Hybrid Video Surveillance Market Size, Share & Industry Analysis, By System type (Analog-IP Integrated Surveillance Systems, Edge-to-Cloud Hybrid Surveillance Systems, and Others), By Component (Hardware, Software, and Services), By Deployment mode (On-Premise, Cloud-Managed Hybrid, Edge + On-Premise Hybrid, and Others), By Application (Perimeter Security, Indoor Facility Monitoring, Public Area Surveillance, and Others), By End User (Commercial Enterprises, Industrial & Logistics, Government & Civic Institutions, and Others), and Regional Forecast, 2026-2034

Hybrid Video Surveillance Market Size and Future Outlook

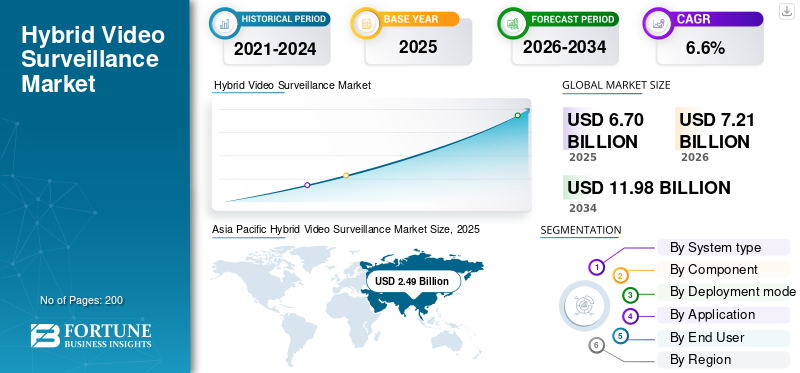

The global hybrid video surveillance market size was valued at USD 6.70 billion in 2025. The market is projected to grow from USD 7.21 billion in 2026 to USD 11.98 billion by 2034, exhibiting a CAGR of 6.6% during the forecast period. Asia Pacific dominated the hybrid video surveillance market with a market share of 37.16% in 2025.

Hybrid video surveillance refers to a security system architecture that combines legacy analog infrastructure with newer IP-based cameras, software, and networked management tools in one operating environment. The market is driven by the cost effectiveness, a flexible and scalable upgrade path, better image quality, stronger data storage efficiency, and broader access to analytics and remote monitoring. The model is important for organizations that want practical modernization rather than a full rip-and-replace program, including public facilities, commercial estates, and small and medium sized enterprises looking for reliable security solutions that can still evolve with future technological advancements.

Key player in the hybrid video surveillance industry are Hikvision, Dahua Technology, Axis Communications, and Milestone Systems are driving the market forward by making the switch from analog to IP easier and smarter. Hikvision promotes DVRs with strong hybrid access. Dahua Technology supports both analog and IP inputs with its XVR platforms. Axis allows for step-by-step migration using video encoders. Milestone is improving its software offerings with VMS, analytics, and VSaaS. These advancements are taking hybrid surveillance beyond basic monitoring to more intelligent and connected setups.

Download Free sample to learn more about this report.

HYBRID VIDEO SURVEILLANCE MARKET TRENDS

Edge-To-Cloud Integration is Making Hybrid Surveillance More Software-Led and Scalable

Major trend in the global market is the shift from simple analog-to-IP migration to more connected, software-driven architectures. Hybrid systems are not used to keep old cameras and cables anymore, they are now being made to connect old infrastructure with cloud-managed video, centralized monitoring, analytics, and remote alarm handling. Resulting the market is moving toward more flexible and scalable deployments, so users can modernize in phases, keep existing assets in service, and still build a path toward stronger operational intelligence. Axis’ encoder portfolio reflects this phased analog-to-IP transition model, while Milestone’s recent releases show hybrid environments are being tied more tightly to cloud and analytics layers.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Phased Analog-to-IP Modernization is Driving Demand for Hybrid Surveillance Systems

Key driver in the global hybrid video surveillance market growth is the need to modernize large installed surveillance estates without forcing a full rip-and-replace cycle. Many end users still operate analog cameras, coaxial cabling, and legacy recording assets that remain functional, so hybrid architecture offers a more practical route to upgrade performance, improve storage efficiency, add analytics, and strengthen remote monitoring while controlling capex. In turn, hybrid systems continue to gain traction as a flexible and scalable upgrade path across transport, public infrastructure, commercial buildings, and multi-site facilities.

