Food Packaging Films Market Size, Share & Industry Analysis, By Material (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl chloride (PVC), and Others), By Type (Flexible Films and Rigid Films), By Application (Meat, Poultry & Seafood, Fresh Produce, Ready-to-Eat Meals, Bakery & Confectionery, Dairy Products, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

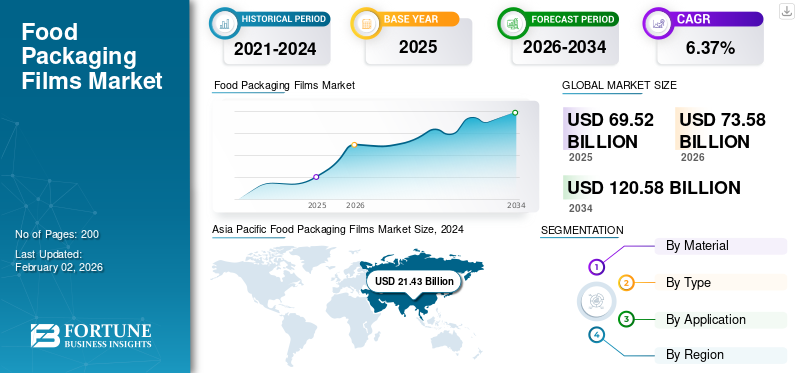

The global food packaging films market size was valued at USD 69.52 billion in 2025. The market is projected to grow from USD 73.58 billion in 2026 to USD 120.58 billion by 2034, exhibiting a CAGR of 6.37% during the forecast period. Asia Pacific dominated the food packaging films market with a market share of 30.83% in 2025.

Food packaging films are thin, flexible sheets used to enclose or safeguard food items, serving as a protective barrier against moisture, oxygen, dirt, and contaminants to prolong shelf life, preserve quality, and improve presentation. The main advantages include extended freshness and safety by preventing spoilage, enhanced product attractiveness for branding with improved appearance, and decreased food waste through longer shelf life.

Innovative, sustainable alternatives, such as biodegradable and eco-friendly packaging films made from plant-derived materials or milk proteins, are being introduced to provide environmental benefits while still offering effective food protection, thereby promoting market growth.

Furthermore, the market encompasses several major players Amcor Plc, Sealed Air, and Mondi, at the forefront. Broad portfolio with innovative product launch, and strong geographic presence expansion have supported the dominance of these companies in the global market.

Download Free sample to learn more about this report.

Food Packaging Films Market Key Takeaways

- 2025 Market Size: USD 69.52 billion

- 2026 Market Size: USD 73.58 billion

- 2034 Forecast Market Size: USD 120.58 billion

- CAGR: 6.37% from 2026–2034

- Asia Pacific dominated the food packaging films market with a 30.83% share in 2025.

- The flexible films segment is projected to account for 63.21% of the market share in 2026.

- The meat, poultry, and seafood application segment is expected to hold 36.15% of the global market share in 2026.

Asia Pacific

Asia Pacific generated USD 21.43 billion in revenue in 2025 and is projected to reach USD 22.87 billion in 2026.

North America

North America accounted for 28.93% of the global market in 2025 and is expected to reach USD 21.30 billion in 2026.

Europe

Europe captured 22.22% of global revenue in 2025 and is projected to reach USD 16.31 billion in 2026.

U.S.

The U.S. food packaging films market was valued at USD 16.79 billion in 2025.

Japan

Japan's is projected to witness the fastest growth during the forecast period.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growth of Online Food Delivery & Rising Demand for Convenience & Packaged Foods Drives the Market Growth

The rising trend among consumers toward ready-to-eat, frozen, and processed foods significantly influences the market. The demand for practical, lightweight, and robust packaging films is being driven by hectic lifestyles, urban development, and a growing workforce in both advanced and emerging economies. The rising trend among consumers toward ready-to-eat, frozen, and processed foods augments the market growth. The demand for practical, lightweight, and robust packaging films is being driven by hectic lifestyles, urban development, and a growing workforce in both advanced and emerging economies. It thus drives the global food packaging films market growth.

