Foam Insulation Market Size, Share & Industry Analysis, By Material Type (Polystyrene, Polyurethane, Polyisocyanurate, Phenolic, and Others), By End-Use Industry (Building & Construction, Consumer Appliances, Transportation, and Others), and Regional Forecast, 2026-2034

Foam Insulation Market Size and Future Outlook

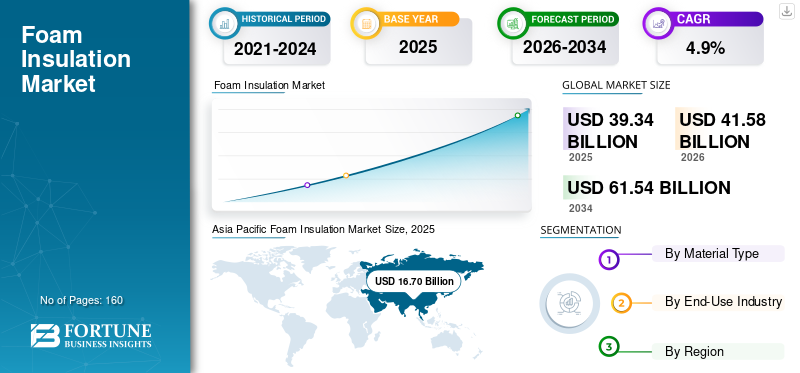

The global foam insulation market size was valued at USD 39.34 billion in 2025. The market is projected to grow from USD 41.58 billion in 2026 to USD 61.54 billion by 2034, exhibiting a CAGR of 4.9% during the forecast period. Asia Pacific dominated the foam insulation market with a market share of 42.45% in 2025.

Foam insulation refers to polymeric insulation materials used to reduce heat transfer in buildings and industrial systems. It is supplied primarily as rigid boards and panels (EPS, XPS, PU, and PIR, phenolic), spray polyurethane foam systems, and specialty forms used in refrigeration and technical insulation. Performance is determined by thermal conductivity, compressive strength, dimensional stability, moisture resistance, and compliance with fire and building codes.

The market growth is driven by building energy-efficiency requirements, ongoing retrofit activity in mature economies, and expanding construction in emerging regions. The market demand is further supported by growth in the cold chain and refrigeration, where PU-based foams are widely used. At the same time, regulatory scrutiny around fire performance and environmental compliance (including blowing agent transitions and product certifications) continues to shape product design and adoption pathways.

Furthermore, the market comprises several major players, including Kingspan, Dow, Owens Corning, Huntsman Building Solutions, Johns Manville, and BASF. Broad product portfolios, technical differentiation, and expanded manufacturing and distribution footprints support these companies' competitive positioning in the global market.

Download Free sample to learn more about this report.

Foam Insulation Market Key Takeaways

- 2025 Market Size: USD 39.34 billion

- 2026 Market Size: USD 41.58 billion

- 2034 Forecast Market Size: USD 61.54 billion

- CAGR: 4.9% from 2026–2034

- Asia Pacific dominated the foam insulation market with a 42.45% share in 2025.

- The polystyrene segment accounted for 48.7% of the global market share in 2025.

- The building & construction segment held the largest market share of 71.9% in 2025.

Asia Pacific

Asia Pacific generated USD 16.70 billion in revenue in 2025 and is projected to reach USD 17.81 billion in 2026.

Europe

Europe is expected to reach USD 9.05 billion in 2026.

North America

North America is projected to reach USD 7.62 billion in 2026.

U.S.

The U.S. foam insulation market was valued at USD 6.13 billion in 2025.

Japan

Japan's market driven by demand for high-performance insulation materials in residential, commercial, and industrial applications.

Read More

FOAM INSULATION MARKET TRENDS

Energy-Efficiency Regulations, Building Retrofits, and Product Compliance Upgrades are Significant Market Trends

Foam insulation demand is increasingly shaped by energy-efficiency policies that prioritize reduced heating and cooling loads, particularly in building envelopes. Regulatory pathways in major regions are pushing higher insulation performance and better documentation of installed performance, accelerating the adoption of higher-R-value materials and system solutions that reduce thermal bridging. In parallel, manufacturers continue to optimize formulations and face transitions in blowing agents and compliance documentation, which influence product positioning across residential, commercial, and industrial segments.

