High Temperature Insulation Market Size, Share & Industry Analysis, By Material Type (Ceramic, fibers, Insulating Firebricks (IFB), Calcium Silicate, and Others), By Temperature Range (600–1,100°C, 1,100–1,400°C, and Above 1,400°C), By End-Use Industry (Petrochemical & Chemical, Iron & Steel, Ceramics, Glass, Cement, and Others), and Regional Forecast, 2026-2034

High Temperature Insulation Market Size and Future Outlook

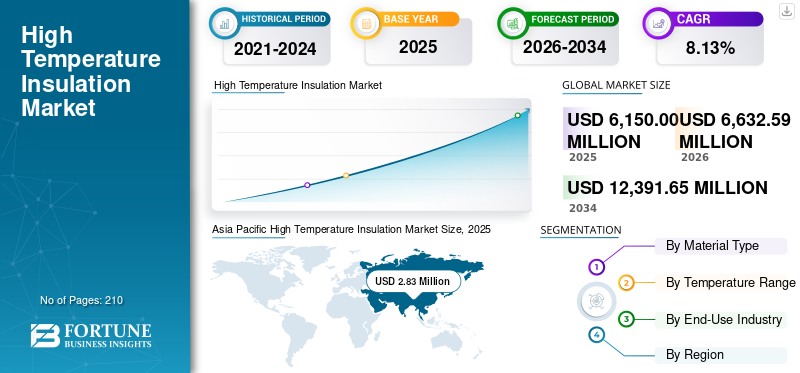

The global high temperature insulation market size was valued at USD 6,150.00 million in 2025 and USD 6,632.59 million in 2026. Moreover, the market is projected to reach USD 12,391.65 million by 2034, exhibiting a CAGR of 8.13% during the forecast period. Asia Pacific dominated the global high temperature insulation market with a market share of 45.98% in 2025. Moreover, Asia Pacific accounts for the largest market revenue share, driven by rapid industrialization, energy-intensive sectors such as steel and petrochemicals, and supportive energy efficiency policies.

High-temperature insulation materials are designed to withstand extreme heat, preventing heat loss and improving energy efficiency in high-temperature industrial and commercial End-Use industries. Demand drivers include the increasing need for energy conservation and efficiency, stricter environmental regulations and the push to reduce greenhouse gas emissions, and the continued growth of high-temperature industries such as oil and gas, petrochemicals, and metallurgy.

- In November 2025, the Government of India announced a target of a USD 1 trillion economy of petrochemicals by 2040. Hence, such developments are expected to impact the High Temperature Insulation demand in the coming years positively.

3M holds a leading position in the high-temperature insulation market. The company is consistently ranked among the top global manufacturers in various insulation sectors. The company offers advanced solutions, including innovative ceramic fibers and microporous insulation technologies, as well as thermal fabrics and materials for aerospace and industrial End-Use industries. They are also involved in the dry transformer insulation market.

Download Free sample to learn more about this report.

High Temperature Insulation Market Key Takeaways

- 2025 Market Size: USD 6,150.00 million

- 2026 Market Size: USD 6,632.59 million

- 2034 Forecast Market Size: USD 12,391.65 million

- CAGR: 8.13% from 2026–2034

- Asia Pacific dominated the high temperature insulation market in 2025.

- The ceramic fibers segment accounted for 47.35% of the global market share in 2025.

- The petrochemical & chemical segment held the largest end-use share of 30.57% in 2025.

Asia Pacific

Asia Pacific emerged as the largest regional market in 2025 with a valuation of USD 2,827.77 million.

North America

North America generated USD 1,105.16 million in revenue in 2025 and is projected to reach USD 1,195.22 million in 2026.

Europe

Europe accounted for the third-largest regional market with a valuation of USD 1,442.18 million in 2025.

U.S.

The U.S. remains a major contributor to the North American market, driven by strong demand for high-temperature insulation across petrochemical, industrial manufacturing, and power generation applications.

Japan

Japan continues to be an important market in Asia Pacific, supported by advanced manufacturing capabilities and increasing adoption of energy-efficient insulation materials.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growth of Infrastructure and Manufacturing Industries to Drive Market Growth

The growth of infrastructure and manufacturing industries is a key driver for the high-temperature insulation market. As sectors such as power generation, petrochemicals, aerospace, and heavy manufacturing expand, the demand for materials that can withstand extreme heat rises significantly.

