Fluid Management Systems Market Size, Share & Industry Analysis By Product (Systems {Standalone Systems and Integrated Systems}, and Disposables & Accessories {Catheters, Tubing Sets, Suction Canisters & Liners, Filters & Collection Bags, and Others}), By Application (Urology & Nephrology, Gastroenterology, Gynecology, General Surgery, Orthopedics, Cardiology, ENT, and Others), By End User (Hospitals & ASCs, Dialysis Centers, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

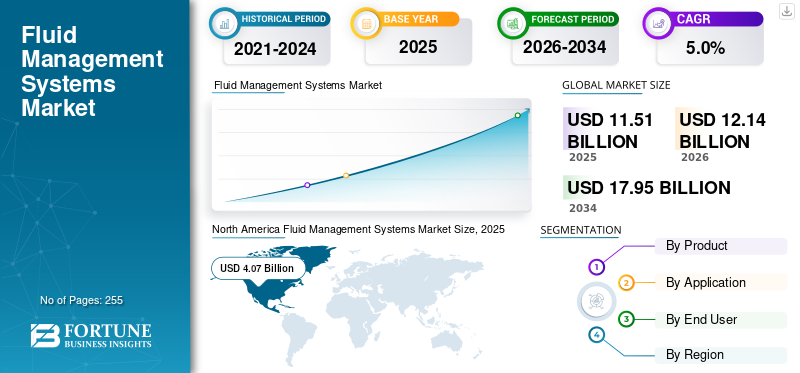

The global fluid management systems market size was valued at USD 11.51 billion in 2025 and is projected to grow from USD 12.14 billion in 2026 to USD 17.95 billion by 2034, exhibiting a CAGR of 5.0% during the forecast period. North America dominated the global fluid management systems market with a market share of 35.4% in 2025.

The fluid management systems are integrated technologies, from simple IV pumps to advanced software, which precisely control, monitor, and track patient fluid intake/output and waste, ensuring accurate delivery of therapies while optimizing surgical cleanup, reducing contamination, and minimizing risks of fluid overload or dehydration for better patient safety and outcomes. The increasing prevalence of chronic conditions, including neurological conditions, cardiovascular conditions, and others, is resulting in a growing number of surgeries among the patient population. The increasing surgical procedures and technological advancements in fluid management systems are further driving the adoption of systems and accessories, thereby contributing to the growth of the market.

- For instance, according to the 2024 data published by the Centers for Disease Control & Prevention (CDC), about 51.4 million inpatient Surgeries are performed in the U.S.

The increasing preference for technologically advanced fluid management systems and accessories contributes to the growing demand for these products in healthcare settings. This, coupled with the rising focus on acquisitions and mergers among key players, is driving the focus of major companies, including Stryker Corporation, Baxter International, B. Braun Melsungen AG, and Medtronic plc, and is expected to support the growth of the global fluid management systems market.

Download Free sample to learn more about this report.

Fluid Management Systems Market Key Takeaways

- 2025 Market Size: USD 11.51 Billion

- 2026 Market Size: USD 12.14 Billion

- 2034 Forecast Market Size: USD 17.95 Billion

- CAGR: 5.0% from 2026–2034

- North America dominated the fluid management systems market with a 35.4% share in 2025.

- The disposables & accessories segment held the largest market share in 2025.

- The urology & nephrology segment accounted for a 35.5% share of the market in 2025.

North America

North America led the market with a value of USD 4.07 billion in 2025 and is projected to reach USD 4.22 billion in 2026.

Europe

Europe is expected to reach USD 3.33 billion in 2026, supported by rising surgical volumes and adoption of advanced fluid management technologies.

Asia Pacific

Asia Pacific is projected to reach USD 3.13 billion in 2026, driven by growing dialysis populations.

U.S.

The fluid management systems market was valued at approximately USD 3.57 billion in 2025.

Japan

The fluid management systems market is estimated to reach USD 0.67 billion in 2026.

Read More

Fluid Management Systems Market Trends

Preferential Shift towards Integrated Surgical Platforms to Boost Product Demand

A defining trend in the global fluid management systems market is the shift toward integrated surgical platforms that unify suction, irrigation, fluid capture, and waste management into centralized, automated systems. Hospitals are increasingly prioritizing OR standardization, and integrated fluid systems provide better workflow coordination and fewer manual touchpoints. Meanwhile, disposable fluid management components such as suction canisters, liners, and tubing sets are benefiting from heightened infection-control vigilance. Following guidelines updated by bodies such as the CDC and ECDC in 2022, healthcare facilities are accelerating their transition to single-use containment products to minimize contamination risks.

