Gastrointestinal Bleeding Treatment Market Size, Share & Industry Analysis, By Treatment Type (Proton Pump Inhibitors (PPIs), Vasoactive Drugs, Non-selective beta-blockers, Anticoagulant, and Others), By GI Tract Division (Upper and Lower), By Type (Acute and Chronic), By Route of Administration (Oral and Parenteral), By Distribution Channel (Hospitals Pharmacies, Retail Pharmacies & Drug Stores, and Online Pharmacies), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

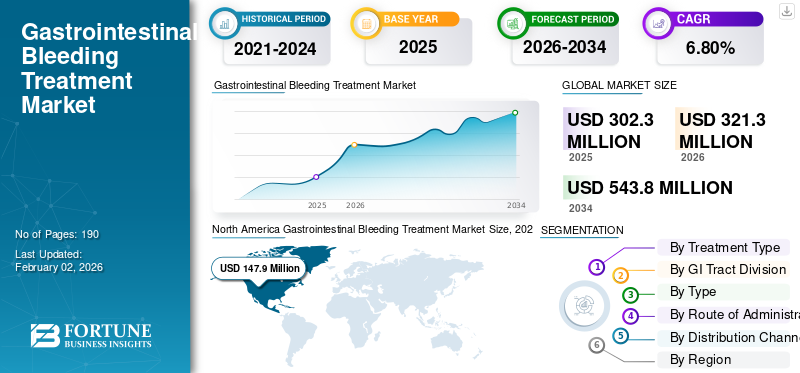

The global gastrointestinal bleeding treatment market size was valued at USD 302.3 million in 2025. The market is projected to grow from USD 321.3 million in 2026 to USD 543.8 million by 2034, exhibiting a CAGR of 6.80% during the forecast period. North America dominated the global market with a share of 48.92% in 2025.

The global gastrointestinal bleeding treatment market has been experiencing growth in recent years. The growth of the global gastrointestinal bleeding treatment market is attributed to rising incidences of gastrointestinal bleeding and frequent use of painkillers. Key companies operating in the market are developing innovative solutions to offer a treatment regimen for bleeding episodes. Additionally, robust support from regulatory bodies and rapid approvals for new drugs further strengthen market growth.

- For instance, in May 2022, Phathom Pharmaceuticals, Inc., a company focused on developing novel treatments for gastrointestinal diseases, announced it received approval from the U.S. FDA for VOQUEZNA TRIPLE PAK and VOQUEZNA DUAL for the treatment of Helicobacter pylori (H. pylori) infection in adults. These infections cause gastrointestinal bleeding.

Major players in the gastrointestinal bleeding treatment industry, such as Octapharma AG, Takeda Pharmaceutical Company Limited, and Novartis AG, are focusing on launching new products to address unmet demand.

Download Free sample to learn more about this report.

GASTROINTESTINAL BLEEDING TREATMENT MARKET TRENDS

Rising Geriatric Population is a Significant Market Trend

A major global trend in the gastrointestinal bleeding treatment market is the rising geriatric population, which is driving demand for gastrointestinal bleeding treatments. Gastrointestinal bleeding is particularly challenging to treat older individuals; therefore, it increases the overall demand for treatment. With increasing age, the stomach and intestinal lining become more fragile and are more susceptible to medicines that trigger or worsen bleeding, such as painkillers and blood thinners. These factors create an unmet demand for effective gastrointestinal bleeding treatment that overcome these challenges.

- For instance, in February 2025, the WHO reported that the number of people aged 60 and older worldwide is projected to increase from 1.1 million in 2023 to 1.4 million by 2030. Such a high population would drive healthcare spending and boost market demand.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Prevalence of Gastrointestinal Disorders to Fuel Market Growth

The increasing prevalence of gastrointestinal disorders is primarily fueling the growth of the GI bleeding treatment market. With the increasing population of people living with gut conditions that cause bleeding, the patient pool requiring hospital treatment increases. Peptic ulcers, gastritis, GERD, IBD, and colorectal cancer are some of the conditions that induce gastrointestinal bleeding. Additionally, lifestyle factors such as smoking, excessive alcohol consumption, and poor dietary habits also play a role in the development of GI bleeding. Such increasing prevalence of gastric disorders create demand for gastrointestinal bleeding treatment and fuel gastrointestinal bleeding treatment market growth.

