Hybrid Operating Room Market Size, Share & Industry Analysis By Component (Imaging Systems [CT Scanners, MRI, Ultrasound and Others], Operating Room Fixtures [Operating Tables, Operating Room Lights, Radiation Shields and Others], Surgical Instruments & Tools and Others), By Application (Cardiovascular Surgery, Orthopedic & Trauma Surgery, Neurosurgical Surgery, General Surgery, and Others), By End User (Hospitals & ASCs, and Specialty Clinics), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

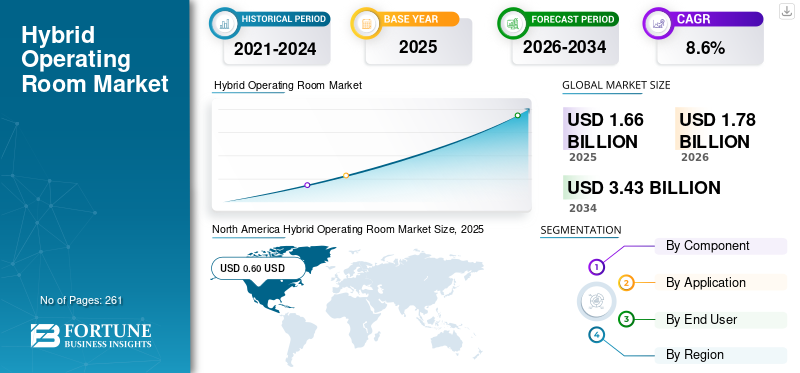

The global hybrid operating room market size was valued at USD 1.66 billion in 2025 and is projected to grow from USD 1.78 billion in 2026 to USD 3.43 billion by 2034, exhibiting a CAGR of 8.6% during the forecast period. North America dominated the global hybrid operating room market with a market share of 36.1% in 2025.

A hybrid operating room is an advanced surgical suite that integrates a traditional operating room with an image-guided interventional suite. The increasing prevalence of chronic conditions, including neurological conditions, cardiovascular conditions, and others, is resulting in a growing number of surgeries among the patient population. The growing surgical procedures and technological advancements in imaging and surgical navigation systems are further driving the adoption of hybrid operating rooms, thereby contributing to the growth of the market.

- For instance, according to the 2024 data published by the Centers for Disease Control & Prevention (CDC), about 1 in 20 adults aged 20 and older has coronary artery disease in the U.S.

Additionally, the increasing preference towards minimally invasive treatment approaches is also a vital factor contributing to the growing demand for these surgical procedures in the hybrid ORs in the market. Hospitals and specialty centers are investing in hybrid OR infrastructure to expand their procedure capabilities, attract referrals, and improve efficiency. This, coupled with the increasing focus on acquisitions and mergers among key players, is driving the focus of major companies, including Siemens Healthineers AG, GE Healthcare, Koninklijke Philips N.V., and others, and is expected to support the global hybrid operating room market.

Download Free sample to learn more about this report.

Hybrid Operating Room Market Key Takeaways

- 2025 Market Size: USD 1.66 billion

- 2026 Market Size: USD 1.78 billion

- 2034 Forecast Market Size: USD 3.43 billion

- CAGR: 8.6% from 2026–2034

- North America dominated the hybrid operating room market with a 36.1% share in 2025.

- The cardiovascular surgery segment accounted for 45.1% of the market share in 2025.

- The hospitals and ASCs segment is projected to hold 89.3% of the market share in 2026.

North America

North America led the global market in 2025 with a valuation of USD 0.60 billion.

Europe

Europe is projected to reach USD 0.54 billion in 2026.

Asia Pacific

Asia Pacific is expected to reach USD 0.46 billion in 2026.

U.S.

The U.S. hybrid operating room market is estimated to reach USD 0.53 billion in 2025.

Japan

Rising adoption of innovative technologies and increasing focus on healthcare modernization are driving market demand.

Read More

Hybrid Operating Room Market Trends

Technological Advancements in these Devices to Boost Product Demand

There is an increasing focus on the integration of artificial intelligence, robotic-assisted technologies, and real-time data analytics in these imaging solutions. Technological advancements, including digitalized surgical guidance, predictive analytics, and AI-driven imaging analytics, among others, reduce intraoperative errors and improve surgical precision.

