LEO Satellite Market Size, Share & Industry Analysis, By Type (Small, Medium, and Large), By Application (Communication, Earth Observation, Navigation, Scientific Research, and Others), By End User (Commercial and Military & Government), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

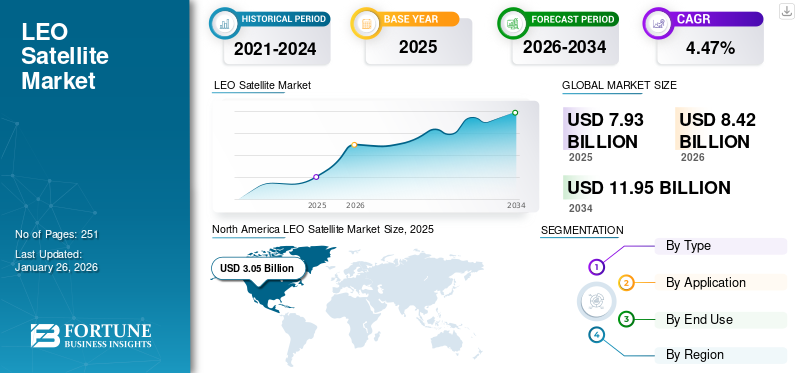

LEO SATELLITE MARKET SIZE & FUTURE OUTLOOK

The global LEO satellite market size was valued at USD 15.16 billion in 2025. The market is projected to grow from USD 17.26 billion in 2026 to USD 42.59 billion by 2034, exhibiting a CAGR of 12.0% during the forecast period. North America dominated the LEO satellite market with a market share of 38.25% in 2025.

Low Earth Orbit (LEO) satellite market covers satellites placed roughly up to 2,000 km above Earth for communications, Earth observation, navigation support, and other data services. It is used for broadband internet, remote sensing, maritime and aviation connectivity, disaster response, and defense surveillance, as LEO systems offer low latency and wider coverage. The main driver is rising demand for fast connectivity in remote and underserved areas, plus expanding non-terrestrial network services.

Key players include SpaceX, which deploys large broadband constellations, Airbus, which builds satellite platforms, and Iridium, Eutelsat, and Planet Labs PBC, which provide global communications and Earth-observation services.

Download Free sample to learn more about this report.

LEO Satellite Market Key Takeaways

- 2025 Market Size: USD 15.16 billion

- 2026 Market Size: USD 17.26 billion

- 2034 Forecast Market Size: USD 42.59 billion

- CAGR: 12.0% from 2026–2034

- North America dominated the market with a 38.25% share in 2025.

- Small segment held the largest market share in 2025.

- Communication segment held the largest market share in 2025.

North America

The market reached USD 5.80 billion in 2025, driven by investments in LEO satellite systems.

Asia Pacific

The market reached USD 4.83 billion in 2025, driven by expanding LEO constellations and launch capabilities.

Europe

The market reached USD 3.51 billion in 2025, supported by investments in LEO satellite infrastructure.

U.S.

The market is projected to reach USD 5.37 billion by 2026, driven by communication and security applications.

Japan

The market is projected to reach USD 1.21 billion by 2026, supported by investments in space infrastructure and communication services.

Read More

- 2025 Market Size: USD 1.82 billion

- 2026 Market Size: USD 2.35 billion

- 2034 Forecast Market Size: USD 18.40 billion

- CAGR: 29.33% from 2026–2034

- North America dominated the market with a 42.86% share, valued at USD 0.78 billion in 2025.

- Software/platforms segment held the largest market share in 2025.

- Care coordination & navigation segment held the largest market share in 2025.

North America

The market reached USD 0.78 billion in 2025, driven by strong EHR adoption and AI implementation.

Asia Pacific

The market is projected to reach USD 0.59 billion by 2026, supported by expanding digital healthcare infrastructure.

Europe

The market is projected to reach USD 0.58 billion by 2026, driven by digital health investments and integrated care adoption.

U.S.

The market is projected to reach USD 0.92 billion by 2026, supported by widespread AI adoption in healthcare.

