food, especially in emerging markets, is a key driver supporting this growth.

Flexible Intermediate Bulk Container Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Flexible Intermediate Bulk Container Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific is the dominating region in the FIBC market. Nations such as India and China are driving demand as their manufacturing industries grow and need affordable bulk packaging options. In India, sectors such as fertilizers and food grains depend significantly on FIBCs for both storage and transportation. In addition, the growing pharmaceutical sector across several countries in the region is further boosting the demand for flexible bulk containers.

- According to the Food Export Organization, China's food industry experienced consistent growth in 2022, with leading companies recording revenues of USD 1.3 trillion, marking a 5.6% increase from the previous year. Furthermore, the country is increasing its imports of food ingredients, creating further opportunities for packaging solutions such as FIBCs.

- The Press Information Bureau (PIB) indicates that India's pharmaceutical sector reached USD 50 billion in FY 2023-24, with domestic consumption amounting to USD 23.5 billion and exports totaling USD 26.5 billion. India's pharmaceutical industry is recognized as the third largest globally in terms of volume and ranks 14th in production value.

North America

North America is the second-largest market for the global flexible intermediate bulk container market. The U.S. and Canada widely utilize FIBCs in industries such as food and beverage, chemicals, construction, and agriculture due to their strength and compliance with OSHA and FDA regulations. For example, the U.S. chemical industry favors FIBCs for the secure transport of hazardous substances, while the food industry employs FDA-approved bulk bags for handling grains and powders. Moreover, the rapidly growing flexible packaging sector is further cushioning market expansion.

- The Flexible Packaging Association reports that flexible packaging is the second-largest segment within the U.S. packaging sector. The food industry (both for retail and institutional) accounts for approximately 50% of total deliveries. Other sectors utilizing flexible packaging include pet food at 2%, personal care at 5%, beverages at 6%, various non-food items at 9%, industrial applications at 7%, consumer goods at 2%, and the medical and pharmaceutical sector at 16%.

Europe

Europe is a significant market for flexible intermediate bulk containers. Sustainability trends are shaping demand, with consumers and regulators demanding eco-friendlier materials. This shift has driven advancements in biodegradable and recyclable foams, along with bio-based options, opening up fresh paths for growth. Additionally, the pharmaceutical industry plays a role in the expansion of the market.

- For example, the research-driven pharmaceutical industries can play a crucial role in revitalizing Europe’s growth and ensuring its future competitiveness in an evolving global market. In 2023, it allocated around USD 54,110 million for R&D within Europe.

Latin America

The market in Latin America is estimated to attain moderate growth in the forthcoming years, owing to the rising demand from the food processing sector. FIBCs are designed to support hygienic storage of processed foods, allowing safe stacking and lifting, and easy transportation. Their diverse bag designs and customizable features tailored to the specific requirements of processed food ensure they are ideally suited for the specific product. Thus, major players in the region’s food processing sector are increasingly adopting FIBCs.

Middle East & Africa

The Middle East & African market is expected to grow steadily in the upcoming years, owing to the growing demand from the building and construction industry. In the construction industry, flexible intermediate bulk containers (FIBCs) play a crucial role by enabling easy filling and emptying, efficient vehicle loading, and secure transport from one location to another. Additionally, flexible bulk containers can improve the safety standards of construction sites, as their robust construction makes them ideal for the demanding conditions of these environments, thus enhancing their utilization in the region.

- The International Trade Administration states that the construction industry in Saudi Arabia has positioned itself as a leader in the MENA region, with an anticipated market size of USD 70.33 billion in 2024, expected to grow to USD 91.36 billion by 2029. This expansion is driven by Saudi Arabia’s Vision 2030 National Development Plan, which reflects the government's significant investments in infrastructure projects.

- The country’s sovereign wealth fund, the Public Investment Fund, plays a crucial role as a financier and strategic backer of major giga-projects. Notable initiatives include Neom, a USD 500 billion futuristic city; Red Sea Global, a USD 23.6 billion eco-friendly luxury tourism initiative along Saudi Arabia’s Red Sea Coast; and Qiddiya, a USD 9.8 billion entertainment and leisure city, among other ventures.

COMPETITIVE LANDSCAPE

Key Industry Players

Continuous Development and Introduction of New Products by Key Companies Resulted in Their Dominating Position in the Market

The global market is concentrated with companies such as Greif Inc., Amcor Plc, Rishi FIBC Solutions Pvt. Ltd., and SIA Flexitanks, accounting for a significant flexible intermediate bulk container market share.

Grief Inc. stands as a leading global provider of industrial packaging products and services. They manufacture and distribute a variety of packaging solutions, such as steel, plastic, and fiber drums, intermediate bulk containers (IBCs), containerboard, and other related items. The company also oversees timber properties and provides value-added services, including filling, packaging, and lifecycle management of containers. Greif operates in more than 35 countries and caters to a wide range of industries, including chemicals, food and beverage, and automotive.

Amcor Plc is a world-renowned company specializing in the creation and production of innovative solutions. They provide a diverse array of packaging products and services, such as flexible packaging, rigid containers, cartons, and closures, serving numerous sectors such as food, beverages, and pharmaceuticals. Amcor prioritizes innovation, sustainability, and a customer-centric approach, which have been central to its global leadership in packaging.

