Used Cars Market Size, Share & Industry Analysis, By Vehicle Type (Hatchbacks, Sedan, and SUVs), By Sales Channel Type (Offline and Online), By Fuel Type (Petrol, Diesel, CNG, and Electric), By Distribution Channel (Franchised Dealer, Independent Dealer, and C2C), By Age (1 to 3 Years old, 4 to 7 Years old, and More than 8 Years old), and Regional Forecast, 2026-2034

Used Cars Market Size & Share

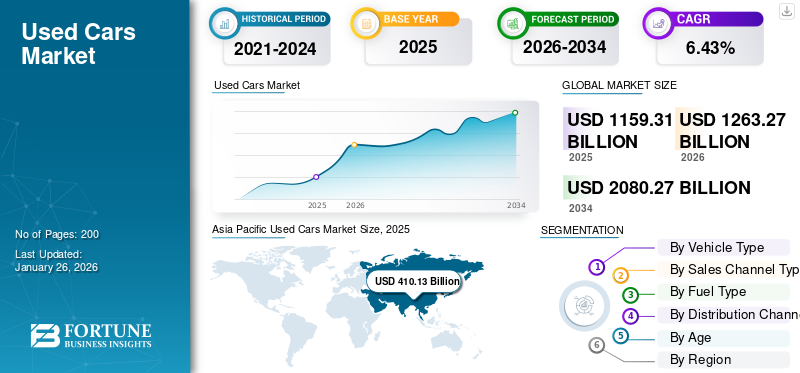

The used cars market size was valued at USD 1,159.31 billion in 2025 and is expected to grow from USD 1,263.27 billion in 2026 to USD 2,080.27 billion by 2034, exhibiting a CAGR of 6.43% during the forecast period. Asia Pacific dominated the global market, accounting for 35.38% market share in 2025.

The used cars market demand expansion reflects affordability pressures in new vehicle markets, extended vehicle lifecycles, and growing consumer acceptance of certified pre-owned ownership models. Across both developed and emerging economies, secondary vehicle transactions now exceed new vehicle sales volumes, reinforcing structural importance within the broader automotive value chain.

Used car market growth is primarily supported by widening price gaps between new and pre-owned vehicles. Rising manufacturing costs, electrification investments, and regulatory compliance expenses continue to elevate new vehicle pricing thresholds. Consequently, consumers increasingly evaluate used vehicles as economically rational alternatives without significant compromise in performance or safety features.

The used car market size continues to expand alongside financing accessibility. Banks and non-banking financial institutions increasingly design credit products tailored specifically for secondary vehicle ownership. This trend significantly broadens addressable consumer segments. From a supply perspective, leasing programs, corporate mobility fleets, and subscription-based ownership models are stabilizing inventory pipelines. Vehicles entering resale markets increasingly maintain documented service histories, improving valuation accuracy.

Used car market trends also indicate structural digitization across sourcing, inspection, and transaction completion processes. Hybrid online-offline retail models are becoming dominant rather than purely physical dealership operations. Regional demand patterns remain uneven. Mature markets emphasize certified quality and digital convenience, while emerging economies prioritize affordability and accessibility. Despite macroeconomic uncertainty affecting discretionary spending cycles, resale mobility demand demonstrates resilience due to its essential transportation role.

A used car is a vehicle that has had one or more previous owners and is resold through various channels, such as private sellers, dealerships, or auctions. The global used car market is a significant segment of the automotive industry, characterized by the resale of these vehicles at lower prices compared to new cars. This market is driven by factors such as economic considerations, changing consumer preferences for cost-effective transportation, and the rising popularity of online platforms for buying and selling used vehicles. In recent years, the market has seen growth due to increased urbanization and a shift towards sustainable transportation options, making used cars an attractive choice for many consumers.

The COVID-19 pandemic had a profound impact on the global used cars market growth, initially causing a decline in both new and used vehicle sales due to economic uncertainty and supply chain disruptions. However, as public transportation became less appealing and personal mobility gained importance, demand for such cars surged. Consumers shifted their purchasing preferences toward more affordable options as new car inventories dwindled due to production delays. This shift resulted in increased sales of pre-owned vehicles, with many car shoppers seeking cost-effective alternatives during the economic downturn. The lasting effects of these changes are expected to influence consumer behavior in the automotive market for years to come.

Download Free sample to learn more about this report.

Used Cars Market Key Takeaways

- 2025 Market Size: USD 1,159.31 Billion

- 2026 Market Size: USD 1,263.27 Billion

- 2034 Forecast Market Size: USD 2,080.27 Billion

- CAGR: 6.43% from 2026–2034

- Asia Pacific dominated the used cars market with a 35.38% share in 2025.

- The sedan segment is projected to account for 22.07% of the market in 2026.

- The offline sales channel segment is projected to hold a 70.54% market share in 2026.