Japan

The market is projected to reach USD 0.12 billion by 2026, driven by growing digital healthcare adoption.

Read More

LEO SATELLITE MARKET TRENDS

Implementation and Updating of LEO Networks to Software-Defined, Crosslinked and Standards-Based Infrastructure to be a Significant Market Trend

LEO networks are shifting from simple bent-pipe satellite capacity toward software-defined, crosslinked, and standards-based network infrastructure. The U.S. Space Development Agency’s planned a 300–500+ satellite LEO architecture providing assured, resilient, low-latency military data and connectivity globally.

SDA’s Optical Communications Terminal standard also defines interoperability specifications for optical space-to-space, space-to-air, space-to-maritime, and space-to-ground links, showing how crosslinks are becoming a formal network requirement rather than a premium add-on.

Airbus’ 2024 contract to build the first 100 satellites for Eutelsat OneWeb’s LEO constellation extension is intended to ensure service continuity and enhancement from late 2026, reinforcing the move toward upgraded, repeatable LEO network infrastructure.

3GPP’s non-terrestrial network framework brings satellites into cellular standards, including LEO/MEO satellite use cases, helping satellite networks connect more naturally with 5G/6G ecosystems. This trend supports higher interoperability, lower integration friction, better roaming potential, and more scalable satellite-to-device and mobility services.

Sources: SDA Transport Layer; Telesat Lightspeed; Airbus OneWeb extension; 3GPP NTN overview; NASA/Telesat CSP brochure.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rise in Satellite Deployment Scale and Launch Attempts to Drive Market Growth

The strongest growth driver for the LEO satellite market is deployment scale. Operators are no longer planning isolated spacecraft, they are building replenishable networks where launch cadence, batch manufacturing, terminal production, and ground-segment automation matter as much as satellite performance.

Furthermore, the market is being pulled by broadband constellations, direct-to-cell rollouts, defense transport layers, enterprise mobility, and sovereign connectivity programs. This changes the revenue logic as replacement cycles, continuous capacity upgrades, and constellation extensions create repeat demand for satellite based services, payloads, antennas, propulsion, software, gateways, and launch services.

Amazon’s first 27 Kuiper production satellites, Airbus’ 100-satellite OneWeb extension contract, Telesat’s 198-satellite Lightspeed program, and SDA’s 300–500 satellite transport-layer architecture all point in the same direction: LEO is becoming a scaled infrastructure market rather than a niche satellite market.

Furthermore, SpaceX's Starlink have over 10,300 satellites in orbit as of April 2026, with approvals for up to 42,000, while Amazon's Project Kuiper (now Leo) has launched 231 production satellites after multiple missions, targeting 3,236 total.

Telecom Standards and SCS Rules Make Satellite-To-Device Commercially Available which Drive Market Growth

Evolving telecom standards and Supplemental Coverage from Space (SCS) rules have unlocked commercial viability for satellite-to-device services, propelling LEO satellite market growth. These regulatory advancements allow standard smartphones to connect directly with LEO satellites without specialized hardware, seamlessly extending terrestrial networks into remote, rural, and disaster-prone areas where coverage gaps persist.

Furthermore, SCS frameworks, pioneered by the FCC, integrate satellite backhaul with cellular spectrum bands, enabling operators to offer unified "single network" experiences that blend 4G/5G with orbital connectivity. This standardization eliminates barriers to entry, permitting LEO providers to deliver low-latency voice, text, and data services as reliable fallbacks, enhancing network resilience for emergency response, IoT monitoring, and maritime applications.

MARKET RESTRAINTS

Orbital Congestion to Restrict Market Growth

Orbital congestion is the main structural restraint for the market. ESA estimates that roughly 40,000 objects are tracked by surveillance networks, about 11,000 of which are active payloads, while debris objects larger than 1 cm are estimated above 1.2 million.

It also affects constellation economics through extra maneuver planning, fuel reserves, conjunction screening, and deorbit planning, insurance scrutiny, launch licensing and end-of-life compliance. As LEO fills with commercial constellations, operators may face tighter rules on disposal reliability, brightness, spectrum coordination, and collision avoidance.

