Glass Mat Market Size, Share & Industry Analysis, By Mat Type (Chopped Strand Mat and Continuous Filament Mat), By End-Use (Construction, Industrial, Automotive, Marine, and Others), and Regional Forecast, 2026-2034

Glass Mat Market Size and Future Outlook

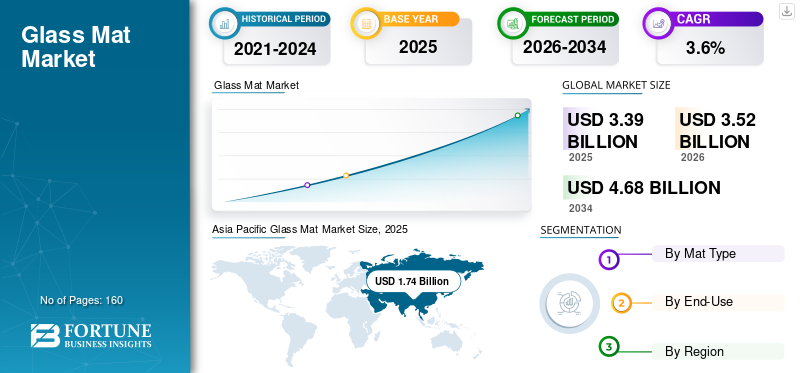

The global glass mat market size was valued at USD 3.39 billion in 2025. The market is projected to grow from USD 3.52 billion in 2026 to USD 4.68 billion by 2034, exhibiting a CAGR of 3.6% during the forecast period. Asia Pacific dominated the glass mat market with a market share of 51.33% in 1.74.

Glass mat refers to nonwoven fiberglass reinforcement supplied in roll or sheet form and used to provide isotropic strength, dimensional stability, and crack control in composite laminates. In this study, the scope includes Chopped Strand Mat (CSM) and Continuous Filament Mat (CFM) used with thermoset resins (polyester, vinyl ester, and epoxy) and selected thermoplastic composite systems across construction, industrial FRP, automotive components, and marine structures.

The market growth is driven by sustained demand for corrosion-resistant, lightweight composite solutions in construction and industrial applications, the expansion of FRP pipes, tanks, panels, and gratings, and the ongoing substitution of metal in selected transportation components. Suppliers are differentiating through mats engineered for faster wet-out and improved binder compatibility, and through formats that support higher-throughput closed-molding processes, while maintaining mechanical consistency for quality-critical end uses.

Furthermore, the market comprises several major players, including Owens Corning, Johns Manville, Jushi Group, Nippon Electric Glass Co., Ltd., and Saint-Gobain. Competitive positioning is shaped by fiber quality consistency, binder and sizing performance, global supply reliability, and the ability to support large composite processors and EPC-driven projects.

Download Free sample to learn more about this report.

Glass Mat Market Key Takeaways

- 2025 Market Size: USD 3.39 billion

- 2026 Market Size: USD 3.52 billion

- 2034 Forecast Market Size: USD 4.68 billion

- CAGR: 3.6% from 2026–2034

- Asia Pacific dominated the glass mat market with a 51.33% share in 2025.

- Chopped strand mat segment held the largest market share in 2025.

- Construction segment accounted for 33.4% of the market in 2025.

Asia Pacific

Asia Pacific led the market with USD 1.74 billion in 2025.

Europe

Europe is projected to reach USD 0.83 billion by 2026.

North America

North America is projected to reach USD 0.62 billion by 2026.

U.S

The market reached USD 0.50 billion in 2025.

Japan

Demand is supported by established composites supply chains and industrial manufacturing.

Read More

GLASS MAT MARKET TRENDS

Higher Closed-Molding Adoption and Infrastructure Durability Upgrades are Significant Market Trends

Glass mat market growth continues to rise as composite processors prioritize productivity, repeatability, and durability in large-area laminates and complex FRP parts. Across regions, there is a steady shift toward faster, cleaner manufacturing routes (including infusion, RTM, compression molding, and pultrusion-enabled systems), which is driving greater interest in continuous filament mats and mat formats engineered for rapid wet-out and stable fiber distribution. In parallel, infrastructure operators are favoring corrosion-resistant FRP solutions for harsh environments, which sustains demand for mats in pipe, tank, and panel laminates. Binder and sizing innovation is also accelerating as end users seek improved compatibility with lower-styrene and higher-performance resin systems.

