Generic Pharmaceuticals Market Size, Share & Industry Analysis, By Type (Simple Generics, Specialized Generics, and Complex Generics), By Therapeutic Indication (Cardiovascular, CNS, Anti-infectives, Endocrine & Metabolic, Gastrointestinal, Respiratory, Dermatology, Oncology & Supportive Care, Pain Management, Vitamins, Minerals & Nutritional, and Others), By Route of Administration (Oral, Parenteral, Topical, Inhalation, and Others), By Distribution Channel (Hospital Pharmacies, Drug Stores & Retail Pharmacies, Online Pharmacies, and Others), and Regional Forecast, 2026-2034

Generic Pharmaceuticals Market Size and Future Outlook

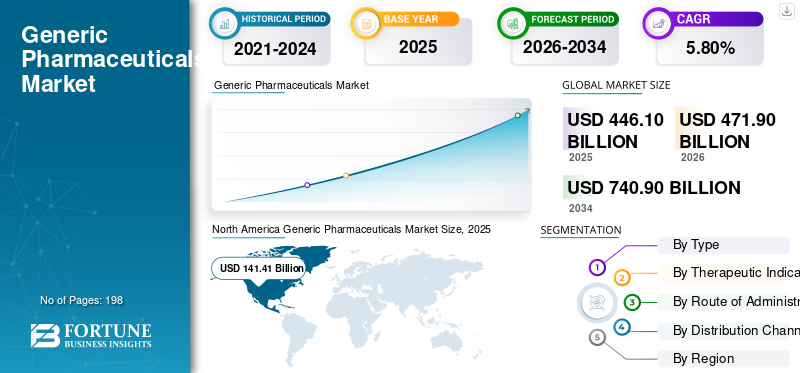

The global generic pharmaceuticals market size was valued at USD 446.10 billion in 2025. The market is projected to grow from USD 471.90 billion in 2026 to USD 740.90 billion by 2034, exhibiting a CAGR of 5.80% during the forecast period. North America dominated the generic pharmaceuticals market with a market share of 31.7% in 2025.

The global generic pharmaceuticals market encompasses off-patent pharmaceutical products that are therapeutically equivalent to branded drugs and are used across high-volume treatment areas such as cardiovascular diseases, CNS disorders, anti-infectives, endocrine & metabolic diseases, gastrointestinal disorders, respiratory conditions, dermatology, oncology supportive care, pain management, and nutrition-related therapies. The market is driven by the rising need for cost-effective medicines, patent expiries of branded drugs, increasing chronic disease burden, and government-led efforts to improve access to affordable treatments. Demand is further supported by the wide availability of oral solids, injectables, topical products, inhalation therapies, and other dosage forms across hospital pharmacies, retail pharmacies, drug stores, and online pharmacy channels.

Key players operating in the global market include Teva Pharmaceutical Industries, Sandoz, Viatris, Sun Pharmaceutical Industries, and Aurobindo Pharma. These companies are focusing on broad generic portfolios, strong ANDA and regulatory filing capabilities, large-scale manufacturing networks, established distribution channels, and increasing focus on complex generics, injectables to strengthen their market presence.

Download Free sample to learn more about this report.

Generic Pharmaceuticals Market Key Takeways

- 2025 Market Size: USD 446.10 billion

- 2026 Market Size: USD 471.90 billion

- 2034 Forecast Market Size: USD 740.90 billion

- CAGR: 5.80% from 2026–2034

- North America dominated the generic pharmaceuticals market with a 31.7% share in 2025.

- The oral segment is projected to hold the largest market share of 62.3% in 2026.

- The drug stores & retail pharmacies segment is expected to account for 52.2% of the market in 2026.

North America

North America led the global market with a valuation of USD 141.41 billion in 2025, maintaining its dominant position.

Europe

Europe is projected to expand at a 4.93% CAGR during the forecast period, supported by government cost-containment initiatives and strong public healthcare systems.

Asia Pacific

Asia Pacific is expected to reach a market value of USD 136.33 billion by 2026, driven by increasing demand for affordable medicines.

U.S.

U.S. The market is projected to reach approximately USD 138.56 billion by 2026.

Japan

Japan The market is estimated to reach around USD 22.67 billion by 2026.

