Heat Stabilizers Market Size, Share & Industry Analysis, By Type (Calcium-Zinc Stabilizers, Barium-Zinc Stabilizers, Organotin Stabilizers, Lead-Based Stabilizers, and Others), By Application (Pipes & Fittings, Profiles & Tubing, Wires & Cables, Films & Sheets, and Others), and Regional Forecast, 2026-2034

Heat Stabilizers Market Size and Future Outlook

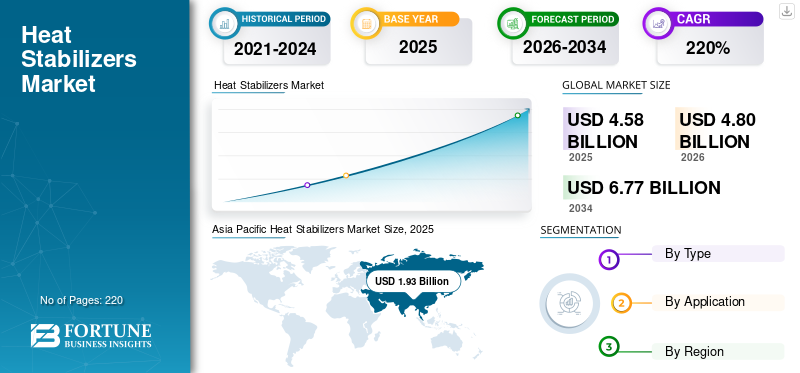

The global heat stabilizers market size was valued at USD 4.58 billion in 2025. The market is projected to grow from USD 4.80 billion in 2026 to USD 6.77 billion by 2034, exhibiting a CAGR of 4.4% during the forecast period. Asia Pacific dominated the global market with a market share of 42.14% in 2025.

The market comprises a range of additive systems used to protect polymers, especially polyvinyl chloride (PVC), from thermal degradation during processing and end-use exposure. The market covers major product types such as calcium-zinc stabilizers, barium-zinc stabilizers, organotin stabilizers, lead-based stabilizers, and other specialty stabilizer blends, which help maintain polymer strength, color stability, processing efficiency, and long-term durability. These stabilizers are widely used across applications, including pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC-based products where heat resistance and material stability are critical. The rising PVC consumption in construction, infrastructure, electrical insulation, and the automotive industry, along with the gradual shift toward lead-free and environmentally preferred stabilizer systems such as calcium-zinc formulations, is driving the market growth.

Furthermore, the major players in the industry include Galata Chemicals, Baerlocher GmbH, Valtris Specialty Chemicals, PMC Group, Inc., and SONGWON. Their competitive position is supported by strong PVC additive portfolios, established expertise in calcium-zinc, mixed metal, and organotin stabilizer systems, reliable raw material and formulation capabilities, and wide supply networks serving applications such as pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC-based products.

Download Free sample to learn more about this report.

Heat Stabilizers Market Key Takeaways

- 2025 Market Size: USD 4.58 Billion

- 2026 Market Size: USD 4.80 Billion

- 2034 Forecast Market Size: USD 6.77 Billion

- CAGR: 4.4% from 2026–2034

- Asia Pacific dominated the heat stabilizers market with a 42.14% share in 2025.

- The calcium-zinc stabilizers segment held the largest market share in 2025 due to its strong adoption in PVC processing and regulatory compliance.

- The profiles & tubing segment accounted for the largest application share in 2025, driven by high demand from the construction and infrastructure sectors.

Asia Pacific

Asia Pacific remained the leading regional market, reaching USD 1.93 billion in 2025, supported by strong PVC manufacturing activities.

Europe

Europe is expected to witness steady growth, with the market projected to reach USD 1.11 billion in 2026.

North America

North America continues to be a mature market, driven by demand for high-performance and compliance-oriented heat stabilizers across PVC applications.

U.S.

U.S. The market is estimated to reach approximately USD 0.83 billion in 2026, supported by steady construction and infrastructure demand.

Japan

Japan The market is estimated to reach approximately USD 0.27 billion in 2026, driven by sustained demand for advanced PVC processing applications.

