High Purity Alumina Market Size, Share & Industry Analysis, By Grade (3N, 4N, 5N, and 6N), By Application (LED & Optoelectronics, Lithium-ion Batteries, Semiconductor, Ceramics, and Others), By End-Use Industry (Electronics & Electrical, Automotive (EV), Energy Storage, Medical, and Others), and Regional Forecast, 2026-2034

High Purity Alumina Market Size and Future Outlook

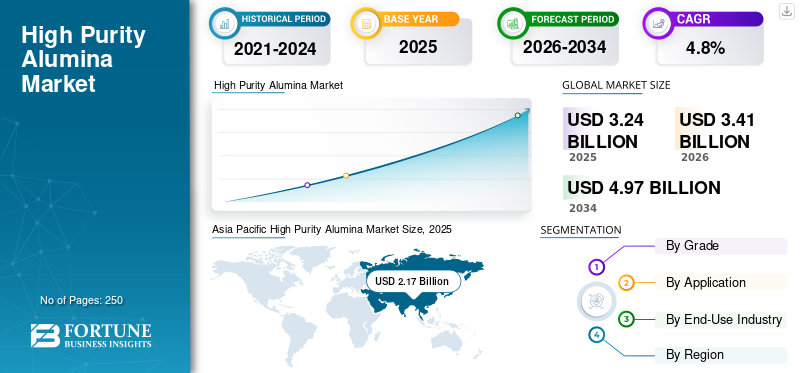

The global high purity alumina market size was valued at USD 3.24 billion in 2025. The market is projected to grow from USD 3.41 billion in 2026 to USD 4.97 billion by 2034, exhibiting a CAGR of 4.8% during the forecast period. Asia Pacific dominated the high purity alumina market with a market share of 66.98% in 2025.

The high purity alumina (HPA) market is progressing steadily as industries increasingly rely on advanced materials that enhance performance, durability, and product reliability. Rising demand for energy-efficient LED lighting, electric vehicle batteries, and high-strength electronic components is encouraging broader adoption across electronics, automotive, and industrial sectors. HPA adds functional value by improving thermal stability, insulation properties, and surface resistance, supporting longer product lifecycles and consistent quality. Expanding investments in clean energy technologies, battery manufacturing, and next-generation display systems are further driving market growth.

Leading companies, including Sumitomo Chemical Advanced Technologies, Sasol, Baikowski, Nippon Light Metal Holdings Co., Ltd., and Chalco Qingdao International Trading Co., Ltd., are reinforcing their presence in the market by advancing product development, scaling up production capacities, and strengthening their international supply and distribution networks.

Download Free sample to learn more about this report.

High Purity Alumina Market Takeaways

- 2025 Market Size: USD 3.24 billion

- 2026 Market Size: USD 3.41 billion

- 2034 Forecast Market Size: USD 4.97 billion

- CAGR: 4.8% from 2026–2034

- Asia Pacific dominated the high purity alumina market with a 66.98% share in 2025.

- The 4N grade segment is expected to grow at a CAGR of 4.5% during the forecast period.

- The lithium-ion batteries segment is projected to expand at a CAGR of 5.4% over the forecast period.

North America

North America represented a technologically advanced market and reached approximately USD 0.34 billion in 2025

Europe

Europe attained a market value of USD 0.47 billion in 2025.

Asia Pacific

Asia Pacific led the global market with USD 2.17 billion in 2025 and is expected to reach USD 2.29 billion in 2026.

U.S.

The market was valued at USD 0.30 billion in 2025, accounting for approximately 88.4% of North American revenue, supported by investments in EV battery production.

Japan

The country remains a key consumer of high purity alumina, supported by its advanced electronics, LED, and battery manufacturing industries.

Read More

HIGH PURITY ALUMINA MARKET TRENDS

Rapid Expansion of Electric Vehicles to Fuel Market Growth

A prominent trend in the market is the rising use of the material in next-generation energy storage systems. With the rapid expansion of electric vehicles and stationary energy storage, manufacturers are increasingly utilizing HPA as a coating material for lithium-ion battery separators to enhance thermal stability and operational safety. Its ability to improve battery lifespan and reduce the risk of overheating makes it a preferred choice in performance-driven applications. Beyond batteries, growing investments in clean energy infrastructure and advanced power management systems are further reinforcing the material’s role in supporting reliable and efficient energy technologies.