MARKET RESTRAINTS

Data Privacy and Compliance Burdens are Restraining Wider Adoption of Advanced Hybrid Surveillance Deployments

Major restraint in the global market is the compliance burden tied to video data collection, retention, access control, and analytics use. Additionally, the hybrid systems add cloud-managed workflows, cross-site monitoring, AI-enabled analysis, or biometric-linked functions on top of legacy infrastructure. Buyers are adopting a more measured approach to security procurement, recognizing that modern solutions require navigation of complex GDPR, strict data governance, and higher audit risks related to video storage and sharing. That leads to lengthen decision cycles and raise deployment complexity, especially in public-facing and multi-location environments.

MARKET OPPORTUNITIES

Smart City and Command-Center Modernization is Opening a Long-Cycle Retrofit Opportunity for Hybrid Surveillance Vendors

Main opportunity in this market is the expansion of smart city initiatives and public-infrastructure surveillance programs, especially in areas authorities want broader coverage, centralized monitoring, and better incident response without replacing every installed camera in one step. That plays directly to hybrid video surveillance, as it allows older field infrastructure to be linked with newer VMS platforms, analytics, storage, and control-center workflows over multiple budget cycles. As cities increase their use of traffic cameras and other smart technologies in transportation and law enforcement, the opportunity extends well beyond hardware into software integration, analytics overlays, and lifecycle services.

MARKET CHALLENGES

Cybersecurity Exposure Across Mixed Legacy and IP Environments is Challenging Hybrid Surveillance Adoption

Major challenge in the global market is cybersecurity hardening across mixed analog-to-IP environments. Hybrid systems are valuable as they let users modernize in phases, but this flexibility can create a broader attack surface across legacy cameras, encoders, recorders, VMS layers, storage, and remote access links. Many operators not just evaluate performance and cost, they also deal with patching gaps, credential risks, network segregation, and the difficulty of securing older infrastructure inside a more connected architecture. That raises deployment complexity, mainly in public infrastructure, transport, industrial, and multi-site environments.

Impact of Russia-Ukraine War

Russia-Ukraine War is Accelerating Demand for Border, Infrastructure, and Cyber-Resilient Surveillance Upgrades

The Russia-Ukraine war has strengthened the business for hybrid video surveillance by increased investment in video surveillance, pushing governments and operators to upgrade monitoring around borders, transport assets, energy sites, logistics corridors, and other critical infrastructure. The hybrid systems are growing as they let users reinforce coverage faster by connecting existing analog estates with newer IP, storage, and monitoring layers instead of waiting for a full rip-and-replace cycle. The war has also raised the cybersecurity bar for surveillance networks, making resilient architectures, camera hardening, and tighter system control more important than before.

In May 2025, the U.K.’s National Cyber Security Centre, alongside international partners, disclosed that Russia’s GRU had targeted organizations involved in support to Ukraine and had also targeted internet-connected cameras at Ukrainian border crossings and near military installations to monitor aid shipments.

Segmentation Analysis

By System type

Due to Large Installed Analog Base and Lower-Cost Phased Migration Path, Analog-IP Integrated Surveillance Systems Segment Dominated Market

In terms of system type, the market is categorized into analog-IP integrated surveillance systems, edge-to-cloud hybrid surveillance systems, and multi-site hybrid surveillance systems.

Analog-IP integrated surveillance systems segment held the largest hybrid video surveillance market share in 2025, as they solve the most common buyer problem in hybrid surveillance, to modernize without replacing every working camera, recorder, and cable at once. This architecture lets end users keep legacy analog CCTV assets in service while adding IP functionality, better image quality, centralized recording, and gradual software-led upgrades. That makes it the most commercial option across transport, commercial buildings, industrial sites, and public facilities where budget discipline and operational continuity is important than a full rip-and-replace approach.