These requirements raise satellite design complexity and operating cost, especially for smaller companies trying to deploy large constellations. Regulators are also tightening rules as the FCC now requires LEO satellite operators to dispose of satellites within five years after mission completion, replacing the older 25-year guideline.

MARKET OPPORTUNITIES

Direct-to-Device, IoT and Mobility Services Expand Market Opportunity

Direct-to-device, IoT and mobility services create a practical expansion path for the global market. D2D can convert mobile dead zones into a satellite service opportunity; IoT connects sensors, assets and machines outside terrestrial coverage; and mobility supports maritime, aviation, rail, defense, emergency response, energy and mining users.

The opportunity is attractive as these customers do not all need the same service. Some need text and emergency messaging, some need narrowband machine data, and others need high-throughput broadband on moving platforms. That segmentation lets LEO operators monetize different payload classes instead of chasing one broadband model.

Supporting evidence is visible in T-Mobile/Starlink’s dead-zone beta, AST SpaceMobile’s BlueBird launches, Iridium’s standards-based NB-IoT NTN strategy and Sateliot’s EIB-backed IoT constellation rollout.

Furthermore, in 2024, the FCC adopted the world’s first Supplemental Coverage from Space framework, creating a formal path for satellite operators and wireless carriers to extend mobile coverage into areas without terrestrial service. This makes satellite-to-smartphone connectivity more commercially practical, especially for emergency messaging, remote sensing coverage, and rural/mobile dead zones.

MARKET CHALLENGES

Limited Gateway Locations Create Market Challenge

Limited gateway locations create market challenge for operators as gateways must be positioned where they have reliable fiber backhaul, favorable weather, and regulatory approval. When gateway sites are scarce, network capacity becomes concentrated in a few places, which can create congestion, raise latency, and reduce service quality in remote or high-demand regions. It also increases deployment costs as operators need more site acquisition, interconnection, and coordination work to expand coverage.

SEGMENTATION ANALYSIS

By Type

Small Segment Captured Largest Market Share Due to its Cost Effectiveness and Agility

On the basis of type, the market is classified into small, medium, and large.

The small segment held the largest LEO satellite market share, driven by the cost-effectiveness, rapid development, agility, and reduced launch complexity. Smaller satellites often benefit from advancements in miniaturization and the use of commercial off-the-shelf components, enabling the integration of cutting-edge satellite technologies in a more affordable and compact form. Satellite mass plays a crucial role in the market, as the majority of operational satellites weigh between 100 to 500 kg, significantly influencing launch costs and design considerations.

The large segment is anticipated to rise with a CAGR of 8.3% over the forecast period.

By Application

Communication Segment Secured Largest Share Due to Rise in Demand for High Speed Connectivity

On the basis of application, the market is classified into communication, earth observation, navigation, scientific research, and others.

The communication segment held the largest market share owing to the growing demand for mobile communication and the increasing need for high speed internet connectivity for information sharing. Communication satellite enable global telecommunications systems by relaying voice, video, and data signals to and from one or many locations. Various companies are developing and deploying communication satellite, which is expected to further drive the growth of the segment. For instance, in August 2024, SpaceX successfully launched ASBM-1 and ASBM-2 Falcon 9 rocket for the Arctic Satellite Broadband Mission (ASBM). The satellites are designed to provide both military satellite communications broadband connectivity in the northern polar region. Low earth orbit satellites are strategically positioned to provide low-latency communication services.

The earth observation segment is anticipated to rise with a high CAGR of 12.9% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Commercial Segment Held Largest Share Due to Expansion in Satellite Usage and Application in Various Industries

On the basis of end user, the market is classified into commercial and government & military.

The commercial segment captured the largest share in the market due to expansion of satellite applications in areas such as weather forecasting, forest monitoring, earth observation, IoT connectivity, and others. Moreover, companies such as SpaceX, OneWeb, Amazon's Project Kuiper and Telesat are increasingly investing in commercial LEO satellite deployment.