Read More

GENERIC PHARMACEUTICALS MARKET TRENDS

Strong Government Support for Generic Substitution is a Major Trend Observed in Global Market

Robust governmental backing for generic substitution is emerging as a significant growth trend in the global market as healthcare systems face pressure to minimize medicine expenses while ensuring access to treatments. Authorities and regulators are urging doctors, pharmacists, hospitals, and insurers to turn to cheaper generic options when name-brand medications become non-exclusive. This trend boosts the volume of generic prescriptions, enhances substitution at the pharmacy level, and facilitates quicker adoption of straightforward, specialized, and complex generics. It is particularly crucial in chronic illness sectors such as cardiovascular diseases, diabetes, CNS conditions, respiratory illnesses, pain relief, and anti-infectives, where prolonged medication usage leads to significant cost pressure. With the increasing structure of generic substitution via policies, reimbursement guidelines, and expedited regulatory review processes, manufacturers are encouraged more effectively to enhance product submissions, production capabilities, and distribution networks. This directly boosts market expansion by enhancing affordability, expanding patient access, and reinforcing competition against expensive branded drugs. These factors are supporting the overall global generic pharmaceuticals market growth.

- For instance, in October 2025, the U.S. FDA announced a new ANDA prioritization pilot program to support generic drug manufacturing and testing in the U.S. The program aims to provide faster review for certain abbreviated new drug applications and strengthen the domestic generic pharmaceutical supply chain, showing direct regulatory support for expanding access to generic medicines.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Affordable Medicines to Boost Market Growth

Increasing need for cost-effective medications significantly influences the worldwide Generic Pharmaceuticals Market as patients, healthcare facilities, insurers, and governments seek to lower treatment expenses while ensuring access to vital therapies. Generic medications alleviate this pressure by providing therapeutically comparable options to branded drugs at reduced costs. This is particularly crucial for chronic illnesses like diabetes, cardiovascular issues, CNS disorders, respiratory ailments, and digestive conditions, as patients require ongoing medication. With the rise in medicine expenditures, healthcare systems are promoting greater adoption of generics by implementing prescribing policies, substitution regulations, reimbursement assistance, and public procurement initiatives. This boosts prescription quantities for basic generics, while simultaneously providing chances for specialized and intricate generics in injectables, inhalation products, and other more valuable dosage forms. Consequently, the pressure of affordability directly encourages the use of generic drugs in hospital pharmacies, retail pharmacies, and online pharmacy platforms.

- For instance, in August 2025, Teva Pharmaceutical Industries announced the FDA approval and U.S. launch of generic Saxenda (liraglutide injection), the first generic GLP-1 indicated for weight management. The company stated that the launch addresses increased demand for this therapy category in the U.S. market and supports its complex generic medicine portfolio.

MARKET RESTRAINTS

Regulatory and Quality Compliance Burden to Limit Market Growth

Regulatory and quality compliance burden acts as a major restraint for the global market growth as generic manufacturers must consistently meet strict GMP, bioequivalence, stability, data integrity, and manufacturing documentation standards. Any failure in inspection, testing, validation, or quality control can delay approvals, block product launches, trigger recalls, or restrict imports into key markets such as the U.S. and Europe. This is especially challenging for companies manufacturing high-volume oral generics, sterile injectables, complex generics, inhalation products, and API-dependent formulations. As regulators increase scrutiny on manufacturing sites and data reliability, companies need higher investment in quality systems, facility upgrades, audits, and remediation activities. These added costs reduce margins in an already price-sensitive market and can make some low-margin generic products commercially unattractive. Therefore, compliance pressure limits supply continuity, slows new generic entry, and creates operational risk for manufacturers.

- For instance, in July 2025, the U.S. FDA issued a warning letter to Glenmark Pharmaceuticals Limited after inspecting its Madhya Pradesh, India facility from February 3–14, 2025. The FDA cited significant violations of current Good Manufacturing Practice regulations for finished pharmaceuticals, showing how quality compliance issues can directly affect generic drug manufacturing and regulatory confidence.

MARKET OPPORTUNITIES

Increasing Patent Expiry of Branded Drugs to Offer Lucrative Opportunities

The rising expiration of patents for branded medications is generating substantial opportunities in the global market, as it allows generic producers to access lucrative therapeutic domains that were once controlled by original brand companies. When exclusivity concludes, firms can introduce more affordable versions and swiftly attract demand from patients, pharmacies, hospitals, and payers seeking cost-effective options. This chance is particularly significant in long-term and high-expense areas including diabetes, obesity, heart diseases, CNS conditions, respiratory medications, oncology support, and anti-infective treatments. Patent expirations also motivate firms to invest in intricate generics such as injectables, inhalation products, long-lasting formulations, and prefilled pens, as competition is reduced and profit margins are higher. With the expiration of protections for more blockbuster drugs, generic companies possessing robust regulatory, clinical, and manufacturing skills can develop unique portfolios. This establishes a distinct growth trajectory for both international and local businesses, simultaneously enhancing access to medicine and reducing healthcare expenses. All these factors would drive the market growth in the coming years.

