Home Textiles Market Size, Share & Industry Analysis, By Material (Synthetic Fibers and Natural Fibers), By Product (Bedroom Linen, Bathroom Linen, Carpets & Floor Coverings, Curtains & Drapes, and Others), By Fabric Type (Woven and Non-woven), By Distribution Channel (Specialty Stores, Supermarkets/Hypermarkets, Online, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

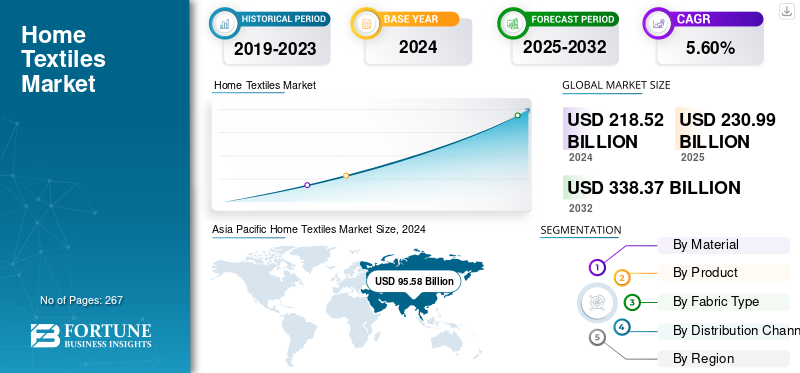

Home Textiles Market Size and Industry Overview

The global home textiles market size was valued at USD 230.99 billion in 2025. The market is projected to grow from USD 244.76 billion in 2026 to USD 471.90 billion by 2034, exhibiting a CAGR of 8.55% during the forecast period. Asia Pacific dominated the home textiles market with a market share of 44.17% in 2025.

The home textile industry forms a vital part of the textile industry, encompassing products such as bedroom and bathroom linens, carpets and floor coverings, curtains and drapes, as well as kitchen and decorative textiles. These products are integral to home furnishing, comfort, and interior aesthetics, combining both functional and decorative value. The market is primarily driven by rising urbanization, increasing household incomes, home décor trends, and the expansion of e-commerce. Furthermore, growing housing construction in emerging economies further drives the product demand. Woven fabrics account for the majority of home-textile products. On the other hand, nonwovens and blended synthetics are gaining market share due to their cost efficiency and functional benefits. With a growing focus on sustainable, organic, and recycled fibers, the sector is undergoing material innovation and design diversification.

Major players, including Welspun India Ltd., Springs Global, Trident Group, Indo Count Industries Ltd., Mohawk Industries, Ralph Lauren Home, IKEA, and Bed Bath & Beyond, are some of the well-established brands in the market. These companies focus on sustainability, vertical integration, and product innovation. For instance, Welspun and Trident invest heavily in eco-friendly manufacturing and traceable cotton sourcing, while IKEA emphasizes circular design and the use of recyclable materials.

Download Free sample to learn more about this report.

Home Textiles Market Key Takeaways

- 2025 Market Size: USD 230.99 billion

- 2026 Market Size: USD 244.76 billion

- 2034 Forecast Market Size: USD 471.90 billion

- CAGR: 8.55% from 2026–2034

- Asia Pacific dominated the home textiles market with a 44.17% share in 2025.

- The natural fibers segment is projected to grow at a CAGR of 6.15% during the forecast period.

- The bathroom linen segment is expected to expand at a CAGR of 6.58% during the forecast period.

Asia Pacific

Asia Pacific generated USD 102.03 billion in 2025 and is projected to reach USD 109.17 billion in 2026.

North America

North America accounted for 25.79% of the global market in 2025 and is expected to reach USD 62.63 billion in 2026.

Europe

Europe contributed 21.12% of global revenue in 2025 and is projected to reach USD 58.14 billion in 2026.

U.S.

Strong consumer spending on home furnishings and renovation activities continues to support market growth.

