Herbicides Market Size, Share & Industry Analysis, By Type (Synthetic [Glyphosate, Atrazine, Glufosinate, 2,4-Dichlorophenoxyacetic Acid, Acetochlor, and Others] and Biological), By Mode of Action (Selective Herbicides and Non-Selective Herbicides), By Form (Liquid and Dry), By Application Method (Foliar Method, Seed Method, Soil Method and Others), By Crop Type (Cereals & Grains, Oilseeds & Pulses, Fruits & Vegetables and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Jul 2026)

KEY MARKET INSIGHTS

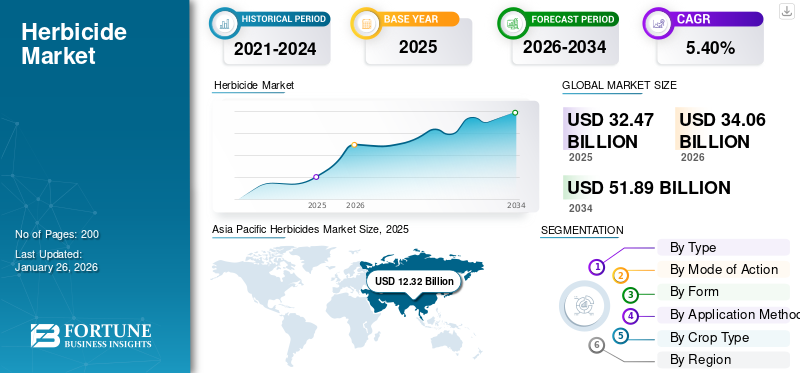

The global herbicides market size was valued at USD 32.47 billion in 2025 and is projected to grow from USD 34.06 billion in 2026 to USD 51.89 billion by 2034, exhibiting a CAGR of 5.40% during the forecast period. Asia Pacific dominated the herbicides market with a market share of 37.94% in 2025.

Herbicides are agricultural chemicals designed to prevent or destroy undesirable vegetation. Herbicides prevent unwanted weeds from competing with crops for sunlight, nutrients, and water.

Increasing food demand globally, arable land, and the necessity to improve agricultural productivity are motivating the use of chemical and bio-based herbicides in all key crop segments. According to the Food and Agriculture Organization (FAO), herbicide usage has increased since 2010, accounting for nearly 45% of all pesticide use globally, primarily driven by cereals and oilseed crops. The industry’s shift toward precision agriculture, low-drift spraying technologies, and integrated weed management systems has redefined the efficiency and sustainability of herbicide applications global.

Key players include Bayer AG, BASF SE, Syngenta AG, FMC Corporation, DowDuPont, UPL Ltd, Adama Agricultural Solutions, Nufarm Ltd, Valent Biosciences, Chemtura, and others.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Rising Global Food Demand and Shrinking Arable Land to Drive Market Growth

The increasing world population, which is set to grow beyond 9.7 billion by the year 2050, according to FAO, continues to put pressure on food systems. Cultivated land is gradually diminishing around the world due to urban growth, soil degradation, and climate change, forcing farmers to squeeze more production from each hectare. With decreasing farmland per capita, farmers are increasingly turning to sophisticated crop protection chemicals, such as herbicides, to maximize yields from each hectare. New herbicide formulations enable effective weed management and reduce labor requirements, thereby contributing directly to food production capabilities and driving herbicides market growth.

- According to the Food and Agriculture Organization (FAO), between 2001 and 2023, the global total cropland area per person decreased by 20%, falling from 0.24 to 0.19 hectares per capita. During this same period, however, land productivity grew by over 60%, from about USD 550 to almost USD 900 per hectare.

Market Restraints

Regulatory Limitations and Environmental Impact to Hamper Market Growth

Stringent regulatory constraints and environmental impact concerns are key reasons inhibiting the growth of the herbicides market. Ecological and health hazards from man-made herbicides, including water pollution, soil pollution, damage to non-target organisms, and residual properties, have prompted growing regulatory attention and public resistance across major agricultural economies.

- For instance, increasing regulatory focus, particularly in the European Union and North America, has resulted in the partial or total prohibition of various active ingredients, including Paraquat, and phase-outs of Atrazine.

Market Opportunities

Integration of Artificial Intelligence and Smart Spraying Systems to Unlock New Growth Opportunities

The use of Artificial Intelligence (AI) and intelligent spraying systems offers huge potential in the herbicide market by allowing targeted, effective, and environmentally sustainable control of weeds. Such technologies are increasingly being adopted in North America and Europe for optimization of costs and chemical consumption. Major agrochemical players such as Bayer, Syngenta, Corteva, and BASF are investing in AI and smart spraying technology to mitigate increasing weed resistance issues and sustainable agriculture demand.