- For instance, in January 2026, Sun Pharmaceutical Industries received DCGI approval to manufacture and market generic semaglutide injection in India. The company stated that it would launch the product under the brand name Noveltreat after the expiry of the semaglutide patent in India, showing how patent expiry is creating new opportunities for generic companies in high-demand metabolic and weight-management therapies.

MARKET CHALLENGES

Complex Manufacturing Requirements for High-Value Generics Pose a Prominent Challenge to Market Growth

The global market faces significant difficulties due to intricate manufacturing demands, as expansion progressively transitions from basic oral generics to more complex offerings such as inhalers, injectables, ophthalmic, topical formulations, long-acting products, and drug-device combinations. These products require sophisticated formulation development, specialized production lines, rigorous device performance testing, sterility measures, and more comprehensive regulatory documentation. Consequently, the time needed for development is extended, and the capital needed is significantly greater than for simple tablets or capsules. Lesser-known generic firms might struggle to compete in these sectors due to their requirement for scientific knowledge, clinical or in-vitro proof, and specialized manufacturing capabilities. Any variation in manufacturing can impact bioequivalence, product efficacy, and timelines for approval. Consequently, although intricate generics provide improved margins, they establish greater entry hurdles and restrict the number of firms capable of successfully introducing such products. All the factors cumulatively affect the market growth.

- For instance, in December 2025, Amneal Pharmaceuticals received the U.S. FDA approval for generic albuterol sulfate inhalation aerosol, a generic version of ProAir HFA. The company highlighted it as its second complex respiratory therapeutic product approval in Q4 2025, showing that inhalation generics require specialized respiratory formulation and device capabilities, which makes this segment more difficult to develop and manufacture than simple oral generics.

Segmentation Analysis

By Type

Simple Generics Segment Dominated Due to High Prescription Volumes, Lower Development Cost, and Broad Use Across Chronic Diseases

In terms of type, the market is divided into complex generics, simple generics, and specialized generics.

The simple generics segment led the global generic pharmaceuticals market share in 2025. As these products include high-volume tablets, capsules, and conventional oral formulations used widely across various therapeutics indications. Moreover, simple generics require lower development cost, shorter regulatory pathways, and relatively easier manufacturing scale-up, which allows more companies to enter the market and supply large patient populations. Their demand is also supported by strong use in retail pharmacies and drug stores, where chronic prescriptions are repeatedly refilled. In addition, payers and public health systems prefer simple generics as they reduce treatment costs while maintaining therapeutic equivalence to branded drugs.

- For instance, in May 2025, Lupin launched Tolvaptan Tablets, 15 mg, 30 mg, 45 mg, 60 mg, and 90 mg, in the U.S. after receiving U.S. FDA approval for its ANDA.

The complex generics segment is anticipated to rise with a CAGR of 7.99% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Therapeutic Indication

Endocrine & Metablic Segment to Grow Fastest Due to Soaring Prevalence of Metabolic Disorders

Based on therapeutic indication, the market is classified into cardiovascular, CNS, anti-infectives, endocrine & metabolic, gastrointestinal, respiratory, dermatology, oncology & supportive care, pain management, vitamins, minerals & nutrition, and others.

The endocrine & metabolic segment is expected to grow at a fastest CAGR of 6.69% over the forecast period. The soaring prevalence of metabolic disorders is anticipated to boost demand and drive segmental growth.

The others segment accounted for the dominant market share in 2025. The wider disease coverage increases prescription volume across both chronic and acute care settings. The segment is also supported by frequent generic launches in ophthalmic, urological, renal, and specialty supportive therapies where branded products have lost exclusivity. Moreover, the others segment benefits from a broader product base, higher molecule diversity, and demand across retail, hospital, and online pharmacy channels. This makes it a major revenue-generating therapeutic indication segment in the global market. Furthermore, the segment is set to hold 15.7% share in 2026.