- For instance, suppliers are expanding product families of chopped strand and continuous filament mats with binder systems designed to improve handling, wet-out speed, and laminate quality for both open-mold and closed-mold processing.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

FRP Adoption in Construction and Industrial Assets Drives Market Growth

Glass mat is a non-discretionary reinforcement for many FRP laminates used in panels, gratings, pipes, and tanks where durability, crack control, and corrosion resistance are critical. As construction and industrial operators invest in longer-life materials for aggressive environments, mats support higher volumes of composite fabrication, particularly in hand lay-up and spray-up laminates, as well as in mechanized production lines. In industrial applications, the growth of chemical processing, water and wastewater infrastructure, and utility projects is supporting steady demand for FRP systems where mats deliver isotropic reinforcement and reliable resin distribution.

- For instance, large FRP pipe and tank projects typically specify mat layers for corrosion barriers and structural laminates, increasing mat usage with larger installed surface areas.

MARKET RESTRAINTS

Pricing Volatility, Processing Sensitivity, and Qualification Requirements Can Limit Adoption

Glass mat value is sensitive to glass fiber energy costs and the supply-demand balance, leading to pricing volatility for processors. Performance also depends on resin compatibility, wet-out behavior, and process control; poor handling or inadequate resin impregnation can increase scrap and constrain switching between suppliers. In higher-spec applications, qualification requirements for laminate properties, consistency, and long-term durability can slow substitution and lengthen approval cycles, particularly for critical industrial and transportation parts.

MARKET OPPORTUNITIES

Infrastructure Rehabilitation and Lightweighting in Transportation Create Growth Opportunities

Opportunities are rising as infrastructure owners increasingly adopt FRP solutions for rehabilitation and corrosion mitigation, including bridge and utility-related composites, modular panels, and chemical-resistant structures. Transportation programs that prioritize lightweighting and durability can lift demand for mats in semi-structural components and interior applications. In addition, the expansion of closed-mold processes and automated composite manufacturing supports higher-value mat formats optimized for rapid wet-out, dimensional stability, and consistent laminate thickness.

MARKET CHALLENGES

End-Market Cyclicality and Substitution Risk Across Reinforcement Formats May Affect Growth

Demand is linked to construction, industrial capex, and transportation production cycles, which can create variability in volumes. Customers can also switch between reinforcement formats (e.g., rovings, stitched fabrics, or mat-heavy laminates) depending on mechanical targets and total installed cost. Finally, evolving environmental and workplace rules regarding emissions and handling can require changes to resin systems, binders, and processing practices, creating qualification and change-management burdens for both suppliers and processors.

Segmentation Analysis

By Mat Type

Wide Use in Open-Mold Processing Led to Chopped Strand Mat Segmental Dominance

Based on mat type, the market is segmented into chopped strand mat and continuous filament mat.

The chopped strand mat segment accounted for the largest glass mat market share in 2025. The segment is driven by its wide use in open-mold processing and general-purpose laminates for construction, industrial FRP, and marine components, where isotropic reinforcement and cost-effective layer build-up are valued.

The continuous filament mat segment growth is supported by increasing adoption of closed molding, productivity targets, and demand for a more uniform mat structure in repeatable manufacturing environments. The continuous filament mat segment is projected to grow at a 3.5% CAGR during the study period.

By End-Use

To know how our report can help streamline your business, Speak to Analyst

Construction Segment Dominated Market Due to Extensive Use of Product

By end-use, the market is categorized into construction, industrial, automotive, marine, and others.

The construction segment accounted for the largest share in 2025, driven by the use of FRP panels, roofing and cladding components, gratings, and other composite building products that require mat layers for laminate thickness and durability. Furthermore, the segment held a 33.4% share in 2025.

The industrial segment is also expected to grow favorably over the projected period. The segment's growth is supported by FRP pipes, tanks, ducts, and corrosion-resistant equipment in chemical processing, water and wastewater, and utilities along with reliability-driven replacement cycles and incremental capex upgrades. The segment is expected to grow at a CAGR of 3.5% over the forecast period.