- For instance, in February 2020, Bayer, in collaboration with Bosch, created a "Smart Spraying" system that employs cameras and sensors to detect weeds and spray them directly in real-time. This spot-spraying technique cuts herbicide usage by 10% to 55% below broadcast application, yet retains weed control efficiency.

Herbicides Market Trends

Increasing Focus on Sustainable and Eco-Friendly Formulations to Shape the Industry

The increasing focus on sustainable and eco-friendly formulations is among the newest and most prominent trends in the herbicide industry. This trend is prompted by escalating environmental regulations, consumer pressure for residue-free and organic crops, and the requirement to combat herbicide resistance and ecological influence. Companies are innovating with bio-based herbicides, developing products with new modes of action that reduce chemical load, and integrating precision agriculture for targeted application to minimize environmental footprint.

- For instance, in August 2025, UPL Sustainable Agri Solutions launched a new weed management solution, Brucia, a next-generation post-emergent herbicide specifically for maize crops in India. The company restates its commitment to sustainable, farmer-centric innovation by providing a simple-to-use, climate-resilient herbicide, Brucia.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Type

Synthetic Segment to Emerge as Dominant Segment Owing to its Cost-Effectiveness

On the basis of type, the market is bifurcated into synthetic and bio-herbicides.

Synthetic herbicides dominated the global herbicides market in 2026, accounting for 94.22% of the total market share, with the segment valued at USD 32.09 billion, driven by their broad-spectrum activity, reliability, and cost efficiency. Key synthetic herbicides include glyphosate, atrazine, glufosinate, 2,4-Dichlorophenoxyacetic Acid (2,4-D), acetochlor, and others. Synthetic herbicides typically require lower application rates due to their potency, saving costs and labor.

The bio-herbicides segment is projected to grow at a CAGR of 6.25% through 2032, supported by rising adoption in organic farming and government subsidies for biological crop protection.

To know how our report can help streamline your business, Speak to Analyst

By Mode of Action

Effectiveness in Targeted Weed Control to Lead Selective Herbicides Segment Growth

Based on the mode of action, the market is segmented into selective herbicides and non-selective herbicides.

Selective herbicides captured the largest share of the market in 2026, accounting for 54.49% of the total market share, primarily due to their high adoption in cereal, maize, and soybean fields, where targeted weed control is essential. Selective herbicides are highly popular because they can target certain species of weeds without harming the intended crop. This specificity lowers crop damage and increases crop yield, hence making them a must-have for farmers seeking to ensure weed control without compromising crop yield.

The non-selective herbicides segment is expected to grow at a moderate pace, at a CAGR of 5.23%. These herbicides are primarily used for non-crop and industrial vegetation management, but they are subject to stringent regulations.

By Form

High Absorption Rate and Compatibility to Lead Liquid Segment Growth

On the basis of the form, the market is segmented into liquid and dry.

The liquid herbicides accounted for approximately 67.16% of the total market revenue in 2024, owing to their superior ease of use, high absorption rates, and compatibility with foliar application systems and drones. These technologies enable precise and targeted spraying, thereby reducing waste and environmental impact.

Dry formulations such as granules, dusts, and powders held the remaining share and are preferred in water-scarce and mechanized regions including Australia and parts of Africa. The segment is expected to grow at a CAGR of 4.83% in the global herbicides market forecast period.

By Application Method

Foliar Method Segment to Exhibit High Growth Due to Quick Absorption and Effectiveness

On the basis of the application method, the market is segmented into foliar method, seed method, soil method, and others.

The foliar method led the market in 2026, accounting for 63.07% of the total market share, driven by its precision, quick action, and ease of integration. Additionally, it integrates easily with modern spraying technologies such as drones and automated sprayers, allowing for efficient and controlled application, which boosts its popularity among farmers.

The soil method segment is anticipated to grow significantly at a CAGR of 6.50% during the forecast period. Pre-emergence herbicides are mostly used in soil application methods.

By Crop Type

Large Cultivation Area and Global Staple Food Importance Fuels the Cereals & Grains Segment Market Leadership

On the basis of the crop type, the market is segmented into cereals & grains, oilseeds & pulses, fruits & vegetables, and others.