MARKET RESTRAINTS

Stringent Regulations on Plastics Hampers Market Growth

One of the major restraints for the market is growing regulatory constraints regarding plastic use. Authorities in Europe, North America, and select regions in Asia are implementing bans or stringent restrictions on single-use plastics, which encompass various traditional food packaging films. These regulations compel manufacturers to rethink their products, allocate resources toward sustainable options, and navigate intricate legal requirements, all of which increase expenses and hinder product adoption.

MARKET OPPORTUNITIES

Growth of Ready-to-Eat & Frozen Food Creates Lucrative Growth Opportunities

Lifestyle changes and expansion of contemporary retail outlets are fueling an increase in the consumption of ready-to-eat meals, frozen foods, and snacks. This market segment presents steady growth opportunities for flexible films that provide convenience and preservation. Additionally, categories of frozen foods such as meat, poultry, seafood, vegetables, and pre-prepared meals depend significantly on robust films that endure extreme cold without cracking or compromising their integrity. The growth of modern retail platforms and e-commerce grocery delivery also propels this trend, as films protect food products during storage, handling, and last-mile delivery.

MARKET CHALLENGES

Recycling Complexity of Multilayer Films & Regulatory Pressure Challenges Market Growth

Global regulations aimed at reducing single-use plastics present a significant hurdle for the food packaging films industry. Meeting sustainability requirements necessitates expensive material innovations and redesigns. Although multilayer barrier films are sought after for prolonging shelf life, they create considerable recycling issues due to blend of various polymers. The absence of adequate recycling infrastructure further complicates the situation, thus challenging the market growth.

FOOD PACKAGING FILMS MARKET TRENDS

Integration of Smart, Active, and Compostable Films Booms as a Market Trend

There is a significant trend in the industry toward replacing conventional plastics such as PE and PP with bio based films created from PLA, PHA, and starch blends. These environmental friendly options resonate with worldwide sustainability initiatives and consumer preferences for more sustainable products. In the food industry, innovations such as anti-fog, antimicrobial, and temperature-sensitive films, and advanced packaging solutions are gaining popularity. These films contribute to better food quality monitoring, improve safety, and serve the premium and perishable food sector.

Download Free sample to learn more about this report.

Segmentation Analysis

By Material

Remarkable Benefits Offered by Polyethylene Material Boosts Segment Growth

In terms of material, the market is categorized into polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polyvinyl chloride (PVC), polyester (PET), and others.

The polyethylene (PE) segment captured the largest food packaging films share in 2025. In 2026, the segment is anticipated to dominate with a 41.47% share. Polyethylene (PE) packaging materials provide outstanding value, resilience, and adaptability, acting as a robust barrier against moisture that prolongs shelf life and safeguards food from contamination. It is a safe, non-toxic, and multifunctional material, sanctioned by the FDA, that can be tailored to meet specific packaging requirements. Its lightweight characteristics lower shipping expenses, and heat-sealing capability streamlines the packaging operations.

The polypropylene (PP) material segment is expected to grow at a CAGR of 6.26% over the forecast period.

By Type

Outstanding Properties of Flexible Films Propel Segment Growth

In terms of type, the market is categorized into flexible films and rigid films.

The flexible films segment captured the largest food packaging films market share in 2025. In 2026, the segment is anticipated to dominate with a 63.21% share. Consumers want convenient, modern packaging solutions, and sustainable options, which flexible films provide due to their lightweight nature, barrier properties, and ability to be formed into pouches, bags, and other formats. Flexible films are essential for protecting food from damage, spoilage, and external factors such as light, air, and microorganisms, extending shelf life.

The rigid films packaging type segment is expected to grow at a CAGR of 5.70% over the forecast period.

By Application

Rising Utilization of Films for Meat & Seafood Drives Segment’s Growth

Based on application, the market is segmented into meat, poultry & seafood, fresh produce, ready-to-eat meals, bakery & confectionery, dairy products, and others.