Alongside building efficiency policy, fire performance, and code compliance requirements are influencing product testing, labeling, and selection, especially for facade and high-rise applications. This is increasing attention on system-level certification, installation quality, and application-specific product selection. As retrofit markets expand, demand is also rising for solutions that enable fast installation with minimal disruption, including rigid boards, insulated panels, and spray foam systems for complex geometries.

- For instance, the revised EU Energy Performance of Buildings Directive (EPBD) entered into force on 28 May 2024 and must be transposed by 29 May 2026, supporting multi-year renovation activity and insulation demand.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Building Energy Codes, Retrofit Activity, and Cold-Chain Insulation Needs are Driving Market Growth

Building and construction remains the largest demand center for foam insulation market growth, supported by energy codes and the practical need to lower operating costs by reducing heat losses and gains. Rigid foam boards and insulated panels are widely used in roofs, walls, floors, and foundations where high thermal resistance per thickness and moisture resistance are valued. In addition, the growth of prefabricated construction and industrialized building methods is increasing the usage of foam-core insulated panels for speed and performance consistency.

Outside building envelopes, polyurethane-based foams are structurally important in refrigeration, cold storage, and transport refrigeration applications where stable insulation performance helps maintain temperature control. Rising cold-chain requirements in food and pharmaceuticals support steady demand for foam insulation systems and panels. In industrial facilities, technical insulation demand is also linked to process temperature management, energy efficiency, and condensation control.

- For instance, the IEA notes that high-performing building envelopes are among the most effective ways to reduce buildings' thermal needs, reinforcing insulation as a key efficiency lever.

MARKET RESTRAINTS

Fire Safety Scrutiny, Code Complexity, and Material Compliance Costs Can Restrict Market Expansion

The market faces constraint linked to fire performance scrutiny and varying code requirements across jurisdictions. Compliance requirements can vary by application (roofs, facades, cavities) and by building type, increasing the cost of product testing, certification, and system approvals. In addition, reputational risk and liability considerations can influence specification decisions, particularly for high-rise or facade applications.

Cost volatility in key petrochemical feedstocks and additives can also create pricing uncertainty and influence material selection across foam types. In cost-sensitive markets, buyers may down-specify thickness, shift between foam chemistries, or switch to non-foam alternatives depending on project economics and availability. Supply chain disruptions can further affect lead times for boards, panels, and spray foam systems.

- For instance, major suppliers frequently cite input cost volatility and supply-chain conditions as drivers of pricing actions and margin management in insulation businesses.

MARKET OPPORTUNITIES

Deep Retrofit Programs, High-Performance Building Envelopes, and Industrial Cold-Chain Expansion are Creating Lucrative Opportunities

Deep retrofit programs in mature markets are creating a multi-year opportunity for foam insulation, particularly where policy incentives support high-performance envelopes and electrification of heating. Higher-performance building targets increase demand for materials that deliver more thermal resistance per thickness, enabling design flexibility while meeting stringent energy targets. Manufacturers with strong technical support, system certifications, and installer networks are better positioned to capture these opportunities.

Cold-chain expansion and the growth of temperature-controlled logistics also create long-duration demand for foam insulation in insulated panels, cold rooms, and transport refrigeration. In parallel, industrial users continue to demand reliable technical insulation to achieve energy savings and control condensation in process plants and commercial refrigeration facilities. Product innovation focused on lower environmental impact and improved compliance documentation can further widen addressable applications.

- For example, EPBD implementation timelines are expected to increase renovation activity across the European Union, which can expand demand for insulation materials used in retrofit applications.

MARKET CHALLENGES

Regulatory Compliance, Application Industry-Specific Performance, and Installation Quality Control can Hamper Market Growth

A key challenge in foam insulation is navigating evolving regulatory frameworks that address energy efficiency, fire safety, and environmental compliance simultaneously. This increases complexity in product development and the cost of maintaining multiple compliant product lines across regions. Manufacturers must also respond to market-specific requirements for vapor control, compressive strength, and long-term dimensional stability.

Installation quality remains a critical determinant of realized performance, particularly for spray foam systems and assemblies where air leakage control is a major part of the value proposition. Poor installation can reduce performance and raise warranty or safety risks, reinforcing the need for trained installers, quality assurance programs, and system-level guidance. In markets with fragmented contracting ecosystems, maintaining consistent installation quality can be difficult.

- For instance, leading suppliers emphasize system solutions and installer/contractor support to ensure performance and compliance across applications.