The integration of automated systems, real-time analytics, robotics, and other features in these suites has improved clinical outcomes and accuracy, and efficiency in these surgical procedures. This, along with the growing focus of key players on R&D activities to develop and introduce technologically advanced devices such as digital and interconnected surgical ecosystems and advanced operation tables, is anticipated to fuel the adoption rate for these surgical environments in the market.

- In December 2024, Fraunhofer IPA developed high-tech hybrid operating rooms that harness the power of 5G and AI to unlock whole new applications.

Other Prominent Trends

- Growth of multidisciplinary care models involving surgeons, interventional radiologists, and cardiologists in a single OR.

- Rising demand for flexible, modular hybrid OR designs that can support multiple specialties and procedure types.

- Focus on infection control, ergonomics, and workflow optimization in hybrid OR planning and design.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Prevalence of Chronic Health Conditions to Drive Market Growth

The increasing prevalence of chronic conditions, including neurological, cardiovascular, and orthopedic conditions, among others, is contributing to the growing demand for hybrid operating room imaging solutions and procedures among the patient population. As a result, the penetration rate of these products in the market is being boosted.

For instance, according to 2021 data published by the American Heart Association (AHA), about 8.5 million adults are suffering from peripheral artery disease.

Moreover, the increasing demand for minimally invasive procedures is resulting in the growing investment in hybrid ORs, further supporting the rising adoption of these surgical environments worldwide. Therefore, the factors above, along with the increasing focus of key players on developing and introducing novel imaging solutions for these settings, are expected to drive the adoption rate, thereby contributing to the global hybrid operating room market size.

Other Prominent Drivers

- Investments by hospitals and health systems to differentiate on quality, safety, and advanced clinical capabilities

- Supportive clinical guidelines and evidence emphasizing the benefits of image-guided and hybrid procedures

Market Restraints

High Cost Associated with Hybrid Operating Room to Limit the Market Growth

There is a growing demand for hybrid ORs owing to their advantages, such as advanced imaging, among others. However, the high cost associated with these surgical environments is expected to hamper the penetration rate for these systems, particularly in developing markets, including China, Brazil, and others.

The high capital cost associated with designing, installment, and maintenance of hybrid operating rooms represents a huge financial barrier, particularly for emerging nations. Furthermore, the establishment of a hybrid OR requires advanced imaging equipment, extensive structural modifications, which is an expensive and complex process, and makes it challenging for small and mid-sized hospitals in emerging countries.

- For instance, according to 2024 data published by SKYTRON LLC, it was reported that the establishment of a modern surgical suite costs about USD 5.0 million.

Market Opportunities

Increasing Emphasis on Upgrading Surgical Infrastructure Leads to Lucrative Market Opportunities

There is an increasing emphasis on developing surgical infrastructure, creating a lucrative opportunity for the hybrid operating room market growth. Healthcare facilities are prioritizing advanced and digitally integrated surgical environments with an aim to cater to the growing demand for minimally invasive procedures to improve patient safety and enhance workflow efficiency.

Additionally, many healthcare systems are replacing traditional surgical suites and upgrading them with hybrid ORs, which have enhanced procedural throughput among patients. This, along with, growing focus of key players towards integration of robotic-assisted surgical systems in these suites, is expected to drive the adoption rate for these systems in the market.

- In October 2024, Jeroen Bosch Hospital opened a new hybrid operating room in the Netherlands.

Market Challenges

Limited Healthcare Access in Developing Nations to Limit the Market Growth

There is an increasing demand for minimally invasive procedures among the patient population. However, shortage of technologically advanced devices, limited healthcare expenditure, coupled with inadequate reimbursement policies, especially in emerging countries, are resulting in limited access to healthcare facilities among the patient population.

Furthermore, a limited number of clinical facilities and limited specialist surgeons, delayed procurement cycles, pressure on hospital budgets, space constraints in existing hospital infrastructure, among others, are some of the crucial factors, resulting in the delayed surgical procedures among patients, especially in emerging countries, including Mexico, Brazil, among others.

- For instance, according to 2023 data published by The World Bank Group, it was reported that about 4.5 billion people lack full access to essential health services.

Other Prominent Challenges

- Complex coordination between multiple vendors, clinical teams, and hospital departments during project design and implementation.

SEGMENTATION ANALYSIS

By Component

Growing Prevalence of Chronic Conditions to Drive Imaging Systems Segment Dominance

Based on component, the market is classified into imaging systems, operating room fixtures, surgical instruments & tools, and others. Imaging systems are further bifurcated into CT scanners, MRI, ultrasound, and others. Additionally, operating room fixtures are further divided into operating tables, operating room lights, radiation shields, and others.