North America

North America is the second-largest market expected to hold USD 363.31 billion in 2025, documenting a CAGR of 6.30% during the forecast period (2025-2032).

Asia Pacific

The Asia Pacific market accounted for USD 410.13 billion in 2025, representing 35.38% of the global industry, and is expected to reach USD 458.88 billion in 2026.

Europe

In 2025, Europe generated USD 134.46 billion, contributing 11.60% to global market revenue, and is projected to grow to USD 144.81 billion in 2026.

U.S.

The market is projected to reach USD 274.59 billion in 2026, supported by large vehicle parc volumes, robust financing availability, and expanding certified pre-owned vehicle sales.

Japan

The market is expected to reach USD 53.07 billion in 2026, benefiting from a highly efficient resale ecosystem, strict vehicle inspection standards, and strong domestic and export demand.

Read More

Key Market Dynamics

Market Trends

Digital Platform Adoption and Technological Advancements in Vehicles Are Key Market Trends.

Download Free sample to learn more about this report.

A major ongoing trend in the global used cars market is the increasing adoption of digital platforms for buying and selling vehicles. Online marketplaces such as Carvana and AutoTrader have transformed the traditional car shopping experience, allowing consumers to browse extensive inventories, conduct virtual inspections, and complete purchases from the comfort of their homes. This shift is largely driven by consumer demand for convenience and transparency, particularly in the wake of the COVID-19 pandemic, which accelerated the digital transformation of various industries.

Digitalization represents the most transformative structural shift shaping the current used car market trends. Online marketplaces increasingly integrate vehicle sourcing, inspection verification, financing approval, and logistics coordination within unified digital ecosystems. Artificial intelligence-driven pricing engines now analyze historical transactions, vehicle condition data, and regional demand signals to establish standardized valuations. This reduces negotiation dependency and improves transaction efficiency.

Hybrid retail models combining digital discovery with physical inspection are becoming industry norms. Buyers increasingly begin purchase journeys online before completing transactions through dealership networks. Another evolving trend involves increasing institutional participation. Automotive manufacturers and leasing companies actively expand certified resale programs to retain lifecycle revenue participation beyond first ownership. Electrification also influences inventory composition. As electric vehicle adoption rises, early-generation models gradually enter resale channels. Market participants are developing battery certification frameworks to address buyer concerns.

Additionally, there's a significant focus on technological advancements within used vehicles. Features such as adaptive cruise control and advanced infotainment systems are increasingly sought-after by buyers, with modern tech-equipped cars selling faster than their less-equipped counterparts. The integration of artificial intelligence into pricing and valuation processes is also enhancing product efficiency. As consumer preferences evolve toward SUVs and fuel-efficient models, the used electric vehicle segment is anticipated to grow rapidly due to heightened interest in sustainability and affordability. These trends indicate a dynamic shift in consumer engagement with the used car market, emphasizing the increasing role of technology and convenience.

Market Opportunity

Rising Demand for Electric and Hybrid Vehicles to Present Opportunity for Market Players

A significant opportunity in the market lies in the increasing demand for electric vehicles (EVs) and hybrid models. As consumer awareness about sustainability grows, many buyers are opting for used EVs as a cost-effective alternative to new models, particularly given the rising prices of new vehicles. This trend is further supported by industry reports indicating rapid expansion of the used electric vehicle segment, driven by both environmental concerns and economic factors.

The digitalization of the car-buying process presents another major opportunity. Online platforms such as Carvana and Vroom have revolutionized how consumers shop for used cars by offering comprehensive vehicle listings, virtual inspections, and seamless purchasing processes. This shift toward e-commerce is particularly appealing to younger consumers who prioritize convenience and transparency when making significant purchases.

A significant opportunity exists within the ongoing formalization of historically fragmented resale ecosystems. Organized platforms capable of standardizing inspection, pricing, and financing processes are positioned to capture an increasingly used car market share. Emerging economies present particularly strong expansion potential. Rapid urbanization combined with rising middle-income populations drives demand for affordable personal mobility solutions. Used vehicles often represent the first ownership step within these markets.

Fleet electrification transitions also generate future inventory pipelines. Corporate mobility operators replacing internal combustion fleets introduce large volumes of structured resale supply. Financial institutions increasingly view the secondary automotive sector as a scalable lending opportunity. Customized credit assessment models based on vehicle performance data improve loan accessibility. Another developing opportunity involves refurbishment ecosystems. Professional vehicle reconditioning improves resale value while extending lifecycle utilization, supporting sustainability objectives increasingly prioritized by regulators.

The expansion of subscription-based services for used cars is gaining traction, allowing consumers to access vehicles without long-term commitments. This model caters to changing consumer preferences and provides flexibility in ownership, making it an attractive option in urban areas where mobility needs are evolving. Overall, these opportunities indicate a robust growth trajectory for the global used cars market share as it continues to adapt to shifting consumer demands and technological advancements.

