GEO Satellite Market Size, Share, Industry Analysis, By Propulsion (Chemical, Electric, and Hybrid), By Type (Small GEO (<2000 kg), Medium GEO (2000-4000 kg), and Large GEO (>4000 kg)), By Application (Telecommunication, Earth Observation, Surveillance & Intelligence, Navigation, and Others), By End User (Commercial, Government and Military, Civil, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

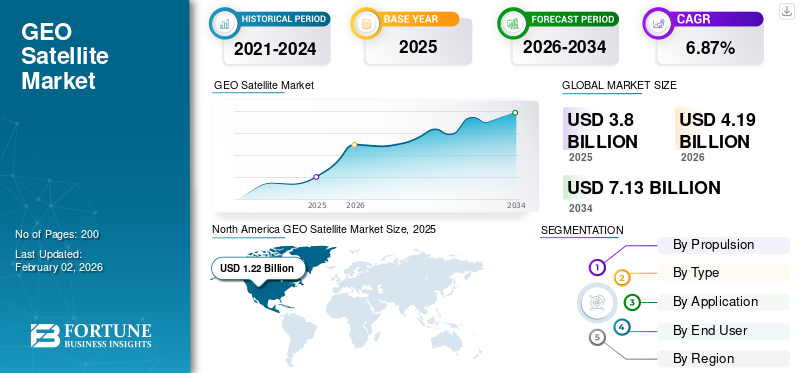

The global GEO satellite market size was valued at USD 3.80 billion in 2025. The market is projected to grow from USD 4.19 billion in 2026 to USD 7.13 billion by 2034, exhibiting a CAGR of 6.87% during the forecast period. North America dominated the GEO satellite market with a market share of 32.23% in 2025.

Geostationary satellites are in a geostationary orbit, which is at a height that is nearly 35,786 km and maintains the satellite stationary over one longitude at the equator. These satellites seem to be stationary above a specific location above the equator. Following such a satellite does not require ground-based receiving and transmitting antennas. These antennas are far less expensive than tracking antennas and may be mounted in a fixed location. These satellites have transformed weather prediction, television broadcasting, and worldwide communications. They also have several significant military and intelligence uses.

The rising demand for broadband connectivity, increase in defense, intelligence and government based applications are the key driving factors in the market.

Key players include leading satellite operators such as NASA, ISRO, Thales Group, and SES, among others. These companies are focused on investing in technological upgradation and satellite launches for geostationary orbit owing to an increase in demand by commercial and private enterprises.

For the majority of leading space players, the COVID-19 pandemic has hindered mission deployments and slowed the delivery of new goods as a result of supply chain issues. Through expedited and advance payments, space agencies have offered substantial financial and administrative assistance to government contractors in Asia, Europe, and North America.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Escalated Demand for High-Capacity Telecommunications Broadcasting and Broadband Services to Bolster Market Growth

GEO satellites are positioned to deliver consistent and wide area coverage, making them indispensable for television broadcasting, internet connectivity, and mobile communications. The integration of advanced technologies, such as high throughput satellites (HTS), electric propulsion, and modular designs, has enhanced the operational efficiency and lifespan of these satellites. The increasing reliance on satellite-based solutions to support 5G networks and Internet of Things (IoT) is also a significant driver.

Market Restraints

High Launch Cost and Maintaining Constellations of Satellites to Restrict Market Expansion

Launching satellites into GEO orbit is expensive due to the significant energy required to carry high payloads at high altitudes. The cost varies depending on launch vehicles, type of payload, and type of rocket (small, medium, and heavy). For example, India’s GSLV MK III launch cost is around USD 60 million per launch. This high upfront investment acts as a substantial barrier to entry for new market participants.

Furthermore, maintaining a constellation of GEO satellites brings technical and financial challenges. Ensuring continuous service requires parodic replenishment, upgrades, and deployment of backup satellites in some cases. Moreover, the complexity of managing multiple satellites in GEO orbit increases operational risks and requires a good ground infrastructure for command, control, and coordination, which add additional cost in the overall process.