In February 2024, TransPennine Trains Limited published the contract award notice for its Video Surveillance System (VSS/CCTV) Renewal, covering the supply and installation of video surveillance devices.

Edge-to-cloud hybrid surveillance systems segment is expected to grow at a CAGR of 12.1% over the forecast period.

By Component

Due to Installed-Device-Heavy Nature of Hybrid Architectures, Hardware Dominated Market

On the basis of component, the market is classified into hardware (cameras, recorders, connectivity, storage devices, and others), software (video management software (VMS) and video analytics software), and services (professional services and lifecycle services).

Hardware segment led the market in 2025, as these deployments begin with physical infrastructure consisting of cameras, recorders, connectivity, storage devices, and others. In brownfield upgrades, buyers usually preserve or restore field devices first, then layer software and services on top. As a result, hardware remains the largest segment in this market, mainly in areas where analog cameras and coaxial cabling are still in use and migration occurs in phases.

Software segment is expected to show the fastest growth, registering a CAGR of 10.7% over the forecast period.

By Deployment mode

Due to Stronger Local Control, Legacy-System Compatibility, and Data-Retention Requirements, On-Premise Segment Dominated Market

By deployment mode, the market is segmented into on-premise, cloud-managed hybrid, edge + on-premise hybrid, and edge + cloud hybrid.

On-premise deployment led the market in 2025, as key upgrades still center on local recording, site-level control, and direct integration with existing cameras, encoders, and network infrastructure. Many end users are more comfortable keeping video feeds, storage, and system management within their own facilities, especially in transport, public-sector, industrial, and multi-site environments where uptime, latency, cybersecurity, and retention control matter. That makes on-premise architecture the most commercially recognized format in hybrid surveillance, while cloud-linked models continue to grow from a smaller base.

Cloud-managed hybrid is the fastest growing segment and is expected to grow at a CAGR of 11.7% across the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Need to Detect Intrusion Early and Secure Site Boundaries Perimeter Security Segment Dominated Market

Based on application, the market is segmented into perimeter security, indoor facility monitoring, public area surveillance, critical infrastructure monitoring, traffic and transportation monitoring, retail and commercial loss prevention, and others.

Perimeter security led the market in 2025, as it serves as the outermost layer of defense, protecting the site before deeper coverage is needed. In real deployments, buyers first focus on fences, gates, access roads, external approaches, yards, and other exposed boundary areas where early detection, visual verification, and incident response is important. That makes perimeter applications important across airports, utilities, industrial facilities, logistics sites, public campuses, and other security-sensitive environments where hybrid systems are used to upgrade surveillance in phases by keeping legacy infrastructure in service.

In May 2024, the U.S. Department of Veterans Affairs revised its Physical Security and Resiliency Design Manual, stating that perimeter barriers must help identify intentional trespassers and support campus or facility security operations, and that P/T/Z cameras must be used for all site perimeter and exterior building areas.

Traffic and transportation monitoring is the fastest growing segment in market and is expected to grow at a CAGR of 7.9% during the forecast period.

By End User

Due to Broad Installed Base Across Retail, BFSI, Offices, and Hospitality, Commercial Enterprises Segment Dominated Market

Based on end user, the market is segmented into commercial enterprises, industrial & logistics, government & civic institutions, critical infrastructure operators, defense & homeland security, and residential & community estates.

Commercial enterprises segment led the market in 2025, as they represent the widest concentration of everyday surveillance demand across branch networks, office buildings, retail outlets, hotels, and other customer-facing properties. These users need continuous monitoring for loss prevention, employee and visitor safety, access control, and business continuity, but they also tend to modernize in phases rather than replace all infrastructure at once. That makes hybrid surveillance mainly attractive in this segment, as it supports gradual analog-to-IP upgrades across large multi-site estates by also keeping capex under control.

In May 2024, State Bank of India issued an e-tender for the supply, installation, testing, commissioning, and maintenance of CCTV systems, including maintenance of existing CCTV systems, at branches, offices, and cells under its Administrative Office in Mohali, Punjab.

Critical infrastructure operators segment is expected to show the fastest market growth, registering a CAGR of 8.3% over the forecast period.