- For instance, in August 2024, NIH published a blog titled ‘Upper Gastrointestinal Bleeding’ that reported peptic ulcers affect 5-10% of people globally, with a point prevalence of around 4-5%, while peptic ulcer bleeding (PUB) is a major complication, accounting for roughly half of all acute upper gastrointestinal bleeds (UGIB).

MARKET RESTRAINTS

Risk Associated with Side Effects of Medication Used to Hamper Market Growth

Side-effect concerns with long-term acid-blocking medicines (PPIs) can restrain the GI bleeding treatment market. Administering PPI and other beta blockers is one of the important approaches for treating upper GI bleeding. Still, as awareness has grown, the long-term use is linked with problems such as low magnesium, higher fracture risk, and certain gut infections. These factors have prompted clinicians to step down the dose and use them only when necessary, hinder the market's growth potential.

- For instance, in June 2020, the NIHR reported that according to study led by the London School of Hygiene & Tropical Medicine, the global clinical trial of 12,000 patients with severe gastrointestinal bleeding showed that tranexamic acid, a drug that stops blood clots from breaking down, failed to cut bleeding deaths but caused side effects such as unwanted clots in the legs and lungs.

MARKET OPPORTUNITIES

Development of Oral Formulations to Offer Market Growth Opportunity

A key market growth opportunity in gastrointestinal bleeding treatment lies in expanding easy-to-use, patient-friendly PPI formulations. When a bleeding ulcer is controlled in the hospital, patients are typically administered continuous acid suppression to facilitate ulcer healing and prevent re-bleeding. However, many patients, especially within the aging population, struggle with swallowing pills or sticking to therapy. The development of oral formats and packaging suitable for outpatient use enables hospitals to discharge patients, offering a market growth opportunity. Improved ease of use enhances adherence, lowers the risk of recurrence, and increases prescription volumes beyond the inpatient setting, creating demand for medication-based treatment.

- For instance, in February 2021, Dr. Reddy’s Laboratories Ltd., along with its subsidiaries, launched Lansoprazole DR Orally Disintegrating Tablets, a therapeutic equivalent generic version of Prevacid SoluTab Delayed Release Orally Disintegrating Tablets, 15 mg and 30 mg, approved by the U.S. FDA.

MARKET CHALLENGES

High Cost of Gastrointestinal Bleeding Treatment Poses a Critical Challenge to Market Growth

The overall gastrointestinal bleeding treatment market faces a critical challenge related to high cost. A single bleeding episode can quickly complicate and become a resource-hospital case. Many patients need urgent tests, 24/7 specialist teams, endoscopy in an equipped suite, anesthesia support, blood transfusions, and sometimes ICU monitoring.

Additionally, certain cases involve costly add-ons, such as clotting-factor products or medications to reverse blood thinners. Because hospitals and insurers operate within fixed budgets, they often attempt to control these expenses by limiting the use of high-cost therapies to the most severe cases, delaying non-urgent procedures, or preferring lower-cost alternatives where possible. These cost-containment measures restrain overall market growth.

Segmentation Analysis

By Treatment Type

New Product Launches for Proton Pump Inhibitors Led PPIs Segment Growth

Based on treatment type, the market is categorized into proton pump inhibitors (PPIs), vasoactive drugs, non-selective beta blockers, anticoagulants, and others.

The PPIs segment dominated the gastrointestinal bleeding treatment market in 2025. The dominance of the segment is due to its routine application across a large number of cases to lower the chance of bleeding again. Additionally, PPIs are easier to administer and are generally well-tolerated, supporting the segment’s dominance. Furthermore, strategic collaborations among key companies and the launch of new products offering innovative solutions support segment growth.

- For instance, in June 2025, Eisai Co., Ltd. launched Pariet S, a proton pump inhibitor that was converted from a prescription to an over-the-counter (OTC) medication in Japan. The medication is highly effective in alleviating severe heartburn and stomach pain caused by gastric acid reflux.

The anticoagulant segment is expected to grow at a CAGR of 11.47% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By GI Tract Division

High Incidence Rate of Upper Gastrointestinal Led Upper Segment Growth

Based on GI tract division, the market is segmented into upper and lower.

In 2025, the upper segment dominated the market due to a higher incidence rate of upper GI tract bleeding compared to lower tract bleeding. Many common triggers, such as stomach ulcers, irritation from painkillers, and bleeding related to liver disease, often affect the upper GI area, resulting in a higher patient volume.

- In April 2023, PubMed published a report titled ‘The global epidemiology of upper and lower gastrointestinal bleeding in the general population: A systematic review’ which estimated the incidence of Upper Gastrointestinal bleeding to range from 15.0 per 100000 to 172.0 per 100000 people, while Lower GI Bleeding (LGIB) ranged from 20.5 to 87.0 per 100,000 person-years.