Market Opportunities

Demand for High Resolution Earth Observation and Environmental Monitoring Services Offer Major Growth Opportunities

A significant market opportunity for GEO satellites is provision of real time, high resolution earth observation and environmental monitoring services. This application leverages the unique vantage point of geostationary orbit, enabling continuous surveillance over fixed geographic areas. As climate change natural disasters and resource management become increasingly critical global challenges, the demand for persistent, wide area monitoring is surging.

GEO satellites are equipped with advanced imaging and the sensor payloads attached can deliver uninterrupted data streams for weather forecasting, disaster detection, and other applications.

The expansion of high resolution imaging and analytics from GEO platform is also opening new commercial opportunities. Industries such as insurance energy and logistics are increasingly relying on satellite derived data for risk assessment, infrastructure minting, and supply chain optimization.

Market Challenges

Rise in Failure of GEO Satellite can Lead to Growth Challenge

The surge in failure of GEO satellites has emerged as a significant market challenge, impacting both operational reliability and business confidence in the sector. Even with advanced engineering, failures can occur due to onboard system malfunctions and exposure to harsh space environment such as elevated radiation levels at geostationary altitudes. The failure of GEO satellite can result in the loss of service to a vast geographic area or significant share of provider’s capacity.

- In October 2024, One of Intelsat's geostationary satellites appeared to break in orbit, causing the firm to announce a service outage on the Intelsat 33e satellite, which impacted users in Europe, Africa, and some areas of the Asia Pacific region.

The technical causes of satellite failures are diverse, ranging from component defects and software anomalies to external factors such as micrometeoroid impacts, space weather events, and others. Such incidents are a primary challenge for GEO satellite market growth.

GEO Satellite Market Trends

High-Throughput and Software-Defined Satellites is a Key Market Trend

A major trend in the market is the deployment of high-throughput satellites (HTS) and the shift toward software-defined payloads. HTS technology increases the bandwidth and data rates, enabling GEO satellites to support connectivity for broadband internet in remote areas. Software defined satellites offer flexibility, allowing operators to reconfigure coverage areas and satellite services profiles in response to changing market needs.

Furthermore, the growth of large LEO constellations is a big challenge, forcing GEO operators to come up with new and unique services, such as better coverage in particular areas or specialized uses that demand lower latency. Additionally, the market is seeing an increase in the integration of AI (artificial intelligence) and machine learning to enhance satellite operations and network performance. Additionally, the search for sustainable practices is becoming increasingly popular, with initiatives aimed at minimizing the environmental effect of satellite operations and extending the lifespan of satellites.

Download Free sample to learn more about this report.

Future Outlook - GEO Satellite Market

The future outlook of geostationary satellites is combined of technological evolution, new service opportunities, and intense competition. In February 2025, in just six years, Elon Musk's Starlink internet constellation has broken the near-complete monopoly that big satellites are held in geosynchronous equatorial orbit, or GEO, as the primary way of providing internet services from space.

According to Viasat, GEO satellites will continue to be a crucial element of satellite networks. Depending on the orbit, there are different benefits. For national or regional applications, geostationary satellites are by far the most cost-effective. Around sixty different countries around the globe issue licenses for geostationary satellites. The majority of those nations utilize their satellites for national or regional communication purposes. Many of the same nations view ownership and control of their space systems as essential to their national sovereignty and/or security. To provide the advantages of each for civil, commercial, and national security operations in accordance with globally shared and sustainable orbital resources, the company is collaborating closely with both international LEO and regional GEO satellite operators to integrate hybrid multiorbit and multiband satellite communication networks.

SEGMENTATION ANALYSIS

By Propulsion

Chemical Segment Dominated the Market Owing to its Extensive Usage in GEO Satellite Launches

Based on propulsion, the market is classified into chemical, electric, and hybrid.

In 2026, the chemical segment is projected to lead the market with a 43.27% share and is the fastest growing segment over the forecast period (2026-2034). The dominance of the segment is owing to high thrust, enabling rapid orbit insertion and station keeping. This propulsion type is reliable, which makes it a default choice for heavy and complex payloads.

The electric propulsion segment is anticipated to show significant growth during the study period. The segment is gaining momentum as it uses less propellant, allowing reduced launch cost. The growth is also driven by technological advancements and increased adoption in new satellite designs, among other factors.