The cereals & grains segment dominated the market in 2026, accounting for 46.30% of the total market share, as crops such as wheat, rice, and corn require significant herbicide use for yield optimization. As dietary staples for the majority of the global population, maintaining crop productivity high and quality-assured is essential, necessitating the heavy use of crop protection products, including herbicides, to manage competitive weeds that are detrimental to crop yields.

The fruits & vegetables segment is anticipated to grow at a CAGR of 6.39% during the forecast period.

Herbicides Market Regional Outlook

Regionally, the report covers the global market analysis across North America, Europe, Asia Pacific, South America, the Middle East, and Africa.

Asia Pacific

Asia Pacific Herbicides Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 12.32 billion in 2025, capturing 37.94% of the global market share, and is projected to reach USD 13.01 billion in 2026. Expansion is sustained by higher usage of herbicides in India, China, and Southeast Asia, backed by FAO-sponsored programs for the modernization of crop protection. India's imports of herbicides increased by almost 30% in 2023, based on data provided by the U.S. Department of Agriculture (USDA), driven by more acreage of cereals and the usage of selective post-emergence herbicides. The Japan market is projected to reach USD 1.29 billion by 2026, the China market is projected to reach USD 4.93 billion by 2026, and the India market is projected to reach USD 2.94 billion by 2026.

North America

In 2025, North America generated USD 8.73 billion, contributing 26.89% to global market revenue, and is projected to grow to USD 9.13 billion in 2026. The region is dominated by mechanized agriculture on a vast scale, high usage of genetically modified (GM) herbicide-tolerant crops, and extensive coverage of precision agriculture technologies.

The U.S. herbicides market is the largest segment of the country’s crop protection industry, driven primarily by extensive cultivation of corn, soybeans, and cotton. Herbicides account for 69.62% of total pesticide usage in the U.S. in 2024, with demand dominated by glyphosate, 2,4-D, and emerging bio-herbicide formulations. The adoption of herbicide-resistant crops supports growth, but regulatory scrutiny and concerns about resistance management are steering R&D toward integrated weed management and sustainable chemical alternatives. The US market is projected to reach USD 6.32 billion by 2026.

Europe

The Europe market accounted for USD 6.1 billion in 2025, representing 18.78% of the global industry, and is expected to reach USD 6.34 billion in 2026. The Europe herbicide market is a mature but highly regulated herbicides market, with a situation of high environmental standards and advanced farming systems, accompanied by sustained adoption of sustainable crop protection products. Europe had an approximate share of 18.95% in the global market for herbicides in 2024. The UK market is projected to reach USD 0.48 billion by 2026, while the Germany market is projected to reach USD 1.03 billion by 2026.

South America

South America is projected to be the fastest-growing herbicide market globally with a CAGR of 6.38%, driven by the expansion of soybean, maize, and sugarcane production in Brazil and Argentina. The region’s large-scale agricultural base and export-oriented economy make it a strategic market for global agrochemical producers. Brazil alone accounts for 62.80% of South America’s herbicide use, led by soybean cultivation. The Brazilian Ministry of Agriculture (MAPA) recorded a 12% year-on-year increase in herbicide imports in 2023, reflecting strong demand from large commercial farms.

Middle East & Africa

The Middle East & Africa market generated USD 1.77 billion in 2025, representing 5.46% of the global market landscape, and is expected to reach USD 1.83 billion in 2026. The Middle East and Africa market is a smaller but fast-growing market for herbicides with excellent prospects as farm modernization gains momentum. While total consumption volumes remain lower than in other regions, increasing farm mechanization and government-supported diversification initiatives are fueling herbicide uptake.

Latin America

Latin America accounted for USD 3.55 billion in 2025, representing 10.93% of the global market share, and is projected to reach USD 3.76 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

R&D and New Active Ingredient Development to Maintain Competitive Advantage

The global herbicides market is moderately consolidated, with the presence of a few large multinational corporations that dominate active ingredient manufacturing and distribution, alongside several regional and domestic formulators driving the demand for herbicides. Companies such as Bayer CropScience AG, Syngenta AG, BASF SE, and Corteva Agriscience dominate due to large patent portfolios, advanced formulation technologies, and strong presence across North America, Europe, and the Asia Pacific. These firms invest heavily in new molecule discovery, digital farming solutions, and resistance-management programs.

Key Players in the Herbicides Market

|

Rank |

Company Name |

|

1 |

BASF SE |

|

2 |

Bayer AG |

|

3 |

Syngenta AG |

|

4 |

UPL Ltd. |

|

5 |

FMC Corporation |

List of Key Herbicide Companies Profiled

- Bayer CropScience AG (Germany)

- BASF SE (Germany)

- Syngenta AG (Switzerland)

- Corteva Agriscience (U.S.)