Japan

Rising demand for premium and sustainable home textile products is driving market expansion.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rising Urbanization and Home Improvement Spending to Drive Market Expansion

The global home textiles market growth is primarily driven by the accelerating pace of urbanization, coupled with a surge in home renovation and interior improvement activities. As more people move to urban areas and adopt modern lifestyles, the demand for aesthetically appealing and functional home furnishings for living spaces has grown significantly. Rising disposable incomes and expanding middle-class populations, particularly in emerging economies such as India, China, and Indonesia, are enabling consumers to invest in better-quality bedding, towels, and decorative fabrics. In developed markets, shifting lifestyle preferences and the increased amount of time spent at home post-pandemic have also strengthened the focus on comfort and home ambience. Together, these trends are fueling steady growth in both basic household textile demand and premium, design-oriented segments.

MARKET RESTRAINTS

Fluctuating Raw Material Prices Continue to Restrict Market Expansion

The volatile prices of key raw materials such as cotton, polyester, and other fibers create a significant challenge for market growth. These materials account for a major portion of production costs, sudden fluctuations driven by unpredictable weather patterns, supply chain disruptions, and changes in global trade policies for textile imports. It can directly impact manufacturers’ margins. Smaller producers, in particular, face difficulties maintaining price competitiveness and profitability, which can slow investment and innovation within the sector.

- For instance, in Q1 (quarter ending June 2024), Trident Ltd. reported a 21% drop in net profit compared to the same quarter a year ago. Although their revenue rose by 17%, the cost of raw materials (especially cotton) increased by nearly 18%, squeezing margins.

MARKET OPPORTUNITIES

Sustainable & Circular Textiles as a Differentiator to Create Lucrative Growth Opportunities

Consumers’ rising demand for eco-friendly, recycled, and circular textile products creates a growth avenue for brands that adopt sustainable fabrics and closed-loop systems. For instance, according to the Textile Exchange’s 2024 Materials Market Report, recycled polyester and mechanically recycled cotton witnessed year-on-year growth of over 20% in production volume, outpacing virgin fiber growth rates. This indicates rising supply and adoption in the industry, implying that home textile brands using recycled/sustainable blends can capture premium margins and marketing differentiation.

HOME TEXTILES MARKET TRENDS

Rising Influence of E-Commerce and Direct-to-Consumer Channels to Shape Market Trends

The growing penetration of online retail platforms is reshaping how consumer demands for home textiles are met, with digital sales becoming a major growth avenue across both developed and emerging markets. According to the U.S. Census Bureau, e-commerce platforms accounted for 15.9% of total retail sales in 2024, up from 14.7% in 2023. This reflects the steady migration of consumer spending toward digital channels. It has significantly benefited home-textile brands and manufacturers, enabling them to bypass traditional retail markups, personalize product offerings, and reach wider audiences through data-driven marketing. As consumers increasingly prefer online discovery and home delivery for bedding, towels, and décor items, companies investing in robust e-commerce ecosystems and omni-channel strategies are positioned to capture long-term growth.

Download Free sample to learn more about this report.

Home Textiles Market Segmentation Analysis

By Material

Synthetic Fibers Dominate Owing to Cost Efficiency and Functional Versatility

On the basis of material, the market is segmented into synthetic fibers and natural fibers.

To know how our report can help streamline your business, Speak to Analyst

The synthetic fibers segment holds a dominant share of the market, accounting for roughly 57.75% of total material use in 2026. This growth is driven by the cost-effectiveness, durability, and performance advantages of synthetic materials such as polyester and nylon, which offer wrinkle resistance, ease of maintenance, and color retention compared to natural fibers. Additionally, advancements in recycled and eco-friendly synthetic fabrics have further strengthened their adoption, allowing manufacturers to balance affordability with sustainability goals. This key factor sustains their market leadership.

The natural fibers segment is projected to expand at a CAGR of 6.15% over the projected years.

By Product

Essential Utility and High Replacement Demand to Contribute to Bedroom Linen Segment

By product, the market is categorized into bathroom linen, bedroom linen, carpets & floor coverings, curtains and drapes, and others.

The bedroom linen segment dominates the home textiles market with a share of 31.06% in 2026, accounting for the majority of sales across essential bedding items, including bed sheets, pillowcases, quilts, and duvet covers. Its dominance stems from the universal necessity and frequent replacement cycle of these products as well as continuous innovation in fabric quality, design, and comfort. Rising consumer spending on premium and wellness-oriented bedding, including organic cotton, temperature-regulating, and hypoallergenic materials, further reinforces this segment’s leadership in the home textiles sector.

The bathroom linen segment is expected to grow at a CAGR of 6.58% over the forecast period.

