Hybrid Excavators Market Size, Share & Industry Analysis, By Type (Crawler Hybrid Excavators and Wheeled Hybrid Excavators), By Operating Weight (Below 20 Tons, 20–40 Tons, and Above 40 Tons), By Engine Power (Below 100 HP, 100–200 HP, 200–300 HP, and Above 300 HP), By End-User (Construction Contractors, Mining Operators, Government & Infrastructure Agencies, Utility & Energy Companies, and Others (Defense Engineering, Forestry Operations, etc.)), and Regional Forecast, 2026–2034

Hybrid Excavators Market Size and Future Outlook

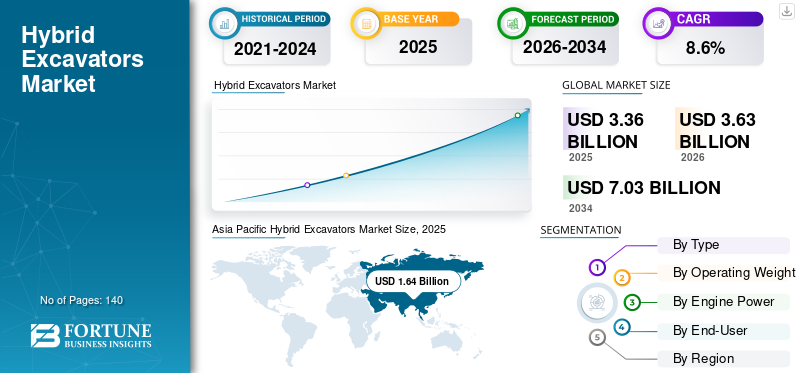

The global hybrid excavators market size was valued at USD 3.36 billion in 2025. The market is projected to grow from USD 3.63 billion in 2026 to USD 7.03 billion by 2034, exhibiting a CAGR of 8.6% during the forecast period. Asia Pacific dominated the hybrid excavators market with a market share of 48.81% in 2025.

Hybrid excavators are advanced construction equipment that combine conventional hydraulic systems with energy recovery and electric assist technologies to improve fuel efficiency and reduce emissions during operations. The market is witnessing steady growth driven by increasing infrastructure development, rising fuel costs, and growing emphasis on sustainable construction practices across key regions, including Asia Pacific and Europe. These machines are widely used across construction and mining sites to optimize fuel consumption while maintaining operational performance in residential, commercial, and large-scale infrastructure projects. They play a critical role in enhancing equipment efficiency, reducing operating costs, and supporting compliance with stringent emission regulations.

Current market trends indicate rising adoption of energy recovery systems such as swing and boom regeneration technologies, enabling improved energy utilization during repetitive duty cycles. Contractors are increasingly focusing on lowering total cost of ownership, improving machine productivity, and aligning with environmental targets. Additionally, the gradual shift toward electrification in construction equipment is further supporting the adoption of the product as a transitional solution. From a regional analysis perspective, growth is supported by infrastructure investments and regulatory frameworks promoting low-emission equipment, while the competitive landscape of key players continues to influence market penetration across various segments.

- For instance, in November 2025, Komatsu Ltd. unveiled its next-generation hybrid excavator lineup at a BAUMA 2026 preview event, featuring advanced energy recovery systems and improved battery capacity designed to enhance fuel efficiency and reduce emissions in mid- to large-sized construction End-Users.

Komatsu Ltd., Caterpillar Inc., Volvo Construction Equipment, Hitachi Construction Machinery Co., Ltd., and Kobelco Construction Machinery Co., Ltd. are among the key players holding a significant share in the market. Their competitive positioning is strengthened by strong expertise in hydraulic and hybrid technologies, the ability to deliver fuel-efficient and End-User-specific equipment solutions, extensive global distribution and aftersales service networks, and continuous innovation in energy recovery systems and low-emission machinery to meet evolving construction and sustainability requirements.

Download Free sample to learn more about this report.

Global Hybrid Excavators Market KEY TAKEAWAYS

- 2025 Market Size: USD 3.36 billion

- 2026 Market Size: USD 3.63 billion

- 2034 Forecast Market Size: USD 7.03 billion

- CAGR: 8.6% from 2026–2034

- Asia Pacific dominated the global market with a 48.81% share in 2025 and a market value of USD 1.64 billion.

- The crawler hybrid excavators segment held the largest market share, driven by high digging force.

- The 20–40 tons segment held the largest market share, supported by its balance of power.

North America

The market was valued at USD 0.60 billion in 2025, supported by construction.

Europe

The market is witnessing growth driven by sustainability initiatives, emission regulations.