Read More

HEAT STABILIZERS MARKET TRENDS

Growing Shift toward Lead-Free and High-Performance Stabilizer Systems in PVC Applications

One of the key trends in the market is the growing shift toward lead-free and performance-oriented stabilizer systems across PVC processing applications. End users are increasingly moving toward calcium-zinc, barium-zinc, organotin, and other advanced stabilizer blends that can provide better thermal stability, color retention, processing efficiency, and long-term product durability while supporting stricter environmental and regulatory requirements. As a result, suppliers are expanding their stabilizer portfolios for pipes and fittings, profiles and tubing, wires and cables, films and sheets, and other PVC-based products, where formulation quality and compliance are becoming more important.

- According to PVC.org, lead stabilizers were fully phased out in Europe by 2015 under the VinylPlus commitment, supporting the shift toward lead-free heat stabilizer systems such as calcium-zinc and organotin formulations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising PVC Use in Construction and Infrastructure Applications to Support Market Growth

The primary driver of the heat stabilizers market growth is the rising demand for PVC-based products in construction and infrastructure applications. In these areas, these stabilizers are essential for maintaining polymer stability during processing and improving long-term product performance. These additives are widely used in pipes & fittings, profiles & tubing, wires & cables, and films & sheets as they help prevent thermal degradation, discoloration, and loss of mechanical strength during high-temperature PVC processing. An additional layer of support comes from the growing preference for durable, cost-effective, and low-maintenance PVC materials in building, water management, electrical insulation, and infrastructure systems, which continues to strengthen the demand for heat stabilizer formulations.

- According to the Vinyl Institute, PVC building materials are used in rigid applications such as siding, windows, fencing, and decking, and flexible applications such as roofing, flooring, and wall coverings. This supports the heat stabilizer demand across construction-linked PVC products.

MARKET RESTRAINTS

Raw Material Volatility and Regulatory Pressure May Restrain Market Growth

The market faces a key restraint due to its dependence on metal-based compounds, organotin chemistry, specialty additives, and other formulation inputs that can be affected by raw material price volatility and supply availability. Since heat stabilizers are widely used in cost-sensitive PVC applications such as pipes & fittings, profiles & tubing, wires & cables, and films & sheets, fluctuations in input costs can directly influence production economics and product pricing. At the same time, regulatory pressure on heavy metal-based stabilizers, especially lead-based systems, is pushing producers and processors toward alternative formulations that may involve higher costs or reformulation challenges.

- According to the European Chemicals Agency (ECHA), lead compounds in PVC articles are considered hazardous to human health and the environment. The agency has proposed restricting PVC articles containing lead compounds as stabilizers above 0.1% by weight.

MARKET OPPORTUNITIES

Expanding Infrastructure and Water Management Applications to Create Market Opportunities

One of the key opportunities in the market is the expanding use of PVC products in infrastructure and water management applications. Heat stabilizers are essential in PVC pipes & fittings, profiles, tubing, and cable compounds as they help the material withstand processing temperatures while maintaining strength, color stability, and long-term durability. As governments and private developers continue investing in water supply, sanitation, housing, irrigation, power distribution, and urban infrastructure, the need for durable and cost-effective PVC products is expected to increase.

- According to the PVC Pipe Association (Uni-Bell), PVC pipe is used in water and wastewater systems as it offers longer life, lower maintenance, and corrosion-proof performance.

MARKET CHALLENGES

Balancing Performance, Compliance, and Cost to Create Challenges for Market Expansion

The market faces a key challenge in balancing product performance, regulatory compliance, and cost efficiency across large-volume PVC applications. PVC heat stabilizers are used in pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other products, where processors require stable thermal protection, good color retention, processing efficiency, and long-term durability. However, the shift away from traditional heavy metal-based stabilizers can increase formulation complexity and raise costs for manufacturers that need to maintain the same performance standards. The challenge becomes more significant in price-sensitive applications where buyers expect dependable supply, consistent quality, and competitive pricing at commercial scale.

- According to ECVM (PVC.org), PVC resin is usually combined with carefully selected additives in controlled formulations and nearly 500 different additives may be used depending on the required product function, with their use regulated under REACH in Europe.

