Healthcare Chatbots Market Size, Share & Industry Analysis, By Component (Software and Services), By Deployment (Cloud-based, and On-premise), By Technology (Natural Language Processing, Machine Learning, and Others), By Application (Medication & Drug Information Assistance, Appointment Scheduling, Automated Patient Support, and Others), By End User (Healthcare Providers, Healthcare Payers, and Others), and Regional Forecasts, 2026-2034

KEY MARKET INSIGHTS

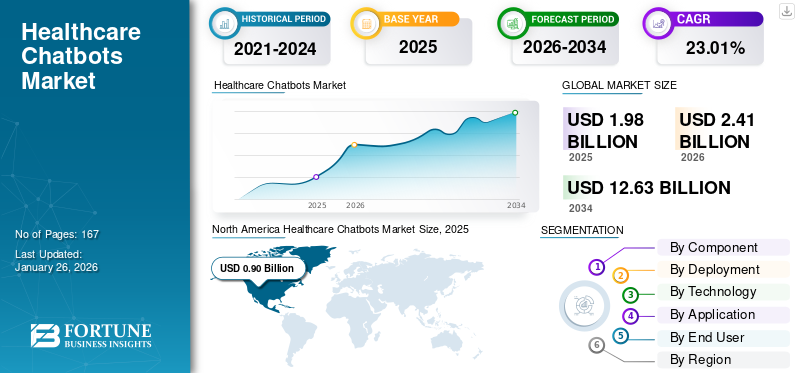

The global healthcare chatbots market size was valued at USD 1.98 billion in 2025. The market is projected to grow from USD 2.41 billion in 2026 to USD 12.63 billion by 2034, exhibiting a CAGR of 23.01% during the forecast period. North America dominated the healthcare chatbots market with a market share of 45.56% in 2025.

Healthcare chatbots are AI-powered virtual assistants that simulate human conversation, helping with tasks such as scheduling appointments, checking symptoms, and providing information, among various other applications. They automate routinely administrative tasks, reducing workload for healthcare providers and optimizing costs for both patients and providers. The significant global market growth is observed as healthcare providers are increasingly adopting these virtual solutions to automate repetitive tasks to optimize efficiency.

Furthermore, owing to various advantages and cost-optimization of these chatbots, the market is witnessing various funding initiatives by key operating players.

- For instance, in October 2025, Honey Health raised USD 7.8 million in seed funding. The company’s AI agents automate administrative workflows, including patient data retrieval, patient notes, post-visit orders, refills, faxes, and prior authorizations.

Furthermore, many key industry players, such as Ada Health GmbH, Healthily LTD., eMed, Woebot Health, Sensely, Inc., and HealthTab, Inc., are focusing on developing various innovative solutions to support the rising demand for effective patient engagement.

Download Free sample to learn more about this report.

Healthcare Chatbots Market Key Takeaways

- 2025 Market Size: USD 1.98 billion

- 2026 Market Size: USD 2.41 billion

- 2034 Forecast Market Size: USD 2.41 billion

- CAGR: 23.01% from 2026-2034

- North America dominated the healthcare chatbots market with a 45.56% share in 2025.

- The software segment held the largest share of 53.29% in 2026.

- The cloud-based segment accounted for a 75.76% share in 2026.

North America

North America accounted for USD 35.8 billion in 2025 and is projected to reach USD 37.69 billion in 2026.

Europe

Europe stood at USD 21.81 billion in 2025 and is expected to grow to USD 22.88 billion in 2026.

Asia Pacific

Asia Pacific generated USD 20.95 billion in 2025 and is projected to reach USD 22.3 billion in 2026.

U.S.

The market reached USD 0.86 billion in 2025.

Japan

Growing adoption of AI-driven healthcare solutions is supporting market expansion.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Increasing Adoption of Digital Healthcare Services to Drive Market Growth

One of the leading factors driving the growth of the market is the increasing adoption of digital healthcare services to reduce routinely administrative workload from the healthcare providers. The implementation of healthcare chatbots improve patient engagement and support regulatory tasks. Furthermore, increasing government support and incentives for digital adoption for outpatient care support the market growth.

- For instance, in October 2025, the European Commission launched COMPASS-AI, a flagship initiative to increase the use of AI in healthcare and to advance the safe and effective use of artificial intelligence (AI) in healthcare. Such initiatives are anticipated to drive the market growth.