To know how our report can help streamline your business, Speak to Analyst

By Type

Large GEO (>4000 kg) Segment Dominated the Market Owing to Multi-Mission Capabilities

Based on type, the market is segmented into small GEO (<2000 kg), medium GEO (2000-4000 kg), and large GEO (>4000 kg).

The large GEO (>4000 kg) segment is projected to dominate the market with a share of 47.59% in 2026 and is set to be the fastest growing segment over 2025-2032. These satellites are used for high throughput communications, broadcastings, and government missions. Such multi mission satellite capabilities make it flexible for operators to use for various payloads and purposes.

The medium GEO (2000-4000 kg) segment is anticipated to witness significant growth during the study period. There are various advantages of these satellites, such as faster manufacturing cycles and lower launch cost, and can be used to deploy experimental payloads. This gives the segment boost for market growth during the study period.

By Application

Telecommunication Segment Led the Market Impelled by Increasing Demand for High Speed Internet Access and Broadband Demand

By application, the segment is categorized into telecommunication, earth observation, surveillance & intelligence, navigation, and others.

The telecommunication segment is expected to lead the market, contributing 37.33% globally in 2026. GEO satellites are known to provide wide area data coverage in remote areas. Growth factor for the segment include proliferation of internet-enabled services, expansion of mobile networks, and increasing need for reliable, high bandwidth connectivity.

The earth observation segment is anticipated to show moderate growth during the study period. The segment has a growing application in the market owing to the purpose of persistent monitoring of weather, environmental changes, and disaster response. The growth is also owing to the rising importance of environmental intelligence, government investments in disaster preparedness, and others.

By End User

Commercial Segment Dominated with Rising Demand for Connectivity and Digital Solutions on Enterprise Level

By end user, the segment is categorized into commercial, government and military, civil, and others.

The commercial segment will account for 39.67% market share in 2026. The segment benefits from rising demand for data solutions and internet access on enterprise level. The product demand from telecom operators, internet service providers, and media companies aiming to expand their reach and service offerings further supports segment growth.

The government and military segment is anticipated to show significant growth during the study period. Governments are increasingly investing in satellite infrastructure to support defense modernization program, public services, and others. The growth of the segment is further escalated by geopolitical tensions and the need for reliable communication satellites network.

GEO SATELLITE MARKET REGIONAL OUTLOOK

Geographically, the market is segmented into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America GEO Satellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the North America market stood at USD 1.22 billion, representing 32.23% of global demand, and is projected to grow to USD 1.35 billion in 2026. The region leads the market driven by substantial research and development, robust ecosystem of commercial and defense satellite operators, and strong government support for space infrastructure. The presence of leading private sector players and focus on modernizing satellite fleets with software defined technologies further boost the regional growth.

The U.S. government, through agencies such as NASA and the Department of Defense, is a major end user. The U.S. market is projected to reach USD 0.91 billion by 2026. The country exhibits a significant product demand for secure communication, surveillance, and weather monitoring applications.

Europe

The Europe region captured 29.51% of the global market in 2025, generating USD 1.12 billion in revenue, and is projected to reach USD 1.24 billion in 2026. The European space agency (ESA) and national agencies in countries such as France, Germany, and U.K. play a pivotal role in advancing satellite technology for telecommunications, earth observation, and climate monitoring. Initiatives such as EU’s Copernicus program underscore Europe’s strategic focus on leveraging satellites for sustainable development and independent access to space. The UK market is projected to reach USD 0.33 billion by 2026, while the Germany market is projected to reach USD 0.28 billion by 2026.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 0.79 billion in 2025, accounting for 20.93% share, and is expected to reach USD 0.88 billion in 2026. Major economies such as China, India, and Japan are making significant investments in satellite technologies to expand telecommunication, broadband services, and others. Rapid urbanization and increasing demand for digital connectivity are fueling the deployment of GEO satellite for both commercial and government applications. Technological advancements and expanding national space programs, among other factors, propel the regional market. The Japan market is projected to reach USD 0.15 billion by 2026, the China market is projected to reach USD 0.28 billion by 2026, and the India market is projected to reach USD 0.23 billion by 2026.