Market Drivers

Increasing Demand for Vehicle Ownership in Emerging Economies to Boost Market Growth

One of the major driving factors for the global used car market is the escalating prices of new vehicles, prompting consumers to seek more affordable alternatives. As new car prices continue to rise, due to supply chain disruptions and increased production costs, many buyers are turning to used cars as a viable solution. This trend is particularly pronounced among budget-conscious buyers and first-time car owners who prioritize affordability.

Organizations such as AutoNation and CarMax have reported substantial increases in their used car sales, attributing this trend directly to the high costs of new vehicles. For example, AutoNation's recent earnings report indicated that used vehicle sales surged by over 15% year over year as consumers opted for pre-owned options amid economic uncertainty and rising living costs.

Rising new vehicle acquisition costs, influenced by advanced safety technologies and electrification investments, continue widening entry barriers for first-time buyers. Used vehicles, therefore, provide immediate mobility access at substantially lower capital commitment. Urbanization patterns further reinforce demand growth. Expanding suburban commuting requirements increase reliance on personal transportation, particularly in regions with limited public transit scalability. Secondary vehicle ownership becomes a practical solution for households managing cost constraints.

Digital transformation across vehicle discovery platforms also reduces information asymmetry historically associated with resale transactions. Buyers increasingly access verified ownership records, pricing benchmarks, and inspection data before purchase decisions. Another important driver influencing used car market growth involves extended vehicle durability improvements. Modern vehicles maintain operational reliability for longer lifecycles, expanding resale viability beyond traditional ownership periods.

Additionally, the ongoing shift toward digital marketplaces has made purchasing used cars more accessible and transparent. Platforms such as Carvana and Vroom have streamlined the buying process, allowing consumers to easily compare vehicle prices and access a wide range of vehicles online. This convenience attracts buyers seeking efficient purchasing experiences without the traditional pressures of physical dealerships. Overall, the combination of rising new car prices and the enhanced accessibility of digital buying platforms has created a robust growth environment for the used car market.

Market Restraints

Rising Interest Rates and High Maintenance Costs are Hindering Market Growth

One significant restraining factor for the global used cars market is the high cost of servicing and maintenance associated with older vehicles. As cars age, they require more frequent repairs and upkeep, which can deter potential buyers due to the financial burden. According to recent industry insights, the average annual maintenance cost for a vehicle is around USD 900, but this figure can escalate significantly for certain brands, especially luxury vehicles. For instance, brands such as Land Rover and Porsche can incur maintenance costs exceeding USD 19,000 and USD 14,000 over ten years, respectively.

This issue is particularly problematic in a market where consumers are increasingly sensitive to total ownership costs. Additionally, rising interest rates, averaging over 14% for used car loans, make financing for used vehicles less attractive compared to new car options that often come with zero percent APR incentives. Consequently, some buyers may opt for new models, which, despite their higher upfront prices, offer lower long-term costs.

Despite strong demand fundamentals, several structural challenges continue to limit optimized expansion within the used car industry. Quality inconsistency across fragmented resale ecosystems remains one of the most persistent barriers affecting consumer trust. Vehicle history transparency varies significantly between regions. In markets lacking centralized ownership databases, buyers face uncertainty related to accident exposure, maintenance quality, or mileage manipulation. These risks directly influence pricing volatility and purchasing hesitation.

Regulatory complexity also introduces operational friction. Documentation transfer procedures, taxation differences, and registration compliance requirements increase transaction timelines in several jurisdictions. Electric vehicle adoption introduces an additional complexity layer. Battery degradation assessment remains technically challenging for average buyers. Concerns surrounding replacement costs may delay secondary adoption until diagnostic standardization improves.

Moreover, the growing availability of online platforms has changed consumer behavior, making it easier for buyers to compare options and seek transparency in pricing and vehicle history. However, the fear of unexpected repair costs continues to loom large in consumer decision-making processes. For example, as used car prices have softened recently, many sellers are facing declining trade-in values, complicating their ability to transition to new vehicles. This dynamic highlights how maintenance costs impact individual buyer decisions and shape broader market trends in the used car sector.

- For Instance, in November 2024, the National Consumer Commission (NCC) of South Africa issued warnings after receiving complaints regarding buyers discovering major defects in their used cars shortly after purchase. Such incidents further erode consumer confidence in the used car market.

SEGMENTATION ANALYSIS

By Vehicle Type

Growing Consumer Preference for Larger Vehicles has led to the Dominance of SUVs in the Market.

Based on vehicle type, the market is segmented into hatchbacks, sedans, and SUVs.

Sedan

In 2026, the sedan segment is projected to lead the market with a 22.07% share, as consumers prioritize comfort and utility in their vehicle choices. This trend is particularly evident in markets such as North America and Asia, where SUVs have experienced a surge in popularity due to their perceived safety and capability. For instance, brands such as Toyota and Ford have reported strong sales in their used SUV models, reflecting a robust demand.

