Healthcare BPO Market Size, Share & Industry Analysis, By Product (Healthcare Payers {Claims Administration, Data Management, Medical Billing, and Others} and Healthcare Providers {Patient Access, Care Management, Revenue Cycle Management (RCM), and Others}), By Application (Medical Coding & Documentation, Billing & Enrollment, Healthcare Network Management, Fraud & Risk Management, Claims Management, Risk & Compliance, Audit Services, Payment Integrity, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

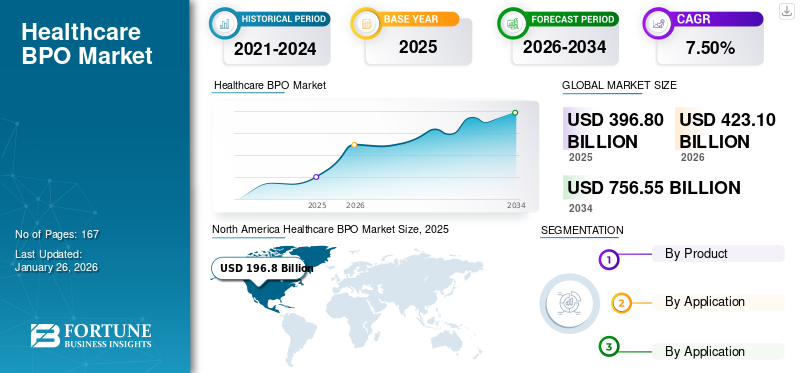

The global healthcare BPO market size was valued at USD 396.80 billion in 2025 and is projected to grow from USD 423.1 billion in 2026 to USD 756.55 billion by 2034, exhibiting a CAGR of 7.50% during the forecast period. North America dominated the healthcare BPO market with a market share of 49.60% in 2025.

The healthcare BPO market is expanding rapidly as providers, payers, and life sciences companies face rising operational and regulatory complexities. Increasing administrative costs, driven by billing, coding, claims management, and compliance with evolving laws such as HIPAA and GDPR, are pushing organizations to seek cost-efficient outsourcing solutions. Outsourcing enables hospitals and insurers to focus on patient care and core functions while delegating repetitive back-office tasks. The digital transformation of healthcare with EHR/EMR adoption, telehealth growth, and AI integration has further accelerated the demand for specialized outsourcing partners. At the same time, rising claim denials, payment integrity challenges, and fraud risks require advanced analytics and dedicated vendor expertise. Life sciences companies are also outsourcing pharmacovigilance, regulatory submissions, and clinical data management to meet stringent FDA and EMA requirements. Growing pressure to optimize revenue cycles, improve member engagement, and enhance care management creates sustained demand for BPO services.

The market encompasses several major players with NTT DATA, Inc., MDI NetworX LLC., and Invensis Technologies Pvt Ltd at the leading position. Technology integration, advancement in AI and ML strengthen the position of these companies due to innovative services.

Download Free sample to learn more about this report.

Healthcare BPO Market Key Takeaways

- 2025 Market Size: USD 396.80 billion

- 2026 Market Size: USD 423.10 billion

- 2034 Forecast Market Size: USD 756.55 billion

- CAGR: 7.50% from 2026–2034

- North America dominated the healthcare BPO market with a 49.60% share in 2025.

- The healthcare providers segment is projected to hold a 59.99% share in 2026.

- The claims management segment is projected to account for a 19.87% share in 2026.

North America

North America generated USD 196.80 billion in 2025 and is projected to reach USD 210.26 billion in 2026.

Asia Pacific

Asia Pacific represented 18.20% of global revenue in 2025 and is expected to reach USD 78.28 billion in 2026.

Europe

Europe accounted for 23.90% of the global market in 2025, reaching USD 94.71 billion.

U.S.

The market is projected to reach USD 197.10 billion in 2026, driven by rising administrative costs and increasing healthcare claim denials across hospitals.

Japan

The healthcare BPO market is projected to reach USD 23.86 billion in 2026, supported by growing healthcare digitalization and outsourcing adoption.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Administrative Burden Heighten Demand for BPO Services Propelling Market Growth

The rising administrative complexity due to frequent updates in coding standards, stricter reimbursement policies, and growing compliance requirements heighten the demand for outsourcing business services. This results in diverting attention of healthcare providers away from patient care and strategic priorities. To overcome these challenges many organizations increasingly rely on outsourcing partners to manage functions such as billing, claims adjudication, coding, and payment integrity more efficiently. Consequently, the cost effectiveness along with the mounting administrative workload is acting as a strong catalyst for the healthcare BPO market growth.

- In 2025, the American Hospital Association, reported that between 2022 and 2023, care denials increased to an average of 20.2% and 55.7% for commercial and Medicare Advantage (MA) claims, respectively. To facilitate such large scale operations, the demand for the global market is increasing.