Hybrid Video Surveillance Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and rest of the world.

Asia Pacific

Asia Pacific Hybrid Video Surveillance Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominates the global market, and is anticipated to grow at a CAGR of 6.4% over the forecast period. The dominance is owing to the region combining three powerful demand drivers, a very large legacy camera base, sustained public and commercial surveillance expansion, and stronger preference for phased modernization instead of full rip-and-replace projects. Many users across transport, industrial sites, campuses, retail networks, and urban monitoring programs rely on analog infrastructure, but they increasingly want IP-level image quality, centralized monitoring, analytics, and better data storage efficiency. That makes hybrid architecture mainly attractive across the region, as it offers a more flexible and scalable path to market expansion while keeping upgrade costs manageable.

China Hybrid Video Surveillance Market

The Chinese market revenues stood at around USD 0.93 billion in 2025, representing roughly 37.43% of the global sales.

Japan Hybrid Video Surveillance Market

The Japanese market stood at around USD 2.22 billion in 2025, accounting for roughly 20.21% of Asia Pacific revenues.

North America

North America holds the significant market share for hybrid video surveillance solutions, and is anticipated to grow at a CAGR of 5.9% during the forecast period, due to the wide existing infrastructure of traditional video surveillance systems within business organizations, transportation systems, industrial plants, educational institutions, and public places. The need for new products within this region is more oriented toward the process of modernizing the current systems than introducing new systems, implying that the buyers want efficient mechanisms for integrating their traditional systems with IP cameras, central management, cloud-based supervision, and analytics tools. The U.S. hybrid video surveillance market is experiencing robust growth as organizations bridge legacy analog systems with modern IP technology.

U.S. Hybrid Video Surveillance Market

Based on the strong contribution of North America to the market and the dominance of U.S. within the region, the U.S. market stood at around USD 1.41 billion in 2025, growing at a CAGR of 5.7% during the forecast period.

Europe

Europe held around 25.73% share of global market in 2025. The presence of a large number of companies across the region have retained Europe position in the market and prefer an incremental approach to development rather than a comprehensive overhaul. Significant demand generated by commercial organizations, governmental bodies, transport infrastructure, industrial organizations, and critical infrastructure, which are looking for improvements in surveillance capabilities, increased efficiency in data handling, and streamlined security activities. Regulatory expectations, including the General Data Protection Regulation (GDPR) in Europe, are shaping operators design storage, access control, and video processing workflows in hybrid deployments.

France Hybrid Video Surveillance Market

France market reached approximately USD 0.21 billion in 2025, equivalent to around 12.47% of Europe revenues.

U.K. Hybrid Video Surveillance Market

The U.K. market stood at around USD 0.24 billion in 2025, representing roughly 14.04% of Europe revenues.

Rest of the World

Rest of the World (Middle East & Africa and Latin America) holds a comparatively smaller market share but is expected to grow at a highest CAGR of 8.6% during the forecast period. The market is driven by upgrades, enhanced public safety needs, commercial security expansion, and infrastructure-led surveillance deployment across transport hubs, utilities, campuses, municipal environments, and secure facilities.

Latin America Hybrid Video Surveillance Market

The market in Latin America reached around USD 0.38 billion in 2025, accounting for roughly 43.04% of revenues.

Middle East & Africa Hybrid Video Surveillance Market

The Middle East & Africa market stood at around USD 0.50 billion in 2025 and is expected to reach USD 1.10 billion in 2034, representing roughly 56.96% sales in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Scale-Led Asian Manufacturers and Software-Centric Enterprise Specialists are Defining Competitive Landscape

The competitive landscape in hybrid video surveillance is expanding across key markets and led by companies that can serve both ends of the market, a high-volume hardware migration and higher-value software integration. Hikvision and Dahua Technology remain mainly influential on the device and recorder side since their portfolios are built around large installed bases, broad channel reach, and practical analog-to-IP transition paths. Hikvision operates an AIoT ecosystem with 30,000+ products, while Dahua continues to position itself as a video-centric AIoT provider and its XVR platform is designed to record HDCVI, AHD, TVI, CVBS, and IP feeds simultaneously, these flexibility keeps these firms strong in brownfield hybrid upgrades.