Sedans occupy a transitional positioning between affordability and comfort-oriented mobility preferences. Demand is particularly strong among professional commuters and family buyers upgrading from entry-level vehicles. In mature markets, sedan resale activity benefits from corporate fleet disposals and leasing returns. These vehicles typically enter secondary markets with documented service histories, improving buyer trust. Sedans demonstrate relatively balanced depreciation curves, which appeals to lenders and dealerships managing financing exposure. Buyers often perceive them as offering higher value retention compared with compact alternatives.

However, shifting consumer preference toward sport utility vehicles has moderated long-term growth in certain regions. Even so, sedans maintain a stable used car market share due to affordability advantages in secondary ownership cycles.

Hatchbacks

The hatchback segment is experiencing rapid growth, particularly among younger buyers seeking affordable and fuel-efficient options. Hatchbacks are often favored in urban areas due to their compact size, making them easier to navigate and park. The rise of electric hatchbacks, such as the Nissan Leaf, has also contributed to this segment's appeal.

Hatchbacks continue to represent one of the highest transaction volume categories across the global used car market, particularly in densely populated urban economies. Their dominance is closely tied to affordability, fuel efficiency, and operational practicality within congested city environments. Demand remains strong among first-time vehicle buyers and budget-conscious households seeking low acquisition and maintenance costs. Compact dimensions also reduce insurance and parking expenses, strengthening ownership economics.

Supply availability supports sustained liquidity within this segment. Large volumes originate from ride-hailing fleets, corporate leasing programs, and short ownership cycles common in metropolitan regions.

To know how our report can help streamline your business, Speak to Analyst

SUVs

Sport utility vehicles represent the fastest-growing vehicle category within the used car market growth trajectory. Changing consumer preferences toward larger vehicles, improved safety perception, and versatility continue supporting demand expansion. SUV supply entering resale channels has increased significantly due to strong new vehicle adoption during the previous decade. This expanding inventory pipeline improves accessibility for middle-income buyers previously priced out of the segment.

Despite higher acquisition costs, financing penetration remains strong because lenders consider SUVs relatively liquid resale assets. Electric and hybrid SUVs entering secondary markets are expected to reshape pricing benchmarks gradually. As a result, SUVs increasingly contribute disproportionally to overall used car market share growth despite lower transaction frequency compared with hatchbacks.

By Sales Channel Type

Hands-On Experience in Inspection and Buying Dominates the Offline Segment

By sales channel, the market is divided into offline and online.

Offline

The offline sales channel remains the dominant method for purchasing used cars, accounting for over 70% of transactions. Traditional dealerships provide a hands-on experience that many consumers still prefer, allowing them to inspect vehicles physically and negotiate prices directly. Major players such as CarMax and AutoNation have established extensive networks of franchised dealerships to cater to this demand. Additionally, offline channels benefit from long-standing trust and brand recognition, crucial factors for buyers making significant investments. The Offline segment is poised to account for 70.54% of the market share in 2026.

Traditional offline dealership networks continue to account for a substantial portion of global transactions, particularly in markets where physical inspection remains central to buyer confidence. Offline channels benefit from established trust relationships and localized inventory management capabilities. Buyers often prefer an in-person evaluation before purchase, especially when transaction values represent a significant household investment.

Independent dealerships remain dominant contributors within developing economies where digital penetration varies. However, operational inefficiencies and pricing inconsistencies persist in fragmented offline ecosystems. Even with digital disruption, offline retail remains strategically important due to logistics infrastructure and post-sale servicing capabilities.

Online

The online sales channel is the fastest-growing segment in this market. The COVID-19 pandemic accelerated the shift toward digital platforms, with companies such as Vroom and Carvana leading the charge by offering seamless online purchasing experiences. The convenience of browsing inventory from home and having vehicles delivered directly to their doorsteps has attracted tech-savvy buyers. The segment is likely to register a considerable CAGR of 13.10% during the forecast period (2025-2032).

Online platforms represent the most disruptive structural transformation across the used car market trends. Digital marketplaces increasingly centralize vehicle discovery, pricing comparison, inspection reporting, and financing approval processes. Consumer behavior increasingly favors transparency and convenience offered by digital channels. Algorithm-based pricing models reduce negotiation uncertainty while improving valuation consistency.

Hybrid approaches combining online discovery with offline fulfillment are emerging as dominant structures. Online channels, therefore, contribute significantly to future used car market growth rather than fully replacing dealership ecosystems.

By Fuel Type

Widespread Availability and Lower Initial Costs Help the Petrol Segment Dominate the Market

In terms of fuel type, the market is divided into petrol, diesel, CNG, and electric.