- In November 2025, Moderna invested USD 140M to onshore drug product manufacturing at its Norwood, MA facility in the U.S., completing full end-to-end US mRNA production by mid-2027, reducing reliance on contractors. This biopharma expansion drives demand for high-temperature insulation in sterile processing equipment and cleanrooms.

High temperature insulation enhances operational efficiency and safety by reducing heat loss and protecting equipment from thermal damage. Infrastructure projects such as refineries, power plants, and industrial facilities require advanced insulation to meet regulatory standards and improve energy conservation. This expanding industrial activity fuels increasing adoption of high-temperature insulation solutions, contributing strongly to market growth across the globe.

Energy Efficiency & Emission Reduction Regulations to Propel Market Growth

Energy efficiency and emission reduction regulations are significant drivers for the high-temperature insulation market. Strict government regulations worldwide mandate reduced energy consumption and lower emissions, compelling industries to adopt advanced high-temperature insulation materials that minimize heat loss and improve thermal efficiency.

By enhancing energy conservation, these regulations lower operational costs and reduce environmental impact. Industries such as petrochemical, steel, and power generation increasingly rely on high-temperature insulation to comply with emission standards and ensure safer, more sustainable operations. This regulatory push accelerates innovation and market adoption of high-performance insulation solutions globally.

MARKET RESTRAINTS

Volatility in Raw Material Prices to Restraint Market Growth

Volatility in raw material prices is a significant restraint for the high-temperature insulation market. Key raw materials such as alumina, silica, and zirconium dioxide constitute 40-60% of production costs for ceramic fiber insulation. Price fluctuations in these materials, driven by supply chain disruptions, geopolitical tensions, and reliance on suppliers from regions such as China, create margin pressures for manufacturers. Crude oil price changes impact raw material costs derived from petrochemical sources, adding to cost instability. Smaller players face particular vulnerability due to their limited ability to absorb price spikes or secure long-term contracts, which hampers market predictability and growth.

MARKET OPPORTUNITIES

Shift from Conventional Refractory Bricks to Lightweight Ceramic Fibers to Create Lucrative Opportunities

The shift from conventional refractory bricks to lightweight ceramic fibers presents lucrative opportunities in the high-temperature insulation market. Ceramic fibers offer significant advantages, such as being 5-10 times lighter than refractory bricks, which reduces equipment load and structural stress.

- In December 2024, RATH launched production of ALTRA FLEX oxide ceramic continuous fibers (K99, M75) at Mönchengladbach, Germany, via sol-gel process, yielding up to 10 tons/year for CMCs and heat-resistant fabrics. This bolsters the high-temperature insulation market with innovative, thermally resistant reinforcements.

They provide superior thermal insulation with lower thermal conductivity, enabling energy savings of 20-40%. Installation is faster and simpler due to flexibility and ease of cutting, reducing labor costs and downtime. Ceramic fibers also resist thermal shock better, enhancing durability in fluctuating conditions. These factors make ceramic fibers attractive for modern industrial End-Use industries, driving high temperature insulation market growth through cost-effectiveness and performance benefits.

MARKET CHALLENGES

Competition from Alternative Anode Innovations Creates Challenges for Market Energy & Expansion

Competition from low-cost insulation material providers poses significant challenges to the high-temperature insulation market. Regional manufacturers, particularly from China and Asia Pacific, offer ceramic fibers and alternative materials at 20-30% lower prices than premium brands such as 3M, Morgan Advanced Materials plc, and Luyang Energy-saving Materials Co., Ltd. These low-cost options often compromise on thermal performance, durability, and safety certifications, attracting price-sensitive buyers in emerging markets.

Premium providers face margin erosion and market share loss in cost-driven sectors such as steel and cement. This intensifies pricing pressures, forcing innovation in cost-effective, high-performance solutions to maintain a competitive edge.

HIGH TEMPERATURE INSULATION MARKET TRENDS

Increasing Lightweight Ceramic Fiber Adoption is emerging as a Key Trend

Lightweight ceramic fiber adoption is a prominent trend in the advanced high-temperature insulation market size and growth. Driven by industrial expansion in steel, petrochemicals, and power generation, ceramic fibers provide superior thermal efficiency with lower conductivity, enabling 20-40% energy savings over traditional materials. Their lightweight nature, 5-10 times lighter than refractory bricks, reduces structural loads and installation time, cutting costs and downtime. Stricter energy regulations and emission standards further accelerate this shift, particularly in the Asia Pacific, where rapid urbanization boosts demand.

Download Free sample to learn more about this report.