MARKET RESTRAINTS

Data Privacy & Security Concerns Restrict Market Expansion Despite Cost Advantages

Healthcare BPO involves large-scale handling of protected health information (PHI), insurance claims data, and sensitive patient identifiers, which makes the sector highly vulnerable to cybersecurity threats. Breaches not only expose financial and medical records but also lead to regulatory penalties, reputational damage, and erosion of trust in outsourcing vendors. Such factors may raise concerns about offshoring critical processes, slowing outsourcing adoption despite the cost advantages. As a result, persistent concerns over data security remain a key restraint to the healthcare BPO market share.

- In August 2025, the HHS Office for Civil Rights data shows 58 healthcare breaches affecting 500+ individuals; over 3.7 million individuals had their protected health information exposed in those incidents.

MARKET OPPORTUNITIES

Adoption of AI to Optimize Business Operations will Create Growth Opportunities

The integration of artificial intelligence into various facets of the business operations such as automation into revenue cycle management (RCM) and medical coding is creating significant potential for the market. Rising claim denials, delayed reimbursements, and complex coding requirements that demand faster and more accurate processing create the need for efficient practices to resolve these challenges. By outsourcing to vendors equipped with AI-powered platforms, healthcare organizations drastically reduce turnaround times and error rates.

- For instance, in April 2025, RamSoft Inc., partnered with Maverick Medical AI, an innovative provider of artificial intelligence for revenue cycle optimization. This strategic collaboration integrated Maverick Medical AI's CodePilot directly into company platforms such as PowerServer and OmegaAI RIS/PACS, enabling radiology practices to streamline workflows and improve billing accuracy.

MARKET CHALLENGES

High Transition and Integration Costs Creates Obstacles for Market Development

One of the major challenges in the healthcare BPO market is the high cost and complexity of transitioning critical functions such as medical coding, revenue cycle management (RCM), and claims processing to outsourcing partners. Integrating a BPO vendor’s systems with existing hospital or payer IT infrastructure often demands significant upfront investment, including technology upgrades, data migration, and process reconfiguration. Beyond the financial burden, providers and payers face operational challenges such as staff retraining, workflow redesign, and maintaining service continuity during the transition period. These integration hurdles can delay outsourcing decisions, particularly among mid-sized hospitals and insurers with limited budgets.

HEALTHCARE BPO MARKET TRENDS

Shift Toward Value-Based and Outcome-Driven Outsourcing Models is a Prominent Market Trend

The global healthcare BPO market is witnessing a shift to value-based outsourcing, where vendors are measured on outcomes such as reduction in claim denials, improvement in coding accuracy, faster turnaround times, or enhanced patient/member satisfaction. Payers and providers are increasingly demanding performance linked contracts with KPI’s measurable in performance rather than hours worked. As a result, BPO vendors are investing in analytics, AI, and process redesign to demonstrate measurable impact beyond cost savings, making outcome-driven models a strong differentiating trend in the market.

- In February 2024, Allina Health, transitioned 2,000 IT and revenue cycle (RCM) employees to Optum, in order to leverage advanced technologies and processes across its billing and revenue operations. The development aims to streamline the billing experience by implementing industry-leading technologies and processes across revenue cycle operations.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product

Healthcare Providers Lead Owing to Strong Utilization of Healthcare BPO Services

On the basis of product, the market is classified into healthcare payers and healthcare providers.

To know how our report can help streamline your business, Speak to Analyst

The healthcare providers segment is projected to dominate the market with a share of 59.99% in 2026. The healthcare providers segment is further classified into patient access, care management, revenue cycle management (RCM), and others. Healthcare providers are extensively adopting these services to reduce their costs, improve efficiencies by offloading their administrative functions, and work toward better treatment outcomes for the patients by focusing on clinical work.

- In September 2025, Benefis Health System announced that it had selected Ensemble Health Partners as their strategic partner to manage the organization’s end-to-end revenue cycle operations across its hospitals and clinics.

The healthcare payers segment is expected to grow at a CAGR of 6.69% over the forecast period.

By Application

Robust Demand for Efficient Claims Management Mechanisms to Lead to Segment’s Leading Market Share

In terms of application, the market is categorized into medical coding & documentation, billing & enrollment, healthcare network management, fraud & risk management, claims management, risk & compliance, audit services, payment integrity, and others.

The claims management segment is projected to dominate the market with a share of 19.87%% in 2026. The surge in healthcare claim volumes, combined with rising denial rates and increasingly complex reimbursement policies, is pushing payers and providers to outsource claims processing for improved efficiency and greater accuracy.

- For instance, in July 2025, Ensemble Health Partners announced that Methodist Le Bonheur Healthcare (MLH) has appointed the provider as their strategic revenue cycle management partner.

The risk & compliance segment is expected to grow at a CAGR of 8.10% over the forecast period.

Healthcare BPO Market Regional Outlook

On the basis of regions, the global market is divided into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Healthcare BPO Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

In 2025, the North America market stood at USD 196.8 billion, representing 49.60% of global demand, and is projected to grow to USD 210.26 billion in 2026. The region is anticipated to dominate and grow with a significant CAGR due to the region’s highly complex reimbursement structures, rising claim denials, and heavy regulatory compliance requirements. Outsourcing offers providers and payers cost savings while ensuring accuracy and adherence to HIPAA and other local laws. In 2026, the U.S. market is estimated to reach USD 197.1 billion. The growth in the country can be reiterated due to escalating administrative costs in U.S. hospitals.