- For instance, in September 2025, Amneal Pharmaceuticals received U.S. FDA approval for Bimatoprost Ophthalmic Solution 0.01%, a generic version of LUMIGAN for reducing elevated intraocular pressure in patients with open-angle glaucoma or ocular hypertension.

By Route of Administration

Oral Segment Dominated Due to High Patient Convenience, Large Prescription Base, and Strong Use in Chronic Disease Treatment

On the basis of route of administration, the market is divided into oral, parenteral, topical, inhalation, and others.

In 2025, the market was primarily led by the oral segment. This segment is the most widely prescribed and easily administered generic dosage forms across chronic and acute conditions. Additionally, oral drugs are easier to manufacture, store, distribute, and dispense through retail pharmacies, hospital pharmacies, and online pharmacies. Their high patient acceptance and suitability for home-based treatment also support repeated prescription refills, especially for chronic disease management. Furthermore, the segment is set to hold 62.3% share in 2026.

- For instance, in April 2025, Aurobindo Pharma received the U.S. FDA approval for Oxcarbazepine Extended-Release Tablets, 150 mg, 300 mg, and 600 mg, an AB-rated generic equivalent to Oxtellar XR for treatment of partial-onset seizures.

The parenteral segment is anticipated to rise with a CAGR of 7.14% over the forecast period.

By Distribution Channel

Drug Stores & Retail Pharmacies Segment Dominated Due to High Prescription Refills, Easy Access, and Strong Use in Chronic Disease Treatment

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, online pharmacies, and others.

The drug stores & retail pharmacies segment dominated the market share in 2025. The dominance of the segment is attributed to the fact that most generic medicines are dispensed through community-based pharmacy networks for routine and long-term treatment. The segment is also supported by strong patient preference for local pharmacy care and the availability of lower-cost generic alternatives at the point of dispensing. As retail pharmacies continue to combine physical access with digital refill tools and prescription management services, they remain the main channel for high-volume generic drug distribution. Furthermore, the segment is set to hold 52.2% share in 2026.

- For instance, in October 2025, CVS Health released its 2025 Rx Report, highlighting the continued transformation of community pharmacy and noting its network of more than 9,000 community health destinations.

In addition, online pharmacies are projected to witness 10.41% growth rate during the forecast period.

Generic Pharmaceuticals Market Regional Outlook

Based on region, the global market is divided into Asia Pacific, Latin America, Europe, North America, and the Middle East & Africa.

North America

Request for Customization to gain extensive market insights.

The North America’s market was valued at USD 134.49 billion in 2024 and dominated the global market. In 2025, the region maintained its leading position, with USD 141.41 billion. The regional growth is driven by the strong use of generic substitution, high healthcare spending, and continuous patent expiries of branded drugs. The region also supports growth through faster ANDA approvals, increasing use of complex generics, and strong demand for oral generics, injectables, inhalation products, and specialty generics.

U.S. Generic Pharmaceuticals Market

The U.S. market led the North American region and is projected to be approximately USD 138.56 billion in 2026, representing about 29.4% of the global market.

Europe

Europe’s market is growing at a CAGR of 4.93% during the forecast period. Europe’s growth is supported by government-led cost-containment programs, reference pricing systems, and strong public healthcare focus on affordable medicines. The market also benefits from aging populations, high chronic disease prevalence, and broad use of generics in cardiovascular, gastrointestinal, CNS, anti-infective, and pain management therapies.

U.K. Generic Pharmaceuticals Market

The U.K. market is estimated at around USD 21.92 billion in 2026, representing roughly 4.6% of global revenues.

Germany Generic Pharmaceuticals Market

Germany‘s market size is projected to reach approximately USD 23.60 billion in 2026, equivalent to around 5.0% of global sales.

Asia Pacific

The Asia Pacific’s market size is expected to reach a valuation of USD 136.33 billion by 2026. Asia Pacific is one of the fastest-growing regions due to its large patient population, expanding healthcare access, and strong presence of cost-efficient generic drug manufacturers. India and China are major production hubs for APIs and finished generic formulations, supporting both domestic consumption and exports.

Japan Generic Pharmaceuticals Market

The Japanese market is estimated at around USD 22.67 billion in 2026, accounting for roughly 4.8% of global revenues.

China Generic Pharmaceuticals Market

China’s market is projected to reach revenues of around USD 43.78 billion in 2026, representing roughly 9.3% of global sales.

India Generic Pharmaceuticals Market

The Indian market is estimated at around USD 18.51 billion in 2026, accounting for roughly 3.9% of global revenues.

