GCC Shallow Water Decommissioning Market Size, Share & Industry Analysis, By Service (Project Management, Engineering and Planning, Well Plugging and Abandonment, Pipeline and Power Cable Decommissioning, Materials Disposal and Site Clearance, and Others), By Structure (Topside, Subsea Infrastructure, and Substructure), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

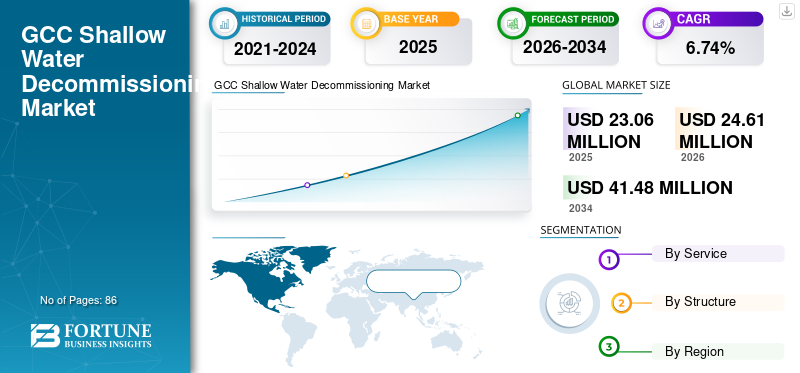

The GCC shallow water decommissioning market size was estimated at USD 23.06 million in 2025 and is projected to reach USD 24.61 million in 2026 to USD 41.48 million by 2034, growing at a CAGR of 6.74% from 2026 to 2034. Qatar dominated the GCC shallow water decommissioning market with a market share of 79.42% in 2025.

When oil and gas fields gets matured, their facilities need to be removed, a process known as “decommissioning”. Decommissioning of offshore machineries is a highly complex and technical method that poses significant health and safety challenges.

The GCC region has more oil and gas infrastructure in the onshore location than offshore. This reduces the demand for decommissioning in offshore locations. The GCC shallow water decommissioning market share is likely to grow in the coming years owing to the decreasing world requirement for oil and gas. Nonetheless, the growth of the renewable energy sector in the major crude petroleum target market (i.e. major crude oil importers from GCC) will likely lead to the decommissioning of oil and gas assets in GCC countries.

In addition, in April 2022, Motive Offshore partnered with Hiretech to bring advanced decommissioning technology to the Middle East. Along with the technology and equipment, Hiretech would provide an inclusive training program to Motive’s engineers and technicians, allowing continuous technical support and product delivery. Such developments will help to boost the GCC shallow water decommissioning market in forecast years.

Such projects for shallow water decommissioning is about to grow as many structures are getting matured in forecast years.

Download Free sample to learn more about this report.

GCC Shallow Water Decommissioning Market Key Takeaways

- 2025 Market Size: USD 23.06 million

- 2026 Market Size: USD 24.61 million

- 2034 Forecast Market Size: USD 41.48 million

- CAGR: 6.74% from 2026–2034

- Qatar dominated the GCC shallow water decommissioning market with a 79.42% share in 2025.

- Project management emerged as the leading service segment in the market.

- The topside segment accounted for the largest market share of 40.54% in 2026.

Qatar

Qatar accounted for USD 18.31 million in 2025 and is projected to reach USD 19.55 million in 2026.

Saudi Arabia

Saudi Arabia remains a major market due to extensive offshore oil and gas infrastructure.

UAE

The UAE is expected to be the fastest-growing market owing to aging oil and gas assets.

U.S.

Advanced offshore decommissioning expertise is supporting GCC market development.

Japan

Offshore engineering capabilities are creating opportunities in GCC decommissioning projects.

Read More

GCC Shallow Water Decommissioning Market Trends

Renewable Energy Transition in GCC is a Latest Trend

The global energy demand is expected to be boosted by renewable energy, driven by rising concerns regarding climate change activities. This might pose a challenge to the energy exports of GCC countries, turning oil and gas assets into liability for these countries. As a result, this may lead to the decommissioning of oil and gas infrastructure. GCC shallow water decommissioning market is expected to grow owing to the several micro and macro economical factors.