Another notable trend is the digitalization of OR equipment. Vendors are incorporating pressure sensors, automated fluid balancing, and real-time data analytics into their platforms to support surgeons during arthroscopy, laparoscopy, and endoscopy. In parallel, the rise of outpatient surgeries and ambulatory surgical centers is reshaping product demand. ASCs favor compact, cost-effective systems and high-turnover consumables, leading to a surge in procedure-specific disposable kits. Finally, sustainability considerations are gradually influencing product development, with manufacturers exploring biodegradable materials or reduced-plastic liner systems to meet hospital environmental targets.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Surgical Volumes Globally to Drive Market Growth

The global fluid management systems market is gaining strong momentum as surgical volumes continue to rise globally. A steadily increasing demand for minimally invasive procedures, estimated to be more than 310 million surgeries performed annually globally, has accelerated the demand for efficient fluid regulation technologies across operating rooms and endoscopy suites. The growing burden of chronic kidney disease (CKD) further reinforces market growth.

- According to the International Society of Nephrology (2023), nearly 850 million people worldwide live with kidney disorders, leading to the consistent use of catheters, tubing sets, and other fluid disposables in dialysis and nephrology care.

Hospitals are also upgrading legacy OR infrastructure to support digital and integrated surgical environments, where automated fluid management plays a key safety role. Infection control remains another compelling driver. Healthcare facilities in the U.S. and Europe have tightened compliance with waste handling and suction liner disposal, encouraging a shift toward closed, disposable systems. Emerging economies, especially in the Asia Pacific, are adding new endoscopy units and expanding GI screening programs, significantly boosting demand for high-volume consumables. Collectively, these clinical and regulatory forces are strengthening the global uptake of both capital equipment and disposable fluid management solutions.

Market Restraints

High Cost Associated with Integrated Operating Room Fluid Management Platforms to Limit the Market Growth

Despite strong underlying demand, the global fluid management systems market faces several limiting forces. High capital costs associated with integrated operating room fluid management platforms continue to deter smaller hospitals and ambulatory centers, particularly in Latin America, Southeast Asia, and parts of Eastern Europe. Many healthcare systems still rely on basic suction devices and non-integrated setups due to limited procurement budgets. Reimbursement constraints further narrow market adoption, especially in developing economies where fluid management consumables are often classified under low-margin general supplies. Compliance with infection control standards introduces additional cost pressures, as hospitals must shift from reusable to single-use liners and tubing, a transition that some centers struggle to justify financially.

Moreover, the presence of commoditized disposable products has intensified price sensitivity, reducing the pricing power of manufacturers. Environmental concerns around the disposal of high-volume plastics and liners may also spur regulatory scrutiny, potentially increasing manufacturers’ compliance burden. These combined economic, regulatory, and logistical factors continue to restrain broader adoption of advanced fluid management systems.

Market Opportunities

Growing Investments to Upgrade Healthcare Infrastructure Leads to New Market Opportunities

The market is entering a promising growth phase as hospitals worldwide modernize their operating rooms and endoscopy suites. A notable opportunity lies in the rapid adoption of integrated and digitally connected operating room ecosystems, where fluid management systems can interface with imaging, suction, and documentation platforms. Healthcare networks are prioritizing technology that enhances workflow efficiency and infection control, two areas where automated fluid regulation offers measurable improvements. Emerging markets represent another substantial opportunity. The Asia Pacific region accounted for more than 40% of new dialysis patient additions in 2023, resulting in sustained demand for catheters, tubing sets, suction liners, and fluid waste management solutions. Expansion of GI screening programs in China, India, and South Korea is increasing the volume of endoscopy procedures, driving recurring disposable usage.

Product innovation also opens new avenues. Manufacturers are exploring closed-loop, sensor-enabled systems that automate suction and irrigation, offering greater precision during minimally invasive surgeries. Sustainability initiatives, such as recyclable liners or reduced-plastic canister designs, can differentiate suppliers and attract healthcare facilities that focus on environmental goals. Strategic partnerships between device manufacturers and hospital networks can further accelerate adoption by offering bundled capital- and consumable-based contracts. Collectively, these trends create a supportive environment for long-term growth.

Market Challenges

Lack of Consistent Guidelines Regarding Infection-Control Protocols to Limit the Market Growth

The fluid management systems market faces several structural challenges that influence both manufacturers and healthcare providers. One of the most significant is the global variability in clinical standards. While North America and Western Europe mandate strict infection-control protocols, many emerging markets lack consistent guidelines, resulting in uneven demand for disposables such as suction liners or sterile tubing sets. The industry also faces increasing scrutiny regarding plastic waste generation, particularly as hospitals worldwide consume millions of disposable canisters and liners each year. Environmental restrictions may pressure manufacturers to redesign products or invest in recycling programs. Supply chain resilience remains an ongoing issue; several manufacturers reported periodic shortages of resin, ABS plastics, and medical-grade polymers from 2021 to 2023, which delayed deliveries of essential disposables.