Asia Pacific

The region dominated the market with a value of USD 1.64 billion in 2025.

U.S.

The market is estimated to reach USD 0.50 billion in 2026.

Japan

The market is estimated to reach USD 0.30 billion in 2026, accounting for approximately 8.3% of global sales.

Read More

HYBRID EXCAVATORS MARKET TRENDS

Increasing Focus on Reducing Fuel Consumption is Boosting Product Demand

Demand for hybrid excavators is increasingly being influenced by the growing need to reduce fuel consumption and optimize operating costs across construction and infrastructure projects. Contractors are placing greater emphasis on improving equipment efficiency, as high fuel usage and extended machine operating hours significantly impact overall project economics. This is driving the product adoption equipped with energy recovery systems and electric assist technologies that enhance fuel efficiency without compromising performance. The variability in duty cycles, including repetitive swing operations and load handling, is encouraging the use of machines capable of recovering and reusing energy during operations. Additionally, operators are prioritizing equipment that can deliver consistent performance across varying site conditions while maintaining lower emissions. Instead of highly complex automation, there is a growing preference for practical efficiency-enhancing features such as optimized power distribution, intelligent engine control, and basic energy monitoring systems that improve operational productivity without increasing system complexity.

- For instance, in February 2025, Volvo Construction Equipment highlighted its ongoing strategy to improve fuel efficiency and reduce emissions across its excavator portfolio, including hybrid solutions such as the EC300E Hybrid, emphasizing energy recovery from boom-down motion to enhance operational efficiency in construction operations.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growing Focus On Improving Fuel Efficiency to Drive Market Growth

The market is witnessing steady growth as construction and infrastructure development activities increasingly focus on improving fuel efficiency, reducing emissions, and accelerating project timelines. Sectors such as road construction, urban infrastructure, mining, and large-scale earthworks are prioritizing equipment that can deliver high performance while minimizing operating costs. The increasing complexity of construction projects, including continuous excavation cycles, material handling, and high-duty operations, is driving the need for advanced excavators capable of optimizing energy usage across different working conditions. Hybrid excavators, equipped with energy recovery systems and electric assist technologies, enable contractors to reduce fuel consumption while maintaining productivity, particularly in repetitive operations such as swing and load cycles. The growing emphasis on lowering total cost of ownership and improving machine utilization is encouraging the adoption of fuel-efficient equipment that can operate reliably under high workloads. As infrastructure investments continue to rise, particularly in developing economies, there is increasing demand for machines that combine performance with sustainability. Equipment manufacturers are responding by enhancing hybrid excavator capabilities through improved energy management systems, optimized hydraulic performance, and better integration of electric components, enabling contractors to achieve higher productivity and operational efficiency across diverse construction operations.

- For instance, in June 2025, Hitachi Construction Machinery Co., Ltd. emphasized the development of energy-efficient excavator technologies, including hybrid and electrified solutions, as part of its mid-term management strategy aimed at reducing environmental impact and improving fuel efficiency in construction operations.

MARKET RESTRAINTS

High Initial Cost and Limited Adoption across Price-Sensitive Markets Continue to Limit Market Growth

The adoption of hybrid excavators is constrained by their higher upfront cost compared to conventional diesel-powered machines, which can be a significant barrier, particularly for small and mid-sized contractors. Hybrid systems involve additional components such as electric motors, energy storage devices, and advanced control systems, increasing the overall equipment cost and complexity. While these machines offer long-term fuel savings and operational efficiency, the return on investment is highly dependent on machine utilization rates, making them less attractive for projects with lower operating hours. In many developing regions, where cost sensitivity remains high, contractors often prioritize lower initial investment over lifecycle cost benefits, limiting the penetration of hybrid technologies. Additionally, the maintenance and servicing of hybrid systems require specialized knowledge and technical expertise, leading to concerns regarding downtime and serviceability, further impacting adoption.

MARKET OPPORTUNITIES

Increasing Shift toward Low-Emission Construction Equipment Creating Growth Opportunities

An emerging opportunity in the market is the increasing shift toward low-emission and fuel-efficient construction equipment across developed and emerging economies. While infrastructure expansion remains a key growth driver, a significant portion of investments is now being aligned with sustainability goals, including reducing carbon emissions and improving energy efficiency in construction operations. Hybrid excavators offer a practical transition between conventional diesel-powered machines and fully electric equipment, enabling contractors to reduce fuel consumption without compromising operational performance. These machines are particularly beneficial in urban infrastructure projects and regulated environments where emission standards are becoming more stringent. Additionally, the growing focus on lifecycle cost optimization is encouraging fleet operators to adopt hybrid solutions that provide long-term savings through reduced fuel usage and improved machine efficiency. The ability of the product to deliver consistent performance across repetitive duty cycles, such as material handling and excavation in confined job sites, further strengthens their adoption across diverse sectors.