Petrol

The petrol vehicles dominate the makret share of 46.12% in 2026, due to their widespread availability and lower initial costs compared to diesel alternatives. Petrol engines are often preferred in regions such as North America and Europe, where they typically offer better performance for everyday driving conditions.

Petrol-powered vehicles maintain the largest inventory base across resale markets globally. Their mechanical simplicity and widespread service infrastructure sustain long-term ownership viability. Urban buyers particularly favor petrol vehicles due to shorter commute patterns and lower upfront maintenance complexity. Petrol vehicles continue contributing significantly to the used car market size despite gradual electrification pressures.

Diesel

Diesel vehicles remain highly relevant in regions characterized by long-distance travel requirements or commercial usage overlap. Fuel efficiency advantages historically supported strong adoption, resulting in large resale inventories entering secondary markets. However, tightening emissions regulations in several regions influences depreciation behavior. Urban restrictions on diesel usage may gradually affect long-term demand. Even so, diesel vehicles maintain relevance in logistics-dependent economies where operational efficiency outweighs regulatory concerns.

CNG

Compressed natural gas (CNG) vehicles are gaining traction in price-sensitive markets, emphasizing fuel cost optimization. Secondary buyers increasingly evaluate operating economics rather than acquisition price alone. Vehicles already equipped with certified CNG systems attract strong interest among urban fleet operators. Growth remains regionally concentrated but contributes incremental diversification within fuel segmentation.

Electric

Electric Vehicles (EVs) represent the fastest-growing segment within the fuel type category. As environmental concerns rise and government incentives for EV purchases increase, more consumers are opting for electric models in the market. For instance, Tesla's Model 3 has become one of the most sought-after used electric cars due to its performance and technology features. This segment is estimated to grow with a substantial CAGR of 12.60% during the forecast period (2025-2032).

Electric vehicles represent an emerging but strategically important segment within the used car market growth outlook. Early adoption challenges include battery performance uncertainty and valuation complexity. However, improving diagnostic transparency and warranty transfers are gradually improving buyer acceptance. Electric resale markets are expected to expand materially as first-generation electric fleets mature.

By Distribution Channel

Associated Trust and Brand Loyalty Make Franchised Dealers Dominate the Market

By distribution channel, the market is divided into franchised dealers, independent dealers, and C2C.

Franchised Dealers

The franchised dealer distribution channel is currently the largest contributor to the global used car market. These dealers leverage brand loyalty and trust associated with established manufacturers such as Ford and Toyota. A key factor driving their dominance is the availability of certified pre-owned programs, which provide buyers with assurances of vehicle quality and reliability. In 2024, franchised dealers were expected to generate significant revenue due to their comprehensive service offerings and customer support. This segment is anticipated to acquire 46.42% of the market share in 2026.

Franchised dealerships increasingly expand certified pre-owned programs to retain customer relationships beyond initial vehicle ownership. Structured inspection standards and warranty offerings improve transaction reliability. Buyers often accept slightly higher pricing in exchange for reduced risk exposure. Manufacturers benefit by maintaining brand ecosystem participation throughout vehicle lifecycles.

Independent Dealers

Independent dealers are emerging as the fastest-growing distribution channel. These dealers often provide competitive pricing and a diverse range of vehicles without brand restrictions. The rise of platforms such as Cars24 has facilitated this growth by connecting independent dealers with consumers looking for better deals on used cars.

Independent dealers remain critical contributors to market liquidity, particularly within fragmented regional ecosystems. Their operational flexibility allows rapid inventory turnover and localized pricing adaptation. However, quality consistency varies significantly across operators. Digital partnerships increasingly integrate independent dealers into broader resale platforms.

Consumer-to-Consumer (C2C)

Consumer-to-consumer transactions continue expanding through online listing platforms, enabling direct interaction between buyers and sellers. Advantages include competitive pricing and wider inventory visibility. However, trust verification challenges persist without intermediary certification support. Technology platforms increasingly introduce escrow systems and inspection partnerships to mitigate transaction risks. The C2C segment is poised to grow with a significant CAGR of 8.50% during the forecast period (2025-2032).

By Age

Tendency to Buy Nearly New Vehicles at Low Cost is Making the 4 To 7-Year-Old Segment Dominate the Market.

By age, the market is divided into 1 to 3 years old, 4 to 7 years old, and more than 8 years old.

1 to 3 Years Old

Vehicles within this category represent premium resale inventory. Most originate from leasing returns or corporate fleets. Buyers benefit from modern features at reduced prices relative to new vehicles. Financing approval rates remain strong due to predictable depreciation profiles. This segment contributes disproportionately to revenue despite lower availability.