At the same time, competition is shifting beyond cameras and recorders toward ownership of the software, analytics, and cloud-control layer. Axis Communications, Motorola Solutions, Milestone Systems, and Canon’s network camera business are driving that side of the market. Axis still promotes encoders as a way to move from analog to IP at your own pace, Canon said network cameras helped drive record 2025 sales, Motorola expanded Avigilon Alta and Avigilon Unity with new emergency-response features in March 2025, and Milestone grew 2025 net revenue by 10% to USD 343.86 million and reinvesting heavily in analytics, responsible artificial intelligence and machine learning, and cloud technology. The market is no longer being shaped only by hardware scale, it is increasingly being shaped by who can connect hybrid estates to stronger VMS, artificial intelligence and machine learning, and cloud-led workflows.

LIST OF KEY HYBRID VIDEO SURVEILLANCE COMPANIES PROFILED IN REPORT

- Hangzhou Hikvision Digital Technology Co., Ltd. (China)

- Zhejiang Dahua Technology Co., Ltd. (China)

- Axis Communications AB (Sweden)

- Motorola Solutions, Inc. (U.S.)

- Canon Inc. (Japan)

- Hanwha Vision Co., Ltd. (South Korea)

- Milestone Systems A/S (Denmark)

- Genetec Inc. (Canada)

- Bosch Security Systems B.V. (Netherlands)

- i-PRO Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- November 2025: The London Borough of Croydon published its CCTV Upgrade contract award worth USD 3.45 million for the replacement and upgrade of the existing CCTV control room, public space cameras, transmission equipment, and maintenance services.

- August 2025: Huntingdonshire District Council published its CCTV Shared Service Control Room Upgrade award worth of USD 307,234.0 to DSSL Group, covering Veracity Viewscape v11 VMS, Windows 11-compatible hardware, migration of configurations, and operator training.

- July 2025: Leeds City Council published a preliminary market engagement notice for a framework covering electronic security equipment, including CCTV cameras, DVRs, NVRs, VMS, accessories, and related security hardware. The estimated framework is valued at USD 4.02 million.

- July 2025: Stoke-on-Trent City Council published a transparency notice for the supply and maintenance of static surveillance cameras to support enforcement on key bus corridors, with integration into existing software.

- April 2025: West Lothian Council published its Security CCTV & Fire Alarm Systems TMC notice for maintenance, installation, monitoring, and repair of council protection systems. The estimated contract value was USD 3.18 million.

- March 2025: Southend City Council published its contract award notice for Provision of CCTV Maintenance Services, covering repair and maintenance of the CCTV control room and borough-wide systems, plus equipment supply and installation.

- February 2025: Kent County Council published a modification notice extending its Supply of CCTV and Access Solutions framework by 6 months while a new framework was being resolved.

- February 2025: Kent County Council published the new Y24007 Supply of CCTV, Access Solutions & Security Services framework notice. The framework was split into three lots, and Lot 1 - CCTV, Security & Access Solutions was estimated at USD 31.56 million.

REPORT COVERAGE

The global hybrid video surveillance market analysis provides an in-depth study of market size, company profiling & forecast by all the market segments included in the report. It includes details on the market dynamics and trends that are expected to drive the market during the forecast period. It offers information on the technological advances, new product launches, key industry experts’ developments, and details on strategic partnerships, mergers & acquisitions. The research report also encompasses detailed competitive landscape with information on the market share and profiles of market key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.6% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation

|

By System type

|

|

By Component

|

|

|

By Deployment mode

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value will capture USD 7.21 billion in 2026 and is projected to reach USD 11.98 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 2.49 billion.

The market is expected to exhibit a CAGR of 6.6% during the forecast period.

Analog-IP integrated surveillance systems segment led the market by system type.

Phased analog-to-IP modernization is driving demand for hybrid surveillance systems.

Top players in the market include Hikvision, Dahua Technology, Axis Communications, Motorola Solutions, Hanwha Vision, Milestone Systems, Canon, and Genetec.

Asia Pacific held the largest share of the market.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us