As per the International Energy Associations, despite the pandemic-induced supply chain challenges, record-level commodity and raw material prices, and construction delays, renewable capacity additions in 2021 surged by 6%, breaking another record and reaching almost 295 GW.

Download Free sample to learn more about this report.

GCC Shallow Water Decommissioning Market Growth Factors

Growing Mature Field Count to Drive Market Growth

Mature offshore oilfields are sea oilfields at a stage of declining production or reaching the end of their production life. The average lifespan of offshore oilfields is 20-25 years, after which the platform must undergo dismantling due to the unproductive machinery and equipment. This dismantling procedure, referred to as decommissioning, plays a critical role in offshore oilfields. The growing number of matured field is driving the market for shallow water decommissioning. In addition, the lower dependency on the oil as a fuel source is also one of the factor boosting shallow water decommissioning projects.

In October 2022, Qatargas, a global energy operator, signed a USD 4.3 billion offshore contract with Saipem. The contract encompasses the installation of two gas compression complexes for the North Field Production Sustainability project. The additional work involved redirecting the hydrocarbons from the present wellhead platform via the new facilities due to the decommissioning of a current pipeline.

Technological Advancements Streamlining Decommissioning to Spur Market Development

Offshore decommissioning is a specialized activity that completely depends on meticulous planning, utilizing technology, equipment, and resources to control costs, ensure complete safety at oilfields, and protect the environment. These are several factors responsible for the growth such as, technology advancements in recent years, have streamlined construction operations, making them easier to understand and implement. Secondly, the oil & gas companies heavily invest in research and development to convert imaginary concepts into reality.

In addition, in In October 2021, Australian wave power technology company Carnegie Clean Energy promised to deliver reliable renewable energy for offshore facilities, starting with the moored vessels used in aquaculture. The USD 3.4 million project is being brought in collaboration with partners, including two of Australia’s major aquaculture companies, Huon Aquaculture and Tassal Group, with USD 1.35 million in funding from the Tasmania-based Blue Economy Cooperative Research Centre. As soon as this technology reaches in other regions, it will boost the offshore operation, including decommissioning, where vessels are continuously used.

RESTRAINING FACTORS

High Cost of Offshore Decommission Services Is Hindering the Market Growth

The decommissioning cost of oil and gas structures is high, especially for offshore oil and gas machinery and tools, as the offshore conditions are relatively complex than onshore. The complexity leads to increased costs due to the requirement for a highly skilled workforce and technologies. In addition, the cost also upsurges as per the complexity of the decommissioning operations.

Additionally, the cost of service may also differ based on the depth of the sea or water level, where shallow water decommissioning costs being lower than those in deep water. However, these operations and services continue to incur substantial expenses.

GCC Shallow Water Decommissioning Market Segmentation Analysis

By Service Analysis

Revolution in the Project Management is driving the Market Growth

Based on service, the market is segmented into project management, engineering, and planning, well plugging and abandonment, pipeline and power cable decommissioning, materials disposal and site clearance, and others.

Project management is the dominating segment and is considered as a crucial service, essential for the successful delivery of decommissioning project. In addition, it guarantees stakeholder management, proper coordination, and compliance with rules, risk reduction, and cost control.

Government standards governing sea activities and operations drive the market for offshore decommissioning services. As per new regulations, the UAE Ministry of Finance announced that the federal tax would be applied to business profits after 1st June 2023, leading to potential changes in offshore decommissioning services.

By Structure Analysis

To know how our report can help streamline your business, Speak to Analyst

Topside Structures Leads the Market as they are a Significant Component in Oil And Gas Installations

Based on structure, the market is segmented into topside, subsea infrastructure, and substructure.

The Topside segment led the market accounting for 40.54% market share in 2026. Topside structure is the dominating segment in the region driven by the presence of multiple structures and rising decommissioning projects. Topside is also the fastest growing, owing to the several factors such as it is visible above the waterline which makes it ideal to remove easily.

Norwell Engineering will handle the UAE offshore decommissioning project for the operator Sinochem Corp. This projects involves both decommission of the topside structure and subsea infrastructure management. The agreement includes developing the abandonment strategy for the UAQ gas & well field and incudes facilities decommissioning planning, procurement services, logistics, marine provision, and operational execution.