Segmentation Analysis

By Type

Broad Use in PVC Processing to Support the Dominance of the Calcium-Zinc Stabilizers Segment

Based on type, the market is segmented into calcium-zinc stabilizers, barium-zinc stabilizers, organotin stabilizers, lead-based stabilizers, and others.

The calcium-zinc stabilizers segment holds the largest heat stabilizers market share due to its wide acceptance in PVC processing, strong regulatory alignment, and growing replacement of traditional lead-based stabilizer systems. Calcium-zinc stabilizers are widely preferred given that they offer effective thermal stability, good color retention, processing efficiency, and lower toxicity compared with heavy metal-based alternatives. Their use is especially strong in pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC applications, where manufacturers require stable performance along with compliance-friendly formulations.

- According to ESPA, lead-based stabilizers were traditionally used in rigid PVC construction products such as pipes, fittings, and profiles, but the European stabilizer industry committed to replacing them by 2015. This supports the growing use of calcium-zinc and other lead-free stabilizer systems.

The barium-zinc stabilizers segment is expected to grow at a CAGR of 3.5% over the forecast period.

By Application

To know how our report can help streamline your business, Speak to Analyst

Profiles & Tubing Segment Led the Market with the Rising Use of PVC Profiles in Various Applications

In terms of application, the market is categorized into pipes & fittings, profiles & tubing, wires & cables, films & sheets, and others.

The profiles & tubing segment held the largest share of the market in 2025, supported by the broad use of PVC profiles and tubing in construction, building materials, and technical applications. Heat stabilizers are widely used in this segment as PVC profiles require strong thermal stability, color retention, weatherability, and dimensional consistency during extrusion and long-term use. Their role in preventing polymer degradation during high-temperature processing makes them especially important in window profiles, door profiles, technical profiles, and tubing products. The strong demand from construction, renovation, infrastructure, and durable PVC product manufacturing continues to support the dominance of the profiles & tubing segment.

- According to Baerlocher, stabilizers are added to PVC to enable processing and improve resistance to outdoor exposure, weathering, and heat ageing, supporting their use in durable PVC profiles and tubing applications.

The pipes & fittings segment is expected to grow at a CAGR of 4.8% over the forecast period.

Heat Stabilizers Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa.

Asia Pacific

Asia Pacific Heat Stabilizers Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2024, Asia Pacific accounted for the largest share of the market, valued at USD 1.80 billion, and continued to lead in 2025, valued at USD 1.93 billion. The region benefits from its large PVC processing base, strong construction activity, expanding infrastructure development, and high consumption of PVC products across China, India, Japan, South Korea, and Southeast Asia. Heat stabilizing solutions are widely used in profiles & tubing, pipes & fittings, wires & cables, films & sheets, and other PVC-based applications, all of which have strong demand across the region’s building, electrical, packaging, and industrial sectors.

China Heat Stabilizers Market

The Chinese market is projected to reach USD 0.91 billion by 2026. China remains the region’s largest demand center, supported by its extensive PVC production and processing base, strong construction materials industry, and large-scale consumption of PVC products in pipes, profiles, tubing, cables, films, and sheets. The product demand is further supported by China’s role as a major manufacturing hub for building products, electrical components, packaging materials, and industrial PVC goods.

To know how our report can help streamline your business, Speak to Analyst

India Heat Stabilizers Market

The Indian market is estimated to touch around USD 0.36 billion in 2026, accounting for roughly 17.7% of the regional revenues.

Japan Heat Stabilizers Market

The Japan market is estimated to reach around USD 0.27 billion in 2026, accounting for roughly 13.3% of the regional revenues.

Europe

The Europe market is expected to experience steady growth over the coming years. During the forecast period, the region is projected to expand at a stable rate, attaining a market valuation of USD 1.11 billion by 2026. The market growth is supported by the strong demand from profiles & tubing, pipes & fittings, wires & cables, films & sheets, and other PVC-based applications across construction, infrastructure, electrical, and industrial sectors. The region also benefits from its established PVC processing base, mature building materials industry, and strong focus on compliant and higher-performance stabilizer systems.

U.K. Heat Stabilizers Market

The U.K. market is estimated to reach around USD 0.21 billion in 2026, accounting for roughly 18.8% of regional revenues.