Glass Mat Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Glass Mat Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant share in 2025, valued at USD 1.74 billion, and is expected to maintain its leading share in 2026, valuing at USD 1.81 billion. The region’s growth is supported by large-scale manufacturing activity, broad construction and infrastructure needs, and a sizeable installed base of FRP fabrication for industrial and consumer applications. China remains the largest consumer, while India, Japan, and South Korea contribute through established composites supply chains and expanding industrial and transportation manufacturing.

China Glass Mat Market

In 2025, the China market reached USD 0.69 billion. High volumes of construction-linked composites, industrial FRP fabrication, and domestic supply capacity support steady demand for both CSM and CFM.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is also a significant contributor to the market, with the market estimated to reach USD 0.62 billion by 2026. The region benefits from an established composites processing base across construction, industrial FRP, and marine applications, alongside demand for higher-throughput manufacturing in selected automotive components.

U.S. Glass Mat Market

In 2025, the U.S. market reached USD 0.50 billion. In the U.S., the demand is supported by industrial FRP fabrication, construction composites, and ongoing replacement and retrofit cycles for corrosion-prone assets.

Europe

Europe is expected to experience significant growth in the coming years. During the forecast period, the European region is projected to grow at CAGR of 3.6% and reach a valuation of USD 0.83 billion in 2026. The region's growth is driven by higher-spec composite components, industrial clusters that require corrosion resistance, and a greater share of process-controlled manufacturing, which lifts demand for uniform mat formats.

U.K. Glass Mat Market

The U.K. market in 2025 reached USD 0.08 billion, representing approximately 2.9% of global market revenue.

Germany Glass Mat Market

Germany’s market reached USD 0.14 billion in 2025, equivalent to around 3.9% of global sales.

Latin America

Latin America is experiencing steady growth and is expected to reach a valuation of USD 0.29 billion in 2026. The demand in the region is linked to construction activity, industrial FRP needs, and selective marine fabrication.

Brazil Glass Mat Market

Brazil’s market reached approximately USD 0.10 billion in 2025, equivalent to around 2.6% of global sales.

Middle East & Africa

The Middle East & Africa region is gradually expanding, with sales valued at around USD 0.07 billion in 2025. GCC countries account for a notable share of regional demand, driven by industrial projects, utilities infrastructure, and imported composite solutions in corrosive environments.

GCC Glass Mat Market

GCC reached USD 0.03 billion in 2025, accounting for approximately 2.0% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players are Adopting Capacity, Portfolio, and Service-Led Strategies to Maintain their Positions in Market

Competition is shaped by fiber quality consistency, binder performance, resin compatibility, conversion efficiency at the processor, global supply availability, and the ability to support qualification requirements for demanding applications. Large glass fiber producers and reinforcement specialists compete through product breadth (CSM and CFM variants), technical support to optimize wet-out and laminate performance, and reliable delivery to large composite processors and distributors. Some of the key market players include Owens Corning, Johns Manville, Jushi Group, Nippon Electric Glass Co., Ltd., and Saint-Gobain. Key competitive differentiators include consistent quality, technical support for system detailing, and reliable project supply across multiple regions.

LIST OF KEY GLASS MAT COMPANIES PROFILED IN REPORT

- Owens Corning (U.S.)

- Johns Manville (U.S.)

- Jushi Group (China)

- Taishan Fiberglass (China)

- Nippon Electric Glass (Japan)

- Nittobo (Japan)

- Ahlstrom (Finland)

- Saint-Gobain (France)

- 3B - the fibreglass company (Belgium)

- GYPSEMNA CO LLC. (UAE)

REPORT COVERAGE

The global glass mat market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also includes a detailed competitive landscape, providing market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 3.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Mat Type, End-Use, and Region |

| By Mat Type |

|

| By End-Use |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights estimates that the global market size was USD 3.39 billion in 2025 and is projected to reach USD 4.68 billion by 2034.

Recording a CAGR of 3.6%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The construction end-use segment led in 2025.

Asia Pacific held the highest market share in 2025.

Owens Corning, Johns Manville, Jushi Group, Nippon Electric Glass Co., Ltd., and Saint-Gobain are some of the top players in the market.

The rising use of FRP/composite structures in construction and industrial equipment, where glass mats deliver corrosion resistance, durability, and cost-effective reinforcement at scale, drives the market growth.

The factors expected to favor product adoption are lower lifecycle costs vs. metals, compatibility with high-throughput molding processes, and increasing demand for lightweight, corrosion-resistant materials in construction, industrial, marine, and selected automotive applications.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us