To know how our report can help streamline your business, Speak to Analyst

The imaging systems segment held the largest market share in 2025. The growth is due to the growing prevalence of chronic conditions, such as neurological disorders, and others, resulting in a growing demand for the establishment of innovative surgical suites worldwide. This, along with the growing focus of prominent players towards R&D activities to launch innovative imaging systems, is further expected to support the segmental growth.

- In December 2025, Koninklijke Philips N.V., launched LumiGuide integrated with Philips’ Azurion platform with an aim to strengthen its product portfolio.

The operating room fixtures segment is expected to grow at a CAGR of 8.0% over the forecast period.

By Application

Increasing Prevalence of Cardiovascular Diseases Led to the Cardiovascular Surgery Dominance

Based on application, the market is segmented into cardiovascular surgery, orthopedic & trauma surgery, neurological surgery, general surgery, and others.

The cardiovascular surgery segment accounted for the largest share in the global market in 2025. By application, the cardiovascular surgery segment held a share of 45.1% in 2025. The growth is primarily owing to the increasing prevalence of cardiovascular diseases is resulting in an increasing number of cardiovascular surgical procedures among the patient population in the market.

- For instance, according to the 2025 data published by the National Institute of Child Health and Human Development (NIH), about 795,000 people have strokes each year in the U.S.

The segment of neurological surgery is set to flourish with a growth rate of 8.9% across the forecast period.

By End-user

Growing Number of Hospitals & ASCs Led to the Segment’s Dominance

Based on end user, the market includes hospitals & ASCs, and specialty clinics.

The hospitals and ASCs segment dominated the market in 2025. The increasing prevalence of chronic conditions and the increasing number of hospitals are some of the crucial factors contributing to the growth of the segment in the market. Furthermore, the segment is set to hold an 89.3% share in 2026.

- For instance, according to 2025 data published by the American Hospital Association, there are about 6,093 hospitals in the U.S.

Additionally, specialty clinics’ end users are projected to grow at a CAGR of 9.5% during the study period.

Hybrid Operating Room Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Hybrid Operating Room Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America hybrid operating room market held the dominant share in 2024, valued at USD 0.56 billion, and also took the leading share in 2025 with USD 0.60 billion. The dominance of the region is owing to certain factors, such as the advanced healthcare infrastructure, high procedure volumes, and strong adoption of minimally invasive and image-guided techniques. Increasing hospitals' focus on cardiovascular, neurovascular, and complex oncology applications, supported by favorable clinical guidelines and the presence of major technology providers, is further supporting the growth of the region in the market. In 2025, the U.S. market is estimated to reach USD 0.53 billion.

- For instance, according to 2024 statistics published by the Alzheimer’s Association, it was reported that about 7 million people are living with Alzheimer disease in the U.S.

Europe & Asia Pacific

Other regions, such as Europe and the Asia Pacific, are expected to witness considerable growth in the forecast period. During the study period, the European region is projected to record a growth rate of 6.7% and reach the valuation of USD 0.54 billion in 2026. This is due to the strong uptake of hybrid ORs, particularly in countries with well-established cardiac and vascular care networks. Investments are focused on comprehensive heart centers, stroke units, and academic hospitals. Moreover, the adoption of advanced imaging technologies in hybrid ORs, emphasis on clinical outcomes, safety, and standardized care pathways, and other factors are supporting the growth of the market in the region. Backed by these factors, countries such as the U.K. are expected to record the valuation of USD 0.08 billion, Germany to record USD 0.11 billion, and France to record USD 0.07 billion in 2026. After Europe, the market in the Asia Pacific is estimated to reach USD 0.46 billion in 2026 and secure the position of the third-largest region in the market. In the region, India is estimated to reach USD 0.04 billion while China is estimated to reach USD 0.15 billion in 2026. An increasing number of large tertiary hospitals and private hospital groups investing in advanced surgical infrastructure, growing cardiovascular disease burden, expanding middle-class populations, and growing medical tourism are key factors driving hybrid OR projects in countries such as China, India, Japan, South Korea, and Australia.