MARKET RESTRAINTS

High Development and Maintenance Costs to Restrict Market Growth

One of the major factors restraining the market growth is the high development and maintenance costs. These AI-driven chatbots require substantial investment in data training, compliance testing, data security, and system integration. In addition, continuous updates to maintain medical accuracy and meet evolving regulations further raise costs. For small- and mid-sized providers, these financial barriers make chatbot implementation less feasible.

- For instance, in September 2025, USM Business Systems published a blog, which reported that on average, an AI chatbot application development cost with basic features ranged from USD 15,000 to USD 100,000.

MARKET OPPORTUNITIES

Development of Multilingual Healthcare Chatbots to Offer Lucrative Avenues for Market Growth

The development of multilingual chatbots in healthcare is expected to create lucrative avenues for market growth as it bridges the communication gap between healthcare providers and diverse patient populations. As chatbots become capable of understanding and responding in multiple languages, they enhance accessibility and patient engagement across regions. This improved communication fosters better compliance, encouraging broader adoption of these digital health solutions.

- For instance, in September 2025, Pocketalk launched the Pocketalk Enterprise App validated on Zebra Technologies. This solution offered multilingual healthcare communication, bringing together real time, secure, accurate language translation with patient engagement and remote care in one trusted ecosystem.

HEALTHCARE CHATBOTS MARKET TRENDS

Shifting Focus of Healthcare Chatbots for Support of Mental Health Patients is a Prominent Market Trend

One of the major global market trends is the increasing applications of these chatbots for automated support for mental health patients. Due to growing global market demand for timely psychological assistance, many healthcare providing systems are increasing the adoption of AI-driven chatbots that provide immediate support. Furthermore, many key companies are focusing on new product launches, anticipating growth opportunities.

- For instance, in June 2025, Wysa launched Wysa Gateway, an AI-powered chatbot in the U.S., designed to streamline mental health patient intake.

MARKET CHALLENGES

Lack of Clinical Accuracy and Validation to Restrict Market Growth

The lack of clinical accuracy and validation is a major challenge restraining the healthcare chatbots market growth. Chatbots often produce inconsistent or incorrect medical advice, especially in complex diagnostic scenarios where reasoning and contextual understanding are crucial. Without clinical benchmarking, healthcare providers remain cautious about integrating these tools into clinical workflows. Consequently, this challenge slows market adoption, limiting deployment to non-critical functions.

- For example, in December 2024, BMC Health Services Research published a report titled ‘Assessing the accuracy and quality of artificial intelligence (AI) chatbot-generated responses in making patient-specific drug-therapy and healthcare-related decisions’, which reported a lack of consistency in the responses that could lead to errors in clinical decisions.

Download Free sample to learn more about this report.

Segmentation Analysis

By Component

Increasing Product Launches for Software to Propel Segmental Growth

Based on the component, the market is divided into software and services.

The software segment dominated the market with a share of 53.29% in 2026 in the forecast period primarily due to the increasing demand for AI-driven conversational platforms and new product launches by key companies to meet this rising demand. The scalability of software platforms allows deployment across multiple functions such as triage, scheduling, and patient engagement. Such wide applications of this software drive segmental growth. Additionally, major key players are streamlining their resources toward new product development and their consecutive launches to capture the market.

- For instance, in February 2025, the University Hospitals of Geneva (HUG) launched the first AI-driven medical chatbot, ‘confIAnce’ in Switzerland, providing reliable, verified general medical information. This innovation represents a major step in integrating artificial intelligence into Swiss healthcare.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Strategic Partnership for New Product Launches to Drive Segmental Growth of Cloud-based Software

Based on deployment, the market is segmented into cloud-based and on-premises.

In 2026, the cloud-based segment dominated the market. The dominance of the segment is due to comparatively lower cost and scalability opportunities. The cloud-based deployment eliminates the need for expensive infrastructure or extensive IT maintenance. Furthermore, strategic collaboration among leading players to improve operational agility, reduce costs, and enhance digital patient experience to drive the growth of the segment. Furthermore, the segment is set to hold 75.76% share in 2026.

- For instance, in March 2021, Koninklijke Philips N.V. partnered with Orbita, Inc., to develop conversational voice and chatbot applications to complement its telehealth solutions. Its conversational platform allowed developers and non-technical staff to build and manage cloud-based virtual assistants.

In addition, the on-premises segment is projected to grow at a CAGR of 18.67% during the study period.