Germany Heat Stabilizers Market

The Germany market is estimated to hit a value of around USD 0.28 billion in 2026, accounting for roughly 24.8% of regional revenues.

North America

North America continues to be a well-established and attractive market, supported by the steady demand from pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC-based applications. The region benefits from its mature construction sector, strong infrastructure base, advanced PVC processing capabilities, and continued use of stabilizers in applications that require thermal stability, color retention, processing efficiency, and long-term durability. The market is also supported by the region’s preference for higher-performance and compliance-oriented stabilizer systems, particularly calcium-zinc and organotin formulations.

U.S. Heat Stabilizers Market

Given North America’s significant contribution and the U.S. dominance in the region, the U.S. market is estimated to reach around USD 0.83 billion in 2026, accounting for roughly 84.6% of regional sales.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are relatively smaller in absolute size, yet continue to present significant growth prospects for the market. Growth in Latin America is supported by the rising demand for PVC products in construction, water management, electrical applications, packaging, and industrial manufacturing. The region’s use of heat stabilizers is closely linked to the demand for pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC-based products, particularly in Brazil, Mexico, and other developing economies. The Middle East & Africa are also showing steady potential, supported by expanding construction activity, infrastructure investment, water supply projects, and rising demand for PVC pipes, profiles, cables, and building materials. The GCC countries such as Saudi Arabia and the UAE benefit from large-scale infrastructure and real estate development, while South Africa and the rest of Middle East & Africa are supported by the demand across construction, utilities, and industrial PVC applications.

Brazil Heat Stabilizers Market

The Brazilian market is estimated to reach USD 0.18 billion in 2026, accounting for approximately 48.0% of regional revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Production Scale, Stabilizer Performance, and Application Reach to Secure a Competitive Edge

The market is moderately fragmented, with competition shaped by producers that can offer reliable production capacity, stable raw material access, efficient formulation capabilities, and strong distribution reach across PVC processing industries. Competitive advantage depends on the ability to maintain consistent stabilizer performance, support large-volume supply requirements, and align product development with demand from pipes & fittings, profiles & tubing, wires & cables, films & sheets, and other PVC-based applications.

Major participants such as Galata Chemicals, Baerlocher GmbH, Valtris Specialty Chemicals, PMC Group, Inc., and SONGWON benefit from strong PVC additive portfolios, technical formulation expertise, and established global supply networks serving construction, infrastructure, electrical, packaging, and industrial PVC markets. As competition continues to evolve, the market is increasingly favoring suppliers that combine dependable raw material sourcing, scale advantages, and application-specific technical support rather than competing only on volume.

LIST OF KEY HEAT STABILIZERS COMPANIES PROFILED

- Kisuma Chemicals (Netherlands)

- GOLDSTAB ORGANICS PVT LTD (India)

- Galata Chemicals (U.S.)

- MODERN CHEMICALS AND PLASTICS (India)

- Baerlocher GmbH (Germany)

- Amfine Chemical Corporation (U.S.)

- Valtris Specialty Chemicals (U.S.)

- PMC Group, Inc. (U.S.)

- Sun Ace Group (Japan)

- SONGWON (South Korea)

- SIAM STABILIZERS AND CHEMICALS (Thailand)

- AM Stabilizers Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Baerlocher GmbH exhibited its Tin Replacement program at K 2025, promoting calcium-zinc based alternatives to tin-based PVC stabilizers for applications including potable water pipes, fittings, medical, and packaging.

REPORT COVERAGE

The global heat stabilizers market analysis provides an in-depth study of market size and forecast by all the market segments included in the report. It includes details on market dynamics and trends expected to drive the market during the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market shares and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.4% from 2026-2034 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Segmentation | By Type, Application, and Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 4.58 billion in 2025 and is projected to reach USD 6.77 billion by 2034.

The market is slated to exhibit steady growth at a CAGR of 4.4% during the forecast period of 2026-2034.

By application, the profiles & tubing segment led the market in 2025.

Asia Pacific held the highest market share in 2025.

The rising demand for PVC products in construction, infrastructure, pipes & fittings, profiles, tubing, wires, and cables is a key factor driving the market growth.

- 2021-2034

- 2025

- 2021-2024

- 220

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us