REGIONAL ANALYSIS

Qatar dominated the market with a valuation of USD 18.31 Million in 2025 and USD 19.55 Million in 2026. Qatar holds the maximum share and dominates the market owing to the rising decommissioning services in the country. This trend is expected to continue in the coming years.

GCC shallow water decommissioning countries majorly operate in the ons hore location and less in the offshore location. Primary countries such as Saudi Arabia, Qatar, and UAE are active in the offshore location.

For instance, In April 2023, Saipem has received Qatarga's confirmation for an additional scope of work within the North Field Production Sustainability Offshore Project. The additional scope of work of the two stages is worth approximately USD 350 million, including decommissioning the 13 km existing pipeline.

UAE is estimated to be the fastest-growing country in the offshore decommissioning market and is predicted to sustain this growth in the coming years. This growth is attributed to factors such as ageing oil and gas infrastructure and the country’s commitment to reducing its dependence on oil and gas exports.

List of Key Companies in GCC Shallow Water Decommissioning Market

Saipem is the Leading Service Provider for the Global Decommissioning Market

Saipem is one of the major companies in the global GCC market in the decommissioning and oilfield sector. It has expertise in the offshore and onshore oil and gas sectors. The company offers a comprehensive array of onshore and offshore services, as a result it is adding value from the early phases of project through and its entire life cycle.

On other hand, other player; Petrofac, is a leading international service provider to the energy industry. The company uses engineering and consultancy expertise to design, build, and operate decommissioning operations. It is trying to expand its presence in GCC.

- 18 May 2023, – Petrofac, a leading provider of offshore services, and Promethean Decommissioning Company (PDC), a decommissioning operator, have formed an partnership to decommission the South Pass 6, South Pass 60, and East Breaks 165 fields, offshore Gulf of Mexico.

List of Key Companies Profiled:

- Saipem (Italy)

- MILAHA (Qatar)

- Worley (Australia)

- Petrofac (Jersey)

- Schlumberger (U.S.)

- Baker Hughes (U.S.)

- Norwell Engineering (Scotland)

- DNV (Norway)

- Aries Marines (UAE)

- Aker Solutions (Norway)

KEY INDUSTRY DEVELOPMENTS:

- In May 2023, Saipem was awarded two fresh offshore contracts. One involves Engineering, Procurement, Construction and Installation (EPCI) in the Black Sea, while the other pertains to decommissioning activities in the North Sea. The overall cost of the contracts amounts to approximately 850 million USD.

- In June 2022, Norwell Engineering, a global well engineering and project management company, signed a multi-million dollar contract to bring an integrated offshore decommissioning project in the UAE for the Chinese operator Sinochem Corporation.

- In April 2022, Motive Offshore partnered with Hiretech to bring advanced decommissioning technology to the Middle East. Along with the technology and equipment, Hiretech provided an inclusive training program to Motive’s engineers and technicians, allowing the continuous delivery of technical support and products. Furthermore, robotics and automation are also crucial in technologies that can reduce human contact with hazards, improve operational productivity, and lower extra equipment costs.

- In April 2021, Saipem received confirmation from Qatargas for the exercise of two options for additional scope of work within the North Field Production Sustainability Offshore Project. The additional scope of work was worth approximately USD 350 million and was related to the rerouting of the hydrocarbons from the current wellhead platform through the new facilities due to the decommissioning of the current pipeline .

- In December 2020, Global thermal and energy management dealer Hanon Systems delivered its innovative R744 heat pump equipment to the Volkswagen Group for its global MEB platform.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading product applications. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.74% from 2026 to 2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Service, Structure, and Region |

|

Segmentation |

By Service

|

|

By Structure

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the market was USD 23.06 million in 2025.

The GCC market is projected to grow at a CAGR of 79.42% in the forecasted period.

The market size of Qatar stood at USD 18.31 million in 2025.

Based on the service, the project management holds the dominating share in the GCC market.

The GCC market size is expected to reach USD 41.48 million by 2034.

Large mature offshore oilfields is the key driver propelling the growth for offshore decommissioning market.

Saipem, Schlumberger, Worley, and Baker Hughes are some of the major players actively operating across the market.

- 2021-2034

- 2025

- 2021-2024

- 86

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us