By Technology

Focus on Expanding Natural Language Processing Capabilities Underscoring its Advantages to Drive Segmental

On the basis of technology, the market is segmented into natural language processing, machine learning, and others.

In 2025, the natural language processing segment dominated the global market, based on technology. The dominance of this technology is due to various advantages over other technologies, such as context awareness, and multilingual capabilities. This leads to better communication and patient engagement. Continuous improvements in NLP capabilities make them suitable for complex healthcare queries. Consequently, healthcare providers are increasingly adopting NLP-based chatbots to improve communication accuracy. Furthermore, the segment is set to hold 40.86% share in 2026.

- For instance, in June 2024, Neurotechnology expanded its natural language processing (NLP) technology capabilities to offer its clients customizable virtual assistants and chatbots, boosting efficiency and customer satisfaction across many industries.

In addition, the machine learning segment is projected to grow at a CAGR of 27.21% during the study period.

By Application

Wide Application and New Product Launches to Lead Segmental Growth

On the basis of application, the market is segmented into medication & drug information assistance, appointment scheduling, automated patient support, and others.

In 2025, the automated patient support segment dominated the market due to increasing demand for automated workflows to reduce the workload of healthcare providers and around-the-clock assistance for effective patient management. Consequently, automated patient support has become the most widely used application, coupled with numerous new product launches, driving higher efficiency and better patient satisfaction. Furthermore, the segment is set to hold 50.2% share in 2026.

- For instance, in November 2021, Koninklijke Philips N.V. collaborated with U.S.-based MedChat to integrate the company’s AI-driven chatbot services into Philips Patient Navigation Manager to improve call center efficiency and speed the time to resolve patient inquiries. Such developments are expected to drive the growth of the segment.

In addition, the appointment scheduling segment is projected to grow at a CAGR of 20.38% during the study period.

By End User

Wide Adoption by Healthcare Providers to Lead Segmental Growth

On the basis of end user, the market is segmented into healthcare providers, healthcare payers, and others.

In 2025, the global market was dominated by healthcare providers on the basis of end users. Healthcare providers such as hospitals, clinics, and telehealth platforms are the primary users of chatbot technology for enhancing patient interaction. Wide adoption by these providers to reduce administrative burden drives the growth of the segment. Furthermore, the segment is set to hold 60.45% share in 2026.

- For instance, in August 2025, SSG hospital in Gujrat, India, launched an AI-powered oncology chatbot to assist cancer patients and their families.

In addition, the healthcare payers segment is projected to grow at a CAGR of 24.95% during the study period.

Healthcare Chatbots Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Healthcare Chatbots Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

North America contributed approximately USD 35.8 billion to the global market in 2025, accounting for 42.32% share, and is expected to reach USD 37.69 billion in 2026. The market in North America is expected to grow strongly due to a combination of favorable government initiatives, the rapid integration of AI. Furthermore, strategic collaborations for new product launches in the region also drive growth.

- For instance, in September 2024, the International Myeloma Foundation (IMF) launched Myelo, the AI-powered responsive chatbot designed to act as the IMF’s virtual assistant for patients, care partners, and healthcare professionals. In 2025, the U.S. market is estimated to reach USD 0.86 billion.

Europe

In 2025, the Europe market stood at USD 21.81 billion, representing 25.77% of global demand, and is projected to grow to USD 22.88 billion in 2026. Other regions, such as Europe, are anticipated to witness a notable growth in the coming years. During the forecast period, the European region is projected to record a growth rate of 21.33%, and reach a valuation of 0.52 billion in 2025. The growth in the region is attributed to new product launches and collaborations among academia and key operating companies in the region. Backed by these factors, countries including the U.K. anticipate to record the valuation of USD 0.13 billion, Germany to record USD 0.15 billion, and France to record USD 0.10 billion in 2026.

Asia Pacific

The Asia Pacific region captured 24.76% of the global market in 2025, generating USD 20.95 billion in revenue, and is projected to reach USD 22.3 billion in 2026. After Europe, the market in Asia Pacific is estimated to reach USD 0.40 billion in 2025 and secure the position of the third-largest region in the market. In the region, India and China are both estimated to reach USD 0.06 billion and USD 0.18 billion, respectively in 2026. The growth in the Asia Pacific region is attributed to government-led healthcare digitalization programs and rising investment in health tech startups.