Competition from low-cost regional players adds another layer of difficulty, compressing margins and making it harder for global companies to differentiate purely on product quality. Addressing these economic, environmental, and regulatory challenges will be essential for sustaining long-term growth.

SEGMENTATION ANALYSIS

By Product

Increasing Shift Toward Minimally Invasive Surgery Led to Disposables & Accessories Segment’s Growth

Based on product, the market is classified into systems and disposables & accessories. Systems are further bifurcated into standalone systems and integrated systems. Additionally, disposables & accessories are further divided into catheters, tubing sets, suction canisters & liners, filters & collection bags, and others.

To know how our report can help streamline your business, Speak to Analyst

The disposables & accessories segment held the largest global fluid management systems market share in 2025. The growth is attributed to the continuous shift toward minimally invasive surgery, the expansion of ASCs, and stronger infection control measures, resulting in higher disposable consumption per procedure. Moreover, dialysis & critical care fluid management lead to higher utilization of disposables & accessories.

- According to the U.S. Renal Data System 2023 Annual Data Report, more than 808,000 people in the U.S are living with End-stage Kidney Disease (ESKD), also known as end-stage renal disease (ESRD), with 68% on dialysis and 32% with a kidney transplant.

The systems segment is expected to grow at a CAGR of 6.7% over the forecast period.

By Application

Increasing Prevalence of Urology & Nephrology Disorders Led to the Dominance of the Segment

Based on application, the market is segmented into urology & nephrology, gastroenterology, gynecology, general surgery, orthopedics, cardiology, ENT, and others.

The urology & nephrology segment dominated the global market in 2025. By application, the urology & nephrology segment held a 35.5% share in 2025. The growth is primarily owing to the increasing prevalence of urology & nephrology disorders is resulting in an expanding number of related procedures among the patient population in the market.

- For instance, according to the National Kidney Foundation, Inc., approximately 10% of the global population is affected by chronic kidney disease (CKD). Over 2 million people worldwide currently receive treatment with dialysis or a kidney transplant to stay alive.

The segment of gynecology is set to flourish with a growth rate of 5.4% across the forecast period.

By End-user

Increasing Prevalence of Several Chronic Disorders Led to Hospitals & ASCs Segment Growth

Based on end-user, the market is segmented into hospitals & ASCs, dialysis centers, specialty clinics, and others.

The hospitals and ASCs segment dominated the market in 2025. The increasing prevalence of several chronic disorders, as well as the growing number of hospitals, are key factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold a 54.0% share in 2026.

- For instance, according to 2025 data published by the American Hospital Association, there are about 6,093 hospitals in the U.S.

Additionally, specialty clinics’ end users are projected to grow at a CAGR of 5.3% during the study period.

Fluid Management Systems Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Fluid Management Systems Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America fluid management systems market held the dominant share in 2025, valued at USD 4.07 billion, and also took the leading share in 2026 with USD 4.22 billion. The dominance of the region is owing to certain factors, such as the growing prevalence of chronic conditions, the adoption of advanced products, and strong reimbursement frameworks for various disorders, among others. High surgical volumes, advanced healthcare infrastructure, and rapid adoption of integrated operating room technologies primarily drive the fluid management systems market growth in North America.

U.S. Fluid Management Systems Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 3.57 billion in 2025, accounting for roughly 31.0% of global hepatitis therapeutics sales.

Europe

Europe is projected to record a growth rate of 4.0% in the coming years, which is the second highest among all regions, and reach a valuation of USD 3.33 billion by 2026. This is due to the growing number of surgical procedures and the adoption of advanced fluid management systems in the region. Europe’s growth is supported by strong public healthcare systems, rising chronic disease burden, and strict infection prevention regulations. Countries such as Germany, France, and the U.K. maintain high volumes of GI endoscopy and urological procedures, fueling steady demand for fluid management consumables.

U.K. Fluid Management Systems Market

The U.K. fluid management systems market in 2025 is estimated to be around USD 0.48 billion, representing approximately 4.1% of global fluid management systems revenues.

Germany Fluid Management Systems Market

Germany’s fluid management systems market is projected to reach approximately USD 0.63 billion in 2025, equivalent to around 5.5% of global fluid management systems sales.

Asia Pacific

Asia Pacific is estimated to reach USD 3.13 billion in 2026 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.52 billion and USD 0.99 billion, respectively, in 2026. China and India account for a significant share of the global chronic kidney disease and dialysis population, creating strong recurring demand for catheters, tubing sets, and fluid disposables.

Japan Fluid Management Systems Market

The Japan fluid management systems market in 2026 is estimated at around USD 0.67 billion, accounting for roughly 5.5% of global fluid management systems revenues.

China Fluid Management Systems Market

China’s fluid management systems market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 0.99 billion, representing roughly 8.1% of global fluid management systems sales.