Segmentation Analysis

By Material Type

Rising Adoption of Insulated Building Shells in Mid-Rise Housing Led to Dominance of Polystyrene Segment

Based on material type, the market is segmented into polystyrene, polyurethane, polyisocyanurate, phenolic, and others.

The polystyrene segment accounted for the largest foam insulation market share of 48.7% in 2025. The segment’s growth is driven by urban construction, rising adoption of insulated building shells in mid-rise housing, and continued focus on lifecycle durability in foundations and external insulation systems. The segment also benefits from standardized board formats and mature distribution networks that make it easier for contractors and developers to specify and install at scale.

The polyurethane segment is expected to grow significantly, supported by roof and wall insulation requirements that prioritize thermal efficiency upgrades. In non-building applications, PU remains structurally important for refrigerators/freezers and select cold-chain applications as it can be foamed in place to improve thermal performance and dimensional fit. Growth is also reinforced by the need for lower operating energy in cooled environments and demand for higher-performing building envelopes. The polyurethane segment is projected to grow at a 4.8% CAGR during the study period.

The polyisocyanurate segment is projected to grow significantly in the coming years. The segment’s growth is driven by increasing adoption of energy-efficient roofing systems and the large installed base of commercial roofs undergoing refurbishment. PIR boards also see demand where long-term thermal stability and durability are critical. Manufacturers’ product development and broader availability of faced boards (for roofing and wall systems) further support uptake in professional construction channels.

The phenolic segment is also expected to grow favorably over the projected period due to higher costs and a narrower supply base; it can grow faster in niches driven by stricter building safety standards, higher penetration of HVAC duct insulation solutions, and demand for performance-driven insulation in public and commercial buildings.

By End-Use Industry

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Segment Dominated Market Due to Extensive Use of Product

By end-use industry, the market is categorized into building & construction, consumer appliances, transportation, and other sectors.

The building & construction segment accounted for the largest share of 71.9% in 2025. The segment's growth is driven by energy-efficiency regulations, consumer preference for lower operating costs, and broader acceptance of insulation as a cost-effective pathway to improved building performance. In emerging regions, continued urbanization and infrastructure expansion further strengthen demand for cost-effective insulation materials.

The consumer appliances segment is also expected to grow favorably over the projected period. The segment's demand is driven by rising household refrigeration penetration in developing economies, replacement demand in mature markets, and continued pressure to improve appliance energy efficiency. In addition, the growth of cold storage and temperature-controlled systems often supports broader demand for foam-based insulation in related equipment. The segment is expected to grow at a CAGR of 4.9% over the forecast period.

The transportation segment is anticipated to grow at a moderate pace during the forecast period. The growth is supported by the expansion of temperature-controlled food and pharmaceutical supply chains, increasing e-commerce grocery penetration in some regions, and rising expectations for reliable cold logistics.

Foam Insulation Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Foam Insulation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 16.70 billion, and is expected to maintain its leading share in 2026, valuing at USD 17.81 billion. The region benefits from construction intensity, expanding urban infrastructure, and growing demand for cold-chain and refrigeration insulation. China remains the largest consumption base, while India and Southeast Asia continue to increase demand linked to housing, commercial development, and logistics expansion.

China Foam Insulation Market

In 2025, the China market reached a valuation of USD 7.84 billion. China’s market demand is supported by large-scale construction activity, infrastructure programs, and the widespread use of EPS and XPS boards in construction applications.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 7.62 billion by 2026. The market’s growth is driven by residential renovation, commercial construction, and energy-code adoption across states and provinces. Foam boards and spray foam systems remain widely used across roofing, wall assemblies, and foundations.

U.S. Foam Insulation Market

In 2025, the U.S. market reached a valuation of USD 6.13 billion. The U.S. dominates regional consumption due to its large building stock, high new construction volume, and broad adoption of foam boards and spray foam for performance upgrades.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at a 4.9% rate and reach a valuation of USD 9.05 billion in 2026. The market’s growth is supported by building renovation activity, established insulation standards, and policy-driven efficiency targets. The region benefits from mature manufacturing and distribution networks and a strong focus on system-level compliance and performance documentation.

U.K. Foam Insulation Market

The U.K. market was valued at around USD 1.67 billion in 2025, representing approximately 4.4% of global market revenue.

Germany Foam Insulation Market

Germany’s market reached a valuation of approximately USD 1.59 billion in 2025, equivalent to around 5.9% of global sales.