Latin America and the Middle East & Africa

Latin America recorded a market size of USD 3.44 billion in 2025, capturing 4.06% of the global market share, and is projected to reach USD 3.56 billion in 2026. In 2025, Middle East & Africa generated USD 2.61 billion, contributing 3.08% to global market revenue, and is projected to grow to USD 2.68 billion in 2026. Over the forecast period, Latin America and the Middle East & Africa regions would witness a significant growth in this marketspace. The Latin America market in 2025 is set to record USD 0.09 billion as its valuation. Strong public-private investments, rapidly advancing healthcare infrastructure and the rising number of digital hospitals and specialty outpatient centers are fueling healthcare chatbot adoption in the region. They are expected to drive market growth in these regions further. In the Middle East & Africa, GCC is set to attain the value of USD 0.04 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Strategic Acquisitions by Key Players to Capitalize Market Share and Propel Market Growth

The global market holds a semi-consolidated market structure, constituting prominent players such as Ada Health GmbH, Healthily LTD., eMed, Woebot Health, and HealthTab, Inc., among others. The significant share of these companies in the market is due to numerous strategic activities, such as key mergers and acquisitions for robust product offerings, along with increasing focus on approvals by various regulatory bodies.

- For instance, in June 2024, Teckel Medical acquired Sensely Inc. to strengthen its position and increase efficiencies and reduce costs using its complementary technologies, including the company’s AI medical assistant.

Other notable players in the global market include Teckel Medical., K Pharmacy, LLC, and Infermedica. These companies are anticipated to prioritize new product launches and collaborations to boost their global healthcare chatbots market share during the forecast period.

LIST OF KEY HEALTHCARE CHATBOTS COMPANIES PROFILED

- Ada Health GmbH (Germany)

- Healthily LTD. (U.K.)

- eMed (U.S.)

- Woebot Health(U.S.)

- HealthTab, Inc. (Canada)

- K Pharmacy, LLC(U.S.)

- Buoy Health, Inc. (U.S.)

- Teckel Medical. (U.K.)

- Infermedica (Poland)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Healthily received a Class IIa certification for its Dot AI Medical Assessment under the European Union Medical Device Regulation (Regulation (EU) 2017/745)(EU MDR).

- June 2025: Cigna Healthcare launched a series of new digital features, including AI-powered virtual chatbot to improve the customer experience.

- July 2024: Gupshup collaborated with Meta, the Sudan Medical Specialization Board, and Shabaka to launch the telemedicine chatbot providing healthcare access for Sudanese refugees in Egypt, Eritrea, Saudi Arabia, Libya, Djibouti, and other neighboring countries. The solution aimed to bridge the gap in healthcare services for the Sudanese refugee population.

- November 2024: TeleVox received a purchasing agreement for AI chatbots with Premier, Inc. The agreement enabled Premier members, for special pricing and terms pre-negotiated by Premier for TeleVox’s SMART Web, SMART Voice, and SMART SMS powered by Iris, the conversational AI virtual agent for healthcare.

- February 2022: Ada Health GmbH received USD 120.0 million in funding that accelerated its growth and strengthened its presence in the U.S., following strong interest and traction in that market.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 23.01% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Component · Software · Services By Deployment · Cloud-based · On-premises · Natural Language Processing · Machine Learning · Others By Technology · Medication & Drug Information Assistance · Appointment Scheduling · Automated Patient Support · Others By End User · Healthcare Providers · Healthcare Payers · Others By Region · North America (By Component, Deployment, Technology, Application, End User, and Country) o U.S. o Canada · Europe (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o Germany o U.K. o France o Spain o Italy o Scandinavia o Rest of Europe · Asia Pacific (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o Brazil o Mexico o Rest of Latin America · Middle East & Africa (By Component, Deployment, Technology, Application, End User, and Country/Sub-region) o GCC o South Africa o Rest of the Middle East & Africa |

Frequently Asked Questions

The global healthcare chatbots market size was valued at USD 1.98 billion in 2025. The market is projected to grow from USD 2.41 billion in 2026 to USD 12.63 billion by 2034, exhibiting a CAGR of 23.01% during the forecast period.

In 2025, the market value stood at USD 0.90 billion.

The market is expected to exhibit a CAGR of 23.01% during the forecast period.

The cloud-based segment led the market on the basis of deployment.

Increasing adoption of healthcare chatbots to reduce repetitive administrative workload of healthcare providers is one of the leading factors to drive the market growth during the forecast period.

Ada Health GmbH, Healthily LTD., Woebot Health, and HealthTab, Inc. are some of the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 167

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us