- For instance, in March 2025, Caterpillar Inc. highlighted its ongoing development of fuel-efficient and low-emission excavator technologies, including hybrid solutions. These advancements as part of the company’s strategy to support sustainable construction practices and reduce operating costs across infrastructure projects.

MARKET CHALLENGES

Limited Awareness and Uncertain Return on Investment Continue to Impact Product Adoption

A key challenge in the hybrid excavators market growth is the limited awareness and uncertainty surrounding return on investment among end-users, particularly in developing and price-sensitive markets. While such products offer clear advantages in terms of fuel savings and reduced emissions, their higher initial cost and relatively longer payback period can discourage adoption among small and mid-sized contractors. The benefits of hybrid systems are most evident in high-utilization application, such as continuous excavation and material handling, but may not be fully realized in projects with lower machine operating hours. Additionally, the lack of standardized performance benchmarks and limited field-level data on long-term cost savings creates hesitation among buyers when evaluating hybrid technology. Operational factors, including varying duty cycles and site conditions, can further impact efficiency gains, making it difficult for contractors to accurately assess potential savings. This uncertainty, combined with the need for trained operators and specialized service support for hybrid systems, continues to influence purchasing decisions and slows the widespread adoption of the product across global markets.

Segmentation Analysis

By Type

Crawler Hybrid Excavators Segment Led due to their Load-Bearing Capability

By type, the market is segmented into crawler hybrid excavators and wheeled hybrid excavators.

Crawler hybrid excavators held the largest market share as they are extensively deployed across major end-users such as infrastructure development, mining operations, and large-scale construction projects, where stability, higher digging force, and efficient operation on uneven terrain are critical. These machines are equipped with tracked undercarriages that provide superior traction and load-bearing capability, making them highly suitable for heavy-duty operations and challenging ground conditions. Additionally, hybrid crawler excavators benefit significantly from energy recovery systems during repetitive swing and digging cycles, enhancing fuel efficiency and reducing operational costs. Their ability to deliver consistent performance across diverse operations further strengthens their dominance in the market.

- For instance, in March 2024, Volvo Construction Equipment highlighted the performance of its EC300E Hybrid excavator, featuring boom-down energy recovery technology designed to improve fuel efficiency and reduce emissions in heavy-duty construction applications.

The wheeled hybrid excavators segment is projected to expand at a CAGR of 7.3% during the study period. The growth of this segment is driven by increasing demand for equipment suited to urban construction, roadwork, and municipal infrastructure projects where Engine Power and ease of movement between job sites are essential. Wheeled excavators offer advantages such as faster travel speed, reduced ground damage, and improved operational flexibility, making them highly suitable for end-users operating in developed urban environments.

To know how our report can help streamline your business, Speak to Analyst

By Operating Weight

20–40 Tons Segment Led Owing to its Operational Flexibility

By operating weight, the market is segmented into below 20 tons, 20-40 tons, and above 40 tons.

The 20-40 tons segment held the largest market share as they are extensively deployed across a wide range of operations such as road construction, urban infrastructure development, and general construction activities. This segment offers an optimal balance between power, fuel efficiency, and operational flexibility, making it the preferred choice for contractors handling medium to large-scale projects. Hybrid systems are most effectively utilized in this category due to the high frequency of repetitive operations such as swinging and loading, where energy recovery technologies can significantly improve fuel efficiency.

The above 40 tons segment is projected to expand at a CAGR of 8.3%. The growth of this segment is driven by increasing demand from mining and large-scale infrastructure projects that require high-capacity equipment capable of handling intensive excavation and material movement tasks. Hybrid technology in this segment is gaining traction as operators seek to reduce fuel consumption and improve efficiency in high-duty cycle operations.

By Engine Power

100–200 HP Segment Led due to their Widespread Usage in Mid-Sized Construction and Infrastructure Projects

By engine power, the market is segmented into below 100 HP, 100–200 HP, 200–300 HP, and above 300 HP.

The 100–200 HP segment held the largest hybrid excavators market share, driven by their extensive use in mid-sized construction and infrastructure projects such as urban development, road construction, and utility works. This power range offers an optimal balance between fuel efficiency, operational capability, and cost-effectiveness, making it the preferred choice for contractors handling diverse operations. Hybrid systems are most effectively utilized in this segment due to frequent load cycles and swing operations, where energy recovery technologies can significantly enhance fuel efficiency. Additionally, machines within this range provide sufficient power for general excavation tasks while maintaining lower operating costs, further supporting their widespread adoption.