By Fabric Type

Structural Versatility and Established Supply Chains to Support Growth of Woven Fabric Segment

Based on fabric type, the market is bifurcated into woven and non-woven.

The woven fabric segment accounts for the largest home textiles market share of 83.43% in 2026, as these materials provide the strength, durability, drape, and aesthetic flexibility needed for core household uses such as bedding, curtains, and upholstery. Additionally, woven fabrics enable a wide range of patterns, textures, and finishes, supporting both functional and premium aesthetic requirements, which further reinforces their dominance over nonwoven alternatives. Their established supply chains and finishing infrastructure also favor their continued dominance.

The non-woven segment is expected to grow at the fastest CAGR over the forecast period. They are being increasingly used in holstery, mattress covers, curtains, and table linens as they combine versatility, durability, along with low production cost.

By Distribution Channel

Broader Brand Assortments and Personalized Shopping Experience to Drive Specialty Stores Segmental Growth

Based on distribution channel, the market is segmented into supermarkets/hypermarkets, specialty stores, online, and others.

In 2025, the global market was dominated by specialty stores, as consumers increasingly seek curated selections, expert guidance, and premium-quality products tailored to their specific lifestyle or décor needs. These stores focus on brand-driven assortments and personalized shopping experiences, allowing customers to explore diverse textures, fabric types, and design trends firsthand. Their ability to offer exclusive collections, customization options, and design consultancy positions them as preferred destinations for discerning buyers, fueling faster growth compared to mass retail channels. Furthermore, the segment is estimated to have touched a 44.41% share in 2026.

In addition, the online channel is the fastest-growing and is projected to grow at a CAGR of 6.38% during the study period.

Home Textiles Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Home Textiles Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

Asia Pacific accounted for USD 102.03 Billion in 2025, representing 44.17% of the global market share, and is projected to reach USD 109.17 Billion in 2026. Growth of the region is attributed to rapid urbanization, rising disposable incomes, and strong manufacturing capabilities in countries such as China, India, and Pakistan. The region benefits from abundant raw material availability, cost-efficient labor, and a growing middle-class population investing in home décor and comfort. For instance, UN Comtrade data (2023) shows that China, India, and Pakistan together accounted for over 70% of global home-textile exports, underscoring Asia-Pacific’s dominant role in both production and consumption growth.

In 2025, the China market is estimated to have reached USD 34.93 billion, & indian market reached USD 31.55 billion

North America and Europe

Other regions, such as North America and European markets, are anticipated to witness steady growth in the coming years. During the forecast period, the North America market generated USD 59.57 billion in 2025, representing 25.79% of the global market landscape, and is expected to reach USD 62.63 billion in 2026. The region’s growth is fueled by high consumer spending on home décor, increasing demand for premium and sustainable products, and a strong e-commerce presence.

Europe contributed 21.12% to the global market in 2025, with a valuation of USD 48.79 billion, and is projected to reach USD 58.14 billion in 2026. In this region, Germany and the U.K. are estimated to have reached USD 11.01 billion and 9.65 billion, respectively, in 2025. The regional market growth is driven by a strong preference for high-quality, sustainable, and design-oriented products, supported by consumers’ focus on home aesthetics and comfort. The growing demand for eco-certified and organic fabrics, particularly under EU sustainability directives, encourages innovation in textile sourcing and production. Additionally, the presence of established brands and a robust hospitality sector fuels consistent demand. According to Eurostat, the household expenditure on furnishings and home textiles accounts for nearly 5% of total consumer spending across the EU, reflecting steady market momentum.

South America and the Middle East and Africa

Over the forecast period, the South America and Middle East and Africa regions are expected to witness significant growth in this market. South America maintained a strong presence in the global market, reaching USD 14.16 Billion in 2025, accounting for a 6.13% share, and is expected to reach USD 14.96 Billion in 2026. Rising urbanization, expanding middle-class incomes, and growing investments in real estate and home décor across countries such as Brazil, Argentina, and Chile drive South America’s market growth.