The lower segment is projected to grow at a CAGR of 7.68% during the forecast period.

By Type

Urgent Care in the Hospital Settings Boosted the Acute Segment Growth

Based on type, the market is segmented into acute and chronic.

In 2025, acute type dominated the global market as most gastrointestinal bleeding episodes are sudden events, pushing patients to seek urgent care in hospital settings. They require rapid stabilization and quick procedures, which drive up the treatment cost.

Hospitals prioritize acute cases and treatment typically happens in emergency settings where drug use is standardized and time-sensitive, in contrast to the chronic segment.

- For instance, in February 2025, Hyloris Pharmaceuticals SA entered into an exclusive licensing agreement to develop a ready-to-use formulation for (IV) administration of pantoprazole, a molecule used to treat gastric acid-related conditions.

The chronic segment is projected to grow at a CAGR of 9.32% during the study period.

By Route of Administration

Ease of Administration Boosted Oral Route Of Administration Segment Growth

Based on route of administration, the market is segmented into oral and parenteral.

In 2025, the oral route of administration captured the key gastrointestinal bleeding treatment market share due to its ease of administration. Oral therapy is convenient, less expensive to deliver, and suitable for long-term follow-up periods, resulting in higher prescription volumes. Many preventive and recovery medications linked to GI bleeding, such as ulcer-healing therapy and iron supplements, are administered orally. These advantages reinforce the segment's dominance. Underscoring these advantages, many key companies are also focusing on new product launches in the segment.

- For instance, in March 2025, Aurobindo Pharma Limited received approval from the U.S. FDA for its Abbreviated New Drug Application Pantoprazole Sodium for Delayed-Release Oral Suspension, 40 mg, an AB-rated generic equivalent to the reference listed drug (RLD).

The parenteral segment is projected to grow at a CAGR of 7.61% during the study period.

By Distribution Channel

Hospital Pharmacies Segment Dominated due to Early Care

Based on distribution channel, the market is segmented into hospitals pharmacies, retail pharmacies & drug stores, and online pharmacies.

The hospital pharmacies held a largest market share in the global market in 2025. This is attributed to the fact that they are the first point of contact to provide treatment to patients. Hospital pharmacies supply critical medicines used in the early stages of care. Severe cases also require inpatient monitoring and procedures, which keep medication procurement tied to hospital pharmacies. Additionally, government hospitals have reimbursement programs for treating diseases.

- For instance, in 2022, the UK national audit update on Acute Upper Gastrointestinal Bleeding (AUGIB), surveyed across 147 U.K. hospitals and showcased improved outcomes as the first center of care provider.

The retail pharmacies & drug stores segment is projected to grow at a CAGR of 4.90% during the study period.

Gastrointestinal Bleeding Treatment Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Gastrointestinal Bleeding Treatment Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valued at USD 139.4 million, and maintained its leading position in 2025, with a value of USD 147.9 million. The market in the region is expected to increase significantly over the forecasted years, leading to market growth, driven by government funding, stringent regulatory compliance, and high investment in the region. Healthcare providers in the U.S. and Canada are investing in research and development.

U.S. Gastrointestinal Bleeding Treatment Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 143.9 million in 2026, accounting for roughly 44.80% of the global market.

Europe

Europe is projected to record a growth rate of 5.95% in the coming years, the second-highest among all regions, and reach a valuation of USD 72.3 million by 2026. The region is expected to experience robust growth due to government support for the development of shared infrastructure.

U.K Gastrointestinal Bleeding Treatment Market

The U.K. market in 2026 is estimated to be around USD 11.0 million, representing roughly 3.41% of the global market in 2026.

Germany Gastrointestinal Bleeding Treatment Market

Germany’s market is projected to reach approximately USD 16.6 million in 2026, equivalent to around 5.16% of the global market.

Asia Pacific

Asia Pacific is estimated to reach USD 76.1 million in 2026 and secure the position of the third-largest region in the market.

Japan Gastrointestinal Bleeding Treatment Market

In Japan, the market in 2026 is estimated to be around USD 17.7 million, accounting for approximately 5.51% of the global market.

China Gastrointestinal Bleeding Treatment Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 26.1 million, representing approximately 8.11% of global sales.