- According to the International Energy Agency (IEA), global electric car sales exceeded 17 million units in 2024, representing strong year-on-year growth and accelerating demand for advanced lithium-ion batteries, where ceramic materials such as HPA are widely used to enhance separator safety and thermal stability.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand from LED Lighting Systems and Electric Vehicle Production Drives Market Growth

The market is strongly driven by increasing demand from LED lighting systems and electric vehicle battery production. As countries continue to promote energy-efficient infrastructure and low-emission transportation, the adoption of LEDs and electric mobility is expanding rapidly across global markets. HPA plays a critical role in the production of sapphire substrates for LEDs and a coating material in lithium-ion battery separators, improving thermal stability, durability, and operational safety.

- According to the International Energy Agency (IEA), lighting accounts for around 15% of global electricity consumption, and the widespread adoption of LED technology could reduce electricity demand for lighting by up to 30% by 2030, reinforcing the growing need for materials used in LED production, such as HPA.

MARKET RESTRAINTS

High Production Costs and Energy-Intensive Processing to Restrain Market Expansion

The market faces challenges associated with high production costs and energy-intensive refining processes. Producing HPA requires advanced purification technologies, strict quality control, and significant energy input, which increases overall manufacturing expenses compared to standard alumina products. In addition, fluctuations in raw material prices and power costs can directly impact profitability for producers and pricing stability for end users.

- According to the International Energy Agency (IEA), alumina refining is an energy-intensive process, with electricity and fuel accounting for a significant share of production costs in the aluminum value chain, highlighting the cost pressures associated with producing high-grade alumina materials.

MARKET OPPORTUNITIES

Growing Investments in Semiconductor and Advanced Display Manufacturing to Create New Growth Opportunities

The market presents strong growth opportunities as global investments in semiconductor fabrication and advanced display manufacturing continue to rise. Increasing demand for high-performance consumer electronics, data infrastructure, and next-generation display technologies is driving the need for materials that offer superior thermal resistance, optical clarity, and structural stability. HPA is widely used in sapphire substrates, specialized ceramics, and electronic components that require consistent performance under demanding conditions. As countries expand domestic chip production and technology manufacturing capabilities, the need for reliable and high-grade alumina materials is expected to create sustained opportunities across the electronics value chain.

- According to SEMI, global semiconductor manufacturing capacity is expected to expand significantly with the addition of numerous new fabrication plants worldwide between 2024 and 2026, reflecting sustained investment in advanced chip production infrastructure that relies on high-performance materials.

MARKET CHALLENGES

Supply Chain Concentration and Quality Consistency to Hinder Market Expansion

The market faces challenges related to concentrated supply chains and the need for consistent ultra-high purity standards. Production of HPA is limited to a relatively small number of specialized manufacturers with advanced refining capabilities, increasing dependence on select suppliers and specific regions. Any disruption in raw material availability, energy supply, or export regulations can affect pricing and lead times across the value chain. In addition, maintaining uniform purity levels and particle characteristics is critical for applications in LEDs, batteries, and electronics, and even minor quality variations can impact end-product performance, creating operational risks for downstream manufacturers.

- According to the U.S. Geological Survey (USGS), Bauxite and Alumina, China, Australia, Brazil, and India accounted for 85% of total world alumina production in 2022, indicating a high level of concentration in global alumina supply.

Segmentation Analysis

By Grade

Ultra-high Purity Support the Dominance of the 5N Grade Segment

Based on grade, the market is segmented into 3N, 4N, 5N, and 6N.

The 5N grade segment holds the largest high purity alumina market share due to its balanced combination of ultra-high purity and commercial scalability. With a purity level of 99.999%, 5N grade alumina is widely used in lithium-ion battery separators, LED substrates, and advanced electronic components where thermal stability and material consistency are essential. Its suitability for large-scale battery manufacturing, particularly in electric vehicles and energy storage systems, has significantly strengthened demand.

- According to the International Energy Agency (IEA), electric car sales exceeded 17 million units in 2024, with continued rapid growth in lithium-ion battery production to support this expansion, reinforcing demand for high-purity materials used in battery components. This includes ultra-high purity alumina grades such as 5N that enhance separator performance and safety.

The 4N grade segment is expected to grow at a CAGR of 4.5% over the forecast period.