- In 2025, American Hospital Association reported that U.S. hospitals witnessed an increase in the number of claim denials with over 20.2% in commercial claims and 55.7% in Medicare Advantage claims in the period of 2022–23.

Europe

The Europe region captured 23.90% of the global market in 2025, generating USD 94.71 billion in revenue, and is projected to reach USD 99.95 billion in 2026. This is primarily due to increasing adoption of digital health and telemedicine platforms that require back-office and claims support. Owing to these parameters, key countries present in the region such as the U.K. are projected to reach a valuation of USD 20.2 billion, Germany to record USD 23.4 billion in 2026 and France to record USD 15.82 billion in 2025.

Asia Pacific

Asia Pacific maintained a strong presence in the global market, reaching USD 72.35 billion in 2025, accounting for 18.20% share, and is expected to reach USD 78.28 billion in 2026. In terms of Asia Pacific, the Japan market is projected to reach USD 23.86 billion by 2026, the China market is projected to reach USD 22.83 billion by 2026, and the India market is projected to reach USD 15.32 billion by 2026.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa would witness a moderate growth. In 2025, Latin America represented USD 18.1 billion, accounting for 4.60% of the worldwide market, and is projected to grow to USD 19.01 billion in 2026. Rising investments in healthcare IT infrastructure and multilingual service capabilities further drive growth in these regions. In Middle East & Africa, GCC is set to attain the value of USD 7.22 billion in 2025. The Middle East & Africa market accounted for USD 14.84 billion in 2025, representing 3.70% of the global industry, and is expected to reach USD 15.59 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Presence of Varied Healthcare BPO Services Offerings Boost Market Presence of Key Companies

The global healthcare BPO market reflects a fragmented structure with several large, mid-sized, and small-sized companies operating in the market. These players are actively engaged in product and services innovation, strategic partnerships, and geographic expansion. They actively invest in technology advancement and offer a wide array of BPO services at one stop.

NTT DATA, Inc., MDI NetworX LLC. And Invensis Technologies Pvt Ltd. are major players in the market. A comprehensive range of healthcare BPO services to enable efficient operations and collaborations with other operating entities in the market are a few characteristics of these players that support their dominance.

Apart from this, other prominent players in the market include Accenture, Optum, Inc., Knack RCM, and others. These companies are undertaking various strategic initiatives, such as investments in R&D to enhance their market presence.

LIST OF KEY HEALTHCARE BPO COMPANIES PROFILED

- NTT DATA, Inc. (Japan)

- MDI NetworX LLC. (U.S.)

- Invensis Technologies Pvt Ltd (India)

- Accenture (Ireland)

- Optum, Inc. (U.S.)

- Knack RCM (U.S.)

- Genpact (U.S.)

- Cognizant (U.S.)

- TATA Consultancy Services Limited (India)

KEY INDUSTRY DEVELOPMENTS

- February 2025: TruBridge, Inc. selected Cibolo Health, as a preferred partner for financial optimization of independent rural hospitals and medical practices. The company extends its revenue cycle management (RCM) technology and services to members of the rural clinically integrated networks (CINs).

- October 2024: NTT DATA collaborated with Duke Health to create a highly interactive and technologically advanced model for augmented home care delivery. The solution enabled medical staff to be in direct contact with the patient while allowing patients to receive more of their care at home.

- September 2024: EQT AB. Acquired GeBBS, a global provider of healthcare outsourcing solutions. The development aimed to benefit from strong relationships with a diverse range of customers across US-based hospitals, physician groups, and other healthcare firms.

- January 2023: Rhino Health collaborated with NTT DATA to provide clinical researchers and AI developers with access to healthcare data at scale. The collaboration leveraged NTT DATA's Advocate AI imaging software, healthcare delivery, and consulting services, performing with Rhino Health's scalable distributed computing architecture.

- February 2023: AGS Health acquired the patient access outsourcing business unit of Availity. The development enabled AGS Health to provide faster and flexible financial clearance solutions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.50% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product, Application, and Region |

|

By Product |

Healthcare Payers

Healthcare Providers

|

|

By Application |

|

|

By Geography |

North America (By Product, Application, and Country)

Europe (By Product, Application, and Country/Sub-region)

Asia Pacific (By Product, Application, and Country/Sub-region)

Latin America (Product, Application, and Country/Sub-region)

Middle East & Africa (Product, Application, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 423.1 billion in 2026 and is projected to reach USD 756.55 billion by 2034.

In 2025, the market value stood at USD 196.8 billion.

The market is expected to exhibit a CAGR of 7.50% during the forecast period of 2026-2034.

The healthcare providers segment led the market by product.

The increasing burden of administrative workload, technology integrations is anticipated to drive the market growth.

NTT DATA, Inc., MDI NetworX LLC., and Invensis Technologies Pvt Ltd are some of the prominent players in the market.

North America dominated the healthcare BPO market with a market share of 49.60% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us