4 to 7 Years Old

The 4 to 7-year-old segment is currently dominating the used car market due to its appeal among buyers seeking nearly new vehicles at reduced prices compared to new models. This age group typically includes certified pre-owned cars that come with warranties and have undergone rigorous inspections, making them attractive options for risk-averse consumers. Major OEMs such as Honda and BMW have reported strong sales in this category as buyers look for reliability without paying full price. This segment is foreseen to grow with 44.80% of the market share in 2025.

The four-to-seven-year category forms the operational core of global resale activity. Vehicles remain technologically relevant while offering meaningful affordability advantages. Maintenance costs typically remain manageable during this ownership phase. Demand stability makes this segment central to dealership profitability.

More than 8 Years Old

The more than 8-year-old segment is experiencing rapid growth as budget-conscious consumers increasingly turn to older vehicles amid rising new car prices. This trend is particularly pronounced in developing markets where affordability is paramount. Organizations such as Kelley Blue Book have noted a significant uptick in interest for older models due to their lower purchase costs despite potentially higher maintenance needs. This segment is expected to register a considerable CAGR of 8.30% during the forecast period (2025-2032).

Older vehicles dominate transaction volumes in emerging markets where affordability outweighs feature preference. Although margins remain lower, demand remains resilient due to essential mobility requirements. Refurbishment ecosystems increasingly extend usable vehicle lifecycles, sustaining liquidity within this category and reinforcing long-term used car market expansion dynamics.

Regional Insights

Based on the region, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia-Pacific Used Car Market Analysis:

Asia Pacific is the Dominant Market Owing to Increasing Vehicle Ownership in Emerging Markets

Asia Pacific Used Cars Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The Asia Pacific market accounted for USD 410.13 billion in 2025, representing 35.38% of the global industry, and is expected to reach USD 458.88 billion in 2026. The region holds the largest market share and is expected to witness the fastest growth during the forecast period. This dominance is driven by rapid urbanization, rising disposable incomes, and a growing middle class in countries such as China and India.

Asia-Pacific represents the fastest-expanding used car market growth region, driven by rising vehicle ownership turnover and expanding middle-income populations. Market formalization remains uneven across countries, creating opportunities for organized platforms. Financing penetration and digital inspection systems increasingly improve buyer trust. Urbanization pressures and affordability considerations sustain strong resale demand, particularly across developing economies experiencing accelerated personal mobility adoption.

China is estimated to reach a market value of USD 156.08 billion in 2026. The expansion of organized businesses offering used car trading services has further facilitated this growth. For instance, companies such as Alibaba and CarMax are enhancing their online platforms to cater to the increasing demand for used vehicles. India is estimated to gain USD 71.8 billion in 2026, while the Japanese market is poised to reach USD 53.07 billion in the same year.

Japan Used Car Market:

Japan maintains a highly efficient resale ecosystem supported by strict vehicle inspection regulations and predictable ownership cycles. Vehicles typically enter secondary markets in strong mechanical condition, enhancing export competitiveness. Domestic demand remains stable, while international shipments significantly influence pricing structures. Auction-based distribution systems dominate transactions, ensuring transparency and liquidity within the Japanese used car market supply chain.

China Used Car Market:

China’s used car market continues transitioning from fragmentation toward organized digital platforms and standardized inspections. Policy reforms reducing interprovincial transfer restrictions have improved inventory mobility. Increasing vehicle ownership maturity expands resale supply volumes annually. Consumer acceptance of certified vehicles strengthens organized dealer participation. Electrification growth introduces emerging resale valuation models, reshaping long-term used car market trends across major metropolitan regions.

North America Used Car Market Analysis:

North America is the second-largest market expected to hold USD 363.31 billion in 2025, documenting a CAGR of 6.30% during the forecast period (2025-2032). North America continues to be a key player in the used car market, with growth driven by changing consumer preferences for more affordable vehicle options in light of rising new car prices and inflation. The rise of certified pre-owned programs has enhanced buyer confidence in purchasing used vehicles. Major companies like AutoNation and eBay Motors are utilizing online platforms to improve accessibility and streamline the buying of a used car process, catering to the needs of modern consumers seeking convenience. This digital shift is significantly reshaping the landscape of vehicle sales in the region. The U.S. market is estimated to acquire USD 274.59 billion in 2026.

North America represents one of the most structured resale ecosystems within the global used car market, supported by leasing penetration and organized dealer networks. High vehicle replacement frequency sustains inventory inflow across certified and independent channels. Digital retail adoption continues to accelerate transaction efficiency. Financing accessibility and vehicle history transparency tools strengthen buyer confidence, supporting stable used car market growth despite interest rate sensitivity influencing purchasing timing.

United States Used Car Market:

The United States dominates the regional used car market size due to large vehicle parc volumes and a mature financing infrastructure. Lease returns and fleet disposals consistently replenish supply pipelines. Online marketplaces increasingly influence pricing discovery and inventory distribution. Rising new vehicle prices continue redirecting consumers toward resale alternatives. Certified pre-owned programs expand manufacturer participation, reinforcing structured market share consolidation among organized dealerships and digital platforms.