IMPACT OF TARIFFS

Tariffs increase high-temperature insulation costs by raising prices for imported raw materials and finished products, leading to higher prices for consumers and potentially lower demand. This forces companies to adjust supply chains by shifting to domestic production, seeking alternative suppliers in tariff-free regions, or forging strategic partnerships to mitigate risks and maintain competitiveness. Tariffs have also increased investments in local manufacturing and created a more fragmented global market with regional differences in innovation and pricing.

SEGMENTATION ANALYSIS

By Material Type

Ceramic Fibers are expected to Dominate Market Due to their High adoption in Petrochemical Industry

Based on material type, the market is segmented into ceramic fibers, Insulating Firebricks (IFB), calcium silicate, and others.

Ceramic fibers is expected to dominate the market, with a 47.35% high temperature insulation market share in 2025, with strong demand driven by superior thermal efficiency in steel, petrochemicals, and power sectors.

- In September 2025, CNR-ISSMC supplied ultra-high temperature ceramic matrix composites (UHTCMCs) for the Wintertime experiment on the International Space Station, advancing extreme heat-resistant materials. These innovations enhance high-temperature insulation for aerospace thermal protection systems and industrial furnaces.

The Insulating Firebricks (IFB) segment is expected to witness the fastest growth. IFBs are favored for their high thermal resistance and low thermal conductivity, making them essential for furnaces, kilns, and reactors that require maintaining extreme operational temperatures while minimizing heat loss. Their demand is driven by heavy industries such as steel, petrochemicals, cement, and glass, where efficient insulation enhances energy savings and operational safety.

By Temperature Range

600–1,100°C is expected to Dominate Market Due to its Application in Various Manufacturing Processes

Based on the temperature range, the market is segmented into 600–1,100°C, 1,100–1,400°C, and above 1,400°C.

600–1,100°C is expected to dominate the market, with a 41.29% market share in 2025. The segment growth is driven by significant demand in the high-temperature insulation market, essential for petrochemical furnaces, kilns, and boilers. It accounts for a major revenue share, fueled by energy efficiency regulations and industrial expansion.

The above 1,400°C segment is experiencing robust demand growth in the high-temperature insulation market, driven by industries such as aerospace, nuclear, and specialty metallurgy. Advanced materials such as nanomaterials and ceramics provide thermal stability and corrosion resistance, meeting extreme temperature and harsh environment needs.

By End-Use Industry

Petrochemical & Chemical Segment is expected to Dominate Market owing to Prominence in Major Countries

Based on the end-use industry, the market is segmented into petrochemical & chemical, iron & steel, ceramics, glass, cement, and others.

Petrochemical & chemical dominated the global high temperature insulation market in 2025 with a revenue share of 30.57%. The petrochemical and chemical end-user industries are major growth drivers of the market for high-temperature insulation. These sectors require advanced insulation solutions to manage process temperatures, improve energy efficiency, and ensure operational safety in reactors, distillation columns, and furnaces.

However, the ceramics segment will grow at the fastest CAGR of 8.89% owing to the demand for ceramic fibers and firebricks in kilns, furnaces, and advanced manufacturing. Energy efficiency mandates and Asia Pacific industrialization boost adoption for heat management in ceramics production.

To know how our report can help streamline your business, Speak to Analyst

HIGH TEMPERATURE INSULATION MARKET REGIONAL OUTLOOK

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

The Asia Pacific market emerged as the largest market with a valuation of USD 2,827.77 million in 2025, driven by rapid industrialization, energy-intensive sectors such as steel and petrochemicals, and supportive energy efficiency policies. For instance, in August 2024, Saudi Aramco announced investment plans in China's petrochemical sector, driven by rising plastics demand from clean energy growth, potentially exceeding USD 100 million. This fuels high temperature insulation needs for new reactors, crackers, and refineries in the Asia Pacific.

Asia Pacific High Temperature Insulation Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America

North America’s high temperature insulation industry was valued at USD 1,105.16 million in 2025 and is estimated to reach USD 1,195.22 million in 2026. The market grows steadily, fueled by power generation, petrochemicals, and manufacturing demands alongside stringent energy efficiency regulations. The U.S. market is mainly driven by energy efficiency requirements, strict regulations, and demand from core industries such as petrochemical and aerospace.

Europe

Furthermore, the Europe market is expected to account for the third-largest share with a valuation of USD 1,442.18 Million in 2025. Europe's high-temperature insulation market thrives on stringent energy efficiency regulations, industrial expansion in power and chemicals, and EU sustainability initiatives driving advanced insulating material adoption.