Additionally, C.L. Smith and Southern Packaging, LP are among the other prominent players in the market. The company has strengthened its market presence through significant investments in research & development to deliver innovative products.

LIST OF KEY FLEXIBLE INTERMEDIATE BULK CONTAINER COMPANIES PROFILED

- Greif Inc. (U.S.)

- Amcor Plc (Switzerland)

- Rishi FIBC Solutions Pvt. Ltd. (India)

- SIA Flexitanks (Ireland)

- L. Smith (U.S.)

- Southern Packaging, LP (U.S.)

- FPS - Flexible Packaging Solutions (Netherlands)

- Western Packaging LLC (U.S.)

- Fluid-Bag Ltd. (Finland)

- Shandong Guansong Industrial Co., Ltd. (China)

- Kohsei Co., Ltd. (Japan)

- Euroflex FIBC (U.K.)

- JohnPac LLC (U.S.)

- Jumbo Bag Limited (India)

- Palmetto Industries International Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Disha Jute and Allied Products Pvt. Ltd. introduced its latest collection of Single Loop FIBC Bags, created for effective handling of bulk materials. Constructed from premium polypropylene, these bags provide strength, economical benefits, and convenient lifting with a single loop. Perfect for sectors such as agriculture, cement, and chemicals, they can carry substantial loads while remaining customizable and environmentally friendly, positioning them as an intelligent solution for contemporary packaging requirements.

- April 2025: Gravis unveiled its innovative Sustainabulk 100% Recycled FIBC Bulk Bag. This state-of-the-art solution represents more than just a product, reflecting a strong dedication to environmental sustainability. It enables companies globally to achieve eco-friendly objectives while enhancing operational efficiency.

- July 2024: Rapid Packaging, a top importer and master distributor of flexible intermediate bulk container (FIBC) bags, acquired Lawgix to strengthen its industrial bag division. This acquisition aligns with the company’s global strategy to reduce costs, enhance supply capacity, minimize supplier lead times, and improve product quality for clients in agriculture, food manufacturing, construction, retail, resin production, and other bulk bag-using sectors.

- October 2023: CDF Corporation unveiled a new manufacturing line for Form-Fit intermediate bulk container (IBC) liners, which will be located at the state-of-the-art facility of J. Natzan Kunststoffverarbeitung GmbH & Co KG in Lienen, Germany. Having collaborated for six years, the companies continue to share a common vision of providing exceptional, customized, and adaptable packaging solutions to meet evolving market needs.

- June 2020: TriEnda declared the launch of the Bulk Bag Pallet, a groundbreaking flexible intermediate bulk container (FIBC) option aimed at securely moving goods and safeguarding bulk materials during transport, all while remaining competitively priced compared to wooden pallets. This innovative solution was primarily created to address the concerns of customers regarding the damage and contamination of FIBC loads, which they identified as a significant requirement.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.11% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type · Type A · Type B · Type C · Type D |

|

By End-use Industry · Chemicals & Fertilizers · Food & Beverages · Building & Construction · Pharmaceutical · Agriculture · Others |

|

|

By Geography · North America (Product Type, End-use Industry, and Country) o U.S. (By End-use Industry) o Canada (By End-use Industry) · Europe (Product Type, End-use Industry, and Country/Sub-region) o Germany (By End-use Industry) o U.K. (By End-use Industry) o France (By End-use Industry) o Spain (By End-use Industry) o Italy (By End-use Industry) o Russia (By End-use Industry) o Poland (By End-use Industry) o Romania (By End-use Industry) o Rest of Europe (By End-use Industry) · Asia Pacific (Product Type, End-use Industry, and Country/Sub-region) o China (By End-use Industry) o Japan (By End-use Industry) o India (By End-use Industry) o Australia (By End-use Industry) o Southeast Asia (By End-use Industry) o Rest of Asia Pacific (By End-use Industry) · Latin America (Product Type, End-use Industry, and Country/Sub-region) o Brazil (By End-use Industry) o Argentina (By End-use Industry) o Mexico (By End-use Industry) o Rest of Latin America (By End-use Industry) · Middle East & Africa (Product Type, End-use Industry, and Country/Sub-region) o Saudi Arabia (By End-use Industry) o UAE (By End-use Industry) o Oman (By End-use Industry) o South Africa (By End-use Industry) · Rest of Middle East & Africa (By End-use Industry) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.63 billion in 2025 and is projected to reach USD 4.87 billion by 2034.

In 2025, the market value stood at USD 2.63 billion.

The market is expected to grow at a CAGR of 7.11% during the forecast period of 2026-2034.

The chemicals & fertilizers segment led the market by end-use industry.

The key factor driving the growth of the market is the rapidly growing e-commerce sector.

Greif Inc., Amcor Plc, Rishi FIBC Solutions Pvt. Ltd., SIA Flexitanks, C.L. Smith, and Southern Packaging, LP are the top players in the market.

Asia Pacific dominates the market.

Increased demand from the chemicals sector is one of the factors that is expected to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us