The 200–300 HP segment is projected to expand at a CAGR of 8.5% during the forecast period. The growth of this segment is driven by increasing demand for higher-capacity machines in large-scale infrastructure and mining projects, where greater digging force and productivity are required. Hybrid technology in this category is gaining traction as operators seek to improve fuel efficiency in high-duty cycle operations while maintaining performance.

By End-User

Construction Contractors Segment Dominated due to the Growing Need for Faster Project Execution

By end-user, the market is segmented into construction contractors, mining operators, government & infrastructure agencies, utility & energy companies, and others (defense engineering, forestry operations, etc.).

Construction contractors held the largest share of the market, driven by their extensive involvement across a wide range of construction activities such as residential, commercial, and large-scale infrastructure development. Hybrid excavators are widely deployed by contractors for excavation, material handling, trenching, and site preparation tasks, where improving fuel efficiency and reducing operating costs are key priorities. The increasing scale and complexity of urban construction projects, along with the need for faster project execution, is encouraging contractors to adopt equipment that can deliver consistent performance while optimizing energy usage.

Government & infrastructure agencies are projected to expand at a CAGR of 8.7% during the forecast period. The growth of this segment is driven by rising public investments in infrastructure development, including transportation networks, urban infrastructure, and large-scale public works projects.

Hybrid Excavators Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, South America, and the Middle East & Africa.

North America

Asia Pacific Hybrid Excavators Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market accounted for USD 0.60 billion in revenue in 2025, supported by strong demand across construction, infrastructure rehabilitation, and urban development activities in the U.S., Canada, and Mexico. Regional demand is closely linked to increasing investments in highway modernization, bridge repair, and large-scale infrastructure projects, along with a growing focus on improving operational efficiency and reducing fuel consumption. Contractors are increasingly deploying hybrid excavators to optimize performance in high-duty cycle operations, particularly in excavation, material handling, and site preparation.

U.S. Hybrid Excavators Market

The U.S. is expected to dominate the market with an estimated revenue of about USD 0.50 billion in 2026, driven by its extensive infrastructure network, aging public assets, and continuous investments in transportation and urban development projects. Unlike many regions, U.S.-based contractors place strong emphasis on improving equipment efficiency and reducing total cost of ownership. The country is witnessing significant investments in road rehabilitation, highway expansion, and urban infrastructure upgrades, which are increasing the demand for advanced excavation equipment capable of delivering high productivity with lower fuel consumption.

Europe

The European market is driven by a strong focus on sustainability, emission reduction, and advanced construction practices across key economies such as Germany, the U.K., France, Italy, and the Netherlands. Demand for the product is closely linked to the region’s stringent environmental regulations and the increasing adoption of low-emission construction equipment. Contractors and project developers are prioritizing machines that offer improved fuel efficiency, reduced carbon emissions, and optimized energy usage without compromising performance. The growing emphasis on green construction and regulatory compliance is encouraging the adoption of the product, particularly in urban infrastructure projects and environmentally sensitive areas where emission control is a critical requirement.

U.K. Hybrid Excavators Market

The U.K. market is estimated to reach around USD 0.11 billion in 2026, representing roughly 3.1% of global sales.

Germany Hybrid Excavators Market

Germany’s market is projected to reach approximately USD 0.19 billion in 2026, equivalent to around 5.1% of global sales.

Asia Pacific

Asia Pacific remains the fastest-growing market, generating revenue of USD 1.64 billion in 2025 globally. The region continues to dominate the market, driven by rapid urbanization, large-scale infrastructure development, and expanding construction and mining activities across key economies such as China, India, Japan, and Southeast Asian countries. The region’s growth is primarily supported by increasing government investments in transportation infrastructure, including highways, rail corridors, smart cities, and urban development projects.

China Hybrid Excavators Market

China’s market is projected to remain the dominant in the Asia Pacific region, with 2026 revenues estimated to reach around USD 0.68 billion, representing roughly 18.9% of global sales.

Japan Hybrid Excavators Market

The Japanese market is estimated to reach around USD 0.30 billion by 2026, accounting for roughly 8.3% of the global sales.

India Hybrid Excavators Market

The Indian market is estimated to reach around USD 0.26 billion by 2026, accounting for roughly 7.2% of global sales.