Latin America

Latin America’s market growth is driven by sectors such as cement, mining, and glass, while government sustainability initiatives and energy-saving priorities further stimulate market expansion.

Middle East & Africa

Moreover, the Middle East & Africa market is experiencing significant growth with a CAGR of 6.67%. Growth is supported by increasing infrastructure projects, green building regulations, and expanding oil and gas industries, driving demand for advanced insulation materials in commercial and industrial sectors.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Focused on Product Launches and Innovation to Increase Market Share in Future

The competitive landscape is consolidated, with key players in the insulation market including Morgan Advanced Materials, Unifrax/Alkegen, Luyang Energy-Saving Materials Co., Ltd., 3M, and Promat, among others. For instance, in November 2025, Salomon launched the Spectral ski jacket featuring PrimaLoft ThermoPlume insulation, mimicking down's loft and compressibility with synthetic wet-weather resilience. AdvancedSkin Dry 20K/20K shell, ClimateSync vents, removable hood, and powder skirt enhance performance and sustainability. Such developments are expected to foster market growth over the forecast period.

List of the Key High Temperature Insulation Companies Profiled

- Morgan Advanced Materials (U.K.)

- Unifrax/Alkegen (U.S.)

- Luyang Energy-Saving Materials Co., Ltd. (China)

- 3M (U.S.)

- Promat (Belgium)

- RHI Magnesita (Austria)

- NICHIAS Corporation (Japan)

- Isolite Insulating Products Co., Ltd. (Japan)

- Aspen Aerogels (U.S.)

- Ibiden Co., Ltd. (Japan)

- Rath Group (Austria)

- Skamol (Denmark)

- Pyrotek (U.S.)

- Minye Refractory Fiber Co., Ltd. (China)

- Insulcon Group (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Ponda raised USD 2.4M in seed funding to commercialize BioPuff, a Typha-based insulation matching goose down's thermal performance at a lower cost. Cultivation regenerates peatlands, cutting emissions and boosting biodiversity, with partners such as Berghaus.

- September 2025: PrimaLoft launched UltraPeak, its warmest insulation yet, using architectural fibers for superior heat-trapping, loft, and soft feel. Made with 100% recycled content via P.U.R.E. technology, it cuts carbon emissions by over 50%.

- August 2025: Padtex Insulation acquired a 50% stake in McAllister Mills Inc. to accelerate innovation in advanced thermal and fire protection systems, combining expertise in high-temperature textiles for industrial End-Use industries.

- April 2025: Armacell launched ArmaGel XGC, a flexible aerogel insulation blanket designed for cryogenic and dual-temperature End-Use industries. It offers ultra-low thermal conductivity, an integrated zero-perm vapor barrier, hydrophobic properties, and ASTM compliance, enabling exceptional energy efficiency and corrosion protection.

- March 2023: Etex acquired Skamol, a Danish high-temperature insulation expert specializing in calcium silicate and vermiculite boards for kilns, furnaces, and fire protection. The deal strengthens Etex's sustainable portfolio amid rising energy efficiency demands.

REPORT COVERAGE

The global high temperature insulation market report delivers a detailed insight into the market. It focuses on key aspects, such as leading companies in the high temperature insulation market. Additionally, the report provides regional insights and global market trends & technology, as well as highlights key industry developments. In addition to the factors mentioned above, the report encompasses several other factors and challenges that contributed to the market's growth and decline in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| Attributes | Details |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 8.13% from 2026 to 2034 |

| Unit | Value (USD Million) |

| Segmentation | By Material Type, Temperature Range, End-Use Industry, and Region |

| Segmentation |

By Material Type

|

|

By Temperature Range

|

|

|

By End-Use Industry

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the market size was USD 6,150.00 million in 2025.

The market is projected to grow at a CAGR of 8.13% over the forecast period.

The petrochemical & chemical segment is expected to lead the market over the forecast period.

The market size of the Asia Pacific stood at USD 2,827.77 million in 2025.

The growth of infrastructure and manufacturing industries are the key factors driving the market growth.

Some of the top players in the market include Morgan Advanced Materials, Unifrax/Alkegen, Luyang Energy-Saving Materials Co., Ltd., 3M, and Promat, among others.

The global market size is expected to reach USD 12,391.65 million by 2034.

- 2021-2034

- 2025

- 2021-2024

- 210

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us