India Gastrointestinal Bleeding Treatment Market

In India, the market in 2026 is estimated to be around USD 6.3 million, accounting for roughly 1.97% of the global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 10.4 million in 2026. The region is experiencing market growth due to increasing investment and government initiatives. In the Middle East & Africa, the GCC is set to reach a value of USD 2.7 million in 2026.

South Africa Gastrointestinal Bleeding Treatment Market

In South Africa, the market is projected to reach approximately USD 0.8 million by 2026, accounting for roughly 0.26% of the global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on New Product Launches by Key Players to Strengthen their Market Position

The global market has a consolidated market structure, with companies such as Octapharma AG, Takeda Pharmaceutical Company Limited Novartis AG, and Mallinckrodt, Amneal Pharmaceuticals, Inc, holding a significant market share. The leading market share of these companies is attributed to strategic partnerships, technological advancements, and increasing investments in the sector.

- For instance, in February 2025, Amneal Pharmaceuticals, Inc. launched mesalamine 800 mg, an aminosalicylate indicated for the treatment of moderately active ulcerative colitis in adults.

Other notable players in the global market include AstraZeneca, F. Hoffmann-La Roche Ltd, and Bohringer Ingelheim International GmbH. These companies are expected to prioritize technological advncements, strategic collaborations, and new product launches to strengthen their position during the forecast period.

LIST OF KEY GASTROINTESTINAL BLEEDING TREATMENT COMPANIES PROFILED

- Octapharma AG (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Novartis AG (Switzerland)

- Mallinckrodt (Ireland)

- AstraZeneca (U.K.)

- CSL (Australia)

- Hoffmann-La Roche Ltd (Switzerland)

- Boehringer Ingelheim International GmbH (Germany)

- Phathom Pharmaceuticals (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2024: NEXT BIOMEDICAL, a Korean medical solutions company, received U.S. FDA approval for the use of its bleeding prevention powder for lower gastrointestinal (GI) bleeding.

- July 2024: Dr Reddy’s Laboratories Ltd unveiled a non-exclusive patent licensing agreement with Takeda Pharmaceutical Company Limited. The agreement allowed Dr Reddy’s to market Vonoprazan tablets in India.

- June 2024: Akums Drugs and Pharmaceuticals launched Rabeprazole + Levosulpiride SR Capsules, approved by the Drug Controller General of India (DCGI), to provide enhanced relief for patients with gastrointestinal tract (GIT) disorders.

- October 2023: Sanofi collaborated with Teva Pharmaceuticals, a U.S. subsidiary of Teva Pharmaceutical Industries Ltd to co-develop and co-commercialize asset TEV’574, currently in Phase 2b clinical trials for the treatment of Ulcerative Colitis and Crohn's Disease, two types of inflammatory bowel disease.

- September 2022: Azurity Pharmaceuticals, Inc., received approval from the U.S. FDA for Konvomep (omeprazole and sodium bicarbonate for oral suspension). Konvomep is indicated for the treatment of active benign gastric ulcers and for reducing the risk of upper gastrointestinal bleeding in critically ill patients.

REPORT COVERAGE

The global gastrointestinal bleeding treatment market analysis includes a comprehensive study of the market size and forecast by all segments included in the report. It includes details on the market dynamics and trends expected to drive the global gastrointestinal bleeding treatment market over the forecast period. It provides information on key aspects, including the epidemiology of gastrointestinal disorders that cause bleeding, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.80% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Region |

|

By Treatment Type |

· Proton Pump Inhibitors (PPIs) · Vasoactive Drugs · Non-selective beta-blockers · Anticoagulant · Others |

|

By GI Tract Division |

· Upper · Lower |

|

By Type |

· Acute · Chronic |

|

By Route of Administration |

· Oral · Parenteral |

|

By Distribution Channel |

· Hospitals Pharmacies · Retail Pharmacies & Drug Stores · Online Pharmacies |

|

By Region |

· North America (By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Country) o U.S. o Canada · Europe (By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Treatment Type, GI Tract Division, Type, Route of Administration, Distribution Channel, and Country/Sub-region) o GCC o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 302.3 million in 2025 and is projected to reach USD 543.8 million by 2034.

In 2025, the market value stood at USD 147.9 million.

The market is expected to exhibit a CAGR of 6.80% during the forecast period (2026-2034).

By treatment type, the proton pump inhibitor segment led the market.

The increasing geriatric population and rising prevalence of gastrointestinal disorders are the key factors driving market growth.

Octapharma AG, Takeda Pharmaceutical Company Limited, Novartis AG, Mallinckrodt AstraZeneca, and CSL. are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us