Europe Used Car Market Analysis:

In 2025, Europe generated USD 134.46 billion, contributing 11.60% to global market revenue, and is projected to grow to USD 144.81 billion in 2026. The region holds a substantial share, characterized by diverse consumer preferences across various countries. The U.K. market continues to grow, projected to reach a market value of USD 38.73 billion in 2026. However, it faces challenges such as stringent emissions regulations and a relatively slower adoption rate of electric vehicles compared to other regions. Germany is poised to hold USD 46.81 billion in 2026, while the market in France is expected to reach USD 26.24 billion in 2025.

Europe demonstrates stable used car market trends shaped by regulatory oversight, emissions policies, and cross-border vehicle trade. Electrification transition influences depreciation cycles, particularly for diesel inventories. Leasing models across Western Europe generate a predictable resale supply. Buyers increasingly prioritize fuel efficiency and regulatory compliance. Digital vehicle certification frameworks improve transparency, enabling organized players to capture the growing used car market share within fragmented national ecosystems.

Germany Used Car Market:

Germany functions as a major redistribution hub within the European used car market due to strong automotive production and leasing maturity. Premium vehicle resale demand remains consistent domestically and across export markets. Electrified vehicle penetration introduces valuation recalibration challenges. Dealer-backed certification programs support buyer assurance. Export-driven trade flows significantly influence inventory pricing dynamics and reinforce Germany’s strategic importance in regional market liquidity.

United Kingdom Used Car Market:

The United Kingdom's used car market benefits from advanced digital retail adoption and structured financing availability. Subscription mobility models and fleet renewals continue supplying younger resale vehicles. Economic uncertainty periodically influences purchasing cycles; however, affordability advantages sustain demand resilience. Online-first dealerships increasingly reshape transaction processes. Regulatory emphasis on emissions compliance also accelerates the transition toward hybrid and electric vehicles within resale inventories.

Latin America Used Car Market Analysis:

Latin America demonstrates strong reliance on resale vehicles due to affordability constraints and currency volatility impacting new vehicle purchases. Informal dealer networks remain influential, although digital marketplaces gradually improve transparency. Import regulations and taxation structures shape inventory availability. Demand remains resilient across economic cycles, supporting consistent used car market size expansion driven primarily by essential mobility requirements rather than discretionary upgrades.

Middle East & Africa Used Car Market Analysis:

Middle East and Africa markets rely heavily on imported resale vehicles alongside domestic trade activity. Demand growth is supported by population expansion and infrastructure development. Price sensitivity shapes purchasing behavior, favoring durable vehicle categories. Organized dealership penetration remains limited but expanding gradually through digital platforms, improving pricing transparency and transaction security across regional resale ecosystems.

Used Car Industry Competitive Landscape

Key Industry Players

CarMax is a Key Player in the Market, Backed by an Innovative and Customer-Centric Approach

CarMax has established itself as a dominant force due to its innovative approach to automotive retailing, which emphasizes transparency and customer satisfaction. The company's unique no-haggle pricing model allows customers to know the exact price they will pay without the stress of negotiation. This model resonates particularly with consumers who value simplicity and honesty in their transactions. In fiscal year 2024, CarMax sold approximately 770,000 used vehicles, showcasing its extensive reach and operational efficiency in the market.

CarMax has also invested heavily in enhancing its omnichannel retail experience, combining online and physical sales platforms to meet changing consumer preferences. This strategy includes features such as home delivery and virtual consultations, which cater to a growing demographic of tech-savvy buyers who prefer online shopping experiences. Furthermore, CarMax's commitment to operational efficiency has led to significant cost-cutting measures, allowing the company to maintain profitability even amidst market fluctuations. The integration of advanced technologies for inventory management and customer engagement further solidifies CarMax's competitive edge, ensuring its continued leadership in the used car market.

The used car market's competitive environment is undergoing a structural transformation as digitalization reshapes sourcing, pricing transparency, and distribution efficiency. Historically fragmented dealer-led ecosystems are gradually consolidating through technology-enabled intermediaries, integrated financing providers, and manufacturer-backed certified programs. Competitive differentiation increasingly depends on inventory access, data analytics capability, and consumer trust mechanisms rather than physical dealership scale alone.

OEM-affiliated certified pre-owned ecosystems, leveraging brand assurance, inspection standards, and warranty extensions to capture higher-value transactions. These programs strengthen manufacturer lifecycle monetization strategies while stabilizing residual vehicle values. Digital-first marketplaces and platform aggregators, which focus on inventory discovery, pricing intelligence, and logistics integration. Algorithm-driven valuation models improve transaction speed and reduce negotiation friction, attracting urban consumers seeking transparent purchasing processes.