In 2025, Middle East & Africa held 2.79% of the global market, reaching a valuation of USD 6.44 billion, and is projected to grow to USD 6.87 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Intensifying Competition Drives Innovation and Strategic Partnerships in the Market

The global home textiles market is moderately fragmented, featuring a mix of vertically integrated manufacturers, global retail brands, and emerging online players that compete on the basis of cost, design, and sustainability. Key players such as Welspun India, Trident Group, Indo Count Industries, Springs Global, and IKEA are focusing on strategies such as vertical integration to control raw material supply and improve their margins. Further, sustainability initiatives, including the use of organic, recycled, and traceable materials, align with consumer and regulatory demands. Players are also emphasizing product innovation and premiumization, developing performance and design-led fabrics to attract modern consumers, while expanding omni-channel and Direct-to-Consumer (D2C) models to strengthen market presence. Additionally, partnerships with major retailers, adoption of digital supply chain systems, and agile sourcing strategies are enabling companies to remain competitive amid fluctuating costs and evolving lifestyle trends

LIST OF KEY HOME TEXTILES COMPANIES PROFILED

- Hanesbrands Inc. (U.S.)

- IKEA (Netherlands)

- WestPoint Home LLC (U.S.)

- Ralph Lauren Corporation (U.S.)

- Macy’s, Inc. (U.S.)

- Mohawk Industries, Inc. (U.S.)

- Springs Global Participações S.A. (Brazil)

- Indo Count Industries Ltd. (India)

- Trident Group (India)

- Welspun India Ltd. (India)

KEY INDUSTRY DEVELOPMENTS

- October 2025: Christian Fischbacher Bed & Bath AG, a Switzerland-based brand known for its luxurious textiles, announced updates to its bed & bath product lines, emphasizing sustainable textile manufacturing practices. The company introduced new material sourcing protocols and revised production processes to overcome ongoing environmental concerns in the luxury textile sector.

- September 2025: Luxury bedding and home brand Boll & Branch launched a curated collection via partnership with e-commerce registry/marketplace Over The Moon, targeting life milestones and registry buyers.

- June 2025: At NeoCon 2025, textile brands unveiled several standout innovations, including Hyphyn, a biodegradable performance vinyl engineered to break down over 90% within two years without leaching harmful chemicals, offering a sustainable alternative to traditional vinyl. This launch underscores the growing industry focus on eco-performance materials that combine durability with environmental responsibility.

- April 2025: Polyvlies USA, a nonwoven textile firm operating in Winston-Salem, is undertaking a major expansion by purchasing a greenfield site in Union Cross Business Park, committing USD 31 million in capital investment over five years and creating 28 new jobs to support growing North American demand. This move underscores the company’s confidence in local infrastructure, workforce, and market potential, bolstered by regional and state incentives.

- March 2025: Cathay Home Inc., a vertically integrated manufacturer and distributor of premium home textile products, is advancing its market position by executing strategic acquisitions of product and manufacturing assets. In addition, the company launched a new production facility to expand capacity and better serve its brand portfolio and customers. This move underscores its commitment to vertical growth, improved control over sourcing, and faster delivery to market, strengthening its competitive edge in the home textiles sector.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.55% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Material

By Product

By Fabric Type

By Distribution Channel

By Geography North America (By Material, Product, Fabric Type, Distribution Channel, and Country)

Europe (By Material, Product, Fabric Type, Distribution Channel, and Country/Sub-region)

Asia Pacific (By Material, Product, Fabric Type, Distribution Channel, and Country/Sub-region)

South America (By Material, Product, Fabric Type, Distribution Channel, and Country/Sub-region)

Middle East & Africa (By Material, Product, Fabric Type, Distribution Channel, and Country/Sub-region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 230.99 billion in 2025 and is projected to reach USD 471.90 billion by 2034.

In 2025, the market value stood at USD 102.03 billion.

The market is expected to exhibit a CAGR of 8.55% during the forecast period of 2025-2032.

The synthetic fiber is the leading segment in the market by material.

The key factors driving the market growth are rising urbanization, increasing household incomes, home décor trends, and the expansion of e-commerce.

Welspun India Ltd., Springs Global, Trident Group, Indo Count Industries Ltd., Mohawk Industries, Ralph Lauren Home, IKEA, and Bed Bath & Beyond are some of the prominent players in the market.

Asia Pacific dominated the market in 2025.

Growing demand for eco-friendly, recycled, and circular textile products creating a growth avenue for brands that adopt sustainable fabrics and closed-loop systems are expected to favor the product adoption.

- 2021-2034

- 2025

- 2021-2024

- 267

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us