India Fluid Management Systems Market

The India fluid management systems market in 2026 is estimated at around USD 0.52 billion, accounting for roughly 4.3% of global fluid management systems revenues.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2026 is set to record USD 0.84 billion in its valuation. In Gulf countries such as Saudi Arabia and the UAE, large-scale government investments in advanced hospitals and surgical centers are driving the adoption of integrated fluid and waste management systems. In the Middle East & Africa, GCC is set to attain the value of USD 0.34 billion in 2026.

GCC Fluid Management Systems Market

The GCC fluid management systems market is projected to reach approximately USD 0.34 billion by 2026, accounting for roughly 2.8% of global fluid management systems revenues.

Competitive Landscape

Key Industry Players

Increasing Focus on Advanced Products by the Prominent Companies to Support Their Dominance

The global fluid management systems market is moderately consolidated, with a mix of large multinational medical device companies and specialized regional players. Leading companies maintain strong positions by offering end-to-end portfolios that combine capital systems with high-margin consumables such as tubing sets, catheters, suction canisters, and liners. This model enables players to secure long-term contracts through installed systems, generating recurring revenue from disposables. Stryker Corporation, Baxter International, B. Braun Melsungen AG, and Medtronic plc are prominent companies in the market in 2025.

- For instance, in March 2022, STERIS Corporation received FDA 510(k) clearance for its ENDOGATOR Endoscopy Irrigation Tubing is indicated for irrigation during endoscopic procedures.

Other key players, including Fresenius Medical Care, Johnson & Johnson, Olympus Corporation, ConvaTec Group, and others, are also expanding in the market, primarily due to their increasing emphasis on R&D activities to develop advanced products and strengthen their market presence.

List of Key Fluid Management Systems Companies Profiled

- Stryker Corporation (U.S.)

- Baxter International (U.S.)

- Braun Melsungen AG (Germany)

- Medtronic plc (Ireland)

- Fresenius Medical Care (Germany)

- Johnson & Johnson (U.S.)

- Olympus Corporation (Japan)

- ConvaTec Group (U.K.)

- Getinge AB (Sweden)

- Smith+Nephew (U.K.)

KEY INDUSTRY DEVELOPMENTS

- March 2025 - DeRoyal Industries, Inc., a leader in innovative healthcare products and solutions, announced the acquisition of Skyline Medical’s Streamway Wall Suction Waste Fluid Management product line and related assets.

- August 2024 - Baxter International Inc., a global medtech leader, and global investment firm Carlyle today announced that they have signed a definitive agreement under which Carlyle is to acquire Baxter’s Kidney Care segment, to be named Vantive, for $3.8 billion.

- July 2024 - Hologic received FDA 510(k) clearance for its Fluent Pro Fluid Management System, classifying it as a Class II device (Insufflator, Hysteroscopic) used to manage fluid during hysteroscopic procedures.

- January 2024 - Minerva Surgical, Inc. received FDA 510(k) clearance for its Symphion Operative Hysteroscopy System and accessories that are intended for resection and coagulation of uterine tissue, such as intrauterine polyps and myomas.

- August 2023 – Medivators received FDA 510(k) clearance for its ENDOGATOR Hybrid Irrigation Tubing is intended to provide irrigation during GI endoscopic procedures.

REPORT COVERAGE

The market report provides a detailed global fluid management systems market analysis and focuses on key aspects such as leading companies, product, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.0% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Application, End User, and Region |

|

By Product |

· Systems o Standalone Systems o Integrated Systems · Disposables & Accessories o Catheters o Tubing Sets o Suction Canisters & Liners o Filters & Collection Bags o Others |

|

By Application |

· Urology & Nephrology · Gastroenterology · Gynecology · General Surgery · Orthopedics · Cardiology · ENT · Others |

|

By End User |

· Hospitals and ASCs · Dialysis Centers · Specialty Clinics · Others |

|

By Region |

· North America (By Product, By Application, By End User, and by Country) o U.S. (By Application) o Canada (By Application) · Europe (By Product, By Application, By End User, and by Country/Sub-region) o U.K. (By Application) o Germany (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Scandinavia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Product, By Application, By End User, and by Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o Australia (By Application) o Southeast Asia (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Product, By Application, By End User, and by Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Product, By Application, By End User, and by Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 11.51 billion in 2025 and is projected to reach USD 17.95 billion by 2034.

In 2025, the North America regional market value stood at USD 4.07 billion.

Growing at a CAGR of 5.0%, the market will exhibit steady growth over the forecast period (2026-2034).

By product, the disposables & accessories systems segment is the leading segment in this market.

The increasing surgical procedures is one of the major factors driving the market's growth.

Stryker Corporation, Baxter International, B. Braun Melsungen AG, and Medtronic plc are the major players in the global market.

North America dominated the market share in 2025.

The growing number of surgical procedures, increasing product launches, and new product approvals, among others, are some of the vital factors expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 255

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us