By Application

LED & Optoelectronics Segment Leads due to its Critical Role in Sapphire Substrate Production used in LED Lighting

Based on application, the market is segmented into LED & optoelectronics, lithium-ion batteries, semiconductor, ceramics, and others.

The LED and optoelectronics segment holds the largest share of the market due to its critical role in sapphire substrate production used in LED lighting and optical devices. HPA is processed into synthetic sapphire, which provides excellent transparency, thermal stability, and mechanical strength required for high-performance light-emitting diodes. The global transition toward energy-efficient lighting systems across residential, commercial, and industrial infrastructure has significantly increased LED adoption.

- According to the International Energy Agency (IEA), LEDs accounted for more than 50% of global lighting sales in recent years, reflecting their rapid adoption as the standard energy-efficient lighting technology worldwide and supporting strong demand for materials used in LED manufacturing, such as HPA.

The lithium-ion batteries segment is expected to grow at a CAGR of 5.4% over the forecast period.

By End-Use Industry

Expanding Use in Semiconductors Supports the Electronics & Electrical Segment Expansion

In terms of end-use industry, the market is categorized into electronics & electrical, automotive (EV), energy storage, medical, and others.

The electronics & electrical segment holds the largest share of the high purity alumina industry, driven by its widespread use in semiconductors, LED substrates, circuit components, and insulating materials. HPA is valued for its excellent thermal resistance, electrical insulation properties, and mechanical strength, making it suitable for high-performance electronic devices and power systems. Growing production of smartphones, laptops, data servers, and power electronics has increased the need for reliable and high-grade ceramic and substrate materials.

- According to the International Telecommunication Union (ITU), an estimated 5.4 billion people were using the internet in 2023, reflecting the continued expansion of digital infrastructure and electronic device usage worldwide, which supports sustained demand for advanced electronic materials.

To know how our report can help streamline your business, Speak to Analyst

The automotive (EV) segment is expected to grow at a CAGR of 5.5% over the forecast period.

High Purity Alumina Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific High Purity Alumina Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in the high purity alumina market in 2025, valued at USD 2.17 billion, and is expected to maintain its leading role in 2026, reaching USD 2.29 billion. The region’s leadership is supported by its strong presence in electronics manufacturing, LED production, lithium-ion battery assembly, and semiconductor fabrication. Rapid industrialization, expanding electric vehicle production, and large-scale investments in renewable energy and advanced materials processing contribute significantly to regional growth.

China High Purity Alumina Market

Based on Asia Pacific’s significant contribution and China’s position as a major alumina producer and technology manufacturing hub, the China market was valued at USD 1.17 billion in 2025, accounting for approximately 53.7% of regional revenues. The country’s large-scale LED manufacturing base, expanding electric vehicle battery production, and strong semiconductor ecosystem support both domestic consumption and export-oriented demand.

To know how our report can help streamline your business, Speak to Analyst

North America

North America represents a technologically advanced and steadily expanding regional market for HPA, projected to reach a valuation of USD 0.34 billion in 2025. Demand is supported by strong activity in semiconductor manufacturing, advanced battery research, aerospace electronics, and high-performance LED applications. The region benefits from established research institutions, growing investments in domestic chip fabrication, and increasing focus on electric vehicle supply chains.

U.S. High Purity Alumina Market

The U.S. market in 2025 reached a valuation of USD 0.30 billion, accounting for approximately 88.4% of regional revenues. Demand is driven by expanding semiconductor fabrication capacity, rising electric vehicle battery production, and strong defense and aerospace electronics manufacturing. The presence of advanced materials research facilities, supportive policy initiatives for domestic manufacturing, and increasing investment in clean energy technologies continue to reinforce the country’s role in the regional market.

Europe

Europe is expected to demonstrate stable, high purity alumina market growth, reaching a valuation of USD 0.47 billion in 2025. The region’s progress is supported by strong semiconductor research, expanding electric vehicle manufacturing, and increasing investments in battery cell production facilities. Strict environmental regulations and a growing focus on sustainable and energy-efficient technologies are encouraging the adoption of advanced ceramic and electronic materials.