Latin America and Middle East & Africa

The growth in the Middle East & Africa and Latin America regions is anticipated to be moderate in the coming years. Key factors such as increasing demand for low-cost medicines, expanding public healthcare programs, and rising chronic disease treatment needs are expected to boost the market growth in these regions. The Latin America’s market is estimated at around USD 38.33 billion in 2026.

GCC Generic Pharmaceuticals Market

The GCC market is projected to reach approximately USD 11.77 billion by 2026, representing about 2.5% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Broad Oral Generics, Complex Generics, Injectables, Respiratory, and Specialty Portfolios to Support Players’ Market Position

The global generic pharmaceuticals market reflects a highly competitive landscape, consisting of large multinational generic companies, Indian formulation exporters, injectable manufacturers, and specialty generic players. Key players include Teva Pharmaceutical Industries, Sandoz, Viatris, Sun Pharmaceutical Industries, Aurobindo Pharma, Dr. Reddy’s Laboratories, and Cipla. Their market position is supported by large-scale manufacturing, strong regulatory filing capabilities, global distribution networks, and established relationships with hospital, retail, and online pharmacy channels.

- For instance, in May 2025, Lupin launched Tolvaptan Tablets in the U.S. with 180-day exclusivity, strengthening its oral generic portfolio.

Other significant participants include Lupin, Hikma Pharmaceuticals, Fresenius Kabi, Amneal Pharmaceuticals, and STADA. These firms are also focusing on complex generics, injectable launches, respiratory products, and regional expansion to strengthen their presence.

LIST OF KEY GENERIC PHARMACEUTICALS COMPANIES PROFILED IN REPORT

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sandoz Inc. (Switzerland)

- Viatris Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Aurobindo Pharma Limited. (India)

- Reddy’s Laboratories Ltd. (India)

- Cipla (India)

- Lupin (India)

- Amneal Pharmaceuticals LLC. (U.S.)

- STADA Arzneimittel AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Aurobindo Pharma received USFDA approval for Dextromethorphan Polistirex Extended-Release Oral Suspension, 30 mg/5 mL OTC, a generic equivalent to Delsym Extended-Release Oral Suspension. This supports the company’s presence in oral OTC generics.

- March 2026: Hikma launched an authorized generic version of Nucynta ER (tapentadol) extended-release for U.S. patients. The company stated that, at launch, it was the first available generic of this product in the U.S.

- January 2026: Reddy’s announced the first-to-market U.S. launch of Olopatadine Hydrochloride Ophthalmic Solution USP, 0.7% OTC, the generic equivalent of Extra Strength Pataday Once-Daily Relief. The launch expanded its OTC eye-care generic portfolio.

- December 2025: Viatris received U.S. FDA approval for the generic version of Sandostatin LAR Depot — octreotide acetate for injectable suspension. The company highlighted this as its first approved injectable using microsphere technology and its fourth injectable FDA approval in 2025.

- November 2025: Fresenius Kabi introduced Dalbavancin for Injection in the U.S. The product supports its hospital-focused injectable generics portfolio, especially in anti-infective therapy.

REPORT COVERAGE

The global generic pharmaceuticals market analysis includes a thorough evaluation of the market size and forecasts for every segment highlighted in the report. It offers insights into the market dynamics and trends expected to drive the market throughout the forecast period. The global market report provides understanding of essential factors, including technological progress, product innovations, the regulatory environment, and the launch of new products. Additionally, it details partnerships, mergers & acquisitions, as well as key developments within the market. The global market forecast report also provides an in-depth competitive landscape, including information on market share and profiles of key active players.

North America Generic Pharmaceuticals Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.80% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Therapeutic Indication, Route of Administration, Distribution Channel, and Region |

| By Type |

|

| By Therapeutic Indication |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 446.10 billion in 2025 and is projected to reach USD 740.90 billion by 2034.

In 2025, the North America’s market value stood at USD 141.41 billion.

The market is expected to exhibit a CAGR of 5.80% during the forecast period of 2026-2034.

By type, the simple generics segment led the market in 2025.

Rising demand for affordable medicine and expansion of retail pharmacy chains are primarily driving market expansion.

Teva Pharmaceutical Industries Ltd., Sandoz Inc., Viatris Inc., Sun Pharmaceutical Industries Ltd., Aurobindo Pharma Limited, and Dr. Reddy’s Laboratories Ltd. are the top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 198

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us