Rest of the World

The Rest of the World market generated USD 0.66 billion in 2025, representing 17.33% of the global market landscape, and is expected to reach USD 0.72 billion in 2026. The rest of the world includes Latin America and the Middle East & Africa. These regions focus on increasing investment and research activities in telecommunication infrastructure. The Middle East & Africa region is increasing GEO satellites programs through partnerships with international satellite operators to gain competitive edge in the market. However, these regions face challenges such as limited local manufacturing and higher entry barriers, which can affect regional growth.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players Focus on Rapid Technological Innovation and Strategic Partnerships to Gain a Competitive Edge

Key market players are focused on strategic partnerships and entry of both established satellite operator’s companies and emerging tech driven players. Companies are heavily investing in research and development to advance satellite payload capacity, operational lifespan, and communication capabilities. There is also a strong focus on technologies such as high-throughput satellites (HTS), software defined payloads, electric propulsions, and artificial intelligence for autonomous operations. Strategic alliance and joint ventures are enabling companies to share expertise, reduce development costs, and accelerate new satellite solutions.

LIST OF KEY GEO SATELLITE COMPANIES PROFILED

- Airbus Defence and Space (Germany)

- SES (Luxembourg)

- Viasat Inc. (U.S.)

- Thales Group (France)

- Maxar Technologies Inc. (U.S.)

- Eutelsat Communication S.A. (France)

- Indian Space Research Organization (ISRO) (India)

- Inmarsat Plc. (U.K.)

- China Aerospace Science and Technology Corporation (China)

- Intelsat S.A. (U.S.)

- EchoStar Corporation (U.S.)

- National Aeronautics and Space Administration (NASA) (U.S.)

KEY INDUSTRY DEVELOPMENTS

- July 2025 – The U.S. government awarded Boeing a USD 2.8 billion deal to create and manufacture two geostationary orbit satellites. The U.S. president and combined strategic worldwide forces will receive space-based nuclear, command, control, and communications capabilities through the Evolved Strategic Satellite Communications (ESS) program.

- May 2025 – To identify threats and accelerate data delivery to military troops, the Space Systems Command (USSF SSC) of the U.S. Space Force is investigating the potential of renting commercial small and medium satellites capable of moving in Geosynchronous Orbit (GSO). By the following February, the Commercial Satellite Communications Office of the SSC may grant a 10-year Maneuverable Geosynchronous Orbit (M-GEO) Satellite-Based Services contract for between USD 895 million and USD 905 million.

- March 2025 – A private commercial client awarded Maxar Space Systems a deal for a high-power communications satellite for geostationary orbit (GEO). The satellite will be constructed at the company's California sites in Palo Alto and San Jose using the Maxar 1300 series platform. For the unidentified client, Maxar intends to create a satellite that will have a multi-spot beam payload.

- March 2025 – Thales Alenia Space (TAS) signed a significant agreement with SKY Perfect JSAT Corporation for building JSAT-32, a geostationary-earth-orbit (GEO) satellite.

- February 2025 – Japan's Ministry of Defense awarded Astroscale Japan Inc., a division of Astroscale Holdings Inc. ("Astroscale"), a contract worth USD 50 million (taxes included) to construct a prototype of a demonstration satellite with a responsive space system.

REPORT COVERAGE

The report outlines competitive dynamics by assessing market segmentations, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global market research analysis provides detailed insights into the market segmentation. Besides this, the report offers insights into the global market trends, Porter’s five forces analysis, supply chain trends, factors increasing the demand for GEO satellites, company profile, and highlights key space industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.87% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Propulsion

|

|

By Type

|

|

|

By Application

|

|

|

By End User

|

|

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the global market size was valued at USD 4.19 billion in 2026 and is anticipated to USD 7.13 billion by 2034.

The market is likely to grow at a CAGR of 6.87% during the forecast period.

The top industry players are Airbus Defence and Space (Germany), SES (Luxembourg), Vaisat Inc. (U.S.), Thales Group (France), Maxar Technologies Inc. (U.S.), and Eutelsat Communication S.A. (France), among others.

North America dominated the GEO satellite market with a market share of 32.23% in 2025.

Escalated global demand for high-capacity telecommunications broadcasting and broadband services is a key factor driving market growth.

High cost associated with the launch and maintenance of satellite constellations may restrict the expansion of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us