Latin America

Latin America is experiencing steady growth. The Latin America market in 2026 is expected to reach a valuation of USD 2.97 billion. The demand is concentrated in building and construction applications, with variability across countries depending on construction cycles, insulation adoption, and availability of local foam board supply.

Brazil Foam Insulation Market

Brazil’s market reached a valuation of approximately USD 1.30 billion in 2025, equivalent to around 3.6% of global sales.

Middle East & Africa

The Middle East & Africa region is gradually expanding, driven by project-driven construction in GCC markets, industrial facilities, and growing cold-chain needs. Harsh climatic conditions and cooling demand reinforce the value proposition of thermal insulation in commercial and residential buildings.

GCC Foam Insulation Market

GCC reached USD 1.83 billion in 2025, accounting for approximately 3.5% of global revenues. GCC demand is supported by large-scale commercial construction, industrial projects, and cooling-driven energy efficiency requirements.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Expanding Deposits, Processing Footprints, and Specialty Grades to Maintain their Positions in Market

The market includes a mix of global insulation manufacturers, chemical companies supplying foam systems and raw materials, and regional board and panel producers. Competition is shaped by thermal performance, compliance and certifications, supply reliability, installer support, and the ability to provide system solutions across multiple building applications. Leading companies differentiate through advanced formulations, insulated panel systems, and technical services that support specification and installation quality. Some of the key market players include Kingspan, Dow, Owens Corning, Huntsman Building Solutions, Johns Manville, and BASF.

LIST OF KEY FOAM INSULATION COMPANIES PROFILED IN REPORT

- Kingspan (Ireland)

- Dow (U.S.)

- Polymer Technologies, Inc. (U.S.)

- Owens Corning (U.S.)

- SOPREMA (France)

- Huntsman Building Solutions (U.S.)

- Johns Manville (U.S.)

- BASF (Germany)

- Covestro (Germany)

- TRIPAK MHS SOLUTIONS PVT. LTD. (India)

- Rogers Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Recticel announced it would acquire a controlling stake in Miclar Group, a specialist in façade/roof cladding and components, signalling a push toward integrated insulated panel solutions and tighter downstream capability in the insulated panels market.

- April 2022: Recticel completed the acquisition of Trimo, a producer of insulated panels for construction, signalling portfolio expansion from PIR insulation boards into premium insulated panels and greater exposure to high-performance envelope systems (including cold-chain and industrial building applications).

- October 2021: Covestro launched/coordinated the “CIRCULAR FOAM” project with multiple partners to develop recycling pathways for rigid Polyurethane (PU) foams used in refrigerators and buildings, signalling a shift toward circularity-enabled insulation materials and end-of-life solutions for PU rigid foams.

- May 2021: Kingspan highlighted upgrades and sustainability initiatives at its Modesto, California, manufacturing facility (including incorporating recycled content initiatives under “Planet Passionate”), signalling ongoing modernization of insulated panel manufacturing and stronger sustainability positioning for panel/foam-based building envelope products.

- December 2020: Recticel announced the acquisition of Gór-Stal’s PIR insulation board business (termPIR) in Bochnia (Poland), signalling capacity-backed expansion into Central & Eastern Europe and a broader footprint in PIR rigid foam board insulation.

- February 2020: Huntsman completed the acquisition of Icynene-Lapolla, a North American manufacturer and distributor of Spray Polyurethane Foam (SPF) insulation systems, signalling deeper downstream integration into building-envelope solutions and a stronger presence in residential/commercial SPF channels.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.9% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Material Type, End-Use Industry, and Region |

| By Material Type |

|

| By End-Use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 39.34 billion in 2025 and is projected to reach USD 61.54 billion by 2034.

Recording a CAGR of 4.9%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building & construction end-use industry segment led in 2025.

Asia Pacific held the highest market share in 2025.

Kingspan, Dow, Owens Corning, Huntsman Building Solutions, Johns Manville, and BASF are some of the prominent players in the market.

The growth is driven by tightening building-energy performance requirements, which push higher insulation levels in new construction and retrofit to cut heating/cooling demand and operating costs.

The major factors expected to favor product adoption in the market is favored for its high thermal efficiency per thickness, broad availability in rigid boards and spray systems, and rising demand for better building envelopes, cold-chain/refrigeration efficiency, and HVAC/mechanical insulation.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us