Middle East & Africa

The Middle East & Africa market is driven by increasing investments in large-scale infrastructure, urban expansion, and energy projects across GCC countries, South Africa, Israel, and North Africa. Demand for the product is linked to the region’s focus on improving construction efficiency and supporting economic diversification. Governments are prioritizing highways, smart cities, industrial zones, and logistics corridors, which require efficient excavation and material handling. GCC countries are investing heavily in mega projects, creating demand for high-capacity excavators in challenging environments. South Africa’s demand is supported by mining and infrastructure activities, while North Africa is witnessing growth in transportation and urban development. Product adoption remains gradual but is increasing as contractors focus on fuel efficiency and operational optimization.

GCC Hybrid Excavators Market

The GCC market is projected to reach around USD 0.12 billion by 2026, representing roughly 3.2% of the global sales.

South America

The South America market is driven by increasing infrastructure development, improving road connectivity, and gradual adoption of advanced construction equipment across key economies such as Brazil, Argentina, and Chile. Demand for the product is supported by expanding construction activities, urban development, and strong mining operations across the region. Contractors are increasingly adopting hybrid excavators to improve fuel efficiency and optimize performance in high-duty cycle end-users such as excavation and material handling. The need to reduce operating costs and enhance equipment productivity is further supporting the adoption of hybrid technologies across infrastructure and mining projects.

Brazil Hybrid Excavators Market

The Brazil market is projected to reach around USD 0.13 billion by 2026, representing roughly 3.4% of the global sales.

COMPETITIVE LANDSCAPE

Key Industry Players

Major Players Emphasis on Technological Capabilities to Deliver High-Performance Excavation Equipment

The market is moderately consolidated, with competitive positioning driven by technological capabilities, fuel efficiency, and the ability to deliver high-performance excavation equipment across diverse end-users such as construction, infrastructure development, mining, and urban projects. Leading players such as Komatsu Ltd., Caterpillar Inc., Volvo Construction Equipment, Hitachi Construction Machinery Co., Ltd., and Kobelco Construction Machinery Co., Ltd. maintain strong market positions by offering advanced hybrid excavators designed to improve fuel efficiency, reduce emissions, and enhance productivity in high-duty cycle operations.

Competitive differentiation is increasingly shaped by the ability to develop energy-efficient machines equipped with advanced energy recovery systems, optimized hydraulic performance, and intelligent control technologies. As contractors focus on reducing operating costs, improving machine utilization, and meeting sustainability targets, market players are investing in hybrid solutions that deliver measurable fuel savings and consistent performance across demanding construction environments.

- For instance, in March 2025, Volvo Construction Equipment highlighted its ongoing transition toward low-emission machinery, including hybrid excavator technologies, as part of its sustainable product development strategy.

LIST OF KEY HYBRID EXCAVATORS COMPANIES PROFILED

- Komatsu Ltd. (Japan)

- Caterpillar Inc. (U.S.)

- Volvo Construction Equipment (Sweden)

- Hitachi Construction Machinery Co., Ltd. (Japan)

- Kobelco Construction Machinery Co., Ltd. (Japan)

- Doosan Bobcat Inc. (South Korea)

- Hyundai Construction Equipment Co., Ltd. (South Korea)

- JCB Ltd. (U.K.)

- CASE Construction Equipment (U.S.)

- Liebherr Group (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Komatsu Ltd. renewed its CSR collaboration agreement with Cummins Inc., focusing on joint community initiatives and supporting technical education in local communities.

- March 2026: Komatsu Ltd., through its subsidiary Komatsu Forest AB, acquired Malwa Forest AB to strengthen its forestry machinery portfolio and expand operational capabilities.

- February 2026: Caterpillar Inc. acquired RPMGlobal Holdings Limited, expanding its portfolio of data-driven mining technologies and software solutions for improved operational efficiency.

- January 2026: Volvo Construction Equipment launched three next-generation compact excavators, including the ECR90, EC65, and EW65, focusing on productivity, operator comfort, and total cost of ownership.

- February 2025: JCB Ltd. launched the NXT series excavators in Nepal, including the NXT 221 LC Fuel Master and NXT 225 LCM, designed for improved fuel efficiency and reduced maintenance costs.

REPORT COVERAGE

The global hybrid excavators market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments and prevalence by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Operating Weight, Engine Power, End-User, and Region |

| By Type |

|

| By Operating Weight |

|

| By Engine Power |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.36 billion in 2026 and is projected to reach USD 7.03 billion by 2034.

In 2025, the North America’s market value stood at USD 0.60 billion.

The market is expected to exhibit a CAGR of 8.6% during the forecast period (2026-2034).

By end-user, the construction contractors segment led the market.

Rising focus on improving fuel efficiency is the key factor driving the market.

Komatsu Ltd., Caterpillar Inc., Volvo Construction Equipment, and Hitachi Construction Machinery Co., Ltd. are the top players in the market.

Asia Pacific dominates the market in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us