In 2025, the global market was dominated by meat, poultry, and seafood in terms of application. Furthermore, the segment is set to hold a 36.15% share in 2026. The meat and seafood sector is experiencing a strong and increasing demand for food packaging films. This is fueled by the desire for longer shelf life, better protection, and a growing preference for convenient, fresh, and frozen products. Flexible films represent a significant packaging category, with growth further driven by heightened consumer awareness regarding food safety and the pursuit of sustainable, mono-material solutions. Additionally, packaging technologies such as modified atmosphere packaging (MAP) and active/intelligent films are playing a role in the expansion of market.

To know how our report can help streamline your business, Speak to Analyst

In addition, the fresh produce application is projected to grow at a CAGR of 6.39% during the study period.

Food Packaging Films Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific Food Packaging Films Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

The market in Asia Pacific reached USD 21.43 billion in 2025, representing 30.83% of total market revenue, and is projected to reach USD 22.87 billion in 2026. Asia Pacific dominated the market owing to several factors. The increasing popularity of online food delivery services such as Meituan, Zomato, and Grab is driving the demand for flexible and lightweight film packaging. Although cost-efficient plastics such as BOPP, PET, and PE films are prevalent in the market, regional governments are progressively implementing regulations to limit single-use plastics, creating a greater demand for recyclable and biodegradable film options. Snack foods, dairy products, frozen dinners, and convenience meals are experiencing a growing demand in nations such as China, India, and areas of Southeast Asia, thus driving the Asia Pacific market growth. In the region, India and China are both estimated to reach USD 6.16 and USD 7.44 billion each in 2026.

North America

The North America market was valued at USD 20.11 billion in 2025, capturing 28.93% of global revenue, and is estimated to reach USD 21.3 billion in 2026. Other regions, such as North America and Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, the North American region is projected to record a growth rate of 5.29%, which is the second highest amongst all the regions, and reach a valuation of USD 2.48 billion in 2025. In North America, the market for food packaging films is being fueled by an increasing consumer demand for convenience and ready-to-eat options, as frozen meals, meal kits, and single-serving packages become commonplace. In 2025, the U.S. market is estimated to reach USD 16.79 billion.

Europe

In 2025, Europe held 22.22% of the global market, reaching a valuation of USD 15.45 billion, and is projected to grow to USD 16.31 billion in 2026. and secure a position of third-largest region in the market. In Europe, the key factors contributing to market growth are regulatory measures and increased consumer awareness of environmental issues. The EU's stringent directive on single-use plastics and its circular economy objectives are compelling manufacturers to implement recyclable, compostable, and mono-material films. Leading food companies such as Nestlé, Unilever, and Danone are pledging to ensure that their packaging is 100% recyclable by 2030, which is driving the demand for sustainable packaging solutions. Backed by these factors, countries including the U.K. are expected to record the valuation of USD 3.15 billion, Germany to record USD 3.6 billion, and France to record USD 2.39 billion in 2025.

Latin America and the Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 5.57 billion, representing 8.01% of global demand, and is projected to grow to USD 5.8 billion in 2026. Over the forecast period, Latin America and the Middle East & Africa regions would witness a moderate growth. The Latin America market in 2025 is set to record USD 6.95 billion as its valuation. The regions are experiencing substantial growth in food packaging films, attributed to a growing middle-class population and greater urbanization. There is a noticeable shift among consumers toward packaged and processed foods, which has led to a higher demand for economical and adaptable packaging solutions. In particular, the utilization of films in the region is being propelled by snacks, confectionery, bakery items, and dairy products. South Africa is set to attain the value of USD 1.39 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

A Wide Range of Product Offerings Supports Their Leading Position

The global market shows a semi-concentrated structure with numerous small-to-mid-size companies actively operating across the globe. These players are involved in product innovation, strategic partnerships, and geographic expansion.