Latin America and Middle East & Africa

Over the forecast period, the Latin America and Middle East & Africa regions are expected to witness moderate growth in this market. The Latin America market in 2026 is set to record USD 0.07 billion as its valuation. The growing hybrid OR installations concentrated in major urban hospitals and private centers, economic conditions, capital availability, demand for hybrid operation rooms, and uneven healthcare infrastructure influence the pace of adoption. In the Middle East and Africa, GCC is set to attain the value of USD 0.03 billion in 2025. In the Middle East and parts of Africa, hybrid OR adoption is supported by investments in flagship hospitals, specialized cardiac centers, and medical tourism hubs, particularly in Gulf Cooperation Council (GCC) countries.

Competitive Landscape

Key Industry Players

Increasing Focus on Partnerships Among the Prominent Companies to Support Their Dominance

A robust and diversified product portfolio of advanced imaging systems, along with a strong geographic presence, is a vital factor supporting the dominance of these players in the market. Siemens Healthineers AG, GE Healthcare, and Koninklijke Philips N.V., are prominent companies in the market in 2025. Furthermore, the increasing focus of prominent players on acquisitions and partnerships among other players is likely to support the global hybrid operating room market share.

- For instance, in April 2024, Koninklijke Philips N.V., partnered with the Dutch Franciscus Gasthuis & Vlietland hospital to open two hybrid operating rooms to enhance patient care.

Other key players, including Getinge, and others, are also growing in the market, primarily due to their growing emphasis on R&D activities to develop and launch advanced products to strengthen their presence in the market.

List of Key Hybrid Operating Room Companies Profiled

- Koninklijke Philips N.V. (Netherlands)

- Getinge (Sweden)

- Siemens Healthineers AG (Germany)

- GE Healthcare (U.S.)

- STERIS (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- MIZUHO Corporation (Japan)

- Stryker (U.S.)

- Olympus Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS

- December 2025 – The government of Tamil Nadu has inaugurated an integrated government sector hybrid neurosurgery operating theatre at Kilpauk Medical College Hospital (KMCH to enable minimally invasive brain procedures in India.

- September 2025 – The Saint John Regional Hospital launched a hybrid operating room with an aim to strengthen its presence in Canada.

- June 2025 – Northwestern Medicine Palos Hospital launched a hybrid vascular operating room with an aim to expand advanced surgical care in the South Suburbs.

- February 2025 – Texas Health Hospital Mansfield opened a new hybrid operating room with the aim of providing innovative services to its patient population.

- October 2024 – St. Michael’s Hospital opened a state-of-the-art hybrid biplane operating room for advanced neurovascular procedures. This helped the hospital to increase its brand presence.

REPORT COVERAGE

The hybrid operating room market report provides a detailed global analysis and focuses on key aspects such as leading companies, component, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.6% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component, Application, End User, and Region |

|

By Component |

· Imaging Systems o CT Scanners o MRI o Ultrasound o Others · Operating Room Fixtures o Operating Tables o Operating Room Lights o Radiation Shields o Others · Surgical Instruments & Tools · Others |

|

By Application |

· Cardiovascular Surgery · Orthopedic & Trauma Surgery · Neurosurgical Surgery · General Surgery · Others |

|

By End User |

· Hospitals & ASCs · Specialty Clinics |

|

By Region |

· North America (By Component, By Application, By End User, and by Country) o U.S. (By Application) o Canada (By Application) · Europe (By Component, By Application, By End User, and by Country/Sub-region) o U.K. (By Application) o Germany (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Scandinavia (By Application) o Rest of Europe (By Application) · Asia Pacific (By Component, By Application, By End User, and by Country/Sub-region) o China (By Application) o Japan (By Application) o India (By Application) o Australia (By Application) o Southeast Asia (By Application) o Rest of Asia Pacific (By Application) · Latin America (By Component, By Application, By End User, and by Country/Sub-region) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) · Middle East & Africa (By Component, By Application, By End User, and by Country/Sub-region) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 1.66 billion in 2025 and is projected to reach USD 3.43 billion by 2034.

In 2025, the North America regional market value stood at USD 0.60 billion.

Growing at a CAGR of 8.6%, the market will exhibit steady growth over the forecast period (2026-2034).

By component, the imaging systems segment is the leading segment in this market.

The introduction of novel hybrid operating rooms is one of the major factors driving the markets growth.

GE Healthcare and Koninklijke Philips N.V., are the major players in the global market.

North America dominated the market share in 2025.

The growing prevalence of chronic conditions, the increasing number of product launches, among others, are some of the vital factors expected to boost the adoption of these products worldwide.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us