Independent dealer networks and regional resellers, which continue dominating volume-driven markets, particularly in emerging economies, where informal sourcing channels remain significant. Competition increasingly centers around control of supply pipelines. Access to lease returns, fleet disposals, rental vehicles, and corporate mobility assets provides pricing advantages and inventory stability. Companies investing in refurbishment infrastructure and reconditioning hubs demonstrate stronger margin resilience.

LIST OF KEY COMPANIES PROFILED:

- CarMax (U.S.)

- AutoNation Inc. (U.S.)

- Asbury Automotive Group Inc. (U.S.)

- Alibaba Group Holding Ltd. (China)

- Cox Automotive Inc. (U.S.)

- Mahindra First Choice Wheels Ltd. (India)

- TrueCar Inc. (U.S.)

- Penske Automotive Group Inc. (U.S.)

- Hendrick Automotive Group (U.S.)

- Carvana Co. (U.S.)

Latest Used Car Industry Developments:

January 2024: CarMax Inc. expanded its artificial intelligence–based vehicle appraisal platform across nationwide operations to improve pricing accuracy and inventory acquisition efficiency. The initiative aimed to strengthen sourcing consistency amid fluctuating vehicle supply conditions. The system integrates predictive valuation analytics, demand forecasting algorithms, and automated inspection data processing capabilities.

March 2024: Auto1 Group SE enhanced its cross-border digital wholesale marketplace infrastructure across European markets to optimize dealer-to-dealer inventory redistribution. The strategic objective focused on balancing regional supply imbalances and accelerating vehicle turnover cycles. The upgrade incorporated logistics optimization software, real-time pricing intelligence, and automated dealer transaction management systems.

July 2024: Lithia Motors Inc. accelerated investment in centralized vehicle reconditioning hubs supporting omnichannel used vehicle retail expansion. The move targeted operational margin improvement through standardized refurbishment processes and faster inventory readiness. Facilities deployed advanced diagnostics platforms, digital inspection workflows, and integrated supply chain coordination technologies.

February 2025: Cazoo Group Ltd. restructured its operating model toward marketplace-led asset-light transactions following earlier inventory-heavy expansion challenges. The strategic adjustment aimed to improve capital efficiency while maintaining digital customer acquisition advantages. Platform upgrades emphasized third-party dealer integration, digital financing interfaces, and automated listing management systems.

May 2025: Penske Automotive Group Inc. expanded certified pre-owned vehicle programs across premium dealership networks to capture higher-margin used vehicle demand segments. The initiative strengthened lifecycle vehicle monetization strategies aligned with manufacturer partnerships. Implementation included standardized inspection protocols, warranty management systems, and connected vehicle history verification technologies.

REPORT COVERAGE

The used cars market report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, vehicle type, and leading product applications. Besides this, it offers insights into the market trends and highlights vital industry developments. In addition to the factors above, the report encompasses several factors that have contributed to the market's growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

6.43% from 2026 to 2034 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Sales Channel Type · Offline · Online |

|

By Fuel Type · Petrol · Diesel · CNG · Electric |

|

|

By Distribution Channel · Franchised Dealer · Independent Dealer · C2C |

|

|

By Vehicle Type Hatchbacks o Economy o Premium o Luxury Sedan o Economy o Premium o Luxury SUVs o Economy o Premium o Luxury |

|

|

By Age · 1 to 3 years old · 4 to 7 years old · More than 8 Years old |

|

|

By Region North America ( By Sales Channel Type, By Vehicle Type, By Fuel Type, By Distribution Channel, and By Age ) o U.S ( By Vehicle Type ) o Canada ( By Vehicle Type ) o Mexico ( By Vehicle Type ) · Europe ( By Sales Channel Type, By Vehicle Type, By Fuel Type, By Distribution Channel, and By Age ) o U.K. ( By Vehicle Type ) o Germany ( By Vehicle Type ) o France ( By Vehicle Type ) o Rest of Europe ( By Vehicle Type ) · Asia Pacific ( By Sales Channel Type, By Vehicle Type, By Fuel Type, By Distribution Channel, and By Age ) o China ( By Vehicle Type ) o Japan ( By Vehicle Type ) o India ( By Vehicle Type ) o South Korea ( By Vehicle Type ) o Rest of APAC ( By Vehicle Type ) · Rest of the World ( By Sales channel Type, By Vehicle Type, By Fuel Type, By Distribution Channel, and By Age ) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1,159.31 billion in 2025 and is projected to reach USD 2,080.27 billion by 2034.

In 2025, Asia Pacific stood at USD 410.13 billion.

The market is projected to grow at a CAGR of 6.43% over the forecast period (2026-2034).

The vehicle type segment is expected to lead this market during the forecast period.

Market is driven by increasing demand for vehicle ownership in emerging economies.

CarMax (U.S.). is a major player in the global market.

Asia Pacific dominated the global market with a share of 35.38% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us