- UPL Ltd (India)

- FMC Corporation (U.S.)

- Sumitomo Chemical Co., Ltd. (Japan)

- ADAMA Agricultural Solutions Ltd. (Israel)

- Nufarm Limited (Australia)

- Nissan Chemical Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Syngenta and M.S. Technologies, L.L.C., announced the development of a groundbreaking herbicide-tolerant soybean trait stack, which is expected to be commercially available around 2029, pending regulatory approvals. This new trait build will be marketed under Syngenta's seed brands, including Golden Harvest and NK Seeds, as well as through licensing agreements with other companies such as Stine Seed Company and Merschman Seeds.

- June 2025: Syngenta AG unveiled a new herbicide molecule named metproxybicyclone, recognized as a breakthrough in weed control technology. It is classified as the fourth generation of ACCase inhibitors, a new chemical subclass officially recognized by the Herbicide Resistance Action Committee (HRAC) and the Weed Science Society of America (WSSA).

- March 2025: Oxford-based agricultural biotech firm Moa Technology has recently strengthened its efforts to develop innovative, safe, and affordable biological herbicides through a strategic partnership with NAICONS, an Italian natural products company. This collaboration aims to harness Moa’s proprietary high-throughput screening platform to evaluate 70,000 micro-bacterial extracts from NAICONS’ extensive library of natural compounds.

- March 2024: Corteva Agriscience launched a new product, Enversa herbicide, as a versatile, residual herbicide designed to tackle tough broadleaf and grass weeds in key crops such as soybeans, cotton, corn, sorghum, peanuts, and sugar beets.

- December 2023: Crystal Crop Protection Limited has acquired the trademark GRAMOXONE from Syngenta for use in the Indian market, a move announced in December 2023. GRAMOXONE is a widely recognized broad-spectrum herbicide brand. This acquisition is a strategic step for Crystal Crop Protection to expand its footprint within the herbicide category, which is currently the fastest-growing segment in crop protection in India.

REPORT COVERAGE

The global herbicides market industry report analyzes the market in depth and highlights crucial aspects such as global herbicides market trends, market dynamics, prominent companies, investment in research and development, and end-use. Besides this, the report also provides insights into the global Herbicides market analysis and highlights significant industry developments.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.40% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentations |

By Type, Mode of Action, Form, Application Method, Crop Type, and by Region |

|

Segmentation |

By Type

|

|

Mode of Action · Selective Herbicides · Non-Selective Herbicides |

|

|

By Form · Liquid · Dry |

|

|

By Application Method

|

|

|

By Crop Type · Cereals & Grains · Oilseeds & Pulses · Fruits & Vegetables · Others |

|

|

By Region · North America (By Type, Mode of Action, Form, Application Method, Crop Type, and Country) • U.S. (By Crop Type) • Canada (By Crop Type) • Mexico (By Crop Type) · Europe (By Type, Mode of Action, Form, Application Method, Crop Type, and Country) • Germany (By Crop Type) • Spain (By Crop Type) • Italy (By Crop Type) • France (By Crop Type) • U.K. (By Crop Type) • Rest of Europe (By Crop Type) · Asia Pacific (By Type, Mode of Action, Form, Application Method, Crop Type, and Country) • China (By Crop Type) • Japan (By Crop Type) • India (By Crop Type) • Australia (By Crop Type) • Rest of Asia Pacific (By Crop Type) · South America (By Type, Mode of Action, Form, Application Method, Crop Type, and Country) • Brazil (By Crop Type) • Argentina (By Crop Type) • Rest of South America (By Crop Type) · Middle East & Africa (By Type, Mode of Action, Form, Application Method, Crop Type, and Country) • South Africa (By Crop Type) • Egypt (By Crop Type) • Rest of the Middle East & Africa (By Crop Type) |

Frequently Asked Questions

Fortune Business Insights says that the global market was USD 32.47 billion in 2025 and is anticipated to reach USD 51.89 billion by 2034.

At a CAGR of 5.40%, the global market will exhibit steady growth over the forecast period.

By type, the synthetic segment leads the market.

Asia Pacific held the largest market share in 2025.

Rising global food demand and shrinking arable land drive the market growth.

BASF SE, Bayer AG, Syngenta AG, UPL Ltd., and FMC Corporation are the leading companies in the market.

Increasing focus on sustainable and eco-friendly formulations is shaping the industry.

- 2021-2034

- 2025

- 2021-2024

- 200

-

(Offer valid till 15th Jul 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us