Germany High Purity Alumina Market

Germany’s market reached a valuation of USD 0.14 billion in 2025, accounting for approximately 30.7% of regional demand. Growth is driven by the country’s strong automotive manufacturing base, expanding electric mobility production, and advanced engineering capabilities. Investments in battery technology, industrial automation, and high-performance electronics support steady consumption of high-grade alumina materials across key industries.

France High Purity Alumina Market

The France market in 2025 was valued at USD 0.075 billion, representing roughly 16.0% of regional revenues. Demand is supported by increasing focus on renewable energy infrastructure, aerospace manufacturing, and advanced electronic component production. Government-backed innovation initiatives and growing interest in clean mobility solutions contribute to gradual but sustained market expansion within the country.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are projected to experience gradual growth during the forecast period. The Latin America market reached a valuation of USD 0.098 billion in 2025, supported by expanding electronics assembly activities, growing renewable energy installations, and increasing interest in electric mobility. The Middle East & Africa market was valued at USD 0.17 billion in 2025, driven by rising industrial diversification efforts, infrastructure development, and investments in advanced materials processing. Strengthening focus on technology manufacturing, energy transition projects, and industrial modernization continues to support high purity alumina adoption across both regions.

Brazil High Purity Alumina Market

The Brazilian market in 2025 was valued at USD 0.049 billion, accounting for approximately 50.0% of global revenues. Demand is supported by the country’s established alumina production base, growing renewable energy projects, and expanding industrial manufacturing sector. Investments in downstream value-added materials processing and the gradual development of advanced electronics and battery-related applications are expected to contribute to steady market expansion in Brazil.

COMPETITIVE LANDSCAPE

Key Industry Players

Industry Participants Focus on Strengthening Their Competitive Position to Expand Production Capacities

The market remains moderately consolidated, as large-scale production requires advanced purification technologies, precise process control, and the ability to consistently achieve ultra-high purity standards. Significant investment in refining infrastructure, quality assurance systems, technical application development, and secure global supply networks creates substantial entry barriers for new participants.

Companies such as Sumitomo Chemical Advanced Technologies, Sasol, Baikowski, Nippon Light Metal Holdings Co., Ltd., and Chalco Qingdao International Trading Co., Ltd. are strengthening their competitive position by enhancing product purity levels and expanding production capacities. This improves technical support for battery and electronic applications, and reinforces their regional and international distribution capabilities.

LIST OF KEY HIGH PURITY ALUMINA COMPANIES PROFILED

- Sumitomo Chemical Advanced Technologies.(U.S.)

- Sasol (South Africa)

- Baikowski (France)

- Nippon Light Metal Holdings Co., Ltd (Japan)

- TAIMEI CHEMICALS Co., Ltd. (Japan)

- Shandong Sinocera Functional Materials Co., Ltd. (China)

- HONGHE CHEMICAL (China)

- Chalco Qingdao International Trading Co., Ltd. (China)

- Alpha HPA (Australia)

- Vizag Chemical (India)

KEY INDUSTRY DEVELOPMENTS

- January 2026: Alpha HPA secured a USD 75 million equity investment from Australia’s National Reconstruction Fund Corporation (NRFC) to support the completion and operation of its Gladstone HPA production facility.

- August 2023: Sumitomo Chemical Advanced Technologies (Sumitomo Chemical) announced mass production of ultra-fine α-alumina (NXA series) at its Ehime Works, positioned for applications including Li-ion battery separators and LED/semiconductor-related uses.

- June 2023: Chalco and Guinea Alumina Corporation (GAC) agreed to explore cooperation on alumina refining in Guinea, following an MoU signed in March 2023.

REPORT COVERAGE

The global market analysis provides an in-depth study of the market size and forecast for all the market segments included in the report. It includes details on the market dynamics and high purity alumina market trends expected to drive the market over the forecast period. It offers information on technological advancements, new product launches, key industry developments, and details on partnerships, mergers, and acquisitions. The market research report also encompasses a detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.8% from 2026 to 2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Grade, Application, End-Use Industry, and Region |

| By Grade |

|

| By Application |

|

| By End-Use Industry |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.24 billion in 2025 and is projected to reach USD 4.97 billion by 2034.

Recording a CAGR of 4.8%, the market is slated to exhibit steady growth during the forecast period.

By end-use industry, the electronics & electrical segment leads the market.

Asia Pacific held the highest market share in 2025.

Rising demand from high-performance LED lighting is the key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us