Amcor Plc, Sealed Air, and Mondi are some of the dominating players in the market. A comprehensive range of food packaging films products, global presence through a strong distribution network, and collaborations with research and academic institutes are a few characteristics of these key players that support their dominance.

Apart from this, other prominent players in the market include Winpak Holdings Inc., Constantia Flexibles, Profol GmbH, and others. These companies are undertaking various strategic initiatives, such as investments in R&D and partnerships with pharmaceutical companies to enhance their market presence.

LIST OF KEY FOOD PACKAGING FILMS COMPANIES PROFILED

- Amcor Plc (Switzerland)

- Sealed Air (U.S.)

- Mondi (U.K.)

- Winpak Holdings Inc. (Canada)

- Constantia Flexibles (Austria)

- Profol GmbH (Germany)

- Glenroy Inc. (U.S.)

- Cosmo Films (India)

- TedPack Company Limited (China)

- Dunmore (U.S.)

- Toppan Printing Co., Ltd. (Japan)

- KM Packaging Services Ltd. (U.K.)

- Trioworld (Sweden)

- UFlex Limited (India)

- Innovia Films (U.K.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: TIPA broadened its product range to incorporate four new high-barrier films and laminate options, aiming to provide compostable substitutes while maintaining performance, barrier properties, and compatibility with machinery. Major uses include single-serve and sachet formats, chips, protein and beverage powders, nutraceuticals including vitamins and gummies, as well as ground coffee and tea.

- December 2024: Berry Global Group, Inc. partnered with VOID Technologies to launch a new advanced polyethylene (PE) film aimed specifically at pet food packaging. This cutting-edge film offers improved strength, durability, and resistance to punctures, making it an entirely PE solution that is appropriate for store drop-off recycling and assists in removing troublesome non-recyclable components.

- June 2024: Crocco, a company specializing in flexible packaging, partnered with Versalis, the chemical division of Eni, to create a food packaging film. This film is created using materials that are partially sourced from the recycling of post-consumer plastics, aiming for large-scale production for the retail market.

- March 2024: INEOS and its collaborators introduced new film packaging made with 50% recycled plastic. This packaging is created by transforming plastic waste into materials suitable for food packaging. A number of partners within the flexible food packaging supply chain have collaborated to unveil new high-quality snack packaging that includes 50% recycled plastic and complies with strict food contact standards.

- February 2022: Cosmo Films Ltd., a worldwide leader in specialty films designed for flexible packaging, labeling, and lamination applications, along with synthetic paper, has introduced a white Cast Polypropylene (CPP) Film featuring a high Coefficient of Friction (COF). With a thickness ranging from 25 to 40 microns, this film removes the necessity for white ink. It is ideal for flexible packaging used in the lamination of noodles, biscuits, snacks, and various bakery items.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.37% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Type, Application, and Region |

|

By Material |

· Polyethylene (PE) · Polypropylene (PP) · Polyethylene Terephthalate (PET) · Polyvinyl chloride (PVC) · Others |

|

By Type |

· Flexible Films · Rigid Films |

|

By Application |

· Meat, Poultry & Seafood · Fresh Produce · Ready-to-Eat Meals · Bakery & Confectionery · Dairy Products · Others |

|

By Geography |

· North America (By Material, Type, Application, and Country/Sub-region) o U.S. o Canada · Europe (By Material, Type, Application, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Type, Application, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Type, Application, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Type, Application, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

The global food packaging films market size was valued at USD 69.52 billion in 2025. The market is projected to grow from USD 73.58 billion in 2026 to USD 120.58 billion by 2034, exhibiting a CAGR of 6.37% during the forecast period.

In 2025, the market value stood at USD 69.52 billion.

The market is expected to exhibit a CAGR of 6.37% during the forecast period of 2026-2034.

The flexible films segment led the market by type.

The key factors driving the market growth is the growth of online food delivery & rising demand for convenience & packaged foods.

Amcor, Klockner Pentaplast, Wipak Group, Sealed Air, Constantia Flexibles, and Honeywell International, Inc., are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Increase in demand from the food sector is one of the factors that are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us