The government and military segment is anticipated to rise with a CAGR of 11.7% over the forecast period.

LEO SATELLITE MARKET REGIONAL OUTLOOK

The global market is segmented on the basis of region into North America, Europe, Asia Pacific, and Rest of the World.

North America

North America LEO Satellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 4.94 billion, and also maintained the leading share in 2025, with USD 5.80 billion. The growth is driven by huge investments in LEO satellite systems to enhance national security, border surveillance, and missile tracking capabilities.

For example, in July 2024, Amazon announced that it had expedited the production and testing of small satellites for its Project Kuiper constellation at its factory in Kirkland, Washington state, with more than 3,000 satellites set to be manufactured at the 16,000 m2 facility over several years.

U.S. LEO Satellite Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 5.37 billion in 2026, accounting for roughly 11.9% CAGR over the forecast period. Vertical integration across manufacturing, launch, and operations strengthens competitive positioning. Demand is concentrated in communication and security applications. Government contracts and private sector investments provide stable revenue streams, supporting continued expansion and technological leadership within the market.

Asia Pacific

In 2025, Asia Pacific generated USD 4.83 billion, contributing a CAGR of 12.6% during the forecast period, and is projected to grow to USD 5.53 billion in 2026. The growth is driven by technological advancement in spaceflight technology and exploration. The expansion of LEO constellations and the rise in the affordable satellite and rocket launches are expected to benefit the region’s market. The region is also witnessing continuous progress in the development of launch technology which is useful for space technologies and services market. For instance, in August 2024, China announced plans to launch first batch of LEO satellites for its mega constellation under the National Reconnaissance Office (NRO). The company signed a contract worth USD 1.8 billion with the agency in 2021 for the development and launch of satellites. The China Aerospace Science and Technology Corporation (CASC) is a key player in the market, contributing to advancements in satellite technology and infrastructure development for global connectivity.

Japan LEO Satellite Market

Japan’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.21 billion. Japan’s market is driven by advanced technological capabilities and increasing investment in space infrastructure. Demand is focused on communication and earth observation applications. Collaboration between government agencies and private companies supports innovation. The country emphasizes high-performance systems and reliability, contributing to steady growth and maintaining its position as a key participant in the market.

China LEO Satellite Market

China’s market is projected to be one of the largest in Asia Pacific, with 2026 revenues estimated at around USD 1.65 billion. China is emerging as a major player, supported by strong government backing and the rapid expansion of satellite constellations. Domestic manufacturing capabilities enable large-scale deployment at competitive costs. Demand spans communication, surveillance, and navigation applications. The country’s strategic focus on space technology development supports increasing market share and positions it as a key contributor to global market growth.

Europe

Europe maintained a strong presence in the global market, reaching USD 3.51 billion in 2025, accounting for 12.0% CAGR during the study period, and is expected to reach USD 4.00 billion in 2026. Europe is anticipated to witness notable growth throughout the forecast period, attributed to the rise in deployment of LEO constellations aimed at improving satellite internet quality and expanding services. The LEO industry is poised to grow significantly as many organizations are already investing heavily in LEO technology and applications. Such developments highlight that the industry is actively developing this robust and emerging technology that will contribute to true global connectivity. For instance, in 2023, the European Parliament approved USD 2.6 billion in financing for the new IRIS2 constellation. This decision highlights the growing importance and potential of LEO satellite technology in global communications and connectivity.

Germany LEO Satellite Market

Germany’s market is projected to be one of the growing region in Europe, with 2026 market size estimated at around USD 1.56 billion. Germany plays a significant role in the European market through strong engineering capabilities and industrial participation. Demand is linked to earth observation and communication projects supported by public and private investment. The country’s focus on precision engineering and innovation supports system development. Its contribution remains steady, driven by involvement in regional space initiatives and technology advancement.

U.K.LEO Satellite Market

The U.K. market is projected to be one of the largest in Europe, with 2026 market size estimated at around USD 0.88 billion. The United Kingdom market is supported by expanding space sector initiatives and investment in satellite communication infrastructure. Demand is driven by both commercial operators and government programs focused on connectivity and defense. The country’s regulatory environment encourages innovation and private participation. Continued investment in space technologies supports steady growth and strengthens its position within the broader European market.

Rest of the World

The rest of the world include Middle East & Africa and Latin America. Latin America presents emerging opportunities within the market, driven by connectivity gaps and limited terrestrial infrastructure. The Middle East & Africa market is driven by demand for connectivity and strategic investments in communication infrastructure.

Middle East & Africa LEO Satellite Market

The market is set to reach a valuation of 0.70 billion in 2026.

Latin America LEO Satellite Market

The market is set to reach a valuation of USD 0.44 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Development of Technologically Advanced Products and Acquisition Strategies to Drive Growth

Prominent market players are prioritizing the advancement of their product offerings. The development of a diverse range of solutions and heightened investment in research and development are key factors contributing to the market dominance of these players. Within the industry, major players are embracing both organic and inorganic growth strategies, including mergers and acquisitions and introducing new products, to sustain their competitive edge. Key players are also investing heavily in building large satellite networks to provide global connectivity.

LIST OF KEY LEO SATELLITE COMPANIES PROFILED IN REPORT

- SpaceX (U.S.)

- Airbus SE (Netherlands)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Space Systems (U.S.)

- York Space Systems (U.S.)

- MDA Space (Canada)

- Rocket Lab Space Systems (U.S.)

- Millennium Space Systems, Inc. (U.S.)

- com, Inc. (U.S.)

- Eutelsat (France)

- Iridium Communications Inc. (U.S.)

- Globalstar Inc. (U.S.)

- Planet Labs PBC (U.S.)

- Spire Global, Inc. (U.S.)

- Satrec Initiative Co., Ltd. (South Korea)

- Nara Space Technology Inc. (South Korea)

- Korea Aerospace Industries (South Korea)

- TelePIX Co., Ltd. (South Korea)

- Hanwha Systems Co., Ltd. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2026: York acquired Orbion Space Technology, bringing flight-proven electric propulsion capability into its broader spacecraft supply chain. The acquisition strengthens York’s supply chain by bringing electric propulsion capability closer to its satellite manufacturing base.

- January 2026: Eutelsat has given Airbus Defence and Space a contract to construct an additional 340 OneWeb low Earth orbit (LEO) satellites. Eutelsat has ordered 440 spacecraft in total, including the 100 satellites from the previous batch that were acquired in December 2024. The OneWeb constellation will continue to function thanks to these new satellites.

- August 2025: 21 communications satellites have been delivered to the Space Development Agency (SDA), according to York Space Systems. By instantly connecting sensors to shooters, these will be the first non-prototype Space Development Agency (SDA) birds to support military satellite

- April 2025: Millennium completed the FOO Fighter Critical Design Review in just 10 months after authorization to proceed. The speed of the design cycle highlighted the maturity of its smallsat architecture and its ability to support rapid fielding schedules for LEO constellation programs.

- March 2025: Rocket Lab completed the final launch for the Kinéis IoT constellation deployment campaign, placing 25 satellites into orbit in less than a year. Although this is a launch program, it demonstrates LEO constellation deployment credibility.

REPORT COVERAGE

The LEO satellite market report provides a detailed analysis of the sector, focusing on important aspects such as key players, type, application, and end-user, segments depending on various regions. Moreover, the research report offers deep insights into the market trends, competitive landscape, market competition, and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the growth of the global market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 12.0% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 15.16 billion in 2025 and is projected to reach USD 42.59 billion by 2034.

Registering a CAGR of 12.0%, the market will exhibit significant growth over the forecast period.

By type, the small segment led the market due to its advantages such as cost efficiency, agility, and compactness.

North America held the highest share of the market.

Rise in satellite deployment scale and launch attempts to drive market growth.

SpaceX (U.S.), Airbus SE (Netherlands), Eutelsat (France), Planet Labs PBC (U.S.) are key players in the global market.

Direct-to-device, IOT and mobility services to expand market opportunities.

- 2021-2034

- 2025

- 2021-2024

- 270

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us